Market Definition

The Global Autonomous Energy Management Systems Market encompasses the development, deployment, integration, and operation of software platforms, hardware controllers, artificial intelligence engines, and digital management architectures that autonomously monitor, optimise, control, and dispatch energy generation, storage, consumption, and trading assets across residential, commercial, industrial, and utility-scale applications with minimal or no continuous human intervention, replacing conventional rule-based energy management approaches with machine learning-driven decision frameworks that adapt continuously to changing energy prices, grid conditions, weather forecasts, occupancy patterns, equipment states, and regulatory constraints to maximise energy cost savings, carbon emission reductions, asset utilisation, and grid service revenue. Autonomous energy management systems integrate and coordinate distributed energy resources including solar photovoltaic generation, battery energy storage, electric vehicle charging infrastructure, heat pumps, flexible industrial loads, diesel and gas backup generation, and grid connection points within a unified optimisation framework whose autonomous decision-making capability extends from real-time millisecond-scale power balancing through intraday energy dispatch scheduling to multi-day and seasonal planning horizons whose complexity and data volume exceed the capacity of human operators working with conventional monitoring and manual control approaches. The market encompasses building energy management systems incorporating artificial intelligence-driven heating, ventilation, and air conditioning optimisation, lighting control, and plug load management; industrial energy management systems coordinating compressed air, steam, refrigeration, and motor drive loads with production schedules and energy tariff structures; microgrid energy management systems autonomously balancing island and grid-connected operation; virtual power plant aggregation platforms orchestrating portfolios of distributed energy resources for wholesale market participation; and enterprise energy management platforms consolidating multi-site energy procurement, sustainability reporting, and decarbonisation program management within integrated digital environments. Key participants include industrial automation and building technology companies, energy management software specialists, artificial intelligence and analytics platform developers, utility and grid technology providers, distributed energy resource aggregators, and the commercial, industrial, and utility operators whose energy cost, carbon, and grid service objectives define the demand landscape for autonomous energy management technology globally.

Market Insights

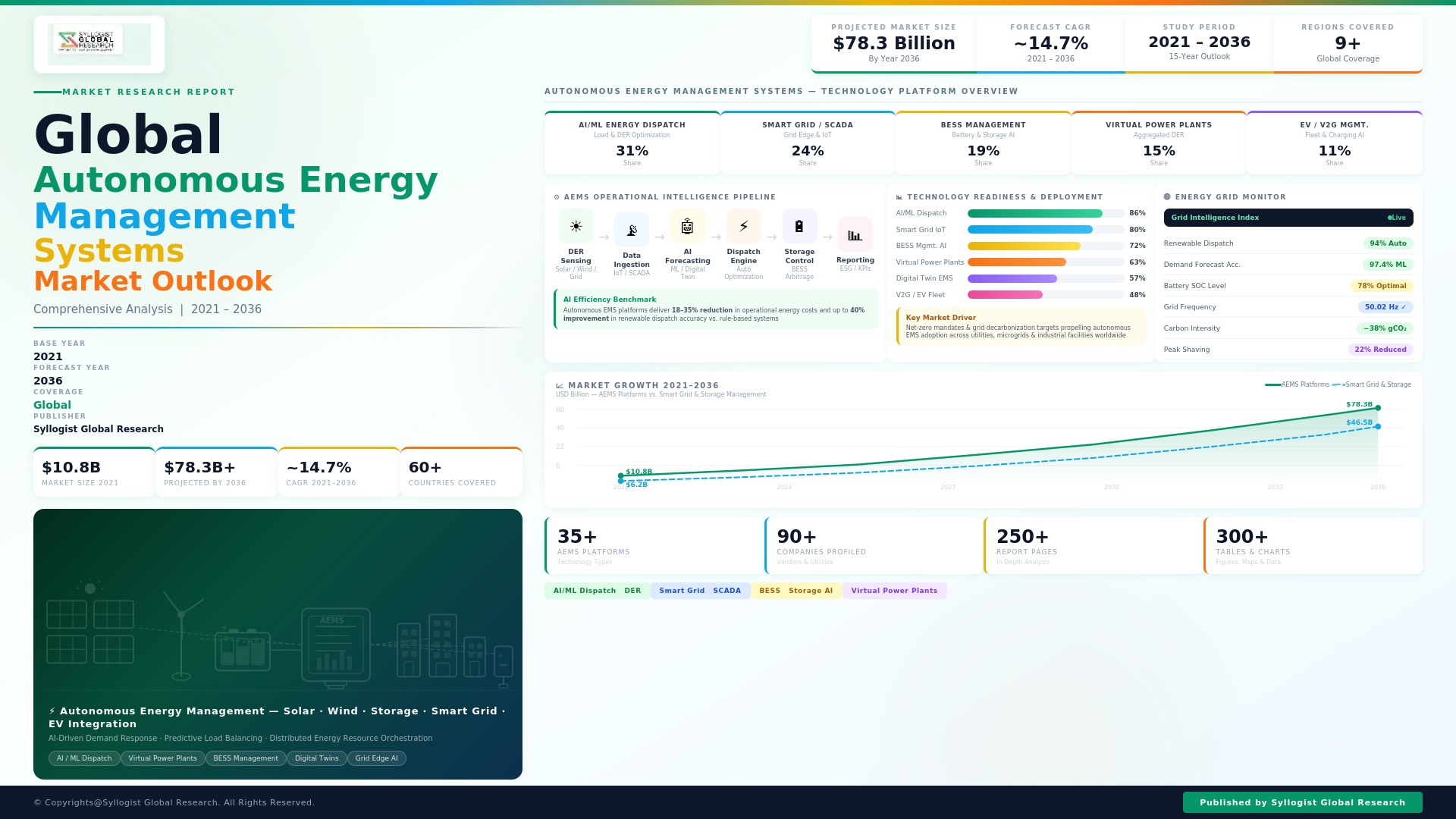

The global autonomous energy management systems market was valued at approximately USD 5.2 billion in 2025 and is projected to reach USD 18.6 billion by 2034, advancing at a compound annual growth rate of 15.2% over the forecast period from 2027 to 2034, driven by the accelerating deployment of distributed energy resources that create operational complexity beyond the capability of conventional rule-based energy management, the expanding economic value of energy flexibility in electricity markets experiencing increasing price volatility from variable renewable energy penetration, and the growing carbon accounting and decarbonisation program management requirements of corporate sustainability commitments that require autonomous energy optimisation capability to achieve measurable scope one and scope two emission reduction outcomes within operational energy cost constraints. The fundamental market driver is the structural transformation of the energy system from centralised, dispatchable, and predictable to distributed, variable, and complex, creating a management challenge whose optimal solution requires the continuous multi-variable optimisation capability that autonomous artificial intelligence-driven systems provide and that human-operated manual or rule-based management approaches cannot deliver at the decision speed, consistency, and data integration depth required for maximum economic and environmental performance.

The commercial and industrial building sector represents the largest current application segment for autonomous energy management systems, accounting for approximately 42% of global market revenue in 2025, driven by the substantial energy cost reduction potential achievable through autonomous heating, ventilation, and air conditioning scheduling optimisation, demand charge management, solar and storage dispatch coordination, and electric vehicle charging load shifting in commercial facilities whose complex occupancy patterns, multiple energy tariff exposure, and growing on-site distributed energy resource portfolios create optimisation opportunities that autonomous systems realise more completely and consistently than manual or schedule-based management. Advanced autonomous building energy management systems incorporating occupancy prediction models, weather forecast integration, real-time electricity price signal response, and multi-asset coordinated dispatch are generating documented energy cost reductions of 15% to 28% and demand charge savings of 20% to 35% relative to conventional building automation system baselines at commercial office, retail, and hospitality facilities where comprehensive sensor coverage and distributed energy resource integration enable the system to exercise full optimisation authority across all controllable loads and generation assets. Industrial energy management represents the highest average revenue per deployment segment within the market, with autonomous energy management systems at energy-intensive manufacturing facilities including aluminium smelters, cement plants, chemical complexes, and steel mills commanding system investment values of USD 2 million to USD 12 million per site due to the scale of energy assets being optimised, the complexity of production-energy interdependency modelling required for autonomous scheduling, and the magnitude of energy cost savings whose 10% to 20% reduction at facilities spending USD 30 million to USD 200 million annually on energy generates return on investment within 12 to 36 months.

The utility and grid services application segment is the fastest-growing market category for autonomous energy management systems, advancing at approximately 19.4% annually, driven by the proliferation of virtual power plant programs and demand response aggregation schemes whose commercial viability requires autonomous real-time control of distributed energy resource portfolios that cannot be operated at grid service response speeds and consistency requirements through manual or operator-directed dispatch processes, and by the growing commercial value of frequency regulation, spinning reserve, and distribution network congestion management services in electricity markets where the increasing penetration of variable renewable generation is escalating the frequency and magnitude of grid balancing events that create revenue opportunities for rapidly dispatchable distributed energy resource portfolios. Europe leads global virtual power plant development with regulatory frameworks in Germany, the United Kingdom, the Netherlands, and the Nordic countries that provide market access for distributed energy resource aggregators at balancing mechanism and frequency regulation markets whose revenue potential of EUR 80,000 to EUR 250,000 per megawatt per year for frequency containment reserve provision creates compelling economics for autonomous energy management investment by residential battery owners, commercial solar plus storage operators, and industrial flexible load participants who access grid service markets through virtual power plant aggregation platforms. Asia-Pacific is the fastest-growing regional market at approximately 17.8% annually, driven by Japan’s demand response aggregation program regulatory framework established in 2022, Australia’s virtual power plant market expansion under the National Electricity Market rule changes enabling distributed energy resource participation in frequency and contingency services, South Korea’s demand response program expansion, and China’s provincial electricity market reform programs that are progressively enabling demand-side and distributed generation participation in wholesale and ancillary service markets.

Artificial intelligence capability integration is rapidly becoming the defining competitive differentiator among autonomous energy management system vendors, with reinforcement learning algorithms that optimise battery dispatch schedules by simultaneously considering electricity price forecasts, solar generation predictions, occupancy patterns, demand charge accumulation, and grid service opportunity values demonstrating 12% to 22% improvement in economic performance relative to rule-based and conventional linear programming optimisation approaches that cannot adapt dispatch strategies in real time as forecast conditions evolve during the operating day. The integration of large language model interfaces within autonomous energy management platforms is enabling non-technical facility managers and building operators to interact with complex energy optimisation systems through natural language query and instruction rather than specialised software interfaces, significantly reducing the operational expertise barrier to full utilisation of autonomous system capability and expanding the addressable market for premium autonomous energy management platforms beyond the technically sophisticated energy management specialist customer base to encompass the broader population of facility operators, property managers, and sustainability coordinators whose engagement with energy system performance has historically been limited by interface complexity. Carbon accounting and decarbonisation program integration within autonomous energy management platforms is creating a new value layer beyond energy cost optimisation, with systems that simultaneously minimise energy cost, maximise renewable energy self-consumption, and report real-time scope one and scope two emission intensity against science-based targets generating enterprise sustainability reporting outputs that serve both operational energy management and corporate environmental, social, and governance disclosure requirements within a single integrated platform, growing at approximately 21.3% annually as corporate climate commitment deadlines drive investment in integrated energy and carbon management infrastructure.

Key Drivers

Distributed Energy Resource Proliferation and Electricity Market Complexity Creating Autonomous Optimisation Imperative Beyond Human and Rule-Based Management Capability

The exponential growth of distributed solar photovoltaic installations, battery energy storage systems, electric vehicle charging infrastructure, and flexible demand resources at commercial, industrial, and residential sites is creating energy portfolio management complexity whose optimal real-time coordination across multiple assets, multiple tariff structures, and multiple revenue streams simultaneously requires autonomous artificial intelligence-driven optimisation that human operators and conventional rule-based building management systems fundamentally cannot perform at the decision frequency, multi-variable scope, and adaptive learning capability that maximises economic and environmental outcomes. Global installed solar photovoltaic capacity exceeded 1.6 terawatts in 2025, with rooftop and commercial solar installations growing at approximately 18% annually, while battery energy storage deployments at commercial and industrial sites grew at approximately 34% annually, collectively creating a distributed energy resource portfolio whose management without autonomous optimisation systems leaves substantial economic value unrealised through suboptimal charging and discharging decisions, missed demand charge reduction opportunities, and uncoordinated load shifting that fails to respond optimally to dynamic electricity pricing signals. The increasing penetration of time-of-use, real-time pricing, and demand charge electricity tariff structures across commercial and industrial customer rate schedules in the United States, European Union, Australia, and Japan is creating a financial imperative for autonomous tariff-aware energy management, with demand charge peaks at commercial facilities accounting for 30% to 50% of total electricity bills under common commercial tariff structures and autonomous peak shaving through coordinated storage dispatch and load control generating annual savings of USD 50,000 to USD 800,000 per facility depending on peak demand magnitude and controllable load portfolio scope.

Corporate Net-Zero Carbon Commitments and Science-Based Emission Reduction Targets Driving Autonomous Energy Management Investment as Operational Decarbonisation Infrastructure

The corporate sustainability commitment landscape has been transformed by the exponential growth of science-based net-zero targets, with over 7,000 companies globally having committed to science-based emission reduction targets as of 2025 whose near-term scope one and scope two milestones require measurable and documented reductions in operational energy-related greenhouse gas emissions that are most cost-effectively achieved through autonomous energy management systems capable of simultaneously minimising energy cost and carbon emission intensity across complex multi-asset, multi-site energy portfolios. The Securities and Exchange Commission climate disclosure rule in the United States, the European Corporate Sustainability Reporting Directive, and the International Financial Reporting Standards S2 climate disclosure framework collectively mandate granular, auditable scope one and scope two emission reporting at levels of frequency and geographic specificity that require automated energy monitoring and carbon accounting infrastructure whose functionality is increasingly embedded within autonomous energy management platforms, making investment in autonomous energy management a regulatory compliance requirement for listed companies and large private corporations in addition to its energy cost reduction and sustainability program value. The growing investor and lender scrutiny of corporate energy transition credibility, expressed through environmental, social, and governance rating agency assessments, green bond framework compliance reviews, and sustainability-linked loan covenant structures, is creating a financial incentive for autonomous energy management platform investment by companies whose cost of capital is measurably affected by energy efficiency and decarbonisation performance metrics that autonomous systems can improve more consistently and documentably than manual or conventional building management system approaches.

Electricity Grid Volatility, Demand Response Program Expansion, and Virtual Power Plant Revenue Opportunities Creating Strong Business Case for Autonomous Grid Services Participation

The structural increase in electricity price volatility driven by high and growing renewable energy penetration, the progressive retirement of synchronous generation providing inertia and frequency response, and the expansion of real-time and intraday electricity markets in which price spreads of USD 50 to USD 500 per megawatt hour within a single operating day are increasingly common is creating monetisable flexibility value for distributed energy resource owners whose autonomous management systems can execute price-responsive dispatch strategies at market response speeds that manual operation cannot achieve, generating incremental annual revenue of USD 30,000 to USD 200,000 per megawatt of flexible capacity from electricity price arbitrage, frequency regulation, and demand response program participation. Utility and grid operator demand response programs in the United States, European Union, and Australia are expanding their technical and commercial eligibility frameworks to include smaller distributed energy resource assets below 100 kilowatts that were previously excluded from wholesale and ancillary service market participation, with aggregation platforms enabled by regulatory reform creating a pathway for residential and small commercial battery and flexible load assets to access grid service revenue through virtual power plant structures whose economic viability requires autonomous real-time control that individual asset owners cannot provide without automated management system support. The electrification of transport and heating is simultaneously expanding the scale of flexible load available for autonomous demand response management, with electric vehicle managed charging programs generating documented demand response capacity contributions of 3 to 7 kilowatts per vehicle during controlled charging periods and heat pump flexible demand programs providing 1 to 4 kilowatts per installation, collectively creating millions of autonomous energy management integration points whose aggregated flexibility represents a significant and growing grid services resource whose value is captured only through coordinated autonomous dispatch.

Key Challenges

Cybersecurity Vulnerability of Autonomous Energy Control Systems and Grid Infrastructure Attack Surface Expansion Constraining Deployment at Critical Facilities

Autonomous energy management systems that directly control physical energy assets including battery storage inverters, electric vehicle chargers, heating and cooling systems, and grid interconnection equipment create operational technology cybersecurity attack surfaces whose exploitation could result in energy service disruption, equipment damage, grid destabilisation at scale from coordinated attacks on aggregated distributed energy resource portfolios, or physical safety incidents from uncontrolled battery charging or discharge events, compelling critical facility operators, grid operators, and national cybersecurity authorities to impose increasingly stringent security architecture requirements on autonomous energy management platforms that substantially increase deployment complexity and cost. The connection of autonomous energy management systems to cloud analytics platforms, utility demand response aggregation networks, and wholesale electricity market interfaces creates information technology and operational technology convergence vulnerabilities that malicious actors have demonstrated the capability to exploit, with the NotPetya and Colonial Pipeline incidents highlighting the physical infrastructure consequences of operational technology cybersecurity failures whose energy sector equivalents could involve autonomous energy system manipulation to generate grid frequency disturbances, suppress demand response at scale during grid stress events, or create localised power quality events through uncoordinated distributed energy resource dispatch. Regulatory frameworks governing cybersecurity of distributed energy resources and autonomous energy management systems are evolving across the United States Federal Energy Regulatory Commission Order 887 framework, the European Union Network and Information Security 2 Directive requirements for energy sector operators, and national critical infrastructure protection standards whose implementation imposes compliance architecture investment, penetration testing obligations, and incident reporting requirements that add operational overhead to autonomous energy management platform operation and require ongoing security investment that some mid-size commercial and industrial operators find difficult to resource adequately.

Data Integration Complexity, Legacy Building Management System Incompatibility, and Sensor Coverage Gaps Limiting Autonomous Optimisation Performance at Existing Facilities

The deployment of autonomous energy management systems at existing commercial, industrial, and residential facilities requires integration with legacy building management and control systems, energy meters, sub-meters, equipment controllers, and utility data interfaces whose communication protocols, data schemas, sampling frequencies, and network architectures are frequently incompatible with modern cloud-based autonomous energy management platform data ingestion requirements without the deployment of integration gateways, protocol converters, and data normalisation middleware whose installation represents a significant portion of total system deployment cost and requires specialist system integration expertise whose availability constrains deployment velocity. Building and industrial facility sensor coverage gaps, including the absence of sub-metering at individual circuit or equipment level, insufficient occupancy and environmental monitoring instrumentation, and lack of real-time equipment status data from legacy process and building systems, prevent autonomous energy management platforms from exercising full optimisation authority across all controllable loads and generation assets, limiting achievable energy savings to a subset of the theoretical optimisation potential and reducing the return on investment of autonomous system deployment relative to fully instrumented new construction scenarios where sensor coverage is designed into the facility from inception. The temporal and spatial granularity of utility metering data available to autonomous energy management platforms varies substantially across utility service territories and metering infrastructure vintages, with some utilities providing only monthly billing data or 15-minute interval smart meter reads that are insufficient for the real-time optimisation and minute-by-minute dispatch decisions that maximise autonomous energy management system economic performance, requiring autonomous platform operators to deploy supplementary metering infrastructure at additional capital cost to achieve the data quality required for full autonomous optimisation capability.

Regulatory Fragmentation Across Electricity Markets, Demand Response Program Eligibility Barriers, and Grid Code Compliance Requirements Constraining Autonomous System Value Realisation

The value of autonomous energy management systems is substantially determined by their ability to access electricity market revenue streams including demand response payments, frequency regulation compensation, capacity market payments, and wholesale price arbitrage that vary enormously in availability, eligibility criteria, and financial magnitude across electricity market jurisdictions, creating a highly fragmented regulatory landscape that autonomous energy management platform developers must navigate across hundreds of utility service territories, regional transmission operator markets, and national electricity regulatory frameworks whose specific rules, qualification processes, and technical requirements differ in ways that impose significant market-by-market customisation and compliance investment requirements on platform vendors seeking broad geographic deployment. The aggregation of distributed energy resources for virtual power plant participation in wholesale electricity markets requires regulatory approval from grid operators and market administrators whose interconnection study processes, technical performance demonstration requirements, and ongoing telemetry and control compliance obligations can extend virtual power plant market entry timelines to 12 to 36 months and impose metering, communication, and control system upgrade requirements at individual asset sites that add capital cost to autonomous energy management deployments whose business case depends on grid service revenue that cannot be accessed until all regulatory prerequisites are satisfied. Autonomous demand response control of energy assets at industrial facilities whose production processes are sensitive to energy supply interruption requires autonomous system algorithms to incorporate complex production constraint models that prevent energy reduction events from affecting process continuity, creating system complexity that increases development cost, extends deployment and commissioning timelines, and requires deep collaboration between autonomous energy management system developers and industrial process engineers whose engagement throughout the system design and tuning process is a prerequisite for safe and reliable autonomous operation at production-critical industrial energy management applications.

Market Segmentation

- Segmentation By Application Segment

- Commercial Building Energy Management (Offices, Retail, and Hospitality)

- Industrial Energy Management (Manufacturing and Process Industries)

- Utility-Scale Virtual Power Plant and Grid Services

- Residential Energy Management and Home Automation

- Microgrid and Campus Energy Management

- Data Centre Energy Optimisation

- EV Fleet and Charging Infrastructure Management

- Others

- Segmentation By System Capability Level

- Rule-Based Automated Energy Management

- AI-Assisted Energy Optimisation with Human Approval

- Fully Autonomous Closed-Loop Energy Dispatch

- Autonomous Multi-Site Enterprise Energy Optimisation

- Autonomous Grid-Interactive Virtual Power Plant Control

- Segmentation By Managed Asset Type

- Solar Photovoltaic Generation Management

- Battery Energy Storage System Dispatch

- Electric Vehicle Charging Load Management

- HVAC and Thermal Load Optimisation

- Industrial Process Load Flexibility

- Backup and Standby Generation Dispatch

- Grid Connection and Import-Export Management

- Multi-Asset Portfolio Coordination

- Segmentation By Revenue Model

- Energy Cost Savings and Demand Charge Reduction

- Grid Service and Demand Response Revenue

- Wholesale Electricity Price Arbitrage

- Renewable Energy Certificate and Carbon Credit Generation

- Subscription Software-as-a-Service Platform Fees

- Energy-as-a-Service and Managed Energy Services

- Segmentation By AI and Analytics Technology

- Reinforcement Learning Dispatch Optimisation

- Machine Learning Demand and Generation Forecasting

- Digital Twin and Physics-Informed Simulation

- Model Predictive Control Algorithms

- Large Language Model and Natural Language Interfaces

- Rule-Based and Heuristic Optimisation

- Segmentation By Deployment Model

- Cloud-Hosted Software-as-a-Service Platform

- On-Premise Enterprise Software Deployment

- Hybrid Cloud and Edge Computing Architecture

- Embedded Controller and Gateway Hardware

- Managed Energy Services with Performance Guarantee

- Segmentation By End User

- Commercial Real Estate Owners and Operators

- Industrial Manufacturers and Process Plant Operators

- Electric Utilities and Grid Operators

- Demand Response Aggregators and Virtual Power Plant Operators

- Data Centre Operators

- Healthcare and Educational Institution Facility Managers

- Residential and Community Energy Program Participants

- Others

- Segmentation By Region

- North America (United States and Canada)

- Europe (Germany, United Kingdom, France, Netherlands, and Others)

- Asia-Pacific (Japan, Australia, South Korea, China, and Others)

- Middle East and Africa

- Latin America (Brazil, Chile, and Others)

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Autonomous Energy Management Systems Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by application segment, commercial buildings, industrial facilities, utility and grid services, residential, and microgrid, by system capability level, rule-based, AI-optimised, and fully autonomous, and by geography, to enable technology vendors, energy management service providers, utilities, and investors to identify which application categories and regional markets will generate the highest absolute revenue and most commercially significant autonomous energy management adoption momentum across the forecast period?

- How is the growing deployment of distributed energy resources including solar photovoltaic, battery energy storage, electric vehicle charging, and flexible industrial loads expected to drive autonomous energy management system adoption and feature requirements through 2034, what are the documented energy cost reduction, demand charge savings, and carbon emission reduction outcomes being achieved at commercial and industrial facilities with fully integrated autonomous energy management deployments relative to conventional building management system baselines, and which distributed energy resource portfolio configurations and facility types are generating the highest autonomous energy management system return on investment at currently operating reference deployments?

- What is the projected commercial trajectory of virtual power plant platforms and autonomous demand response aggregation systems through 2034, which electricity market jurisdictions in the United States, European Union, Australia, Japan, and South Korea are generating the most commercially significant regulatory frameworks for distributed energy resource grid service participation, what revenue per megawatt benchmarks are autonomous energy management systems achieving from frequency regulation, demand response, and wholesale price arbitrage participation at current market conditions, and how are evolving grid operator technical requirements for distributed energy resource controllability and telemetry shaping autonomous energy management platform architecture and compliance investment?

- How are artificial intelligence capability advances including reinforcement learning dispatch optimisation, large language model natural language interfaces, and generative AI scenario planning tools expected to reshape the competitive differentiation, addressable customer base, and economic performance outcomes of autonomous energy management platforms through 2034, which AI capability categories are generating the most measurable performance improvement relative to conventional optimisation approaches at production deployments, and how are leading autonomous energy management platform vendors differentiating their AI investment strategies relative to competitors and to general-purpose AI platforms seeking to enter the energy management vertical?

- Who are the leading autonomous energy management system platform developers, industrial energy optimisation software companies, virtual power plant aggregation platform operators, building energy management AI specialists, and microgrid control system providers currently defining the competitive landscape of the global market, and what are their respective platform capability coverage across application segments and distributed energy resource types, reference deployment performance outcomes, regulatory compliance and grid service market access capabilities, cybersecurity architecture and certification investments, research and development investment in AI optimisation and carbon management integration, and competitive positioning responses to the data integration, regulatory fragmentation, and cybersecurity challenges shaping autonomous energy management market development through 2034?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Cybersecurity, OT/IT Network Convergence & Critical Energy Infrastructure Vulnerability Risk

- AI Model Reliability, Autonomous Decision Failure & Grid Stability Risk

- Legacy System Integration, Interoperability & Data Silos Risk

- Regulatory Compliance, Grid Code Adherence & Energy Market Rule Change Risk

- Capital Investment, ROI Uncertainty & Technology Adoption Barrier Risk

- Regulatory Framework & Standards

- Grid Code, Demand Response & Smart Grid Regulatory Frameworks Applicable to Autonomous Energy Management Systems

- IEC 61850, IEC 62351 & NERC CIP Cybersecurity Standards for Energy Management & Grid Automation

- Building Energy Management, ISO 50001 & Energy Efficiency Directive Compliance Requirements

- Carbon Reporting, Net Zero Target Setting & Scope 1/2/3 Emissions Disclosure Standards for Automated Energy Systems

- Government Incentive Programmes, Smart Energy Investment Grants & Demand-Side Response Policy Frameworks

- Global Green Autonomous Energy Management Systems Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by System Type

- Building Energy Management Systems (BEMS) with Autonomous Control

- Industrial Energy Management Systems (IEMS) with Autonomous Optimisation

- Microgrid Energy Management Systems (MEMS) with Autonomous Dispatch

- Virtual Power Plant (VPP) & Distributed Energy Resource Management Systems (DERMS)

- EV Fleet & Smart Charging Energy Management Systems

- Campus & Multi-Site Autonomous Energy Orchestration Platforms

- Data Centre Autonomous Power & Cooling Management Systems

- Renewable Energy Asset Management & Autonomous Optimisation Platforms

- Market Size & Forecast by Deployment Mode

- Cloud-Based (SaaS & Platform-as-a-Service)

- On-Premise

- Hybrid (Cloud & On-Premise)

- Edge Computing & Embedded Autonomous Control

- Market Size & Forecast by AI & Automation Technology

- Machine Learning & Deep Learning-Based Load Forecasting & Optimisation

- Reinforcement Learning & Autonomous Agent-Based Energy Dispatch

- Predictive Analytics & Digital Twin-Based Scenario Modelling

- Model Predictive Control (MPC) & Advanced Process Control (APC)

- Generative AI & Large Language Model (LLM) Integration for Energy Intelligence

- Market Size & Forecast by Component

- Software (Autonomous Control Platform, Analytics & Optimisation Modules)

- Hardware (Smart Meters, IoT Sensors, Edge Controllers & Gateways)

- Services (Implementation, Integration, Training & Managed Services)

- Market Size & Forecast by Energy Source Managed

- Solar PV Generation

- Wind Energy Generation

- Battery Energy Storage Systems (BESS)

- Grid Electricity & Demand Flexibility

- Combined Heat & Power (CHP) & Thermal Energy

- EV Charging Infrastructure

- Hydrogen & Green Fuel Assets

- Market Size & Forecast by End-User

- Commercial Buildings & Real Estate

- Industrial Manufacturers & Process Industries

- Data Centres & Cloud Infrastructure Operators

- Utilities & Grid Operators

- Hospitals & Healthcare Facilities

- Retail, Hospitality & Mixed-Use Developments

- Government & Public Sector Buildings

- Campuses, Universities & Smart Cities

- Market Size & Forecast by Application

- Autonomous Load Balancing & Peak Demand Reduction

- Renewable Energy Integration & Curtailment Minimisation

- Battery Storage Dispatch Optimisation & Arbitrage

- Demand Response & Grid Services Participation

- Carbon Footprint Tracking, Reporting & Autonomous Abatement

- Predictive Maintenance & Energy Asset Performance Optimisation

- EV Smart Charging Scheduling & Vehicle-to-Grid (V2G) Management

- Market Size & Forecast by Organisation Size

- Large Enterprises

- Small & Medium Enterprises (SMEs)

- Market Size & Forecast by Sales Channel

- Direct Sales & Enterprise Licensing

- System Integrators & Energy Service Companies (ESCOs)

- Cloud Marketplace & SaaS Subscription

- Managed Energy Service & Outcome-Based Performance Contracts

- North America Green Autonomous Energy Management Systems Market Outlook

- Market Size & Forecast

- By Value

- By System Type

- By Deployment Mode

- By AI & Automation Technology

- By Energy Source Managed

- By End-User

- By Application

- By Organisation Size

- By Sales Channel

- By Country

- Market Size & Forecast

- Europe Green Autonomous Energy Management Systems Market Outlook

- Market Size & Forecast

- By Value

- By System Type

- By Deployment Mode

- By AI & Automation Technology

- By Energy Source Managed

- By End-User

- By Application

- By Organisation Size

- By Sales Channel

- By Country

- Market Size & Forecast

- Asia-Pacific Green Autonomous Energy Management Systems Market Outlook

- Market Size & Forecast

- By Value

- By System Type

- By Deployment Mode

- By AI & Automation Technology

- By Energy Source Managed

- By End-User

- By Application

- By Organisation Size

- By Sales Channel

- By Country

- Market Size & Forecast

- Latin America Green Autonomous Energy Management Systems Market Outlook

- Market Size & Forecast

- By Value

- By System Type

- By Deployment Mode

- By AI & Automation Technology

- By Energy Source Managed

- By End-User

- By Application

- By Organisation Size

- By Sales Channel

- By Country

- Market Size & Forecast

- Middle East & Africa Green Autonomous Energy Management Systems Market Outlook

- Market Size & Forecast

- By Value

- By System Type

- By Deployment Mode

- By AI & Automation Technology

- By Energy Source Managed

- By End-User

- By Application

- By Organisation Size

- By Sales Channel

- By Country

- Market Size & Forecast

- Country-Wise* Green Autonomous Energy Management Systems Market Outlook

- Market Size & Forecast

- By Value

- By System Type

- By Deployment Mode

- By AI & Automation Technology

- By Energy Source Managed

- By End-User

- By Application

- By Organisation Size

- By Sales Channel

- By Country

- Market Size & Forecast

- *Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Italy, Norway, Sweden, China, Japan, India, Australia, South Korea, Singapore, Brazil, Chile, Saudi Arabia, UAE, Egypt, South Africa, Israel

- Technology Landscape & Innovation Analysis

- Reinforcement Learning & Autonomous Agent Technology Deep-Dive: Multi-Agent Energy Dispatch, Reward Shaping & Real-World Deployment

- Model Predictive Control (MPC) & Advanced Process Control Technology for Autonomous Green Energy Optimisation

- Digital Twin & Physics-Informed AI Technology for Energy System Simulation & Autonomous Scenario Planning

- DERMS & Virtual Power Plant (VPP) Technology: Aggregation Architecture, Grid Services & Autonomous Bidding Platforms

- Autonomous Microgrid Control Technology: Islanding Detection, Seamless Transition & Multi-Source Dispatch Optimisation

- Generative AI & LLM Integration in Energy Management: Natural Language Interfaces, Report Automation & Decision Support

- Cybersecurity & Resilience Technology for Autonomous Energy Management Systems: Zero-Trust Architecture & OT/IT Security

- Patent & IP Landscape in Green Autonomous Energy Management System Technologies

- Value Chain & Supply Chain Analysis

- AI Platform Software Development, Algorithm Engineering & Energy Domain Data Science Supply Chain

- IoT Sensor, Smart Meter, Edge Controller & Gateway Hardware Supply Chain

- Cloud Infrastructure, Data Centre & Hyperscaler Service Provider Channel

- Telecommunications, Industrial Ethernet & Operational Technology Network Supply Chain

- System Integrator, ESCO & Energy Consultant Implementation Channel

- Renewable Energy Asset Owner, Utility & Grid Operator Procurement Channel

- Carbon Registry, Energy Attribute Certificate & Sustainability Data Platform Channel

- Pricing Analysis

- Green Autonomous EMS SaaS Subscription & Per-Site Licensing Pricing Analysis

- On-Premise & Hybrid Deployment Licence, Implementation & Integration Cost Analysis

- Hardware (Smart Meter, IoT Sensor & Edge Controller) Capital Cost Analysis

- Managed Energy Service & Outcome-Based Contract Pricing & Savings-Sharing Model Analysis

- Total Cost of Ownership (TCO) & ROI Analysis for Green Autonomous EMS Deployments

- SaaS vs. On-Premise vs. ESCO Performance Contract Cost Comparison & Value Benchmarking

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Green Autonomous EMS: Carbon Footprint, Hardware Energy Consumption & Electronic Waste

- Quantified Energy Savings, Carbon Reduction & Renewable Integration Benefits of Autonomous EMS Deployments

- Demand Flexibility, Grid Decarbonisation & System-Level Carbon Abatement Enabled by Autonomous Energy Management

- Green Building Certification, LEED, BREEAM & WELL Standard Compliance Enabled by Autonomous EMS

- Regulatory-Driven Sustainability, SDG 7 (Affordable & Clean Energy) & SDG 13 (Climate Action) Alignment & Green Finance Eligibility

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by System Type, Deployment Mode & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by System Type, End-User & Geography

- Player Classification

- Integrated Building & Industrial Automation Companies with Autonomous EMS Divisions

- Pure-Play AI & Advanced Analytics Platform Providers for Energy Management

- DERMS & Virtual Power Plant Platform Specialists

- Energy Service Companies (ESCOs) Deploying Autonomous EMS Solutions

- Utility & Grid Operator Technology Arms Offering Autonomous Demand Management

- Start-ups & Scale-ups in Autonomous Green Energy Optimisation & Carbon Management

- Cloud Hyperscalers & Enterprise AI Platform Vendors Serving Energy Management

- Competitive Analysis Frameworks

- Market Share Analysis by System Type, End-User & Region

- Company Profile

- Company Overview & Headquarters

- Green Autonomous EMS Products & Technology Portfolio

- Key Customer Relationships & Reference Site Deployments

- R&D Investment & AI Innovation Pipeline

- Revenue (Green Autonomous EMS Segment) & Annual Recurring Revenue (ARR)

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Product Launches, Funding Rounds)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (AI Autonomy Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By System Type, AI Technology, Energy Source Managed, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output