Market Definition

The Global Carbon Trading Platforms Market encompasses the technology infrastructure, regulatory frameworks, financial intermediation services, registry systems, data analytics tools, and marketplace operations that facilitate the issuance, listing, trading, settlement, and retirement of carbon credits and emissions allowances across both compliance-based emissions trading systems and voluntary carbon markets. Carbon trading platforms serve as the operational backbone of carbon markets by providing the electronic trading environments, registry and custody infrastructure, price discovery mechanisms, counterparty matching, clearing and settlement services, and market surveillance capabilities that enable regulated entities, corporate buyers, financial intermediaries, and project developers to transact in carbon instruments including emissions allowances issued under cap-and-trade systems and carbon offset credits generated by emissions reduction and removal projects. The market spans two structurally distinct but increasingly interconnected carbon market segments: compliance carbon markets established by regulatory mandate under systems including the European Union Emissions Trading System, California-Quebec cap-and-trade program, China’s national Emissions Trading Scheme, South Korea’s Emissions Trading Scheme, the United Kingdom Emissions Trading Scheme, and regional carbon pricing programs in Canada, Australia, New Zealand, and Japan, where regulated emitters must surrender allowances equal to their verified annual greenhouse gas emissions under legally enforceable penalty provisions; and voluntary carbon markets where corporations, financial institutions, governments, and individuals purchase carbon credits representing independently verified emissions reductions or removals from project activities including avoided deforestation and forest degradation, renewable energy deployment, methane capture, direct air capture, enhanced rock weathering, blue carbon conservation, and improved cookstove distribution to offset their residual emissions, meet sustainability commitments, or advance climate action beyond regulatory requirements. Key participants include exchange operators, registry and custodian services, project developers and verifiers, corporate buyers and brokers, financial institutions, data and analytics providers, blockchain and fintech infrastructure developers, and regulatory bodies overseeing market integrity and participant compliance.

Market Insights

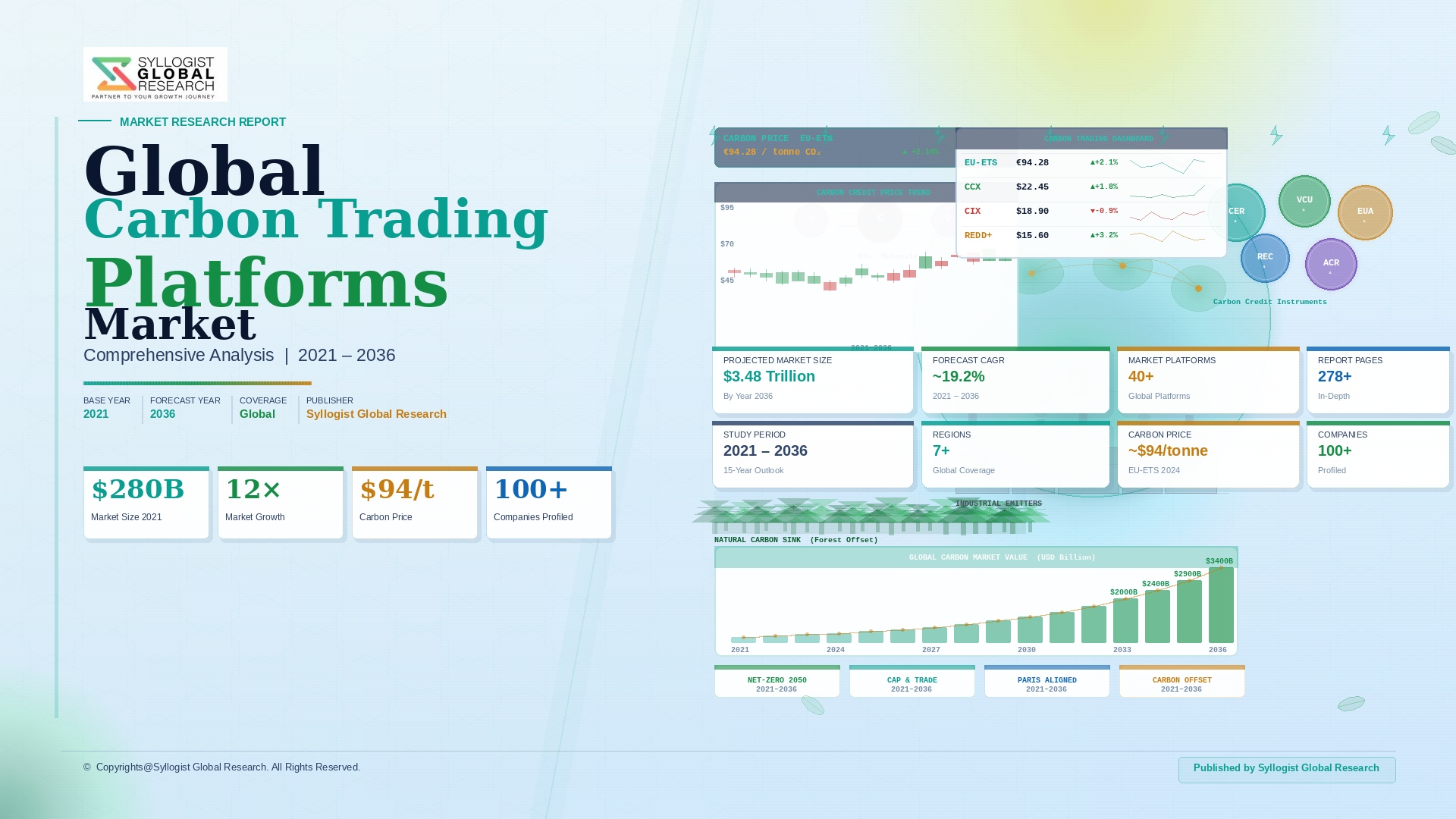

The global carbon trading platforms market was valued at approximately USD 4.8 billion in 2025, encompassing exchange transaction fees, registry services, data and analytics subscriptions, brokerage commissions, compliance management software, and platform technology licensing revenues, and is projected to reach USD 16.4 billion by 2034, advancing at a compound annual growth rate of 14.6% over the forecast period from 2027 to 2034, driven by the expanding geographic coverage and tightening stringency of compliance carbon markets, the growth and quality improvement of voluntary carbon markets following major integrity reform initiatives, and the progressive integration of carbon market participation into corporate net-zero strategy execution that is creating durable institutional demand for sophisticated carbon trading, portfolio management, and reporting platform services. The total value of carbon markets globally reached approximately USD 909 billion in 2025 based on transaction volumes and prevailing carbon prices across all compliance and voluntary markets combined, with the European Union Emissions Trading System alone accounting for approximately USD 756 billion in traded value at an average price of approximately USD 68 per metric ton of carbon dioxide equivalent and a traded volume of approximately 11.1 billion metric tons, establishing the European Union Emissions Trading System as by far the world’s largest and most liquid carbon market and the primary reference market for global carbon pricing signals. China’s national Emissions Trading Scheme, which covers approximately 5,000 power sector installations responsible for approximately 5.1 billion metric tons of carbon dioxide equivalent per year, expanded its compliance period coverage and tightened its benchmark intensity standards in 2024, with expectations for sector expansion to include steel, cement, aluminum, and petrochemicals by 2026 that would increase coverage to approximately 8 billion metric tons per year and make China’s scheme the world’s largest by emissions coverage volume, creating substantial demand for trading platform infrastructure, registry services, and compliance management technology in the Chinese and international carbon markets.

The voluntary carbon market experienced a period of significant turbulence between 2023 and 2025 following investigative journalism reports and academic analyses questioning the environmental integrity of certain forest carbon offset methodologies, with voluntary carbon credit prices declining from peaks of approximately USD 14 per metric ton for nature-based solutions credits in 2022 to below USD 5 per metric ton in 2024 before partial recovery as integrity reform initiatives including the Integrity Council for the Voluntary Carbon Market’s Core Carbon Principles and the Voluntary Carbon Markets Integrity Initiative’s claims framework progressively established clearer quality differentiation between high-integrity and lower-quality credit categories. The voluntary carbon market is projected to recover and expand significantly through the forecast period, with the operationalization of Article 6 of the Paris Agreement establishing internationally transferred mitigation outcomes between countries representing the most commercially consequential regulatory development in voluntary carbon market history, providing a government-backed framework for bilateral carbon credit transfers that carries sovereign guarantee of environmental integrity and additionality and is expected to attract institutional investor participation at a scale that the unregulated voluntary carbon market has historically been unable to sustain. The Core Carbon Principles certification framework introduced by the Integrity Council for the Voluntary Carbon Market, which has certified a growing list of approved carbon crediting methodologies and project categories meeting defined quality thresholds for additionality, permanence, measurement accuracy, and co-benefit delivery, is creating a two-tier market structure in which Core Carbon Principles-approved credits command pricing premiums of approximately 40% to 80% over non-approved equivalents, incentivizing project developers, verification bodies, and registry operators to align their processes with the elevated integrity standards and creating a higher-quality credit supply that is more suitable for corporate net-zero claim substantiation under the Science Based Targets initiative and the Voluntary Carbon Markets Integrity Initiative guidance frameworks.

The technology infrastructure and platform innovation landscape of the global carbon trading market is undergoing rapid transformation as blockchain-based registry and tokenization platforms, artificial intelligence-assisted carbon credit quality assessment tools, real-time satellite monitoring and measurement, reporting, and verification systems, and integrated enterprise carbon management software are progressively replacing the fragmented, manual, and opaque transaction processes that historically characterized voluntary carbon markets with more transparent, efficient, and trustworthy market infrastructure that can support the institutional participation scale required to meet projected voluntary carbon demand growth. Blockchain-based carbon credit tokenization platforms, which create fungible digital tokens representing each individual verified carbon credit on distributed ledger infrastructure providing immutable provenance records and automated retirement verification, are attracting technology investment from financial institutions, energy companies, and sustainability-focused venture capital funds seeking to create more liquid and transparent secondary markets for carbon credits while reducing the double-counting and retirement fraud risks that have historically undermined voluntary carbon market credibility. Remote sensing and satellite monitoring technology is revolutionizing carbon credit measurement, reporting, and verification for forest and land-use carbon projects, with companies deploying synthetic aperture radar, multispectral imaging, and lidar data fusion approaches to provide continuous biomass and deforestation monitoring at sub-hectare resolution that substantially reduces the cost and improves the accuracy of forest carbon project verification relative to periodic ground-truth survey methodologies, enabling higher-frequency credit issuance, improved additionality assessment, and more robust permanence monitoring that supports the elevated integrity standards demanded by institutional carbon credit buyers. The integration of carbon market functionality within enterprise environmental, social, and governance software platforms is creating bundled demand for compliance management, voluntary credit procurement, carbon accounting, and climate disclosure reporting capabilities that corporate sustainability teams require to manage increasingly complex and multi-jurisdictional carbon obligations.

The geopolitical and regulatory evolution of carbon trading frameworks is reshaping global market structure through the parallel development of nationally and regionally distinct compliance systems that are progressively seeking linkage, harmonization, and mutual recognition to enable cross-border carbon price efficiency and prevent carbon leakage through competing carbon cost structures across trading partners. The European Union Carbon Border Adjustment Mechanism, which requires importers of steel, cement, aluminum, fertilizers, hydrogen, and electricity from third countries to purchase carbon certificates equivalent to the embedded carbon content of imported goods at prices reflecting the EU Emissions Trading System carbon price, is creating the most consequential external driver of carbon market development outside the European Union by compelling major exporting nations including China, India, Turkey, Russia, and Ukraine to develop or strengthen their domestic carbon pricing mechanisms to avoid paying EU carbon border costs, effectively extending EU carbon pricing discipline to approximately USD 20 billion of annual EU import value and motivating non-EU governments to establish credible domestic emissions trading systems that could eventually qualify for reduced or zero Carbon Border Adjustment Mechanism obligations through demonstrated price equivalence. The Article 6.2 bilateral carbon trading framework under the Paris Agreement, with bilateral agreements announced between Switzerland and Ghana, Japan and multiple Southeast Asian partners, Singapore and Papua New Guinea, and Sweden and multiple African nations among the first commercial transactions of internationally transferred mitigation outcomes, is establishing the legal and operational precedents for a global network of sovereign carbon trading relationships that will generate demand for standardized transfer documentation, independent verification of mitigation outcomes, and registry interoperability between national carbon accounting systems that represents a growing commercial opportunity for carbon market infrastructure and platform service providers.

Key Drivers

Expanding Geographic Coverage and Tightening Stringency of Compliance Carbon Markets Globally Creating Growing Mandatory Transaction Volume and Platform Infrastructure Demand

The progressive expansion of compliance carbon market coverage to new geographies, additional industrial sectors, and tightening emissions cap trajectories aligned with national net-zero commitments is creating a structurally growing mandatory transaction volume base for carbon trading platforms whose revenue from exchange fees, registry services, and compliance management software scales directly with the number of regulated entities, traded volumes, and transaction frequency within each compliance scheme. The European Union Emissions Trading System’s Phase IV from 2021 to 2030 introduces a linear reduction factor of 4.3% per year from 2024 to 2027 and 4.4% from 2028 to 2030 in the total allowance supply, creating progressively tighter compliance conditions that increase the financial stakes of allowance procurement decisions and stimulate demand for sophisticated trading, risk management, and hedging platform capabilities among regulated entities whose carbon cost exposure at current prices represents a material financial liability requiring active management. China’s national Emissions Trading Scheme expansion to steel, cement, aluminum, aviation, and petrochemical sectors by 2026, which will increase the scheme’s coverage from approximately 5.1 billion metric tons to over 8 billion metric tons per year, represents the largest single extension of compliance carbon market coverage in history and will generate demand for exchange infrastructure, registry services, compliance management software, and verification services across approximately 10,000 additional regulated installations whose participation requires platform technology investment by both the Chinese government and the covered enterprises. The multiplication of carbon pricing initiatives in Canada, Australia, Japan, South Korea, New Zealand, Singapore, and emerging schemes in Brazil, India, Turkey, Chile, and Vietnam is creating a growing global network of compliance carbon markets that collectively require interoperable platform infrastructure supporting cross-border trading, bilateral linking, and mutual recognition of carbon instruments across national systems.

Corporate Net-Zero Commitments Under Science Based Targets Initiative, Voluntary Carbon Market Integrity Reforms, and Article 6 Paris Agreement Implementation Revitalizing Voluntary Market Demand

The wave of corporate net-zero commitments under the Science Based Targets initiative, which had certified over 7,000 companies globally as of 2025 with committed targets to reduce emissions in line with 1.5-degree Celsius pathways, is creating a growing and commercially durable demand base for high-integrity voluntary carbon credits to offset residual hard-to-abate emissions that cannot be eliminated through direct operational decarbonization within committed timelines, with the Science Based Targets initiative’s guidance allowing voluntary carbon credits for residual emissions beyond value chain mitigation efforts provided the credits meet specific integrity standards that align with Core Carbon Principles certification and beyond value chain mitigation framework requirements. The operationalization of Article 6.2 and Article 6.4 mechanisms under the Paris Agreement, following the adoption of detailed implementation rules at COP29, provides government-endorsed international carbon trading frameworks with sovereign-backed additionality guarantees that are expected to attract institutional investor participation and corporate procurement commitments at a scale substantially exceeding the historically fragmented and integrity-challenged voluntary carbon market, with the Article 6.4 mechanism designed to eventually replace the Clean Development Mechanism with a reformed UN-supervised carbon crediting system aligned with Paris Agreement accounting rules. The mandatory climate disclosure requirements progressively being implemented under the International Sustainability Standards Board climate disclosure standard, the United States Securities and Exchange Commission climate disclosure rule, the European Corporate Sustainability Reporting Directive, and equivalent national frameworks are compelling tens of thousands of listed companies to publicly disclose and account for their Scope 1, 2, and 3 greenhouse gas emissions and their net-zero progress in ways that create financial and reputational consequences for inadequate emissions reduction performance, increasing corporate demand for both direct decarbonization investment and high-quality voluntary carbon credit procurement to substantiate net-zero progress claims.

Digitalization of Carbon Market Infrastructure, Blockchain Tokenization, Satellite Monitoring Technology, and Enterprise Carbon Management Platform Integration Expanding Platform Technology Market

The systematic replacement of manual, fragmented, and opaque carbon market transaction and verification processes with digital platform infrastructure incorporating blockchain-based credit registries, satellite and remote sensing measurement, reporting, and verification capabilities, artificial intelligence credit quality assessment tools, and enterprise carbon management software integrated with trading and procurement functionality is creating a rapidly growing technology product and service market that is expanding the carbon trading platform revenue opportunity well beyond exchange transaction fees into a broader ecosystem of software, data, verification technology, and managed service offerings. The carbon credit tokenization market, in which verified carbon credits are converted into blockchain tokens enabling fractional ownership, real-time secondary market trading, automated retirement upon use, and immutable provenance tracking through the entire credit lifecycle from project registration through issuance, transfer, and retirement, attracted approximately USD 360 million in venture and growth equity investment in 2025 as financial institutions, commodity exchanges, and climate technology startups competed to establish the technical standards and market share positions that will define the digital carbon market infrastructure of the next decade. Satellite monitoring and remote sensing technology deployment for forest and blue carbon credit measurement, reporting, and verification is reducing per-project verification cost by approximately 40% to 60% relative to traditional ground-survey methodologies while simultaneously increasing monitoring frequency from annual to near-continuous assessment, enabling more accurate credit quantification, earlier detection of deforestation reversals, and reduced permanence risk that collectively improve the investability of nature-based carbon credits for institutional buyers whose fiduciary obligations require confidence in the environmental integrity of portfolio carbon assets. The integration of carbon accounting, credit procurement, compliance management, and climate disclosure reporting within unified enterprise sustainability platforms offered by software providers is driving subscription revenue growth in the corporate carbon management software segment at approximately 21.4% annually in 2025.

Key Challenges

Persistent Carbon Credit Integrity Concerns, Greenwashing Risk, and Corporate Buyer Confidence Erosion Undermining Voluntary Carbon Market Participation and Pricing

The voluntary carbon market’s structural credibility challenge, rooted in the documented overstatement of emissions reductions in certain avoided deforestation methodologies that formed the historical backbone of the market, has created a crisis of buyer confidence that has suppressed voluntary carbon credit demand, depressed credit prices, reduced project developer investment, and prompted multiple major corporate buyers to suspend or reduce their voluntary offset procurement programs pending clarity on which credit types and methodologies meet sufficiently rigorous integrity standards for defensible net-zero claim substantiation. Investigative journalism investigations published in 2023 documenting that certain prominent avoided deforestation projects issued credits representing significantly fewer emissions reductions than claimed in their verification documentation, combined with academic analyses estimating that a substantial proportion of forest conservation credits globally may have overstated their additionality and permanence, caused average voluntary carbon credit prices to decline by approximately 65% from their 2022 peaks and led several major international corporations including Shell, EasyJet, and Gucci to publicly distance themselves from their previously announced carbon offset programs, creating a market confidence crisis whose resolution through the Core Carbon Principles certification framework, improved satellite monitoring, and Article 6 operationalization is proceeding but remains incomplete as of 2025. The reputational and legal risk associated with corporate net-zero claims substantiated by low-integrity carbon credits is creating voluntary carbon market demand hesitancy among corporate legal and sustainability teams whose organizations face potential greenwashing litigation under consumer protection law in Australia, the United Kingdom, the European Union, and the United States, with the European Union’s Green Claims Directive requiring substantiation of environmental claims against standardized scientific criteria creating a regulatory constraint on voluntary offset-based net-zero marketing claims that is reducing some categories of corporate carbon credit demand while simultaneously elevating quality requirements for the credits that are purchased.

Carbon Market Fragmentation, Lack of Global Price Harmonization, and Incompatible Registry and Accounting Standards Creating Arbitrage Distortions and Compliance Complexity for International Operators

The proliferation of nationally distinct compliance carbon markets operating under different cap levels, allocation methodologies, sectoral coverage definitions, monitoring and reporting protocols, registry systems, and linkage arrangements creates a fragmented global carbon pricing landscape in which the same tonne of carbon dioxide equivalent carries dramatically different cost implications depending on the jurisdiction in which it is emitted, with EU Emissions Trading System prices averaging approximately USD 68 per metric ton in 2025 compared to approximately USD 8 to USD 12 per metric ton under China’s national Emissions Trading Scheme, USD 25 to USD 35 under the California-Quebec program, and below USD 5 in most voluntary carbon market transactions, creating carbon cost arbitrage incentives and competitiveness distortions for internationally operating companies whose production location decisions are influenced by carbon cost differentials that do not reflect true climate impact differences. Multinational corporations operating across multiple compliance carbon market jurisdictions face the complexity of managing distinct compliance obligations, reporting deadlines, allowance procurement strategies, and regulatory relationships under systems whose monitoring, reporting, and verification requirements differ sufficiently to require jurisdiction-specific compliance management processes rather than a unified global approach, creating demand for sophisticated multi-jurisdictional carbon compliance management platform capabilities but simultaneously limiting the addressable market for any single platform provider whose geographic coverage inevitably leaves gaps in the total compliance obligation portfolio of internationally operating customers. The absence of technical interoperability between the national registry systems of the European Union, China, United Kingdom, South Korea, California, and other compliance carbon markets prevents the automated cross-border transfer, mutual recognition, or credit conversion that would enable more efficient global carbon price discovery, requiring manual reconciliation processes, bilateral government negotiations, and legal documentation of any cross-system carbon credit transfer that adds significant transaction cost and complexity to international carbon trading activities.

Regulatory Uncertainty, Policy Reversal Risk, and Carbon Price Volatility Creating Investment Hesitancy and Reducing Long-Term Carbon Market Infrastructure Development Confidence

Carbon trading platform operators, project developers, institutional investors, and corporate carbon market participants face investment planning uncertainty arising from the inherent political sensitivity of carbon pricing policy, whose design, stringency, and continuity are subject to electoral cycle disruption, industry lobbying, and competing economic policy priorities in ways that create carbon price volatility and policy reversal risk that is difficult to hedge and that reduces the confidence of long-term capital investment decisions in carbon market infrastructure and abatement projects dependent on sustained carbon price signals for financial viability. The European Union Emissions Trading System carbon price has demonstrated price volatility exceeding 40% peak-to-trough within individual twelve-month periods, driven by combinations of energy price shocks affecting allowance demand, regulatory uncertainty about Phase IV reform parameters, natural gas price movements affecting fuel switching economics, and macroeconomic recession concerns reducing industrial production and associated compliance demand, creating hedging costs and mark-to-market volatility in corporate and financial institution carbon portfolios that complicate carbon asset management and reduce the attractiveness of voluntary long-term carbon credit forward purchase commitments. The partial withdrawal of the United States from international climate commitments under certain political administrations, the political opposition to carbon pricing in several major economies, and the postponement or softening of compliance carbon market implementation timelines in emerging markets including India, Indonesia, and Brazil reflect the political fragility of carbon pricing frameworks whose continuity over the twenty-to-thirty-year investment horizons of energy transition infrastructure projects and forest carbon conservation programs cannot be reliably guaranteed, creating a risk premium in carbon-dependent investment returns that reduces investment scale and increases the cost of capital for carbon-market-dependent revenue streams.

Market Segmentation

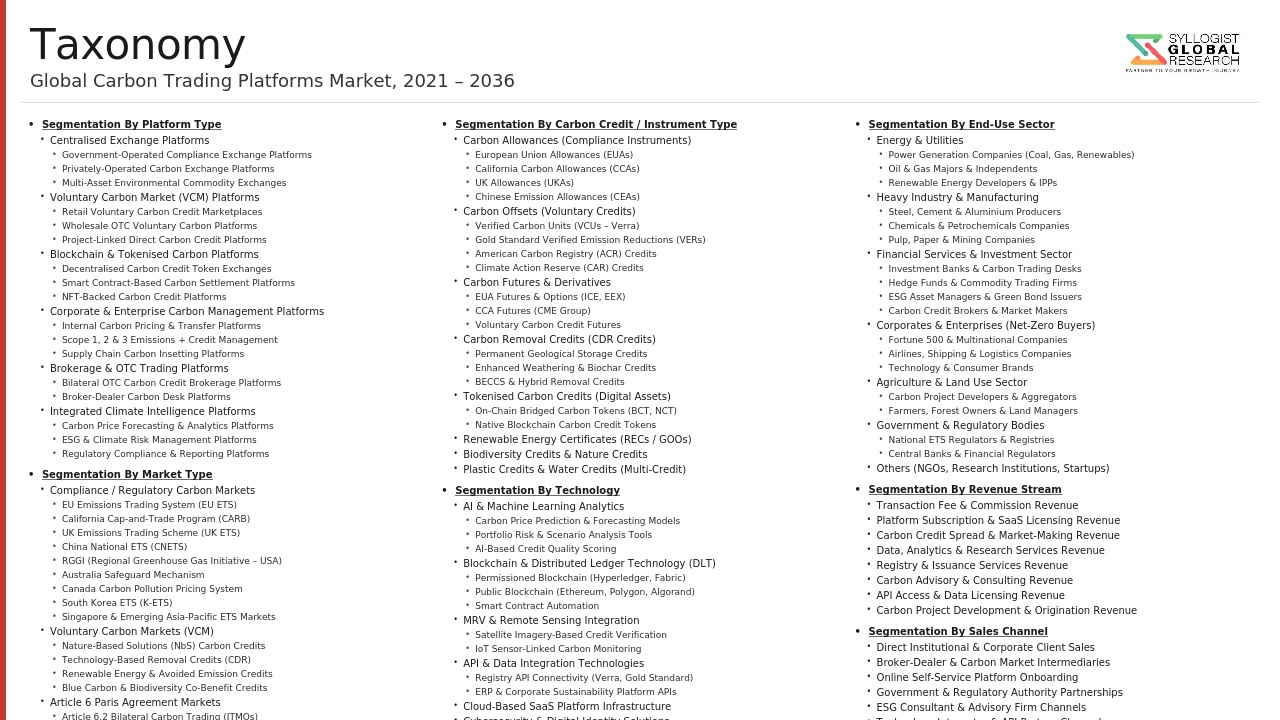

- Segmentation By Market Type

- Compliance Carbon Markets (Cap-and-Trade Emissions Trading Systems)

- Voluntary Carbon Markets (Project-Based Offset Credits)

- Article 6 Paris Agreement International Carbon Markets

- Internal Carbon Pricing and Shadow Carbon Markets

- Others

- Segmentation By Platform Type

- Exchange and Auction Platforms (Primary Issuance and Secondary Trading)

- Over-the-Counter (OTC) Brokerage and Trading Platforms

- Carbon Credit Registry and Custodian Platforms

- Carbon Credit Tokenization and Blockchain-Based Platforms

- Enterprise Carbon Management and Compliance Software

- Carbon Data, Analytics, and Pricing Information Platforms

- Measurement, Reporting, and Verification (MRV) Technology Platforms

- Others

- Segmentation By Carbon Instrument

- Emissions Allowances (EUAs, CCA, RGGI Allowances, and National ETS Permits)

- Renewable Energy Certificates (RECs and Guarantees of Origin)

- Nature-Based Carbon Credits (REDD+, Afforestation, Blue Carbon, and Soil Carbon)

- Technology-Based Carbon Credits (Direct Air Capture, BECCS, and Enhanced Rock Weathering)

- Renewable Energy and Methane Avoidance Credits

- Certified Emission Reductions (CERs) and Article 6.4 Mechanism Credits

- Internationally Transferred Mitigation Outcomes (ITMOs, Article 6.2)

- Others

- Segmentation By End User

- Compliance-Obligated Industrial Emitters

- Corporate Voluntary Buyers (Net-Zero and Sustainability-Committed Companies)

- Financial Institutions and Carbon Market Investors

- Carbon Project Developers and Aggregators

- Governments and National Carbon Market Regulators

- Airlines and Aviation Sector (CORSIA Compliance)

- Shipping Operators (FuelEU and IMO Compliance)

- Retail and Individual Carbon Offset Buyers

- Others

- Segmentation By Technology Infrastructure

- Centralized Exchange Technology (Matching Engine and Order Management)

- Distributed Ledger and Blockchain Registry Infrastructure

- Satellite and Remote Sensing MRV Technology

- Artificial Intelligence Credit Quality Assessment Tools

- Application Programming Interface (API) Integration and Data Feeds

- Cloud-Based Carbon Management Software-as-a-Service

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Carbon Trading Platforms Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by market type including compliance emissions trading systems and voluntary carbon markets, by platform type including exchange and auction platforms, OTC brokerage, registry and custody, blockchain tokenization, enterprise compliance software, data and analytics, and measurement, reporting, and verification technology, and by carbon instrument including emissions allowances, nature-based credits, technology-based credits, renewable energy certificates, and Article 6 internationally transferred mitigation outcomes, to enable platform operators, exchange technology providers, registry developers, enterprise software vendors, data analytics companies, and capital market investors to identify the highest-growth platform and instrument categories generating the most commercially durable revenue trajectories across the forecast period to 2034?

- How are the European Union Emissions Trading System Phase IV tightening trajectory, China’s national Emissions Trading Scheme sector expansion to steel, cement, aluminum, and petrochemicals by 2026, the Carbon Border Adjustment Mechanism extension to additional product categories, and the proliferation of new national carbon pricing schemes across Canada, South Korea, Singapore, Brazil, India, Turkey, Chile, and Vietnam collectively reshaping global compliance carbon market coverage, traded volume, price discovery, and cross-border linkage architecture, and what are the platform infrastructure investment requirements, registry interoperability challenges, and commercial opportunity implications of a global compliance carbon market ecosystem expanding from approximately USD 909 billion in total traded value in 2025 toward multi-trillion-dollar transaction volumes through 2034 as carbon prices tighten and sectoral coverage broadens?

- What are the current status, implementation timeline, eligible project methodologies, governance structure, credit integrity standards, and commercial trading volumes of the Article 6.2 bilateral internationally transferred mitigation outcome framework and the Article 6.4 UN-supervised carbon crediting mechanism under the Paris Agreement, and how are the bilateral agreements between Switzerland and Ghana, Japan and Southeast Asian partners, Singapore and Papua New Guinea, and Sweden and African nations establishing operational precedents for sovereign carbon credit transfers that will generate demand for platform infrastructure, registry interoperability, independent verification services, and standardized transfer documentation, and what market scale and revenue opportunity does full Article 6 operationalization represent for carbon trading platform providers and voluntary carbon market participants through 2034?

- How are the Integrity Council for the Voluntary Carbon Market Core Carbon Principles certification framework, the Voluntary Carbon Markets Integrity Initiative claims guidance, satellite-based monitoring, reporting, and verification technology deployment, and blockchain credit tokenization infrastructure collectively addressing the carbon credit integrity crisis that drove voluntary carbon credit prices down by approximately 65% from 2022 peaks, and what is the projected recovery trajectory for voluntary carbon market volumes and prices through 2034 as these integrity reforms take effect, and what differentiated pricing premiums are Core Carbon Principles-certified credits commanding over non-certified equivalents across nature-based solutions, technology-based removals, and methane avoidance credit categories as institutional and corporate buyers rebuild voluntary procurement programs on higher-integrity foundations?

- What is the current market penetration, technology architecture, commercial business models, regulatory compliance status, and competitive positioning of blockchain-based carbon credit tokenization and registry platforms relative to traditional centralized registry systems operated by Verra, Gold Standard, and American Carbon Registry, and what institutional investor adoption, corporate buyer acceptance, and regulatory recognition milestones are required for tokenized carbon credits to achieve sufficient market liquidity, price transparency, and integrity credibility to displace or substantially complement traditional registry infrastructure as the primary carbon credit custody and trading mechanism, and how are major financial institutions, commodity exchanges, and climate technology companies structuring their blockchain carbon market investments to capture this platform technology transition opportunity?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Carbon Credit Quality, Integrity & Additionality Verification Risk

- Regulatory, Policy Discontinuity & Carbon Price Volatility Risk

- Greenwashing, Reputational & Market Credibility Risk

- Technology, Cybersecurity & Platform Operational Risk

- Liquidity, Counterparty & Settlement Risk in Carbon Markets

- Regulatory Framework & Standards

- Compliance Carbon Market Regulation: EU ETS (EU 2003/87/EC Revised), UK ETS, China National ETS, California Cap-and-Trade, RGGI & Other National and Regional ETS Frameworks

- Paris Agreement Article 6 Implementation: Article 6.2 Bilateral Cooperation, Article 6.4 UN-Supervised Mechanism, Corresponding Adjustment Rules & ITMO Accounting

- Voluntary Carbon Market Integrity Frameworks: VCMI Code of Practice, ICVCM Core Carbon Principles, ICROA Code of Best Practice & Corporate Net Zero Claim Standards

- Carbon Credit Standard & Certification Bodies: Verra VCS, Gold Standard, American Carbon Registry (ACR), Climate Action Reserve (CAR) & Emerging Nature-Based & Removal Standards

- Financial Market Regulation for Carbon Trading Platforms: MiFID II, EMIR, CFTC Oversight of Carbon Derivatives, Market Abuse Regulation (MAR) & AML/KYC Compliance for Carbon Registries

- Global Carbon Trading Platforms Market Outlook

- Market Size & Forecast by Value (Platform Revenue, Transaction Value & AUM)

- Market Size & Forecast by Volume (Tonnes of CO2 Equivalent Traded)

- Market Size & Forecast by Platform Type

- Compliance Carbon Exchange & ETS Trading Platform

- Voluntary Carbon Market (VCM) Exchange & Marketplace

- Hybrid Compliance & Voluntary Carbon Trading Platform

- Over-the-Counter (OTC) Bilateral Carbon Trading Platform & Broker Desk

- Blockchain & Tokenised Digital Carbon Credit Trading Platform

- Carbon Credit Registry, Issuance & Retirement Platform

- Carbon Project Development, Aggregation & Pre-Sale Platform

- Corporate Internal Carbon Pricing & Intra-Company Carbon Trading Platform

- Market Size & Forecast by Carbon Market Type

- Compliance Market: Cap-and-Trade & Emissions Trading Scheme (ETS)

- Voluntary Carbon Market (VCM): Corporate & Individual Offset Procurement

- Article 6 International Carbon Market: ITMOs, Article 6.2 & Article 6.4 Mechanism

- Sectoral Compliance Market: CORSIA (Aviation) & IMO Shipping Carbon Market

- Result-Based Finance & Pay-for-Performance Carbon Programme

- Market Size & Forecast by Carbon Credit & Asset Type

- EU ETS Allowances (EUAs) & EU Aviation Allowances (EUAAs)

- Regional ETS Allowances (UK ETS UKAs, California ARB CCA, RGGI, China CEAs, Korea KAUs)

- Avoided Deforestation & REDD+ Forest Carbon Credits (VCS REDD+, Gold Standard REDD+)

- Renewable Energy & Technology-Based Carbon Credits (Gold Standard RE, ACR, CDM CERs Legacy)

- Nature-Based Solution (NbS) Credits (Blue Carbon, Soil Carbon & Grassland Restoration)

- Carbon Removal & Carbon Dioxide Removal (CDR) Credits (BECCS, DAC, Biochar, Enhanced Weathering)

- Article 6.4 Authorised Mitigation Outcome (A6.4ER) Credit

- Energy Efficiency, Cookstove, Clean Water & Community-Based Carbon Credits

- Market Size & Forecast by Trading Mechanism

- Spot Market & Physical Carbon Credit Trading

- Futures, Forwards, Options & Carbon Derivatives

- Government & Regulator-Run Auction & Primary Allocation

- OTC Bilateral Negotiation & Broker-Facilitated Deal

- Exchange-Traded Fund (ETF), ETP & Carbon-Linked Financial Product

- Tokenised & On-Chain Digital Carbon Credit Transaction

- Market Size & Forecast by Component

- Trading Platform & Exchange Matching Engine Software

- Carbon Credit Registry, Issuance, Transfer & Retirement Infrastructure

- MRV (Monitoring, Reporting & Verification) Tools & Project Data Management

- Carbon Analytics, Price Discovery, Benchmarking & Market Data Feed

- Compliance Reporting, Regulatory Filing & Risk Management Tools

- API Integration, Data Feed & Third-Party Connectivity Services

- Market Size & Forecast by End-User

- Compliance Buyers: ETS-Regulated Entities in Power, Industrial & Aviation Sectors

- Corporate Voluntary Buyers with Net Zero & Science-Based Target Commitments

- Carbon Trader, Broker, Market Maker & Carbon Asset Manager

- Carbon Project Developer, Originator & Aggregator

- ESG-Focused Financial Institution, Bank & Investment Fund

- Government, Regulatory Body & National Climate Authority

- Market Size & Forecast by Sales Channel

- Direct Exchange Membership, Trading Seat & Platform Subscription

- Carbon Broker, Intermediary & Structured Trade Desk

- API, White-Label Platform Licensing & SaaS Technology Integration

- Corporate Procurement Platform & Sustainability Advisory Channel

- North America Carbon Trading Platforms Market Outlook

- Market Size & Forecast

- By Value (Platform Revenue & Transaction Value)

- By Volume (Tonnes of CO2 Equivalent Traded)

- By Platform Type

- By Carbon Market Type

- By Carbon Credit & Asset Type

- By Trading Mechanism

- By Component

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Carbon Trading Platforms Market Outlook

- Market Size & Forecast

- By Value (Platform Revenue & Transaction Value)

- By Volume (Tonnes of CO2 Equivalent Traded)

- By Platform Type

- By Carbon Market Type

- By Carbon Credit & Asset Type

- By Trading Mechanism

- By Component

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Carbon Trading Platforms Market Outlook

- Market Size & Forecast

- By Value (Platform Revenue & Transaction Value)

- By Volume (Tonnes of CO2 Equivalent Traded)

- By Platform Type

- By Carbon Market Type

- By Carbon Credit & Asset Type

- By Trading Mechanism

- By Component

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Carbon Trading Platforms Market Outlook

- Market Size & Forecast

- By Value (Platform Revenue & Transaction Value)

- By Volume (Tonnes of CO2 Equivalent Traded)

- By Platform Type

- By Carbon Market Type

- By Carbon Credit & Asset Type

- By Trading Mechanism

- By Component

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Carbon Trading Platforms Market Outlook

- Market Size & Forecast

- By Value (Platform Revenue & Transaction Value)

- By Volume (Tonnes of CO2 Equivalent Traded)

- By Platform Type

- By Carbon Market Type

- By Carbon Credit & Asset Type

- By Trading Mechanism

- By Component

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Carbon Trading Platforms Market Outlook

- Market Size & Forecast

- By Value (Platform Revenue & Transaction Value)

- By Volume (Tonnes of CO2 Equivalent Traded)

- By Platform Type

- By Carbon Market Type

- By Carbon Credit & Asset Type

- By Trading Mechanism

- By Component

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Germany, France, United Kingdom, Netherlands, Sweden, Norway, Switzerland, Belgium, China, Japan, South Korea, India, Australia, New Zealand, Singapore, Brazil, Chile, Mexico, South Africa, UAE, Saudi Arabia

- Technology Landscape & Innovation Analysis

- Exchange Matching Engine, Order Book Architecture & Carbon Credit Trading Platform Technology Deep-Dive

- Carbon Credit Registry, Issuance, Serial Number Tracking, Transfer & Retirement Technology

- MRV (Monitoring, Reporting & Verification) Technology: Satellite Remote Sensing, IoT Sensor, AI-Based Forest Carbon Monitoring & Project Data Validation

- Blockchain, Distributed Ledger Technology (DLT) & Tokenised Carbon Credit Platform Architecture

- Carbon Credit Pricing, Analytics, Reference Price Benchmark & Real-Time Market Data Technology

- Article 6 International Registry Linking, Corresponding Adjustment Accounting & ITMO Transfer Technology

- AI, Machine Learning & Natural Language Processing for Carbon Market Surveillance, Credit Quality Assessment & Greenwashing Detection

- Patent & IP Landscape in Carbon Trading Platform Technologies

- Value Chain & Supply Chain Analysis

- Carbon Project Origination, Feasibility Assessment & Methodology Selection

- MRV Service Provider, Third-Party Validator & Verifier Supply Chain

- Carbon Standard Body, Registry & Issuance Infrastructure

- Carbon Exchange, Trading Platform & Market Infrastructure Operator

- Carbon Broker, Trader, Market Maker & Carbon Asset Manager Layer

- Corporate Buyer, Compliance Entity & Retail Carbon Credit End-User

- Post-Trade, Settlement, Custody, Audit & Carbon Credit Retirement Service

- Pricing Analysis

- Compliance Carbon Allowance Price Analysis: EU ETS, UK ETS, California ARB, RGGI & China ETS Carbon Price Benchmarking & Forecast

- Voluntary Carbon Credit Price Analysis by Credit Type, Standard & Project Category (Nature-Based, Removal, Renewable, Cookstove)

- Carbon Credit Price Premium & Discount Analysis: Co-Benefits, Additionality Rating, Vintage & Geographical Origin Price Differentials

- Carbon Futures & Derivatives Pricing: Carbon Forward Curve, Options Pricing & Roll Yield Analysis

- Platform Fee, Transaction Cost, Brokerage Commission & Registry Service Fee Structure Analysis

- Carbon Credit Price Convergence Analysis: Compliance vs. Voluntary Market Price Gap & Article 6 Price Impact Modelling

- Sustainability & Environmental Analysis

- Carbon Credit Environmental Integrity Assessment: Additionality, Permanence, Leakage & Measurability Criteria for Platform-Listed Carbon Credits

- Co-Benefits & Social Impact Analysis: Biodiversity, Community Livelihood, Gender Equality & SDG Contribution of Carbon Project Types

- Carbon Trading Platform Carbon Footprint: Energy Consumption, Data Centre Emission & Net Zero Operational Target

- Greenwashing Risk, Corporate Net Zero Claim Integrity & VCMI / ICVCM Alignment for Carbon Platform Participants

- Regulatory-Driven Sustainability: SEC Climate Disclosure, SFDR Taxonomy Alignment, CORSIA Sustainability Criteria & Carbon Market ESG Reporting Standard

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Platform Type & Carbon Market)

- Top 10 Players Market Share by Transaction Volume & Platform Revenue

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Platform Type, Carbon Market Type & Geography

- Player Classification

- Global Diversified Exchange & Multi-Asset Trading Platform Operators with Carbon Market Division

- Specialist Voluntary Carbon Market Exchange & Marketplace Operators

- Compliance Carbon Exchange & ETS Auction Platform Operators

- Blockchain, DLT & Tokenised Carbon Credit Platform Companies

- Carbon Registry, Standard Body & Issuance Infrastructure Providers

- Carbon Data, Analytics, MRV & Market Intelligence Platform Providers

- Carbon Broker, OTC Dealer & Structured Carbon Trade Desk Operators

- Corporate Carbon Management, Offset Procurement & Sustainability Platform Companies

- Competitive Analysis Frameworks

- Market Share Analysis by Platform Type, Carbon Market Type & Region

- Company Profile

- Company Overview & Headquarters

- Carbon Trading Platform Products, Services & Technology Portfolio

- Key Customer Relationships & Listed Carbon Credit Reference Projects

- Platform Infrastructure Footprint & Annual Trading Volume Capacity

- Revenue (Carbon Platform Segment) & Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Platform Launches, Listings, Regulatory Approvals)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Platform Type, Carbon Market Type, Credit Asset Type, End-User & Geography

- White Space Opportunity Analysis

- Strategic Output

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Platform Operations & Market Infrastructure Excellence Strategy

- Geographic Expansion & New Market Entry Strategy

- Customer & Market Participant Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability, Carbon Integrity & ESG Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)