Market Definition

Corrosion inhibitors are specialty chemical compounds added in low concentrations to a corrosive environment to slow, suppress, or completely arrest the rate of metal degradation on industrial assets. They work by forming a thin protective film on the metal surface, modifying the electrochemical reactions at the metal and electrolyte interface, or neutralising aggressive species present in the surrounding medium such as oxygen, hydrogen sulphide, carbon dioxide, chloride ions, and organic acids. These chemistries are deployed extensively across oil and gas pipelines, water treatment plants, cooling tower circuits, boiler feedwater systems, heat exchangers, automotive radiators, marine vessels, and industrial processing equipment to safeguard structural integrity and operational continuity.

The global corrosion inhibitors market covers a wide portfolio of organic, inorganic, and hybrid formulations supplied in water-based, oil-based, and volatile or vapour-phase forms. Organic inhibitors generally contain functional groups bearing nitrogen, sulphur, oxygen, or phosphorus atoms that adsorb onto metal surfaces, while inorganic variants rely on compounds such as molybdates, phosphates, silicates, nitrites, and selected metal salts to deliver passivation. Hybrid blends combine multiple chemistries to enhance protection across mixed-metal systems and demanding operating windows.

The market serves oil and gas, power generation, water treatment, pulp and paper, metal processing, construction, automotive, and marine end users, each requiring tailored chemistries calibrated for temperature, pressure, fluid composition, and exposure duration. The scope of this study covers global production, consumption, pricing dynamics, regulatory frameworks, technology shifts toward biodegradable and chromate-free chemistries, and competitive positioning of leading manufacturers, offering a structured view of how corrosion inhibitors extend equipment service life, reduce maintenance spend, and prevent unplanned downtime.

Market Insights

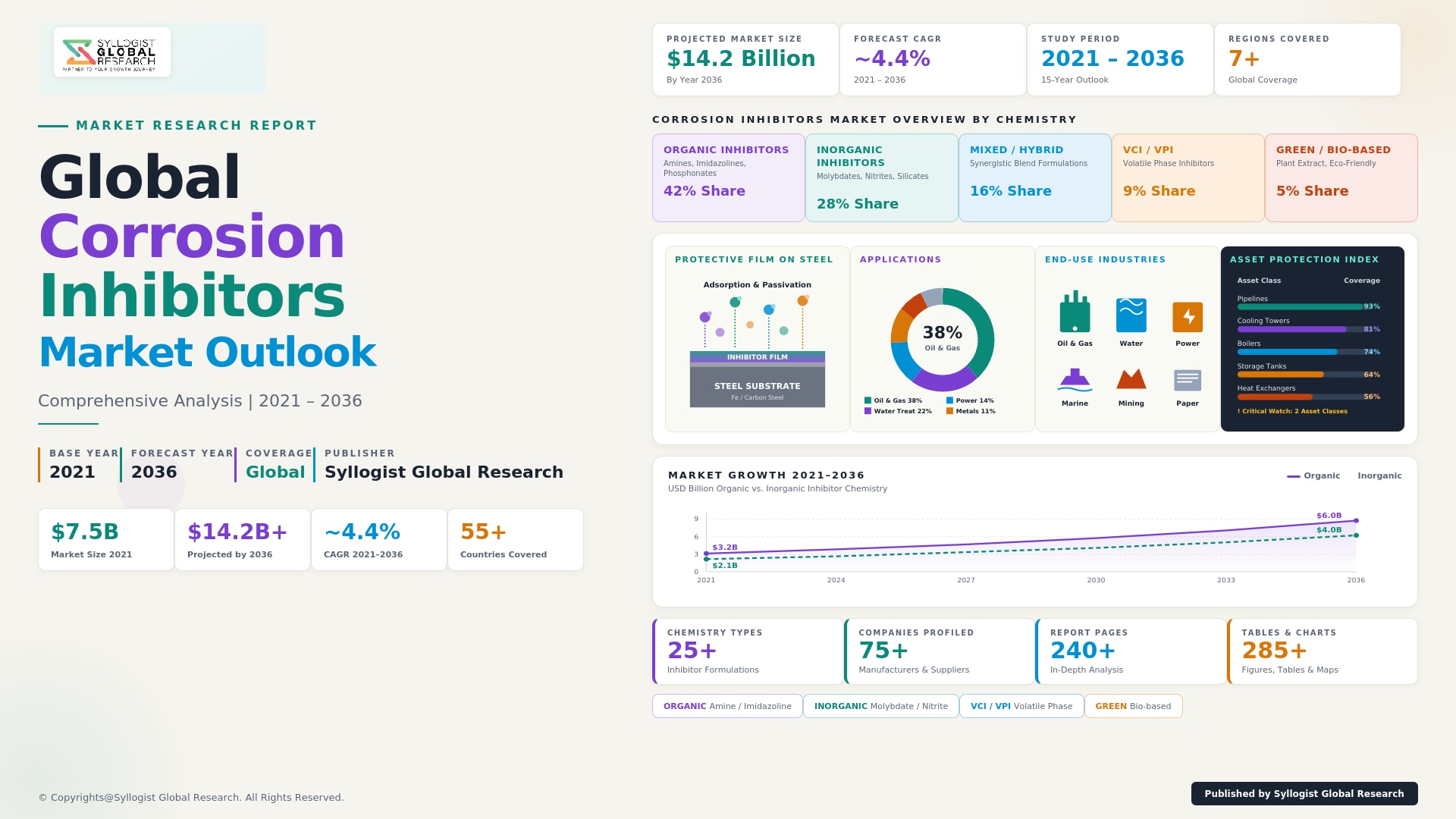

The global corrosion inhibitors market was valued at USD 9.4 billion in 2025 and is projected to reach USD 14 billion by 2035, advancing at a CAGR of 4.1% during the forecast period. Demand momentum is being shaped by accelerating capital expenditure across oil and gas, an ageing stock of industrial assets in developed economies, and a building wave of infrastructure investment across Asia Pacific. Annual global losses attributable to corrosion exceed USD 2.5 trillion, equivalent to roughly 3.4% of global GDP, which provides a compelling economic case for deploying inhibitor chemistries that can reduce these losses by 25% when correctly specified, dosed, and monitored across the asset life cycle.

North America currently holds the largest revenue share at close to 32% of the global market, supported by a mature oil and gas infrastructure, an extensive base of refineries and petrochemical complexes, and stringent regulatory enforcement around pipeline integrity and process safety. The region is anchored by the United States, where shale operations, midstream pipeline networks, and ageing downstream assets sustain a steady pull for high-performance inhibitor packages. Asia Pacific is forecast to register the fastest growth at a CAGR of around 5.4%, with China, India, and Southeast Asia adding new water treatment capacity, expanding power generation fleets, and scaling up manufacturing output. Europe is witnessing a structural shift toward green chemistries driven by REACH regulations and the European Green Deal, which is compressing the addressable market for chromate based formulations and opening commercial space for biodegradable substitutes.

A pronounced shift toward eco friendly, biodegradable, and low toxicity formulations is reshaping the competitive landscape. Plant derived inhibitors based on amino acids, tannins, and saponins are gaining traction in cooling water programmes and acid pickling applications, where regulatory pressure on chromates, nitrites, and phosphates is intensifying. Smart inhibitors that release active ingredients in response to changes in pH, temperature, or mechanical stress are emerging in protective coatings and self healing material systems. Digitalisation is also entering the value chain, with real time corrosion monitoring sensors, predictive analytics, and IoT enabled dosing systems allowing operators to optimise inhibitor consumption by up to 20%, reduce chemical waste, and document compliance for regulators and insurers.

Oil and gas remains the single largest demand centre, accounting for approximately 35% of global consumption, with upstream wellbore protection, midstream pipeline preservation, and downstream refinery applications all contributing volume. Water treatment is the fastest growing application segment, propelled by municipal investment in potable water networks and industrial cooling water programmes that demand both scale and corrosion control. The competitive landscape is moderately consolidated, with the top 10 producers controlling close to 58% of global revenue. Leading suppliers are differentiating through proprietary chemistry portfolios, regional distribution depth, and integrated service offerings that bundle dosing equipment, residual monitoring, and on site technical support. Capacity expansions in low cost geographies, joint ventures with regional formulators, and targeted acquisitions of specialty chemistry assets continue to redraw market shares across the value chain.

Market Drivers

Expansion of Oil and Gas Pipeline Networks and an Ageing Asset Base: Sustained investment in upstream production, midstream pipelines, and downstream refining is anchoring durable demand for corrosion inhibitors. With more than 60% of global hydrocarbon transmission pipelines now over 25 years in service, operators are scaling inhibitor injection programmes to safeguard internal pipeline integrity, lower leak frequency, and meet regulatory standards on mechanical integrity and asset preservation.

Rising Investment in Water and Wastewater Treatment Infrastructure: Municipal and industrial water programmes are expanding rapidly across Asia Pacific, the Middle East, and Latin America. Cooling water systems, boiler feedwater circuits, and desalination plants rely on inhibitor blends to prevent scale formation and metal loss, supporting longer service intervals, lower energy consumption, and consistent water quality across drinking water, irrigation, and process applications.

Tightening Regulations on Asset Integrity and Process Safety: Government bodies and industry associations are issuing stricter mandates around mechanical integrity, emissions control, and unplanned downtime prevention. Compliance with these frameworks requires formal corrosion management programmes, of which inhibitor dosing is a core pillar, prompting operators across power generation, chemicals, mining, and shipping to lock in multi year chemical treatment service contracts.

Market Challenges

Stringent Environmental Regulations on Conventional Chemistries: Restrictions on chromates, nitrites, phosphates, and selected heavy metal salts under frameworks such as REACH, TSCA, and regional ecotoxicity rules are eroding the addressable market for legacy formulations. Reformulation cycles are capital intensive, and obtaining regulatory clearance for new actives can extend product development timelines by 18 to 36 months, slowing commercial roll out.

Volatile Raw Material Pricing and Petrochemical Feedstock Dependency: Many organic inhibitors are derived from amines, imidazolines, and phosphonates that trace back to crude oil and natural gas value chains. Swings in feedstock prices, freight costs, and currency exchange rates compress producer margins, complicate long term contracting, and make stable pricing difficult for formulators serving multi year service agreements with industrial customers.

Performance Limitations Under Extreme Operating Conditions: High temperature, high pressure, and sour service environments common in deepwater oil and gas, geothermal power, and acid pickling lines push conventional inhibitors beyond their effective operating windows. Developing chemistries that maintain protective film stability above 175 degrees Celsius and in CO2 or H2S laden streams remains a persistent technical hurdle for formulators across the corrosion management industry.

Market Segmentation

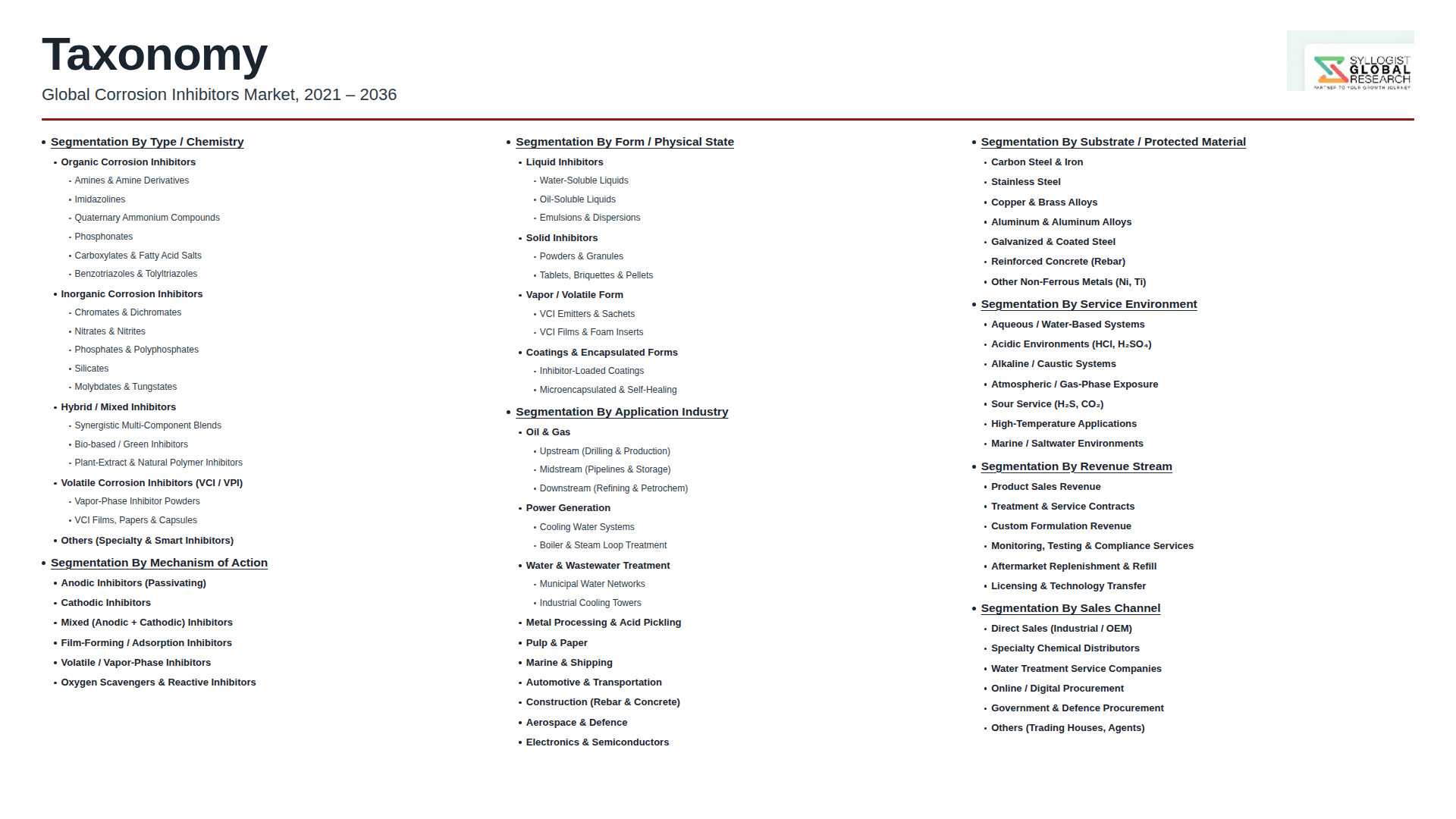

By Compound: Organic Corrosion Inhibitors, Inorganic Corrosion Inhibitors, Hybrid Corrosion Inhibitors

By Type: Water Based, Oil Based, Volatile Corrosion Inhibitors

By Application: Acid Pickling, Cooling Water Systems, Boilers and Heat Exchangers, Pipelines, Coatings and Linings, Others

By End Use Industry: Oil and Gas, Power Generation, Water Treatment, Pulp and Paper, Metal Processing, Construction, Automotive, Others

By Region: North America, Europe, Asia Pacific, Latin America, Middle East and Africa

Key Questions this Study Will Answer

- What is the current size of the global corrosion inhibitors market and what is its projected value through 2035?

- Which compound type (organic, inorganic, or hybrid) and form (water based, oil based, or volatile) is expected to deliver the highest revenue growth?

- How are tightening environmental regulations reshaping demand for chromate free and biodegradable inhibitor chemistries?

- Which end use industries will contribute the largest incremental demand between 2025 and the end of the forecast period?

- Which regions and countries offer the most attractive investment, partnership, and expansion opportunities for inhibitor manufacturers?

- How are leading suppliers differentiating their portfolios through smart inhibitors, digital dosing, and integrated service offerings?

- What are the prevailing pricing trends, raw material cost dynamics, and margin pressures across the corrosion inhibitors value chain?

- Which technology shifts, including IoT enabled monitoring and self healing formulations, will define competitive advantage over the next decade?

- What strategic partnerships, capacity expansions, and merger and acquisition moves are reshaping the competitive landscape?

- What are the key risks, regulatory hurdles, and entry barriers facing new participants in the global corrosion inhibitors market?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Raw Material Price Volatility, Petrochemical Feedstock & Specialty Amine Supply Risk

- Toxicity, Heavy Metal Phase-Out (Chromate, Nitrite) & Regulatory Substitution Risk

- End-Use Demand Cyclicality, Oil & Gas Capex Discipline & Decarbonization Transition Risk

- Field Performance, Microbially Induced Corrosion & Inhibitor Failure Risk

- Trade Policy, Tariff Escalation & Cross-Border Specialty Chemical Logistics Risk

- Regulatory Framework & Standards

- REACH, TSCA, K-REACH & National Chemical Inventory Compliance for Corrosion Inhibitor Formulations

- Drinking Water, NSF 60 & Potable Water Treatment Approval Standards for Phosphate and Silicate Inhibitors

- NACE, ISO 21457, API RP 38 & NORSOK Material Selection and Corrosion Management Standards for Oil & Gas

- Environmental Discharge Limits, Produced Water Disposal & Marine OSPAR/PARCOM Chemical Categorisation

- Worker Safety, GHS Hazard Classification, REACH Annex XVII Restrictions & ESG Disclosure Standards

- Global Corrosion Inhibitors Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Kilotons)

- Market Size & Forecast by Product Type

- Organic Corrosion Inhibitors (Imidazolines, Amines, Amides, Fatty Acid Derivatives, Quaternary Ammonium Compounds)

- Inorganic Corrosion Inhibitors (Phosphates, Polyphosphates, Molybdates, Silicates, Borates, Nitrites)

- Mixed and Blended Inhibitor Formulations

- Vapor Phase Corrosion Inhibitors (VPCI/VCI)

- Bio-Based and Green Corrosion Inhibitors

- Film-Forming Surfactant Corrosion Inhibitors

- Market Size & Forecast by Compound Class

- Amine-Based Inhibitors

- Imidazoline and Quaternary Ammonium Inhibitors

- Phosphonate and Phosphate Ester Inhibitors

- Molybdate, Tungstate and Vanadate Inhibitors

- Nitrite, Nitrate and Chromate-Based Inhibitors (Including Phase-Out)

- Silicate and Borate-Based Inhibitors

- Organic Acid and Carboxylate-Based Inhibitors

- Sulfur-Containing and Thiazole-Based Inhibitors

- Market Size & Forecast by Function and Mechanism

- Anodic Inhibitors

- Cathodic Inhibitors

- Mixed (Ampholytic) Inhibitors

- Film-Forming and Adsorption-Type Inhibitors

- Vapor Phase and Volatile Inhibitors

- Market Size & Forecast by Physical Form

- Liquid Corrosion Inhibitors

- Solid and Powder Corrosion Inhibitors

- Gas Phase (VPCI) and Volatile Corrosion Inhibitors

- Encapsulated, Slow-Release and Controlled-Dose Formats

- Market Size & Forecast by Substrate

- Ferrous Metals (Carbon Steel, Low Alloy Steel, Stainless Steel)

- Non-Ferrous Metals (Copper, Aluminum, Brass, Zinc)

- Galvanized and Coated Substrates

- Mixed-Metallurgy Closed-Loop Systems

- Market Size & Forecast by Water Chemistry

- Freshwater Systems

- Brackish and Brine Systems

- Seawater and Marine Systems

- Sour Service (H2S-Containing) Systems

- Sweet Service (CO2-Dominated) Systems

- High-Temperature, High-Pressure (HPHT) Systems

- Market Size & Forecast by Application

- Oil & Gas Upstream (Downhole, Production Tubing, Subsea, Sour Service)

- Oil & Gas Midstream (Pipeline, Storage, Gathering Lines)

- Oil & Gas Downstream (Refining, Crude Distillation, Catalytic Cracking)

- Water Treatment (Cooling Water, Boiler Water, Potable Water, Closed-Loop)

- Power Generation (Thermal, Nuclear, Geothermal Cooling Loops)

- Chemical Processing and Petrochemical Plants

- Pulp & Paper, Sugar and Food Processing

- Metal Processing, Pickling and Acid Cleaning

- Automotive Coolant, Brake Fluid and Engine Anti-Corrosion

- Marine and Offshore Infrastructure Protection

- Construction, Reinforced Concrete and Rebar Protection

- Electronics, Semiconductor and Precision Component Protection

- Military, Defence, Aerospace and Long-Term Storage

- Market Size & Forecast by End-User

- Oil & Gas Operators (Upstream, Midstream, Downstream)

- Power Generation Utilities and IPPs

- Water Treatment Service Providers and Industrial Water Operators

- Chemical and Petrochemical Manufacturers

- Pulp, Paper and Sugar Industry Operators

- Automotive OEMs and Tier 1 Suppliers

- Marine, Shipping and Offshore Operators

- Metal Processing, Steel and Aluminum Manufacturers

- Construction Contractors and Infrastructure Owners

- Electronics and Semiconductor Manufacturers

- Defence, Aerospace and Government Procurement Agencies

- Market Size & Forecast by Sales Channel

- Direct Sales to End-User (Account-Based Specialty Chemical Supply)

- Distributor and Specialty Chemical Reseller Channel

- Integrated Service Contract (Chemical Plus Treatment Program)

- Digital, E-Commerce and Online Industrial Procurement Platforms

- North America Corrosion Inhibitors Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotons)

- By Product Type

- By Compound Class

- By Function and Mechanism

- By Physical Form

- By Substrate

- By Water Chemistry

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Corrosion Inhibitors Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotons)

- By Product Type

- By Compound Class

- By Function and Mechanism

- By Physical Form

- By Substrate

- By Water Chemistry

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Corrosion Inhibitors Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotons)

- By Product Type

- By Compound Class

- By Function and Mechanism

- By Physical Form

- By Substrate

- By Water Chemistry

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Corrosion Inhibitors Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotons)

- By Product Type

- By Compound Class

- By Function and Mechanism

- By Physical Form

- By Substrate

- By Water Chemistry

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Corrosion Inhibitors Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotons)

- By Product Type

- By Compound Class

- By Function and Mechanism

- By Physical Form

- By Substrate

- By Water Chemistry

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Corrosion Inhibitors Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotons)

- By Product Type

- By Compound Class

- By Function and Mechanism

- By Physical Form

- By Substrate

- By Water Chemistry

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- *Countries Analyzed in the Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Italy, Norway, Sweden, China, Japan, India, Australia, South Korea, Singapore, Brazil, Chile, Saudi Arabia, UAE, Egypt, South Africa, Israel

- Technology Landscape & Innovation Analysis

- Organic Film-Forming Inhibitor Chemistry and Adsorption Mechanism Technology Deep-Dive

- Imidazoline, Quaternary Ammonium and Long-Chain Amine Inhibitor Synthesis Routes

- Phosphonate, Phosphate Ester and Polyphosphate Inhibitor Technology for Cooling and Boiler Water

- Molybdate, Tungstate and Heavy-Metal-Free Inhibitor Substitution Technology

- Vapor Phase (VPCI) and Volatile Corrosion Inhibitor Encapsulation Technology

- Bio-Based and Plant-Extract Green Inhibitor Technology (Tannins, Alkaloids, Amino Acids)

- Microbial Corrosion Inhibitor and Biocide-Combined Formulation Technology

- Smart and Self-Healing Coating-Integrated Inhibitor Technology

- Real-Time Corrosion Monitoring, Coupon Analysis and Digital Inhibitor Dosing Technology

- Patent & IP Landscape in Corrosion Inhibitor Chemistry and Formulation

- Value Chain & Supply Chain Analysis

- Petrochemical Feedstock, Specialty Amine and Fatty Acid Raw Material Supply Chain

- Phosphorus, Molybdenum, Zinc and Inorganic Inhibitor Mineral Feedstock Supply Chain

- Specialty Chemical Manufacturing, Toll Blending and Custom Synthesis Footprint

- Distributor, Specialty Reseller and Service Contract Channel Landscape

- End-User Procurement, Treatment Program and Performance-Based Contracting

- Logistics, Hazmat Transportation and Cross-Border Specialty Chemical Trade

- Waste Management, Spent Inhibitor Recovery and Circular Economy

- Pricing Analysis

- Organic Inhibitor Pricing by Chemistry (Imidazoline, Amine, Quaternary Ammonium)

- Inorganic Inhibitor Pricing by Compound (Phosphate, Molybdate, Silicate)

- Vapor Phase and Specialty Format Inhibitor Pricing

- Bio-Based and Green Inhibitor Pricing Premium and Cost Trajectory

- Treatment Program Pricing, Dosage Optimization and Performance-Linked Contracting

- Total Cost of Ownership: Inhibitor Spend versus Corrosion-Driven Capex and Downtime Avoidance

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Corrosion Inhibitors: Carbon Footprint, Toxicity and Eutrophication Potential

- Chromate, Nitrite and Heavy Metal Phase-Out: Regulatory Substitution Pathways and Replacement Chemistry

- Bio-Based, Plant-Derived and Renewable Feedstock Inhibitor Development and Commercial Readiness

- Produced Water, Cooling Water Blowdown and Industrial Discharge Compliance Considerations

- Regulatory-Driven Sustainability, REACH SVHC, OSPAR PLONOR and Green Chemistry Alignment

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Product Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Product Type, Application & Geography

- Player Classification

- Integrated Specialty Chemical Majors with Corrosion Inhibitor Portfolios

- Oilfield Production Chemicals Specialists (Downhole, Pipeline, Refining Inhibitors)

- Water Treatment Chemical Companies and Service Providers

- Industrial Maintenance, MRO and Coating-Integrated Inhibitor Suppliers

- VPCI and Vapor Phase Corrosion Inhibitor Specialists

- Bio-Based and Green Corrosion Inhibitor Innovators

- Regional and National Specialty Chemical Manufacturers

- Custom Synthesis, Toll Blending and Private-Label Manufacturers

- Competitive Analysis Frameworks

- Market Share Analysis by Product Type, Application & Region

- Company Profile

- Company Overview & Headquarters

- Corrosion Inhibitor Products & Technology Portfolio

- Key Customer Relationships & Reference Treatment Programs

- Manufacturing Footprint & Production Capacity

- Revenue (Corrosion Inhibitor Segment) & Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Capacity Expansion, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Product Type, Compound Class, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)