Market Definition

The Global Coal Gasification and Carbon Capture, Utilisation, and Storage Integration Market encompasses the engineering, construction, operation, and technology supply of integrated industrial systems that convert coal feedstocks into synthesis gas through thermochemical gasification processes and couple this conversion with carbon dioxide capture, transport, utilisation, and geological or industrial storage technologies to substantially reduce or eliminate the lifecycle greenhouse gas emissions associated with coal-derived energy, chemicals, hydrogen, and synthetic fuel production. Coal gasification converts coal through partial oxidation with oxygen or steam at elevated temperatures and pressures into synthesis gas comprising primarily hydrogen, carbon monoxide, and carbon dioxide, which serves as a platform intermediate for power generation via combined cycle gas turbines, hydrogen production through water-gas shift and purification processes, synthetic natural gas production via methanation, liquid fuels synthesis via Fischer-Tropsch processing, ammonia and methanol production, and other chemical synthesis applications. Carbon capture, utilisation, and storage integration at coal gasification facilities encompasses pre-combustion capture of carbon dioxide from synthesis gas streams prior to combustion or further processing using physical absorption with selexol, rectisol, or other solvents; post-combustion capture from flue gas streams using amine scrubbing or solid sorbent systems; oxy-fuel combustion configurations producing concentrated carbon dioxide streams amenable to direct compression and transport; carbon dioxide compression, dehydration, and pipeline transport infrastructure; geological storage in depleted hydrocarbon reservoirs, deep saline aquifer formations, and coal seam formations; and carbon utilisation pathways including enhanced oil recovery, carbon dioxide-to-chemicals conversion, and mineralisation. Key participants encompass gasification technology licensors, carbon capture technology developers, engineering procurement and construction contractors, industrial gas companies, coal producers and coal-to-chemicals operators, national oil and gas companies, project finance institutions, and the government bodies whose industrial decarbonisation policy frameworks and carbon pricing mechanisms define the investment economics of coal gasification with carbon capture, utilisation, and storage integration globally.

Market Insights

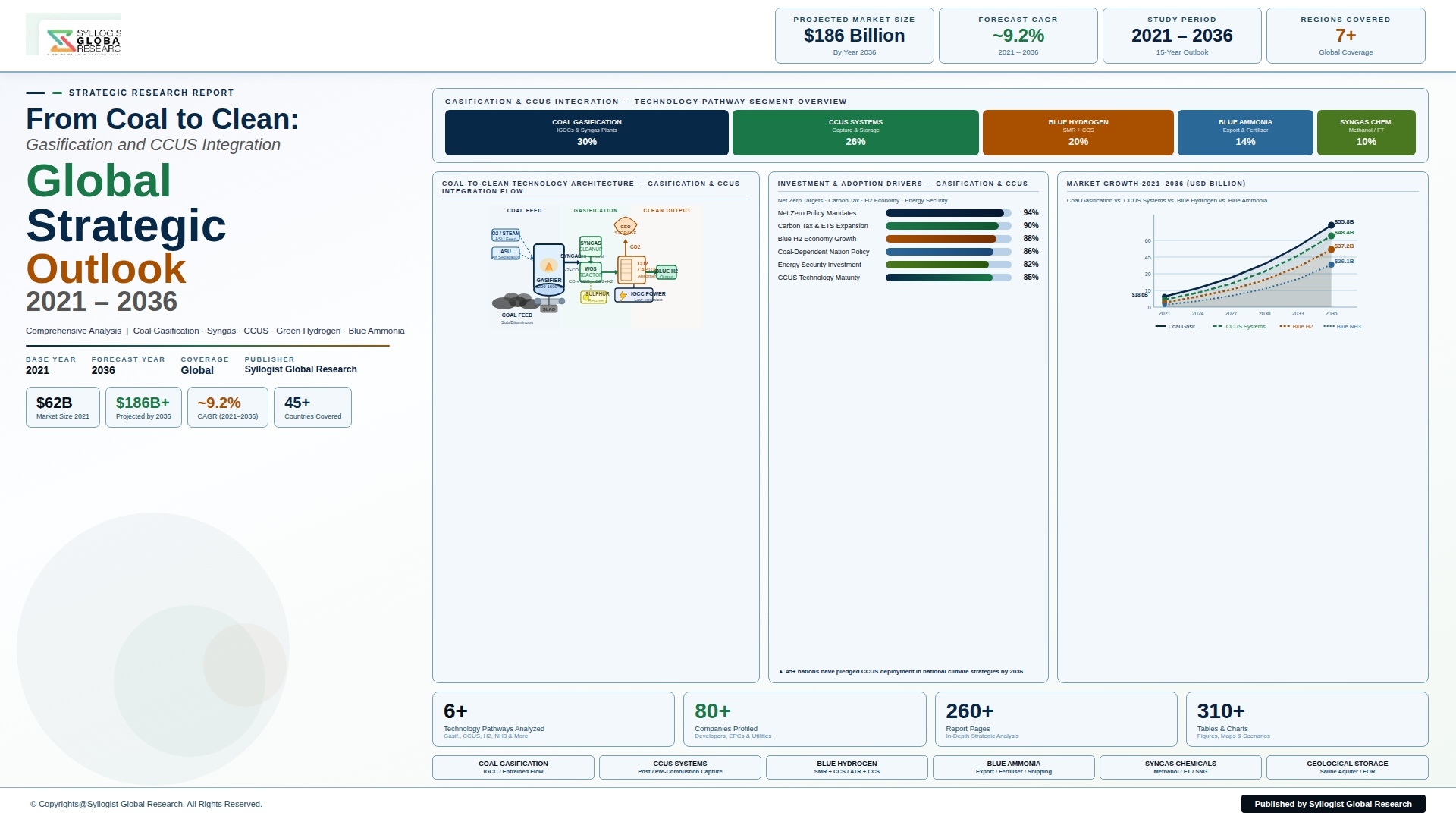

The global coal gasification and carbon capture, utilisation, and storage integration market was valued at approximately USD 4.8 billion in 2025 and is projected to reach USD 14.2 billion by 2034, advancing at a compound annual growth rate of 12.8% over the forecast period from 2027 to 2034, driven by the intersection of energy security imperatives in coal-endowed economies, accelerating industrial decarbonisation regulatory pressure, and the growing recognition that coal gasification with carbon capture integration represents one of the most commercially viable near-term pathways for producing low-carbon hydrogen, chemicals, and synthetic fuels at scale from existing coal resource endowments and established industrial infrastructure in economies where abrupt coal sector transition carries prohibitive economic and energy security costs. China, which operates the world’s largest coal gasification industry with installed coal-to-chemicals and coal-to-synthetic natural gas capacity exceeding 100 million metric tons of coal equivalent annually, represents the largest and most strategically significant national market for coal gasification and carbon capture, utilisation, and storage integration, with Chinese state energy companies and government industrial policy programs driving investment in carbon capture retrofits at existing coal chemical complexes and greenfield integrated low-carbon coal conversion facilities that collectively define the near-term market development trajectory.

The coal-to-hydrogen application represents the most commercially compelling integration pathway for carbon capture, utilisation, and storage at coal gasification facilities, with the water-gas shift conversion of coal-derived synthesis gas to hydrogen followed by pre-combustion carbon dioxide capture from the hydrogen-rich stream producing blue hydrogen at production costs of approximately USD 1.2 to USD 2.8 per kilogram of hydrogen depending on coal feedstock cost, plant scale, carbon capture rate, and carbon transport and storage cost, positioning coal-derived blue hydrogen competitively with green hydrogen at most locations globally through 2030 and providing a commercially viable near-term low-carbon hydrogen supply pathway for hard-to-abate industrial sectors whose hydrogen demand growth exceeds the pace at which low-cost green hydrogen supply can be scaled. The carbon capture rate achievable at coal gasification facilities using pre-combustion capture from synthesis gas, typically 85% to 95% of total carbon in the feedstock at technically optimised designs, substantially exceeds the capture rates achievable at post-combustion capture retrofits to pulverised coal power plants, which commonly capture 85% to 90% of flue gas carbon dioxide but cannot address the remaining carbon dioxide in the dilute flue gas stream as efficiently as the concentrated carbon dioxide streams produced in pre-combustion gasification configurations. Integrated gasification combined cycle power generation with carbon capture represents the power sector application of coal gasification and carbon capture, utilisation, and storage integration, with the thermodynamic efficiency advantage of synthesis gas over conventional pulverised coal combustion and the pre-combustion capture efficiency premium enabling integrated gasification combined cycle with carbon capture to achieve net plant efficiency of 30% to 36% with 90% carbon capture compared to the 26% to 32% net efficiency with 90% capture achievable at post-combustion capture retrofitted supercritical pulverised coal plants.

China commands approximately 58% of global coal gasification capacity and is the dominant national market for coal gasification and carbon capture, utilisation, and storage integration investment, with the government’s dual carbon goals of peak emissions before 2030 and carbon neutrality by 2060 creating a policy framework that requires the country’s enormous coal chemicals industry to substantially reduce its carbon intensity while preserving the energy security and chemicals production capacity that coal-to-chemicals facilities provide as strategic industrial assets. China’s National Development and Reform Commission has identified coal chemical industry decarbonisation as a priority industrial transformation program, with carbon capture retrofit programs at existing coal-to-methanol, coal-to-olefins, and coal-to-synthetic natural gas facilities complemented by greenfield low-carbon coal gasification projects incorporating carbon capture from design inception, with cumulative carbon capture capacity at Chinese coal gasification facilities estimated at approximately 8.2 million metric tons of carbon dioxide annually in 2025 and targeted to reach approximately 40 million metric tons annually by 2035 under ambitious scenario projections. The United States represents the second-largest market for coal gasification and carbon capture, utilisation, and storage integration by investment value, supported by the substantially enhanced Section 45Q tax credit under the Inflation Reduction Act that provides USD 85 per metric ton of carbon dioxide geologically stored and USD 60 per metric ton utilised for enhanced oil recovery, creating investment economics that can cover the incremental capital and operating cost of carbon capture integration at coal gasification facilities in favourable locations with access to geological storage or enhanced oil recovery infrastructure in the Permian Basin, Gulf Coast, and Illinois Basin carbon storage regions.

The coal-to-chemicals integration with carbon capture pathway encompasses the largest installed base of coal gasification capacity globally, with methanol, ammonia, dimethyl ether, and olefins production from coal-derived synthesis gas representing the primary commercial application of gasification technology in China, India, South Africa, and other coal-resource-rich economies whose chemical industries were built on coal feedstock economics and whose transition to lower-carbon operation through carbon capture integration is substantially less disruptive and more capital-efficient than complete feedstock substitution toward natural gas or biomass alternatives. The geological storage infrastructure development required to absorb the carbon dioxide volumes generated by large-scale coal gasification and carbon capture programs represents a critical enabling component whose adequacy constrains the pace at which carbon capture integration can be deployed across the global coal gasification industry, with the characterisation, permitting, and injection infrastructure development for commercial-scale geological storage sites in China, India, and emerging coal gasification economies requiring 5 to 10 years from initial site assessment to first injection, creating a storage infrastructure timeline constraint that must be addressed through parallel development programs whose funding and government support are as critical to market growth as the carbon capture technology investment itself. The emerging integration of coal gasification with carbon capture and green hydrogen co-production, in which electrolytic green hydrogen is blended with coal-derived blue hydrogen to produce lower-cost hydrogen mixes than either pure green or pure blue hydrogen alone at current technology costs, represents a commercially innovative hybrid decarbonisation pathway whose development is advancing at pilot and demonstration scale in China and Australia and whose commercial viability will improve as electrolyser costs continue their learning curve decline trajectory through the forecast period.

Key Drivers

Energy Security Imperatives in Coal-Dependent Economies and Strategic Industrial Policy Mandating Low-Carbon Coal Utilisation Investment

The energy security and economic development imperatives of coal-endowed economies including China, India, the United States, South Africa, Indonesia, and Poland, whose coal resources represent sovereign energy assets whose utilisation underpins national energy independence, industrial employment, and chemicals production capacity, are creating strong governmental and industrial motivation to invest in coal gasification with carbon capture, utilisation, and storage integration as the pathway to maintaining coal utilisation while satisfying increasingly stringent domestic and international carbon reduction commitments that would otherwise require economically and politically disruptive coal phase-out at timescales incompatible with energy system transition realities. China’s strategic designation of coal as the foundation fuel for national energy security, combined with the government’s binding carbon peak and neutrality targets, creates a policy imperative for low-carbon coal technology investment that is reflected in the Fourteenth Five Year Plan’s explicit support for coal-to-chemicals decarbonisation, carbon capture research and deployment programs, and geological storage site characterisation programs whose combined government and state enterprise investment commitments represent the largest national carbon capture deployment program for coal industries globally. The International Energy Agency’s energy security analysis consistently identifies coal gasification with carbon capture as a critical technology for enabling coal-dependent economies to meet climate commitments without jeopardising energy security during the transition period to renewable-dominated energy systems, with scenario modelling indicating that approximately 1.5 billion metric tons of carbon dioxide annually from coal gasification and power applications must be captured and stored globally by 2050 under net-zero pathways that preserve coal utilisation in economies where its phase-out within that timeframe is not feasible.

Carbon Pricing Mechanism Expansion, Industrial Decarbonisation Regulation, and Section 45Q Tax Credit Economics Creating Investment-Grade Project Returns for Carbon Capture Integration

The expansion of carbon pricing mechanisms across major industrial economies is progressively improving the investment economics of carbon capture integration at coal gasification facilities by creating a quantifiable avoided carbon cost benefit that offsets a portion of the capital and operating cost premium of carbon capture systems, with the European Union Emissions Trading System carbon price trading at approximately EUR 60 to EUR 80 per metric ton in 2025 and projected to reach EUR 100 to EUR 150 per metric ton by 2030 under supply constraint trajectories that improve the carbon capture business case at industrial facilities covered by the scheme. The United States Inflation Reduction Act Section 45Q tax credit enhancement, which increased the credit for geological storage from USD 50 to USD 85 per metric ton and extended credit availability to projects beginning construction before 2033, has materially transformed the investment economics of carbon capture at coal gasification facilities in the United States by providing a long-term, predictable revenue stream whose USD 85 per metric ton value covers the full additional cost of carbon capture integration at optimally located facilities with low geological storage transport distances, enabling positive investment returns without additional carbon price support. China’s national emissions trading scheme, which expanded to cover the power sector in 2021 and is scheduled to extend coverage to coal chemical industries including coal-to-chemicals, coal-to-liquids, and coal-to-gas facilities in subsequent compliance periods, will impose carbon cost obligations on the world’s largest coal gasification industry whose facilities currently operate without direct carbon pricing exposure, creating a regulatory compliance investment driver of substantial magnitude whose effect on coal gasification carbon capture adoption will be compounded by the simultaneous availability of government capital grants and concessional financing for carbon capture pilot and demonstration programs.

Low-Carbon Hydrogen Demand Growth and Blue Hydrogen Commercial Viability Window Driving Coal Gasification Carbon Capture Investment in Hydrogen Production Applications

The global low-carbon hydrogen economy’s development trajectory creates a commercially significant near-term window for coal-derived blue hydrogen production with carbon capture to serve industrial hydrogen demand in hard-to-abate sectors including steel, chemicals, refining, and heavy transportation whose decarbonisation requires large-scale, reliable, and cost-competitive hydrogen supply at volumes and price points that green hydrogen cannot fully satisfy during the period before electrolyser cost reduction and renewable energy scaling achieve full economic competitiveness with coal-based hydrogen production. Coal gasification with pre-combustion carbon capture can produce blue hydrogen at delivered costs of USD 1.5 to USD 3.5 per kilogram at coal-advantaged locations in China, the United States, and Australia, compared to green hydrogen production costs of USD 3.5 to USD 6.0 per kilogram at current electrolyser capital costs and renewable electricity prices outside the most cost-advantaged locations, creating a commercial bridging opportunity for coal-derived blue hydrogen whose window extends approximately through 2032 to 2038 depending on the rate of green hydrogen cost reduction and the carbon price applied to remaining emissions from blue hydrogen production. The hydrogen offtake commitments of Japanese and South Korean steel, fertilizer, and chemical companies seeking low-carbon hydrogen imports from coal-endowed partner nations including Australia, the United States, and Indonesia are creating long-term demand signals that enable project finance for coal gasification with carbon capture hydrogen production facilities, with government-to-government hydrogen partnership frameworks including the Australia-Japan Hydrogen Energy Supply Chain and equivalent United States-Japan hydrogen cooperation programs providing the institutional framework for commercial offtake agreement development that is progressing toward first commercial-scale blue hydrogen supply contracts.

Key Challenges

High Capital Cost of Integrated Gasification and Carbon Capture Systems, Project Finance Complexity, and Cost Overrun History Constraining Commercialisation Pace

The capital cost of an integrated coal gasification combined cycle power plant with pre-combustion carbon capture at commercial scale ranges from USD 3,500 to USD 5,500 per kilowatt of net electrical output, compared to USD 1,200 to USD 1,800 per kilowatt for a supercritical pulverised coal plant without capture, representing a capital cost premium whose financing at commercial project scale requires either substantial government capital grant support, highly favourable carbon credit or product premium pricing, or concessional development finance institution lending that is not universally available across all project geographies and development contexts. The historical performance of first-of-a-kind and early commercial integrated gasification combined cycle with carbon capture projects, including significant cost overruns, schedule delays, and below-nameplate availability factors at reference facilities in the United States, has created a risk perception among private project finance lenders that increases the required return on equity and constrains debt availability for new coal gasification with carbon capture projects, necessitating government risk-sharing through loan guarantees, offtake agreements, or capital grants to achieve bankable project finance structures at costs of capital consistent with competitive product pricing. The operating cost of pre-combustion carbon capture at coal gasification facilities, encompassing solvent regeneration energy, carbon dioxide compression power, makeup solvent costs, and additional operations and maintenance, adds approximately USD 15 to USD 35 per metric ton of carbon dioxide captured to the cost of synthesis gas production, an operating cost increment that must be recovered through carbon credit revenue, product price premium, or avoided carbon compliance cost to maintain facility profitability relative to uncaptured operation.

Geological Carbon Storage Site Availability, Permitting Timelines, and Transport Infrastructure Development Requirements Constraining Carbon Capture Deployment Scale

The commercial deployment of carbon capture at coal gasification facilities at the scale required to achieve meaningful industrial sector emissions reduction is fundamentally constrained by the availability of adequately characterised, permitted, and accessible geological storage formations within economically viable carbon dioxide transport distance of capture facilities, with the global geological storage resource base being theoretically vast but commercially accessible storage capacity in the near term being severely limited by the time and investment required to advance storage sites from initial geological assessment through detailed characterisation, regulatory permitting, injection well drilling, and operational commissioning at the pace required to absorb growing carbon capture volumes. Geological storage permitting processes in the United States, European Union, and Australia require 5 to 10 years from initial site nomination to first injection permit approval, with regulatory frameworks for pore space ownership, long-term liability transfer, and monitoring and verification obligations varying materially across jurisdictions in ways that create investment uncertainty for storage site developers and carbon capture project operators whose project economics depend on assured long-term storage access. Carbon dioxide transport infrastructure connecting capture facilities at coal gasification plants with geological storage sites represents an additional capital investment requirement of USD 1 million to USD 4 million per kilometre of pipeline depending on diameter, terrain, and regulatory environment, with the geographic mismatch between coal gasification industry concentrations and optimal geological storage formations in China, India, and the United States requiring pipeline network investments of USD 500 million to USD 5 billion per regional carbon capture cluster whose development requires multi-party coordination and government infrastructure investment support that is not yet systematically available in most coal gasification geographies.

Public Acceptance, Environmental Justice Concerns, and Regulatory Opposition to Continued Coal Utilisation Limiting Social Licence for Carbon Capture-Enabled Coal Projects

Coal gasification with carbon capture, utilisation, and storage integration faces a complex and evolving social licence landscape in which the technology’s potential to reduce greenhouse gas emissions from coal utilisation is contested by environmental advocacy organisations and climate policy communities who argue that investment in carbon capture for coal perpetuates fossil fuel infrastructure lock-in, diverts capital from renewable energy deployment, and delays the coal phase-out whose acceleration is required under scientifically credible net-zero emissions pathways, creating regulatory and political opposition that complicates project permitting, government funding allocation, and corporate sustainability alignment for coal gasification with carbon capture investments in developed market jurisdictions. Community concerns about geological carbon dioxide storage, including uncertainty about long-term containment integrity, potential groundwater contamination from carbon dioxide migration, and induced seismicity from high-pressure injection operations, generate public opposition to storage site development that has delayed or cancelled storage projects in the European Union and Australia and requires sustained community engagement, transparent monitoring and verification reporting, and regulatory frameworks for long-term storage liability management that are not yet fully established in most storage jurisdictions. The classification of coal gasification with carbon capture as a transition technology rather than a permanent climate solution in the taxonomy frameworks of the European Union Sustainable Finance Taxonomy and equivalent classification systems in the United Kingdom and Canada creates a green finance access limitation for coal gasification with carbon capture projects that may preclude their eligibility for sustainable bond financing, green infrastructure lending, and ESG-aligned equity investment, constraining the capital availability and cost of capital achievable by project developers compared to fully renewable energy infrastructure projects whose access to green finance markets is unrestricted.

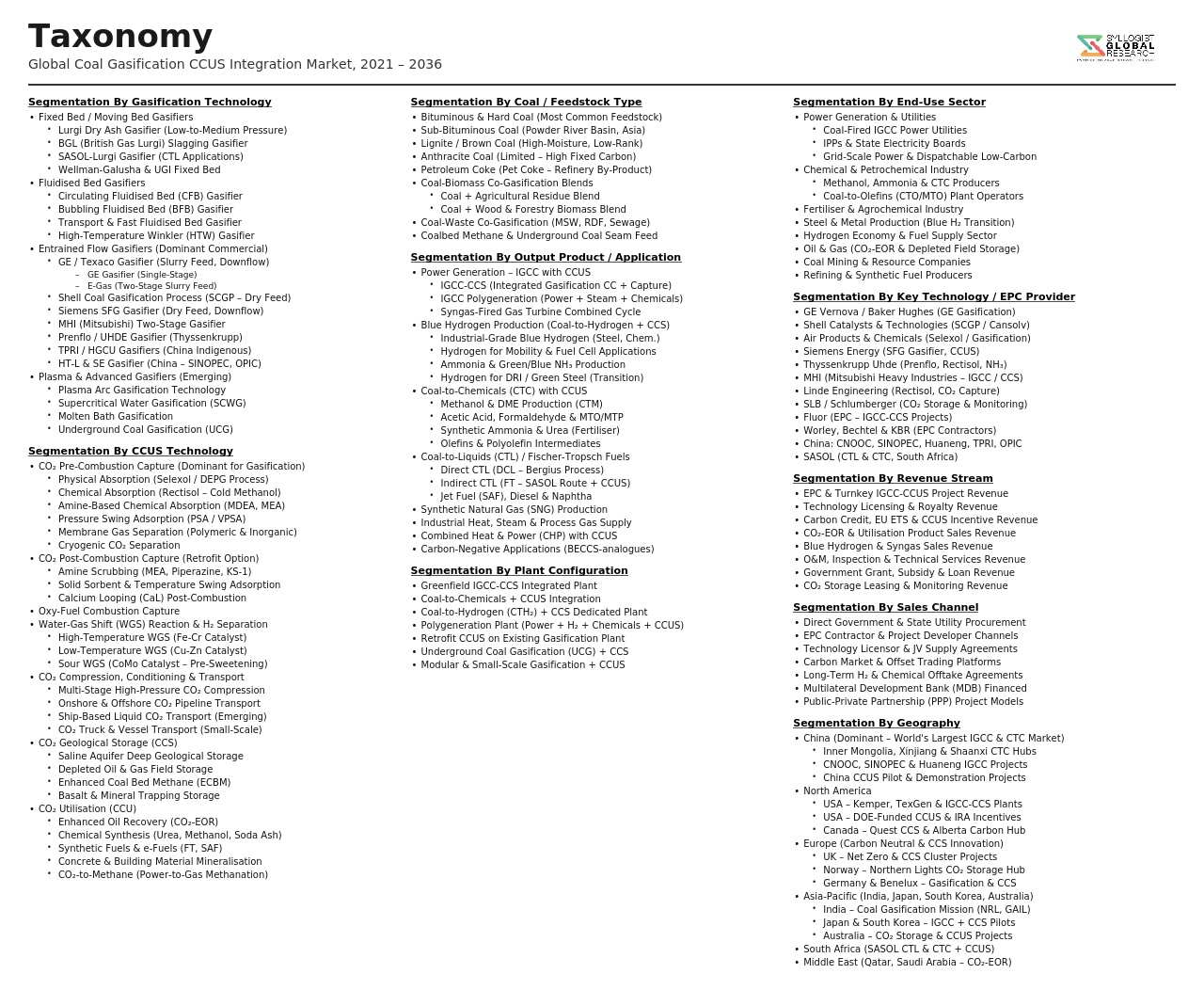

Market Segmentation

- Segmentation By Coal Gasification Technology

- Fixed Bed Gasification (Lurgi and BG Moving Bed)

- Fluidised Bed Gasification (KBR and High Temperature Winkler)

- Entrained Flow Gasification (Shell, GE, and Siemens)

- Underground Coal Gasification (UCG)

- Hybrid and Advanced Gasification Technologies

- Segmentation By Carbon Capture Technology

- Pre-Combustion Capture (Physical Absorption with Selexol and Rectisol)

- Pre-Combustion Capture (Chemical Looping and Sorption Enhanced)

- Post-Combustion Capture (Amine Scrubbing and Solid Sorbents)

- Oxy-Fuel Combustion with Direct CO2 Capture

- Membrane-Based Separation

- Cryogenic CO2 Separation

- Segmentation By End-Use Application

- Power Generation (Integrated Gasification Combined Cycle with CCS)

- Low-Carbon and Blue Hydrogen Production

- Synthetic Natural Gas with Carbon Capture

- Ammonia and Fertilizer Production with Carbon Capture

- Methanol and Olefins Production with Carbon Capture

- Fischer-Tropsch Synthetic Liquid Fuels with Carbon Capture

- Dimethyl Ether and Chemical Feedstock Production

- Others

- Segmentation By Carbon Disposition

- Geological Storage in Deep Saline Aquifers

- Enhanced Oil Recovery (EOR) with CO2 Utilisation

- Depleted Hydrocarbon Reservoir Storage

- Carbon Utilisation in Chemicals and Materials

- Enhanced Coal Bed Methane Recovery

- Mineralisation and Permanent Carbonation

- Segmentation By Project Scale

- Pilot and Demonstration Scale (Below 0.1 Mtpa CO2 captured)

- Early Commercial Scale (0.1 to 1.0 Mtpa CO2 captured)

- Full Commercial Scale (Above 1.0 Mtpa CO2 captured)

- Industrial Cluster and Hub Scale (Above 5.0 Mtpa CO2 captured)

- Segmentation By Project Stage

- Operating Commercial Facilities

- Under Construction and Commissioning

- Front-End Engineering and Design (FEED)

- Feasibility Study and Pre-FEED

- Carbon Capture Retrofit Programs at Existing Gasification Plants

- Segmentation By Ownership Structure

- State-Owned Enterprises and National Energy Companies

- Integrated Private Energy and Industrial Companies

- Independent Power Producers and Project Companies

- Public-Private Partnership Structures

- Joint Ventures with Government Equity Participation

- Segmentation By Region

- Asia-Pacific (China, India, Australia, and Others)

- North America (United States and Canada)

- Europe (Poland, Germany, United Kingdom, and Others)

- Middle East and Africa (South Africa and Gulf States)

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Coal Gasification and Carbon Capture, Utilisation, and Storage Integration Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by application, power generation, hydrogen production, chemicals, and synthetic fuels, by carbon capture technology, pre-combustion, post-combustion, and oxy-fuel, by carbon disposition, geological storage and enhanced oil recovery, and by geography, to enable technology developers, project developers, policy makers, and investors to identify which application segments and regional markets will generate the highest absolute revenue and most commercially significant deployment momentum across the forecast period?

- What is the projected production cost trajectory of coal-derived blue hydrogen with pre-combustion carbon capture through 2034 at reference locations in China, the United States, Australia, and India under varying coal feedstock cost, carbon capture rate, geological storage cost, and carbon pricing assumptions, at what coal input cost and carbon price combinations does coal-derived blue hydrogen achieve or maintain cost competitiveness with green hydrogen from renewable electrolysis, and how are government low-carbon hydrogen support programs including the United States Inflation Reduction Act Section 45V credit and equivalent programs in Japan, South Korea, and the European Union affecting the relative investment economics of coal-based blue hydrogen versus renewable green hydrogen production for hard-to-abate industrial hydrogen demand?

- How are China’s national emissions trading scheme expansion to coal chemical industries, the National Development and Reform Commission coal chemical decarbonisation program, and state enterprise carbon capture investment mandates expected to drive coal gasification carbon capture deployment through 2034, what are the projected carbon capture installation rates at Chinese coal-to-methanol, coal-to-olefins, coal-to-synthetic natural gas, and coal-to-liquids facilities, how does the geographic distribution of Chinese coal gasification capacity align with available geological storage formation locations and the pipeline infrastructure investment required for carbon dioxide transport, and which Chinese regions represent the most commercially viable near-term coal gasification carbon capture deployment clusters?

- What is the current global inventory of geological carbon dioxide storage capacity suitable for coal gasification carbon capture volumes, how does the geographic distribution of commercially accessible storage capacity across the United States, China, Australia, Europe, and emerging coal gasification economies align with the geographic distribution of coal gasification carbon capture project development activity, what are the permitting timeline, pore space ownership, and long-term liability management regulatory developments most critical to enabling adequate storage capacity development by 2030, and what infrastructure investment programs are required to connect carbon capture clusters at coal gasification facilities to geological storage formations within economically viable transport distances?

- Who are the leading gasification technology licensors, pre-combustion carbon capture technology developers, integrated gasification combined cycle engineering contractors, geological storage site developers, carbon dioxide pipeline and transport infrastructure operators, and project finance institutions currently defining the competitive and investment landscape of the global coal gasification and carbon capture, utilisation, and storage integration market, and what are their respective technology portfolio coverage, reference project operating performance data, project development pipeline scale and financial investment decision timelines, government program participation and funding secured, and strategic positioning responses to the capital cost, storage infrastructure, and social licence challenges constraining coal gasification carbon capture commercialisation through 2034?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Coal Supply Security, Price Volatility & Long-Term Fuel Transition Risk for Gasification Assets

- CO2 Storage Reservoir Availability, Injectivity & Long-Term Geological Containment Risk

- Carbon Price Uncertainty, Policy Reversal & CCUS Incentive Discontinuation Risk

- Technology Integration Complexity, Gasifier-CCUS Interface & Process Reliability Risk

- Social Licence, Community Acceptance, Stranded Asset & Reputational Risk

- Regulatory Framework & Standards

- Carbon Capture, Utilisation & Storage (CCUS) Regulatory Frameworks, CO2 Storage Permitting & Liability Standards

- Emissions Trading Schemes (ETS), Carbon Credits & CCUS Project Eligibility Under National & International Carbon Markets

- Coal Gasification Plant Permitting, Air Quality, Syngas & Effluent Discharge Regulatory Requirements

- CO2 Transport Pipeline Safety, Cross-Border CO2 Transfer & Offshore Storage Regulatory Frameworks

- Government Incentive Programmes: Production Tax Credits, Contracts for Difference & CCUS Capital Grant Schemes

- Global Coal Gasification & CCUS Integration Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (CO2 Captured, Metric Tonnes per Annum)

- Market Size & Forecast by Gasification Technology

- Entrained-Flow Gasification (Dry-Feed & Slurry-Feed)

- Moving-Bed (Fixed-Bed) Gasification

- Fluidised-Bed Gasification

- Underground Coal Gasification (UCG)

- Plasma & Advanced Thermal Gasification

- Market Size & Forecast by CCUS Technology

- Pre-Combustion CO2 Capture (Acid Gas Removal & Selexol/Rectisol Process)

- Post-Combustion CO2 Capture (Amine Scrubbing & Solid Sorbent)

- Oxy-Fuel Combustion Capture

- Physical Absorption & Membrane Separation

- Geological CO2 Storage (Saline Aquifer, Depleted Oil & Gas Fields)

- CO2 Enhanced Oil Recovery (EOR) & Enhanced Gas Recovery (EGR)

- Market Size & Forecast by Carbon Utilisation Pathway

- CO2 for Enhanced Oil Recovery (EOR)

- CO2 for Chemical Synthesis (Methanol, Urea & Synthetic Fuels)

- CO2 for Mineralisation & Building Material Production

- CO2 for Food & Beverage Industrial Use

- Geological Permanent Storage (No Utilisation)

- Market Size & Forecast by Syngas End-Use Application

- Power Generation (Integrated Gasification Combined Cycle, IGCC)

- Hydrogen Production (Blue Hydrogen via Coal Gasification & CCUS)

- Synthetic Natural Gas (SNG) Production

- Chemicals & Fertiliser Feedstock (Ammonia, Methanol & Oxochemicals)

- Coal-to-Liquids (CTL) & Synthetic Fuel Production

- Direct Reduced Iron (DRI) & Low-Carbon Steel Production

- Market Size & Forecast by Project Scale

- Large-Scale Commercial Integrated Gasification-CCUS Plants (Above 1 Mtpa CO2 Captured)

- Medium-Scale Industrial & Demonstration Projects (0.1 to 1 Mtpa CO2 Captured)

- Small-Scale Pilot & Early Commercial Projects (Below 0.1 Mtpa CO2 Captured)

- Market Size & Forecast by Project Stage

- Operational

- Under Construction & Final Investment Decision (FID)

- Front-End Engineering Design (FEED) & Pre-FEED

- Concept & Early Development

- Market Size & Forecast by Sales Channel

- EPC & Turnkey Integrated Gasification-CCUS Project Contract

- Technology Licensing & Process Design Package

- Equipment Supply & System Integration

- CO2 Transport & Storage Service Contract

- North America Coal Gasification & CCUS Integration Market Outlook

- Market Size & Forecast

- By Value

- By Volume (CO2 Captured, Metric Tonnes per Annum)

- By Gasification Technology

- By CCUS Technology

- By Carbon Utilisation Pathway

- By End-Use Application

- By Project Scale

- By Sales Channel

- By Country

- Market Size & Forecast

- Europe Coal Gasification & CCUS Integration Market Outlook

- Market Size & Forecast

- By Value

- By Volume (CO2 Captured, Metric Tonnes per Annum)

- By Gasification Technology

- By CCUS Technology

- By Carbon Utilisation Pathway

- By End-Use Application

- By Project Scale

- By Sales Channel

- By Country

- Market Size & Forecast

- Asia-Pacific Coal Gasification & CCUS Integration Market Outlook

- Market Size & Forecast

- By Value

- By Volume (CO2 Captured, Metric Tonnes per Annum)

- By Gasification Technology

- By CCUS Technology

- By Carbon Utilisation Pathway

- By End-Use Application

- By Project Scale

- By Sales Channel

- By Country

- Market Size & Forecast

- Latin America Coal Gasification & CCUS Integration Market Outlook

- Market Size & Forecast

- By Value

- By Volume (CO2 Captured, Metric Tonnes per Annum)

- By Gasification Technology

- By CCUS Technology

- By Carbon Utilisation Pathway

- By End-Use Application

- By Project Scale

- By Sales Channel

- By Country

- Market Size & Forecast

- Middle East & Africa Coal Gasification & CCUS Integration Market Outlook

- Market Size & Forecast

- By Value

- By Volume (CO2 Captured, Metric Tonnes per Annum)

- By Gasification Technology

- By CCUS Technology

- By Carbon Utilisation Pathway

- By End-Use Application

- By Project Scale

- By Sales Channel

- By Country

- Market Size & Forecast

- Country-Wise* Coal Gasification & CCUS Integration Market Outlook

- Market Size & Forecast

- By Value

- By Volume (CO2 Captured, Metric Tonnes per Annum)

- By Gasification Technology

- By CCUS Technology

- By Carbon Utilisation Pathway

- By End-Use Application

- By Project Scale

- By Sales Channel

- By Country

- Market Size & Forecast

- *Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Italy, Norway, Sweden, China, Japan, India, Australia, South Korea, Singapore, Brazil, Chile, Saudi Arabia, UAE, Egypt, South Africa, Israel

- Technology Landscape & Innovation Analysis

- Entrained-Flow Gasifier Technology Deep-Dive: Dry-Feed vs. Slurry-Feed Design, Refractory, Syngas Cooling & Scale-Up

- Pre-Combustion CO2 Capture Technology: Acid Gas Removal, Selexol, Rectisol & Physical Solvent Process Optimisation

- Underground Coal Gasification (UCG) Technology: In-Situ Process, Cavity Control, Water Management & CCUS Integration

- IGCC Power Generation Technology with CCUS: Turbine Integration, Hydrogen Co-Firing & Net-Zero IGCC Pathways

- Blue Hydrogen Production via Coal Gasification & CCUS: Water-Gas Shift, Hydrogen Purification & Cost Competitiveness

- CO2 Utilisation Technology: Methanol Synthesis, Power-to-X Integration & Mineralisation Pathways from Coal Gasification CO2

- Digital Twin, AI Process Optimisation & Advanced Control Technology for Integrated Gasification-CCUS Plants

- Patent & IP Landscape in Coal Gasification & CCUS Integration Technologies

- Value Chain & Supply Chain Analysis

- Coal Supply, Handling, Preparation & Feedstock Logistics Supply Chain

- Gasifier Vessel, Refractory, Burner & Syngas Cooling Equipment Manufacturing Supply Chain

- Acid Gas Removal, CO2 Compression, Dehydration & Purification Equipment Supply Chain

- CO2 Pipeline, Injection Well, Monitoring & Geological Storage Infrastructure Supply Chain

- Technology Licensor, Process Design Package & Proprietary Equipment Provider Channel

- EPC Contractor, Project Developer & Integrated Plant Delivery Channel

- Offtaker, Hydrogen Off-Taker, Power Purchaser & CO2 Credit Buyer Channel

- Pricing Analysis

- Integrated Coal Gasification & CCUS Plant Capital Cost & Total Cost of Ownership (TCO) Analysis

- Blue Hydrogen Levelised Cost of Production (LCOP) from Coal Gasification & CCUS vs. Competing Routes

- CO2 Capture Cost Per Tonne Analysis by Technology: Pre-Combustion vs. Post-Combustion vs. Oxy-Fuel

- CO2 Transport & Geological Storage Cost Per Tonne Analysis by Distance & Formation Type

- Carbon Credit, 45Q Tax Credit & ETS Value Analysis for Coal Gasification-CCUS Project Economics

- IGCC Power Generation Levelised Cost of Electricity (LCOE) with CCUS vs. Alternative Low-Carbon Power Sources

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Coal Gasification & CCUS Integration: Net Carbon Balance, Energy Penalty, Water Use & Solid Waste

- Net CO2 Abatement Potential: Capture Rate, Leakage Risk & Permanence of Geological Storage

- Co-Pollutant Reduction: SOx, NOx, Particulate & Mercury Capture in Integrated Gasification-CCUS Systems

- Just Transition Considerations: Coal Community Employment, Skills Transfer & Social Impact of Gasification-CCUS Projects

- Alignment with NDCs, Net Zero Pathways & IPCC Carbon Budget: Role of Coal Gasification-CCUS in National Decarbonisation Strategies

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Technology, Application & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Gasification Technology, CCUS Route & Geography

- Player Classification

- Gasification Technology Licensors & Process Design Package Providers

- CO2 Capture Technology Licensors & Solvent Process Providers

- Integrated Engineering, Procurement & Construction (EPC) Contractors

- CO2 Transport & Storage Infrastructure Developers & Operators

- Coal & Energy Companies Developing Gasification-CCUS Projects

- Industrial Gas & Chemicals Companies Utilising Coal Gasification-CCUS Syngas

- Competitive Analysis Frameworks

- Market Share Analysis by Gasification Technology, CCUS Route & Region

- Company Profile

- Company Overview & Headquarters

- Gasification & CCUS Technology Portfolio & Process Licensing Capabilities

- Key Customer Relationships & Reference Project Installations

- Operational & Pipeline Project Portfolio & CO2 Capture Capacity

- Revenue (Gasification & CCUS Segment) & Project Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (FID Decisions, Project Awards, Technology Agreements)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Maturity vs. Project Pipeline Scale)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Gasification Technology, CCUS Route, Carbon Utilisation, Application & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output