Brazil Biofuels and Bio-Based Chemicals Market By Product Type, By Feedstock, By Production Process, By Application, By End-Use Industry, By Region, Competition, Forecast & Opportunities, 2021-2036F

Market Definition

The Brazil Biofuels and Bio-Based Chemicals Market covers the production, blending, distribution, export, and downstream consumption of liquid and gaseous biofuels including hydrous and anhydrous sugarcane and corn ethanol, biodiesel from soybean oil, beef tallow, used cooking oil, and emerging macauba and palm oils, renewable diesel and sustainable aviation fuel via HEFA and Alcohol-to-Jet pathways, biomethane and renewable natural gas, second-generation cellulosic ethanol, and emerging green hydrogen, alongside bio-based chemicals encompassing bio-ethylene, bio-polyethylene, bio-MEG, bio-succinic acid, bio-lactic acid, sugarcane-derived polyhydroxyalkanoates (PHAs), bio-based surfactants, and specialty fermentation products. The market spans procurement, off-take, and commercial activity by integrated sugarcane mills, ethanol producers, oil and gas majors, road transportation fuel distributors, airlines, petrochemical producers, polymer converters, agrochemical companies, and emerging green chemicals exporters operating across Brazil. The supplier landscape spans major producers including Raizen, BP Bunge Bioenergia, Cosan, Atvos, Tereos, Sao Martinho, Adecoagro, Petrobras, ECB Group, Be8 (BSBIOS), Vibra Energia, Granol, JBS Biodiesel, Camil, Acelen Renovaveis, Brava Energia, FS Bioenergia, Inpasa, alongside bio-based chemicals players Braskem, Oxiteno, GranBio, Solvay, and emerging entrants in PHA, bio-MEG, and green hydrogen segments. Market dynamics are governed by RenovaBio decarbonization credit framework (CBIO), national biofuel blending mandates including 27% anhydrous ethanol and 14% biodiesel in 2025, sugarcane production cycles, corn ethanol scaling in the Cerrado, SAF mandates under the Combustivel do Futuro law, COP30 climate commitments, and rising export demand into the European Union, the United States, and Asia-Pacific markets.

Market Insights

The Brazil biofuels and bio-based chemicals market is entering a sustained high-growth phase driven by the structural expansion of corn ethanol production in the Cerrado, accelerating sustainable aviation fuel investment under the Combustivel do Futuro law and RenovaBio decarbonization framework, rising biodiesel blending mandates advancing from 14% in 2025 toward 20% by 2030, biomethane and renewable natural gas commercialization, and the strategic positioning of Brazil as a global green chemicals and green hydrogen export hub anchored by COP30 climate commitments. The market was valued at USD 38.6 billion in 2025 and is projected to reach USD 84.2 billion by 2034, advancing at a compound annual growth rate of 9.1% through the forecast period, supported by integrated sugarcane and corn ethanol capacity additions, SAF capacity build-out, biomethane scaling, and bio-based polymer expansion.

Ethanol remains the cornerstone of Brazil’s biofuel landscape, with national production exceeding 36 billion liters in 2025, accounting for approximately 27% of global ethanol output. Sugarcane ethanol production at Raizen, Cosan, Sao Martinho, Tereos, Atvos, BP Bunge Bioenergia, and Adecoagro continues to dominate the southeast and center-west cane belts, while corn ethanol output from the Cerrado has surged from approximately 0.8 billion liters in 2018 to over 8.6 billion liters in 2025, advancing at over 16% CAGR. FS Bioenergia, Inpasa, and emerging corn ethanol players including ECB Group and Be8 are scaling integrated corn ethanol, DDGS, and corn oil production across Mato Grosso, Goias, and Mato Grosso do Sul, leveraging double-cropping economics and the proximity of corn surplus to ethanol-deficient northern and northeastern markets to underpin durable returns.

Sustainable aviation fuel has emerged as the highest-impact emerging segment, with the Combustivel do Futuro law mandating 1% SAF blending in 2027 advancing to 10% by 2037, alongside ANP regulatory frameworks supporting SAF certification under ASTM D7566. Acelen Renovaveis is advancing a USD 2.8 billion SAF and renewable diesel facility at Mataripe, while Raizen, Cosan, ECB Group, Petrobras, and Brava Energia are progressing additional SAF projects targeting commissioning between 2027 and 2032. Renewable diesel and biodiesel capacity expansion is similarly accelerating, with national biodiesel production exceeding 9.4 billion liters in 2025 under the B14 blending mandate at Be8, Granol, JBS Biodiesel, BSBIOS, Olfar, and Camil operations. Biomethane and renewable natural gas commercialization is also scaling rapidly, with over 30 operating biomethane plants converting vinasse, filter cake, and sugarcane bagasse into pipeline-grade RNG.

Bio-based chemicals output is anchored by Braskem’s 200,000 tonne per year bio-ethylene and bio-polyethylene plant at Triunfo, which has produced over 800,000 tonnes of I’m green polyethylene since 2010 and serves global brand owners including Lego, Tetra Pak, Procter & Gamble, Unilever, and Nestle seeking renewable-content packaging. GranBio is advancing second-generation cellulosic ethanol at Alagoas and emerging biopolymer programs, while Oxiteno, Solvay, and Acelen are progressing bio-based surfactants, glycols, and specialty chemicals. The southeast region anchors approximately 48% of national biofuel and bio-chemicals production capacity, followed by the center-west at 32% supporting corn ethanol expansion, the south at 14% supporting biodiesel and biomethane, and the northeast at 6% anchored by sugarcane operations and emerging SAF and green hydrogen investments at Pecem, Suape, and Bahia hubs.

Key Drivers

RenovaBio CBIO Credit Framework, Combustivel do Futuro Law, and Rising Biofuel Blending Mandates Driving Structural Demand Growth

The RenovaBio decarbonization framework generating tradable CBIO credits, the Combustivel do Futuro law mandating 1% SAF blending in 2027 advancing to 10% by 2037, anhydrous ethanol blending at 27% in 2025, and biodiesel advancing from B14 toward B20 by 2030 are anchoring durable structural demand growth across Brazil’s biofuels landscape. National biofuel production exceeding 45 billion liters in 2025 across ethanol, biodiesel, biomethane, and emerging renewable diesel and SAF is projected to advance at 8.4% CAGR through 2034.

Corn Ethanol Expansion in the Cerrado, Double-Cropping Economics, and Integrated DDGS and Corn Oil Co-Product Revenue

Corn ethanol production in the Cerrado has surged from approximately 0.8 billion liters in 2018 to over 8.6 billion liters in 2025, advancing at over 16% CAGR with double-cropping economics, abundant corn surplus, and integrated DDGS animal feed and corn oil co-product revenue underpinning durable returns. FS Bioenergia, Inpasa, ECB Group, Be8, and emerging entrants are scaling integrated capacity across Mato Grosso, Goias, and Mato Grosso do Sul, with announced capex programs exceeding USD 6.4 billion between 2024 and 2030 serving ethanol-deficient northern and northeastern markets.

Sustainable Aviation Fuel Build-Out, Green Hydrogen Export Positioning, and Bio-Based Chemicals Anchoring Long-Term Growth

Acelen Renovaveis advancing a USD 2.8 billion SAF and renewable diesel facility at Mataripe, alongside SAF programs at Raizen, Cosan, ECB Group, Petrobras, and Brava Energia targeting commissioning between 2027 and 2032, is positioning Brazil as a global SAF and renewable diesel hub. Green hydrogen export investments at Pecem, Suape, Acu, and Bahia anchored by Fortescue, Acwa Power, EDP, Casa dos Ventos, and Unigel, alongside Braskem bio-polyethylene scaling and GranBio cellulosic ethanol programs, are reinforcing Brazil’s green chemicals export positioning through 2034.

Key Challenges

Feedstock Cost Volatility, Sugarcane Yield Variability, and Climate Risk Reshaping Production Economics

Sugarcane productivity remains structurally sensitive to climate variability, with 2021 to 2024 cycles delivering yields 8% to 18% below decadal averages across the southeast and center-west, compressing producer margins. Corn feedstock pricing exposure for Cerrado ethanol producers, soybean oil cost volatility for biodiesel operators, and weather-driven disruption to feedstock availability are introducing margin compression across the biofuels value chain. El Nino and La Nina cycles, accelerating climate change pressures, and water availability concerns are reshaping production economics through 2034.

Infrastructure Bottlenecks, Logistics Costs, and Export Capacity Constraints Limiting Regional and International Distribution

Brazil’s ethanol, biodiesel, and bio-based chemicals logistics infrastructure remains structurally constrained, with truck-dominated transport accounting for approximately 64% of fuel and chemical movement, alongside limited pipeline capacity, port congestion at Santos, Paranagua, and Suape, and rail bottlenecks materially elevating logistics costs and lead times. Sao Paulo to northern Brazil ethanol logistics costs typically range from 0.12 to 0.22 USD per liter, while export capacity constraints at major terminals are limiting Brazil’s ability to capture rising European Union, US, Japanese, and Asia-Pacific demand for SAF, renewable diesel, biofuels, and bio-based chemicals.

Land Use, Deforestation Scrutiny, and Sustainability Certification Pressures Reshaping International Market Access

Tightening sustainability scrutiny under the EU Deforestation Regulation (EUDR), ICAO CORSIA SAF eligibility frameworks, ISCC EU and Bonsucro certification requirements, and emerging US Treasury SAF tax credit eligibility guidance is reshaping Brazilian biofuels and bio-based chemicals export economics. Deforestation concerns, indirect land use change attribution, and supply chain traceability requirements at sugarcane, soy, and corn feedstock origin are introducing certification complexity, audit costs, and market access risk for major producers seeking premium international offtake through 2034.

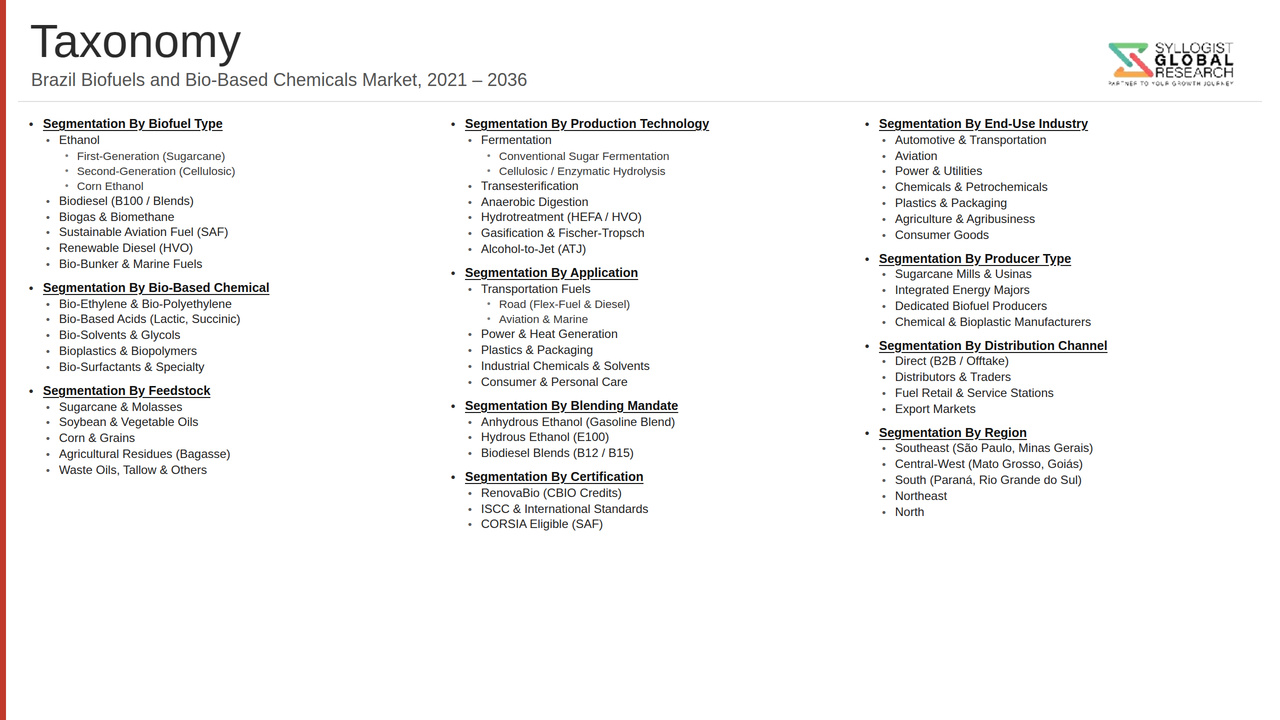

Market Segmentation

- Segmentation By Product Type

- Hydrous and Anhydrous Sugarcane Ethanol

- Corn Ethanol

- Biodiesel

- Renewable Diesel (HVO)

- Sustainable Aviation Fuel (SAF)

- Biomethane and Renewable Natural Gas

- Second-Generation Cellulosic Ethanol

- Green Hydrogen and Derivatives

- Bio-Based Chemicals (Bio-Ethylene, Bio-MEG, Bio-PE, PHAs, Bio-Lactic Acid)

- Others

- Segmentation By Feedstock

- Sugarcane and Sugarcane Bagasse

- Corn

- Soybean Oil

- Beef Tallow and Animal Fats

- Used Cooking Oil

- Macauba and Palm Oils

- Vinasse and Filter Cake

- Forest Residues and Cellulosic Biomass

- Green Hydrogen and Captured CO2

- Others

- Segmentation By Production Process

- Fermentation (1G Sugarcane and Corn)

- Second-Generation (2G) Cellulosic Conversion

- Transesterification (Biodiesel)

- Hydroprocessed Esters and Fatty Acids (HEFA)

- Alcohol-to-Jet (ATJ)

- Anaerobic Digestion and Biomethane Upgrading

- Electrolysis (Green Hydrogen)

- Bio-Ethylene and Bio-MEG Catalytic Conversion

- Others

- Segmentation By Application

- Road Transportation Fuels

- Aviation Fuels

- Marine and Bunker Fuels

- Industrial Heating and Power

- Petrochemical Feedstock

- Polymers and Bioplastics

- Specialty Chemicals and Surfactants

- Renewable Natural Gas Distribution

- Others

- Segmentation By End-Use Industry

- Automotive and Light Transportation

- Commercial Vehicles and Trucking

- Aviation

- Petrochemicals and Polymers

- Agriculture and Agribusiness

- Power Generation

- Marine and Shipping

- Specialty Chemicals and Consumer Goods

- Others

- Segmentation By Region

- Southeast (Sao Paulo, Minas Gerais, Rio de Janeiro, Espirito Santo)

- Center-West (Mato Grosso, Goias, Mato Grosso do Sul, Distrito Federal)

- South (Parana, Rio Grande do Sul, Santa Catarina)

- Northeast (Bahia, Pernambuco, Alagoas, Ceara, Paraiba)

- North (Para, Amazonas, Rondonia, Tocantins)

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total market valuation of the Brazil Biofuels and Bio-Based Chemicals Market in 2025, projected through 2034, disaggregated by product type, feedstock, production process, application, and end-use industry, enabling biofuel producers, bio-based chemicals players, off-takers, exporters, and investors to identify the highest-growth opportunities and most durable revenue corridors across the value chain?

- How is the Combustivel do Futuro law mandating 1% SAF blending in 2027 advancing to 10% by 2037, alongside RenovaBio CBIO credits, anhydrous ethanol at 27% blending, and biodiesel advancing from B14 to B20 by 2030, reshaping biofuel demand patterns across Brazilian producers and off-takers through 2034?

- How is corn ethanol expansion in the Cerrado advancing from 0.8 billion liters in 2018 to over 8.6 billion liters in 2025 at 16% CAGR reshaping competitive positioning across FS Bioenergia, Inpasa, ECB Group, Be8, and emerging Cerrado entrants, and what scaling potential exists across Mato Grosso, Goias, and Mato Grosso do Sul through 2034?

- Which biofuel product categories including sugarcane ethanol, corn ethanol, biodiesel, renewable diesel, SAF, biomethane, second-generation cellulosic ethanol, and green hydrogen are generating the highest growth rates, and how is the supply landscape evolving across Raizen, BP Bunge Bioenergia, Cosan, Atvos, Tereos, Sao Martinho, Adecoagro, Petrobras, ECB Group, Be8, Vibra Energia, Granol, JBS Biodiesel, Acelen Renovaveis, Brava Energia, FS Bioenergia, and Inpasa?

- How is Acelen Renovaveis advancing a USD 2.8 billion SAF and renewable diesel facility at Mataripe, alongside SAF programs at Raizen, Cosan, ECB Group, Petrobras, and Brava Energia targeting commissioning between 2027 and 2032, positioning Brazil as a global SAF and renewable diesel hub through 2034?

- How are bio-based chemicals output anchored by Braskem 200,000 tonne per year bio-ethylene and bio-polyethylene plant at Triunfo serving Lego, Tetra Pak, Procter & Gamble, Unilever, and Nestle, alongside GranBio cellulosic ethanol and Oxiteno, Solvay, and Acelen specialty chemicals programs, reshaping Brazilian bio-based chemicals competitive positioning?

- How are sustainability scrutiny under the EU Deforestation Regulation, ICAO CORSIA SAF eligibility frameworks, ISCC EU and Bonsucro certification, and US Treasury SAF tax credit eligibility guidance reshaping Brazilian biofuels and bio-based chemicals export economics and competitive market access across European Union, United States, Japanese, and emerging Asia-Pacific markets?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Feedstock (Sugarcane & Oilseed) Availability, Climate & Price Volatility Risk

- Policy Dependence, RenovaBio Continuity & Mandate Withdrawal Risk

- Oil Price Competitiveness & Fossil Fuel Substitution Risk

- Technology Scale-Up, 2G Ethanol & SAF Commercialisation Risk

- Financing, Project Development & Stranded Asset Risk

- Regulatory Framework & Standards

- RenovaBio, Biofuel Mandate & Blending Obligation (Ethanol & Biodiesel) Frameworks

- Carbon Credit (CBIO), Decarbonisation Target & Energy Policy Frameworks

- Bio-Based Product, Fuel Specification & Quality Standards (ANP)

- Environmental Licensing, Land-Use & Feedstock Sourcing Regulations

- Green Finance, Carbon Accounting, ESG Disclosure & Sustainable Procurement Standards

- Brazil Biofuels and Bio-Based Chemicals Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Production & Consumption, Million Litres / Kilo Tonnes)

- Market Size & Forecast by Product Type

- Sugarcane Ethanol (First-Generation)

- Cellulosic / Second-Generation Ethanol

- Biodiesel (FAME)

- Renewable Diesel (HVO)

- Biogas & Biomethane

- Sustainable Aviation Fuel (SAF) & Bio-Jet

- Bio-Based Chemicals & Intermediates

- Biopolymers & Bioplastics

- Other Biofuels & Bio-Based Products

- Market Size & Forecast by Feedstock

- Sugarcane & Bagasse

- Corn & Starch Crops

- Soybean & Vegetable Oils

- Animal Fats & Tallow

- Used Cooking Oil (UCO) & Waste Oils

- Lignocellulosic & Agricultural Residues

- Municipal & Organic Waste

- Forestry & Wood Residues

- Other Advanced & Emerging Feedstocks

- Market Size & Forecast by Process Technology

- Fermentation & Distillation (Ethanol)

- Transesterification (Biodiesel)

- Hydrotreating (Renewable Diesel & HVO)

- Anaerobic Digestion (Biogas & Biomethane)

- Thermochemical & Biochemical Conversion

- Market Size & Forecast by Production Scale

- Large-Scale Integrated Biorefineries (Above 200 Million Litres per Annum)

- Medium-Scale Production Plants (50 to 200 Million Litres per Annum)

- Small-Scale & Decentralised Plants (Below 50 Million Litres per Annum)

- Market Size & Forecast by Application

- Road Transportation Fuel & Blending

- Aviation & Marine Fuel

- Power & Heat Generation

- Industrial Chemical Feedstock

- Plastics & Polymer Production

- Other Industrial & Consumer Applications

- Market Size & Forecast by End-User

- Transportation & Automotive Sector

- Aviation & Marine Sector

- Power & Utility Sector

- Chemical & Industrial Manufacturers

- Agriculture & Other End-Users

- Market Size & Forecast by Sales Channel

- Direct Sales & Long-Term Offtake Agreement

- Distributors & Fuel Marketers

- Blending, Trading & Spot Market

- Export & Other Channels

- Southeast Region Biofuels and Bio-Based Chemicals Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Production & Consumption, Million Litres / Kilo Tonnes)

- By Product Type

- By Feedstock

- By Process Technology

- By Production Scale

- By Application

- By End-User

- By State

- By Sales Channel

- Market Size & Forecast

- South Region Biofuels and Bio-Based Chemicals Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Production & Consumption, Million Litres / Kilo Tonnes)

- By Product Type

- By Feedstock

- By Process Technology

- By Production Scale

- By Application

- By End-User

- By State

- By Sales Channel

- Market Size & Forecast

- Center-West Region Biofuels and Bio-Based Chemicals Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Production & Consumption, Million Litres / Kilo Tonnes)

- By Product Type

- By Feedstock

- By Process Technology

- By Production Scale

- By Application

- By End-User

- By State

- By Sales Channel

- Market Size & Forecast

- Northeast Region Biofuels and Bio-Based Chemicals Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Production & Consumption, Million Litres / Kilo Tonnes)

- By Product Type

- By Feedstock

- By Process Technology

- By Production Scale

- By Application

- By End-User

- By State

- By Sales Channel

- Market Size & Forecast

- North Region Biofuels and Bio-Based Chemicals Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Production & Consumption, Million Litres / Kilo Tonnes)

- By Product Type

- By Feedstock

- By Process Technology

- By Production Scale

- By Application

- By End-User

- By State

- By Sales Channel

- Market Size & Forecast

- State-Wise* Biofuels and Bio-Based Chemicals Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Production & Consumption, Million Litres / Kilo Tonnes)

- By Product Type

- By Feedstock

- By Process Technology

- By Production Scale

- By Application

- By End-User

- By State

- By Sales Channel

- Market Size & Forecast

- *States Analyzed in the Syllogist Brazil Research Portfolio: Sao Paulo, Rio de Janeiro, Minas Gerais, Espirito Santo, Parana, Santa Catarina, Rio Grande do Sul, Goias, Mato Grosso, Mato Grosso do Sul, Distrito Federal, Bahia, Pernambuco, Ceara, Maranhao, Para, Amazonas, Tocantins

- Technology Landscape & Innovation Analysis

- Sugarcane Ethanol (1G) Production Technology Deep-Dive

- Cellulosic (2G) Ethanol & Enzymatic Hydrolysis Technology

- Biodiesel (Transesterification) Production Technology

- Renewable Diesel & HVO Hydrotreating Technology

- Biogas, Biomethane & Anaerobic Digestion Technology

- Sustainable Aviation Fuel (SAF) Production Technology

- Bio-Based Chemicals, Biopolymers & Fermentation Technology

- Patent & IP Landscape in Biofuels and Bio-Based Chemicals Technologies

- Value Chain & Supply Chain Analysis

- Feedstock Cultivation, Sourcing & Aggregation Supply Chain

- Biorefinery, Reactor & Processing Equipment Supply Chain

- Enzyme, Catalyst & Chemical Input Supply Chain

- Logistics, Storage & Blending Infrastructure

- Fuel Distributor, Blender & Offtaker Procurement Landscape

- Chemical Producer, Brand Owner & Offtake Partner Channel

- Co-Product, Residue Valorisation & Circular Economy

- Pricing Analysis

- Sugarcane Ethanol Production Cost and Pricing Analysis

- Biodiesel & Renewable Diesel Cost and Pricing Analysis

- Biogas & Biomethane Levelised Cost Analysis

- Bio-Based Chemicals & Biopolymer Price Premium Analysis

- Feedstock Cost, Carbon Credit (CBIO) & Margin Structure Analysis

- Total Biofuels Economics: Cost-per-Litre and Carbon-Abatement Cost Optimisation Analysis

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Brazilian Biofuels: Carbon Footprint, Energy Balance & GHG Savings Across Pathways

- Carbon Neutrality & Net Zero Contribution: RenovaBio, Decarbonisation and Energy Transition Pathway

- Circular Economy & Feedstock Valorisation: Bagasse, Residue and Waste Utilisation Contribution

- Environmental Compliance, Land-Use Change (ILUC), Deforestation & Biodiversity Consideration

- Regulatory-Driven Sustainability, SDG 7 (Affordable Clean Energy) & SDG 13 (Climate Action) Alignment & Green Finance Eligibility

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Product Type & Region)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Product Type, Feedstock & Region

- Player Classification

- Integrated Sugar-Ethanol & Biofuel Producers

- Biodiesel & Renewable Diesel Producers

- Biogas & Biomethane Producers

- Sustainable Aviation Fuel (SAF) Producers

- Bio-Based Chemical & Biopolymer Producers

- Technology Licensors, Enzyme & Catalyst Providers

- Feedstock Suppliers & Agribusiness Companies

- Emerging & Advanced Biofuel Entrants

- Competitive Analysis Frameworks

- Market Share Analysis by Product Type, Feedstock & Region

- Company Profile

- Company Overview & Headquarters

- Biofuels & Bio-Based Products Portfolio

- Key Customer Relationships & Reference Offtake Agreements

- Manufacturing Footprint & Production Capacity

- Revenue (Biofuels & Bio-Based Chemicals Segment) & Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Capacity Expansion, Offtake Deals, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Product Type, Feedstock, Application, End-User & Region

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output