Global Concrete Admixtures Market By Admixture Type, By Function, By Concrete Application, By Form, By Technology, By End User Industry, By Region, Competition, Forecast & Opportunities, 2021-2034F

Market Definition

Concrete admixtures are chemical formulations added to fresh concrete or mortar mixes before or during mixing to modify specific properties of fresh and hardened concrete, including workability, setting time, hydration kinetics, mechanical strength, durability, permeability, freeze-thaw resistance, and aesthetic performance across ready-mix concrete, precast concrete, shotcrete, self-compacting concrete, high-performance concrete, and specialty construction applications. The Global Concrete Admixtures Market encompasses the development, manufacturing, formulation, distribution, and field application of chemical admixtures including water-reducing plasticizers, polycarboxylate ether (PCE) superplasticizers, set retarders, set accelerators, air-entraining admixtures, waterproofing admixtures, corrosion inhibitors, shrinkage-reducing admixtures, viscosity-modifying admixtures, anti-washout admixtures, and specialty performance admixtures deployed across construction, infrastructure, and precast concrete applications globally.

The concrete admixtures market includes liquid and powder formulations engineered for specified dosage rates, compatibility with diverse cement chemistries, ambient temperature performance envelopes, and end-application requirements across high-performance and conventional concrete applications. Market participants include established construction chemicals producers, specialty chemical companies operating concrete admixtures divisions, regional admixture formulators, contract manufacturers, distributors, and end-user industries spanning ready-mix concrete producers, precast concrete manufacturers, infrastructure contractors, commercial and residential builders, and specialty concrete operators. The concrete admixtures market also covers value-added services including custom formulation development, mix design optimization, on-site technical service, dosing equipment supply, and durability performance certification support. The scope explicitly excludes supplementary cementitious materials (SCMs) including fly ash, ground granulated blast furnace slag, and silica fume that are typically classified as cementitious additions rather than admixtures, focusing exclusively on chemical admixtures engineered to modify concrete fresh and hardened properties through targeted chemical functionality globally.

Market Insights

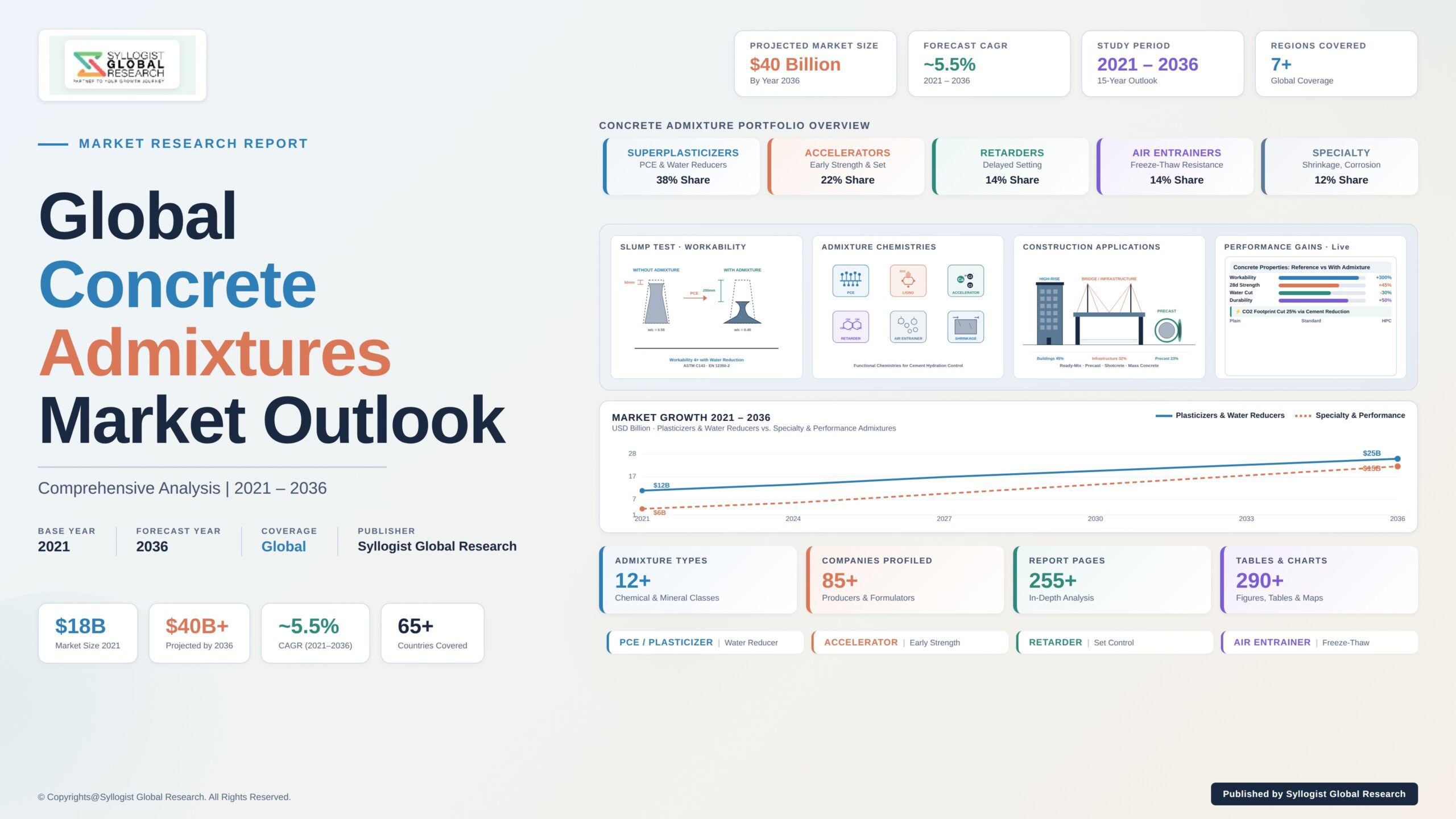

The global concrete admixtures market is undergoing a sustained expansion phase, shaped by accelerating global infrastructure investment programs, sustained urbanization driving residential and commercial construction activity in Asia-Pacific and the Middle East, growing precast concrete adoption supporting modular and prefabricated construction methodologies, tightening sustainability mandates favoring low-carbon and durability-optimized concrete formulations, and the structural shift toward high-performance concrete applications requiring advanced admixture chemistries. The concrete admixtures market was valued at approximately USD 21.4 billion in 2025 and is projected to reach USD 38.5 billion by 2034, advancing at a compound annual growth rate of 6.7% through the forecast period, as ready-mix concrete producers, precast concrete manufacturers, infrastructure contractors, and specialty concrete operators scale admixture procurement across mature and emerging construction operating regions globally.

The concrete admixtures market trajectory is being reshaped by the structural dominance of polycarboxylate ether (PCE) superplasticizer chemistry across high-performance concrete applications, accelerating adoption of low-carbon concrete formulations enabled by sophisticated admixture systems, the deployment of self-healing concrete admixtures supporting infrastructure durability extension, and the emerging commercialization of bio-based and renewable feedstock admixtures supporting circular economy procurement preferences. Polycarboxylate ether superplasticizers account for over 65% of global superplasticizer consumption within the concrete admixtures market, propelled by superior water reduction performance, sustained slump retention, and chemistry tailoring flexibility supporting cement and supplementary cementitious material combinations. Low-carbon concrete formulations enabled by advanced admixture systems can achieve 30% to 50% reductions in embodied carbon per cubic meter relative to conventional concrete mixes, generating sustained procurement preference within the concrete admixtures market among infrastructure contractors and developers operating under net-zero commitments and embodied carbon procurement frameworks.

Plasticizers and superplasticizers represent the largest admixture type segment within the concrete admixtures market, propelled by sustained demand from ready-mix concrete, precast concrete, and high-performance concrete applications requiring water reduction, workability enhancement, and slump retention performance. Set accelerators and set retarders represent the second largest admixture type segment within the concrete admixtures market, supported by sustained demand from infrastructure construction, mass concrete pours, hot-weather and cold-weather concreting applications. Ready-mix concrete represents the largest application segment within the concrete admixtures market in volume terms, fueled by sustained urbanization, infrastructure investment, and commercial construction activity across major operating regions globally. Precast concrete represents the fastest-growing application segment within the concrete admixtures market, propelled by accelerating modular and prefabricated construction methodology adoption, infrastructure precast segment expansion, and sustained capacity additions among precast concrete manufacturers serving residential, commercial, and infrastructure end-user markets.

Asia-Pacific represents the largest regional market within the concrete admixtures market, anchored by sustained infrastructure investment in China, India, Indonesia, Vietnam, and Southeast Asia, expanding residential and commercial construction activity, accelerating precast concrete capacity additions, and continued urbanization driving concrete consumption across mature and emerging operating regions. China hosts the largest concentration of concrete admixtures consumption globally, accounting for over 35% of global cement and concrete consumption, supported by sustained infrastructure investment under national construction programs. North America represents the second largest regional position within the concrete admixtures market, supported by accelerating infrastructure investment under the United States Infrastructure Investment and Jobs Act, sustained residential and commercial construction activity, and growing precast concrete adoption. Europe occupies the third major regional position within the concrete admixtures market, shaped by stringent sustainability regulations driving low-carbon concrete adoption, mature precast concrete capacity in Germany, the Netherlands, and Scandinavia, and continued infrastructure rehabilitation investment supporting accelerated concrete admixtures procurement across the concrete admixtures market value chain globally.

Key Drivers

Global Infrastructure Investment Programs, IIJA-Supported Construction Activity, and Accelerating Asia-Pacific Capacity Buildout Driving Sustained Concrete Admixtures Procurement

The acceleration of global infrastructure investment programs, sustained capital deployment under the United States Infrastructure Investment and Jobs Act, expanding infrastructure construction in Asia-Pacific and the Middle East, and continued urbanization-driven construction activity are collectively driving durable procurement demand for concrete admixtures within the concrete admixtures market across major construction operating regions globally. The United States Infrastructure Investment and Jobs Act provides approximately USD 1.2 trillion in infrastructure spending commitments over a 10-year horizon, supporting bridges, highways, water systems, power infrastructure, and broadband expansion that generate sustained ready-mix concrete and precast concrete consumption alongside corresponding concrete admixtures procurement. India’s National Infrastructure Pipeline targets approximately USD 1.4 trillion in infrastructure investment through 2025 supporting roads, railways, ports, airports, and urban infrastructure, while sustained Chinese infrastructure investment programs continue to support world-leading concrete and concrete admixtures consumption volumes within the concrete admixtures market. Middle Eastern infrastructure investment including Saudi Arabia’s Vision 2030 NEOM, the United Arab Emirates infrastructure investment, and Qatar post-FIFA infrastructure programs reinforces sustained concrete admixtures procurement. Specialty chemical producers are structuring multi-year supply commitments aligning admixture supply with infrastructure project timelines, generating long-duration revenue commitments across the concrete admixtures market value chain globally and reinforcing continued capital deployment toward dedicated concrete admixtures production capacity and technical service support infrastructure.

Sustainability Mandates, Low-Carbon Concrete Formulation Procurement, and Embodied Carbon Reduction Driving Advanced Admixture Technology Adoption

Intensifying sustainability mandates from major contractors, developers, and infrastructure agencies, accelerating low-carbon concrete formulation procurement, and expanding embodied carbon reduction commitments are collectively driving sustained procurement of advanced admixture technologies within the concrete admixtures market across construction and infrastructure operating regions globally. Global cement production accounts for approximately 7% to 8% of global anthropogenic carbon dioxide emissions, with concrete-related emissions representing a focal point for decarbonization efforts among developers, contractors, infrastructure agencies, and material producers within the concrete admixtures market. Low-carbon concrete formulations enabled by advanced superplasticizer chemistries, supplementary cementitious material optimization, and viscosity-modifying admixture systems can achieve 30% to 50% reductions in embodied carbon per cubic meter relative to conventional concrete mixes, generating sustained procurement preference among contractors operating under corporate net-zero commitments, green building certification frameworks including LEED and BREEAM, and embodied carbon procurement mandates. Specialty chemical producers are investing substantial research and development capital in low-carbon concrete admixture chemistry development, supporting customer reformulation toward reduced clinker content concrete formulations, alkali-activated concrete systems, and carbonation-cured concrete applications. Major construction operators are structuring multi-year concrete admixtures supply commitments aligning admixture procurement with sustainability targets and embodied carbon reduction roadmaps, reinforcing continued investment across the concrete admixtures market value chain.

Precast Concrete Capacity Expansion, Modular Construction Adoption, and High-Performance Concrete Specification Driving Specialty Admixture Procurement

Accelerating precast concrete capacity expansion, sustained modular and prefabricated construction methodology adoption, and tightening high-performance concrete specification requirements are collectively driving sustained procurement of specialty admixtures within the concrete admixtures market across precast concrete and high-performance concrete operating regions globally. Global precast concrete production volumes scaled at compound annual rates exceeding 7% between 2021 and 2025, propelled by sustained productivity advantages, quality consistency benefits, and construction schedule compression that modular and prefabricated construction methodologies deliver relative to conventional cast-in-place construction. High-performance concrete applications including high-strength concrete (50 megapascals and above), self-compacting concrete, ultra-high-performance concrete, and fiber-reinforced concrete generate elevated admixture consumption intensity relative to conventional concrete applications, with admixture dosage rates and chemistry sophistication scaling progressively with concrete performance targets within the concrete admixtures market. Major precast concrete manufacturers and high-performance concrete contractors are structuring multi-year specialty admixture supply commitments aligning concrete admixtures procurement with capacity expansion timelines and project pipelines, generating durable revenue commitments and reinforcing continued capital deployment toward dedicated specialty admixture production capacity, formulation engineering, and customer technical service support across the concrete admixtures market value chain.

Key Challenges

Raw Material Cost Volatility, Petrochemical Feedstock Price Fluctuations, and Margin Pressure Across Concrete Admixtures Producers

The concrete admixtures market continues to face material raw material cost volatility, sustained petrochemical feedstock price fluctuations, and persistent margin pressure across producers supplying superplasticizers, water-reducing plasticizers, and specialty admixture products to global ready-mix concrete and precast concrete customers. Raw material costs for polycarboxylate ether (PCE) superplasticizer chemistry, including methacrylic acid, methacrylate esters, polyethylene glycol intermediates, and specialty monomer feedstocks, experienced sustained price volatility of 20% to 40% between 2021 and 2024, generating substantial margin pressure within the concrete admixtures market and complicating long-term pricing commitments to ready-mix concrete and precast concrete customers. Petrochemical feedstock price fluctuations driven by crude oil pricing variability, ethylene supply disruptions, and shifting Asian capacity dynamics continue to generate margin uncertainty for concrete admixtures producers planning multi-year capacity investments and customer supply commitments. Specialty intermediate sourcing complexity for niche admixture variants including shrinkage-reducing admixtures, corrosion inhibitors, and specialty viscosity modifiers adds further supply chain risk, with limited global production capacity for select intermediates generating supply concentration risk. The combined effect of raw material cost volatility, petrochemical feedstock fluctuations, and intermediate sourcing complexity continues to constrain margin stability and complicate strategic capital deployment decisions within the concrete admixtures market across global operating regions and producer capacity expansion plans.

Cement Chemistry Variability, Supplementary Cementitious Material Compatibility, and Field Performance Reproducibility Challenges

The concrete admixtures market continues to confront persistent cement chemistry variability across global cement producers, sustained supplementary cementitious material compatibility complexity, and field performance reproducibility challenges that collectively elevate technical service support requirements, complicate customer mix design specification, and constrain admixture performance consistency across diverse construction operating environments. Cement chemistry variability including alkali content, sulfate content, C3A levels, fineness, and reactivity differences across cement producers and across cement production batches affects admixture-cement interaction, slump retention performance, setting time control, and ultimate strength development, requiring concrete admixtures producers to maintain extensive cement-admixture compatibility databases and customer technical service capability within the concrete admixtures market. Supplementary cementitious material (SCM) compatibility, including the use of fly ash, ground granulated blast furnace slag, silica fume, and limestone fillers alongside admixtures, generates additional formulation complexity with each SCM type generating distinct admixture interactions that affect concrete performance characteristics. Field performance reproducibility challenges, including variations in ambient temperature, aggregate moisture content, mixing equipment performance, and field handling protocols, generate variability in achieved concrete performance relative to laboratory mix design targets, requiring concrete admixtures producers to invest substantial customer technical service capability supporting field troubleshooting and mix design optimization across the concrete admixtures market value chain globally.

Logistics Cost Sensitivity, Regional Price Competition, and Local Production Capacity Concentration Constraining Margin Economics

The concrete admixtures market continues to face material logistics cost sensitivity affecting cross-regional supply commitments, persistent regional price competition from local producers operating dedicated production capacity, and concentrated competitive dynamics that collectively constrain margin economics and complicate strategic capacity deployment decisions across producers globally. Concrete admixtures are typically supplied in liquid form at concentrations of 30% to 50% active solids, with water comprising the balance, generating substantial freight cost per unit of active ingredient that materially affects competitive economics for cross-regional supply commitments within the concrete admixtures market. Logistics cost sensitivity drives producer preference for dedicated regional production capacity located within economic freight radius of customer ready-mix concrete plants and precast concrete production facilities, constraining cross-regional supply commitments and limiting the geographic reach of premium specialty admixture product lines. Regional price competition from local producers operating dedicated production capacity adds further margin pressure, with mature Asian and select emerging market operating regions hosting substantial local concrete admixtures production capacity that competes on price for commodity admixture segments. The combined effect of logistics cost sensitivity, regional price competition, and concentrated competitive dynamics continues to constrain margin economics and reinforce structural reliance on regional production capacity deployment within the concrete admixtures market value chain globally.

Market Segmentation

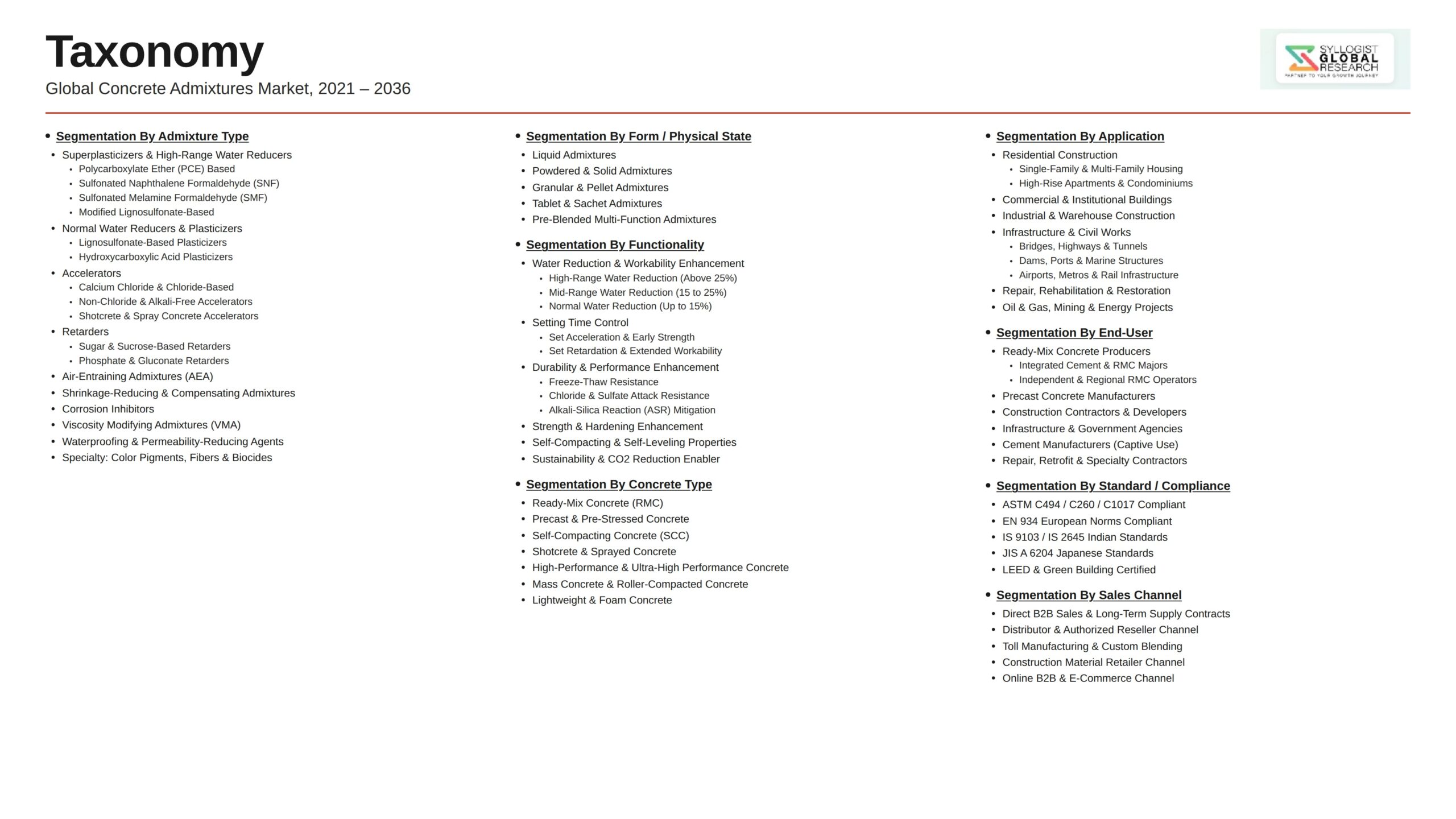

- Segmentation By Admixture Type

- Plasticizers and Water Reducers

- Polycarboxylate Ether (PCE) Superplasticizers

- Naphthalene Sulfonate Superplasticizers

- Melamine Sulfonate Superplasticizers

- Set Retarders

- Set Accelerators

- Air-Entraining Admixtures

- Waterproofing Admixtures

- Corrosion Inhibitors

- Shrinkage-Reducing Admixtures

- Viscosity-Modifying Admixtures

- Anti-Washout Admixtures

- Specialty and Performance Admixtures

- Others

- Segmentation By Function

- Water Reduction and Workability Enhancement

- Set Time Control (Acceleration and Retardation)

- Air Entrainment and Freeze-Thaw Resistance

- Waterproofing and Permeability Reduction

- Corrosion Protection

- Shrinkage and Cracking Mitigation

- Strength Enhancement

- Specialty Performance Modification

- Segmentation By Concrete Application

- Ready-Mix Concrete

- Precast Concrete

- Shotcrete and Sprayed Concrete

- Self-Compacting Concrete

- High-Performance and Ultra-High-Performance Concrete

- Mass Concrete (Dams, Foundations)

- Fiber-Reinforced Concrete

- Carbon-Cured Concrete

- Others

- Segmentation By Form

- Liquid

- Powder

- Granular

- Specialty Concentrated Forms

- Segmentation By Technology

- Conventional Petrochemical-Derived Admixtures

- Bio-Based and Renewable Admixtures

- Low-Carbon Concrete-Enabling Admixtures

- Self-Healing Concrete Admixtures

- Segmentation By End User Industry

- Ready-Mix Concrete Producers

- Precast Concrete Manufacturers

- Infrastructure Contractors

- Commercial and Residential Builders

- Specialty Concrete Operators

- Cement and Concrete Product Manufacturers

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Concrete Admixtures Market in 2025, projected through 2034, segmented by admixture type, function, concrete application, and form, enabling specialty chemical producers, formulators, distributors, and construction industry procurement teams to identify highest-growth segments and most durable revenue opportunities across the concrete admixtures landscape?

- How are ready-mix concrete producers, precast concrete manufacturers, infrastructure contractors, and specialty concrete operators structuring procurement frameworks for concrete admixtures, and which commercial models, including spot purchase, multi-year supply agreements, mix design partnership, and technical service-bundled contracts, are shaping commercial deployment economics within the concrete admixtures market through 2034?

- What sustainability mandates, embodied carbon reduction commitments, low-carbon concrete formulation procurement, and green building certification dynamics are reshaping admixture chemistry preferences and reformulation timelines across mature regulatory jurisdictions and developer procurement frameworks?

- Which admixture types, including polycarboxylate ether superplasticizers, naphthalene-based superplasticizers, set accelerators, set retarders, air-entraining admixtures, waterproofing admixtures, and specialty performance admixtures, are gaining the strongest procurement traction across ready-mix, precast, high-performance, and specialty concrete applications, and what performance, compatibility, and total cost of ownership metrics are shaping technology selection?

- How is the competitive landscape structured among established construction chemicals producers, specialty chemical companies operating admixture divisions, regional admixture formulators, contract manufacturers, and emerging bio-based admixture developers within the concrete admixtures market, and what partnership, acquisition, and platform expansion strategies are enabling new entrants to compete against incumbent admixture producers?

- What infrastructure investment programs, IIJA-supported construction activity, modular and prefabricated construction adoption, and high-performance concrete specification trends are reshaping admixture application engineering, capacity planning, and customer technical service expectations across the concrete admixtures market globally?

- Which regional markets, including Asia-Pacific, North America, Europe, and the Middle East, are projected to generate the largest incremental concrete admixtures procurement opportunities through 2034, and what infrastructure investment, construction activity, sustainability mandate, and precast capacity factors are shaping capability investment priorities and supplier selection decisions in each regional concrete admixtures market?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Cement Industry Cycle Volatility, Construction Activity Variability & Customer Demand Fluctuation Risk

- Raw Material Cost Volatility, Polycarboxylate Ether Feedstock & Specialty Polymer Sourcing Risk

- Regional Standard Variability, Testing and Approval Burden & Project-Specific Qualification Risk

- Supplementary Cementitious Material Availability, Fly Ash Phasedown & Coal-Fired Plant Closure Risk

- Sustainability Mandate Compliance, Carbon-Reduced Cement Adoption & Low-Carbon Admixture Investment Risk

- Regulatory Framework & Standards

- Construction Material Standards (ASTM C494, EN 934, BIS IS 9103) & Performance Certification Frameworks

- Cement & Concrete Sustainability Standards, Low-Carbon Cement & Carbon Reduction Frameworks

- REACH Registration, CLP Classification & EU Chemical Authorisation Frameworks

- US Toxic Substances Control Act (TSCA), EPA Chemical Compliance & Hazardous Substance Reporting Standards

- Globally Harmonised System (GHS), Hazard Communication & Workplace Safety Compliance

- Global Concrete Admixtures Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Admixture Consumption in Million Tonnes and Number of Active Manufacturing Facilities)

- Market Size & Forecast by Admixture Type

- Plasticizers

- Superplasticizers and High-Range Water Reducers (HRWR)

- Retarders

- Accelerators

- Air-Entraining Admixtures

- Water Reducers

- Fly Ash

- Slag

- Silica Fume

- Metakaolin and Calcined Clay

- Corrosion Inhibitors

- Shrinkage-Reducing Admixtures

- Viscosity-Modifying Admixtures

- Others

- Market Size & Forecast by Function

- Workability Enhancement

- Setting Time Control

- Strength Enhancement

- Durability Enhancement

- Special Property (Self-Compacting, Self-Healing, Rapid Hardening)

- Others

- Market Size & Forecast by Form

- Liquid

- Powder

- Granular

- Others

- Market Size & Forecast by Application

- Ready-Mix Concrete

- Precast Concrete

- Shotcrete and Sprayed Concrete

- Underwater Concrete

- Self-Compacting Concrete

- High-Performance and High-Strength Concrete

- Mass Concrete (Dams, Foundations)

- Repair Mortars and Grouts

- Others

- Market Size & Forecast by End-User

- Residential Construction

- Commercial and Institutional Construction

- Industrial Construction

- Infrastructure (Roads, Bridges, Tunnels, Airports)

- Energy Infrastructure (Wind Energy Foundations, Nuclear)

- Marine and Offshore Construction

- Mining

- Others

- Market Size & Forecast by Construction Sector

- New Construction

- Repair and Rehabilitation

- Restoration

- Market Size & Forecast by Performance Tier

- Standard

- High-Performance

- Specialty and Premium

- Market Size & Forecast by Sales Channel

- Direct Manufacturer-to-Customer Supply Contracts

- Specialty Construction Chemical Distributor & Trader Channel

- Custom Formulation & Joint Development Partnerships

- Licensed Production & Contract Manufacturing Arrangements

- Aftermarket Mix Design Optimisation & Technical Service Contracts

- North America Concrete Admixtures Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Admixture Consumption in Million Tonnes and Number of Active Manufacturing Facilities)

- By Admixture Type

- By Function

- By Form

- By Application

- By End-User

- By Construction Sector

- By Performance Tier

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Concrete Admixtures Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Admixture Consumption in Million Tonnes and Number of Active Manufacturing Facilities)

- By Admixture Type

- By Function

- By Form

- By Application

- By End-User

- By Construction Sector

- By Performance Tier

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Concrete Admixtures Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Admixture Consumption in Million Tonnes and Number of Active Manufacturing Facilities)

- By Admixture Type

- By Function

- By Form

- By Application

- By End-User

- By Construction Sector

- By Performance Tier

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Concrete Admixtures Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Admixture Consumption in Million Tonnes and Number of Active Manufacturing Facilities)

- By Admixture Type

- By Function

- By Form

- By Application

- By End-User

- By Construction Sector

- By Performance Tier

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Concrete Admixtures Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Admixture Consumption in Million Tonnes and Number of Active Manufacturing Facilities)

- By Admixture Type

- By Function

- By Form

- By Application

- By End-User

- By Construction Sector

- By Performance Tier

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Concrete Admixtures Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Admixture Consumption in Million Tonnes and Number of Active Manufacturing Facilities)

- By Admixture Type

- By Function

- By Form

- By Application

- By End-User

- By Construction Sector

- By Performance Tier

- By Country

- By Sales Channel

- Market Size & Forecast

*Countries Analysed in the Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Italy, Norway, Sweden, China, Japan, India, Australia, South Korea, Singapore, Brazil, Chile, Saudi Arabia, UAE, Egypt, South Africa, Israel

- Technology Landscape & Innovation Analysis

- Polycarboxylate Ether (PCE) Superplasticizer & Next-Generation High-Range Water Reducer Technology Deep-Dive

- Self-Compacting, Self-Healing & Smart Admixture Technology

- Carbon-Reduced, Bio-Based & Sustainable Admixture Technology

- Supplementary Cementitious Material (SCM) Activation Technology (Slag, Calcined Clay, Metakaolin)

- Shrinkage-Reducing, Crack-Mitigating & Durability-Enhancing Admixture Technology

- Corrosion-Inhibiting & Long-Service-Life Concrete Admixture Technology

- AI-Driven Admixture Optimisation, Concrete Mix Design & Performance Modelling Technology

- Patent & IP Landscape in Concrete Admixtures Technologies

- Value Chain & Supply Chain Analysis

- Petrochemical Feedstock & Specialty Polymer Intermediate Supply Chain

- Fly Ash, Slag, Silica Fume & Supplementary Cementitious Material Supply Chain

- Admixture Formulation, Blending & Specialty Compounding Supply Chain

- Distributor, Specialty Trader & Regional Channel Partner Network

- Ready-Mix Concrete Producer, Precast Manufacturer & EPC Contractor Procurement Landscape

- Infrastructure Project Developer & Public Works Customer Channel

- Aftermarket, Mix Design Optimisation & Technical Service Network

- Pricing Analysis

- Plasticizer & Superplasticizer Pricing Analysis Across Standard & High-Range Categories

- Polycarboxylate Ether (PCE) Pricing Analysis Across Standard, High-Performance & Specialty Grades

- Mineral Admixture Pricing Analysis (Fly Ash, Slag, Silica Fume, Metakaolin)

- Specialty Admixture Pricing Analysis (Corrosion Inhibitor, Shrinkage-Reducing, Viscosity-Modifying)

- Liquid, Powder & Granular Admixture Formulation Pricing Analysis

- Per Tonne & Per Cubic Meter Concrete Admixture Pricing Benchmark Analysis

- Total Cost of Admixture Use: Dosage Economics, Concrete Mix Performance & Customer Return on Investment Analysis

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Concrete Admixtures Across Petrochemical, Bio-Based & Supplementary Cementitious Material Pathways

- Carbon Footprint, Cement Reduction Contribution & Cradle-to-Gate Emissions Analysis Across Admixture Categories

- Supplementary Cementitious Material Adoption, Fly Ash Substitution & Carbon-Reduced Concrete Performance

- Hazardous Substance Reformulation, Low-Emission Concrete & Indoor Air Quality Impact

- Regulatory-Driven Sustainability, SDG 9 (Industry, Innovation and Infrastructure), SDG 11 (Sustainable Cities) & SDG 12 (Responsible Consumption) Alignment & Green Finance Eligibility

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Admixture Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Admixture Type, Application & Geography

- Player Classification

- Integrated Specialty Construction Chemical Producers (Established Global Players)

- Polycarboxylate Ether (PCE) Superplasticizer Specialists

- Mineral Admixture & Supplementary Cementitious Material Specialists

- Specialty Performance Admixture Specialists (Corrosion, Shrinkage, Viscosity)

- Self-Compacting, Self-Healing & Smart Admixture Specialists

- Carbon-Reduced & Sustainable Admixture Specialists

- Regional Producers & Distribution-Focused Channel Specialists

- Independent Contract Formulators & Custom Compounding Specialists

- Competitive Analysis Frameworks

- Market Share Analysis by Admixture Type, Application & Region

- Company Profile

- Company Overview & Headquarters

- Concrete Admixture Products & Technology Portfolio

- Key Customer Relationships & Reference Customer Accounts

- Manufacturing Footprint & Production Capacity

- Revenue (Concrete Admixtures Segment) & Order Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Capacity Expansion, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Admixture Type, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Admixture Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)