Market Definition

The India Green Steel Market encompasses the production, processing, commercialization, and end-use application of steel manufactured through low-emission and decarbonized steelmaking pathways that achieve materially lower carbon dioxide and greenhouse gas intensity relative to India’s prevailing conventional steelmaking methods, which are dominated by coal-based blast furnace and basic oxygen furnace integrated production routes that emit approximately 2.5 to 2.6 metric tons of carbon dioxide per metric ton of crude steel produced, among the highest emissions intensities of any major steel-producing nation globally. Green steel within the Indian market context encompasses steel produced through multiple low-emission production pathways including hydrogen-based direct reduced iron production using green hydrogen generated from renewable electricity-powered electrolysis, natural gas-based direct reduced iron production using India’s established gas-based sponge iron sector with progressive hydrogen blending and carbon capture integration, scrap-based electric arc furnace steelmaking powered by renewable electricity procured through open access or captive renewable power purchase agreements, and hybrid transition technologies incorporating top gas recycling, partial hydrogen injection into blast furnaces, and coal gasification with carbon capture integration into existing integrated steel plant configurations. India’s direct reduced iron and electric arc furnace sector, which already accounts for approximately 42% of domestic crude steel production through the gas and coal-based sponge iron and induction furnace route, provides a structurally advantaged foundation for transitioning toward green steel production as green hydrogen costs decline and renewable electricity availability expands across major steel-producing states. Key participants include integrated steel producers, sponge iron and electric arc furnace steelmakers, green hydrogen developers, renewable energy companies, government bodies including the Ministry of Steel and the Bureau of Energy Efficiency, steel-consuming industries in automotive and construction, and financial institutions providing green finance and sustainability-linked capital for steelmaking decarbonization programs.

Market Insights

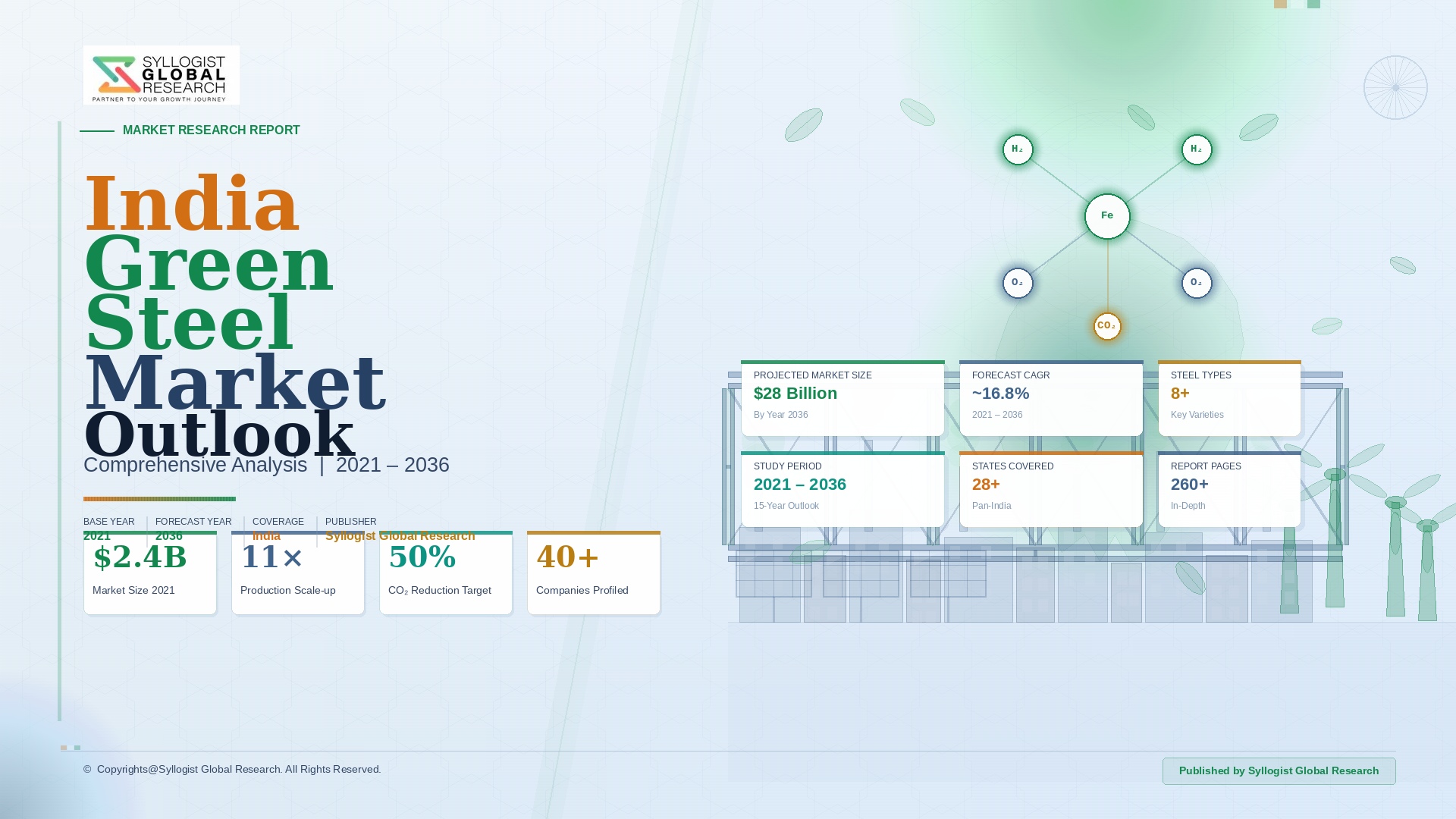

The India green steel market was valued at approximately USD 1.6 billion in 2025 and is projected to reach USD 18.4 billion by 2034, advancing at a compound annual growth rate of 31.2% over the forecast period from 2027 to 2034, representing the highest projected growth rate among all major national green steel markets globally, driven by India’s combination of rapidly expanding steel production capacity, ambitious government decarbonization policy commitments, a large and growing domestic renewable energy sector providing increasingly cost-competitive clean electricity for steelmaking applications, and the strategic imperative of maintaining export market access as carbon border adjustment mechanisms in the European Union and potentially other jurisdictions progressively impose carbon cost penalties on high-emission imported steel products. India’s total crude steel production reached approximately 143 million metric tons in 2025, with green steel produced through certified low-emission routes accounting for approximately 3.2% of total domestic production volume, a share that is projected to increase to approximately 28.6% by 2034 as major producers including Tata Steel, JSW Steel, Steel Authority of India Limited, and Jindal Steel and Power advance their respective green steel investment and transition programs in response to both regulatory requirements and commercial customer demand. The Indian government’s target of achieving 300 million metric tons of annual steel production capacity by 2030 as part of the National Steel Policy, combined with the commitment to reduce the steel sector’s emissions intensity by 30% by 2030 relative to 2005 levels under India’s Nationally Determined Contributions to the Paris Agreement, creates a policy architecture that simultaneously drives steel capacity expansion and decarbonization investment, generating a unique market dynamic where green steel growth is supported by both volume expansion and emissions intensity reduction imperatives operating in parallel.

India’s existing gas-based direct reduced iron and electric arc furnace production ecosystem, which has been built over four decades of sponge iron manufacturing development concentrated in Odisha, Chhattisgarh, Jharkhand, and West Bengal, provides a materially lower-cost and nearer-term pathway to green steel production compared to European or East Asian steelmakers that are predominantly transitioning from coal-based blast furnace operations requiring complete asset replacement. The gas-based direct reduced iron route, used by producers including Essar Steel, Ispat Industries heritage plants, and JSW Steel’s Vijayanagar complex, operates with emissions intensity of approximately 1.1 to 1.4 metric tons of carbon dioxide per metric ton of steel, already substantially below the blast furnace and basic oxygen furnace route intensity, and can achieve near-zero emissions through progressive blending of green hydrogen into direct reduced iron shaft furnace operations without requiring full facility replacement, with technical studies demonstrating that existing Midrex and HYL shaft furnace designs can accept hydrogen blends of 30% to 100% with targeted retrofitting investment estimated at USD 80 to USD 140 million per million metric tons of direct reduced iron capacity. The scrap-based electric arc furnace segment represents the most immediately deployable green steel pathway in India, with approximately 56 million metric tons of electric arc furnace and induction furnace steel capacity already operating in the country that can achieve green steel certification status by transitioning to renewable electricity sourcing through open access procurement, captive solar or wind power installation, or green electricity tariff agreements with state distribution companies, at a capital and operational cost that is substantially lower than the greenfield hydrogen-based facility investment required for blast furnace replacement routes.

The Indian government’s National Green Hydrogen Mission, launched in January 2023 with a total outlay of approximately USD 2.4 billion including production-linked incentive support for green hydrogen production targeting 5 million metric tons of annual domestic green hydrogen production capacity by 2030, represents the most consequential policy intervention for the long-term competitiveness of hydrogen-based green steel in India, as green hydrogen cost reduction is the single most important variable governing the timeline and economics of transitioning India’s substantial direct reduced iron sector from natural gas feedstock to green hydrogen operation. Green hydrogen production cost in India is currently estimated at approximately USD 4.2 to USD 5.6 per kilogram depending on electrolyzer technology, renewable electricity cost, and plant scale, compared to the approximately USD 0.8 to USD 1.2 per kilogram effective cost of the natural gas-derived hydrogen currently used in gas-based direct reduced iron operations, representing a cost gap of approximately USD 3.0 to USD 4.5 per kilogram that translates into a green steel production premium of approximately USD 220 to USD 340 per metric ton relative to natural gas-based direct reduced iron steel at current green hydrogen cost levels. India’s rapidly declining solar power tariff, which reached a record low of approximately USD 0.021 per kilowatt-hour in competitive auction results in 2025 and is projected to decline further toward USD 0.015 per kilowatt-hour by 2030 as solar capacity deployment scales under the 500 gigawatt renewable energy target, provides a credible pathway for Indian green hydrogen production cost to decline toward USD 1.4 to USD 1.8 per kilogram by the early 2030s, at which point hydrogen-based green steel production economics in India would be among the most competitive globally due to the combination of low renewable electricity cost, established direct reduced iron manufacturing capability, and lower labor and construction cost relative to European or North American greenfield green steel investment.

The demand landscape for green steel within India is being shaped by the convergence of export market carbon compliance requirements, domestic corporate sustainability procurement commitments, and public infrastructure investment programs that are progressively creating commercial pull for low-emission steel across the country’s major steel-consuming sectors. Indian steel exporters face a structurally urgent decarbonization imperative arising from the European Union Carbon Border Adjustment Mechanism, which entered its transitional reporting phase in 2023 and will require importers of Indian steel entering the EU market to surrender carbon certificates equivalent to the embedded carbon content of imported steel from 2026 onward, directly imposing a carbon cost penalty on India’s conventional blast furnace steel exports that is estimated at approximately USD 90 to USD 130 per metric ton under projected EU carbon prices, incentivizing export-oriented Indian steelmakers to invest in green production capability to preserve EU market access competitiveness. Domestic demand pull is emerging from India’s automotive sector, where Tata Motors, Mahindra and Mahindra, and the Indian manufacturing subsidiaries of Maruti Suzuki, Hyundai, and Toyota are beginning to incorporate supply chain decarbonization requirements within their supplier engagement frameworks as part of broader environmental, social, and governance commitments, creating an initial demand signal for domestically produced green steel that is expected to strengthen materially as Indian automotive manufacturers align with global parent company net-zero commitments through the forecast period.

Key Drivers

European Union Carbon Border Adjustment Mechanism and Export Market Carbon Compliance Requirements Creating an Urgent Commercial Imperative for Indian Steel Export Decarbonization

The implementation of the European Union Carbon Border Adjustment Mechanism represents a direct and quantifiable financial incentive for Indian steel producers to invest in green steel production capability, as the mechanism imposes a carbon certificate cost equivalent to the EU Emissions Trading System carbon price on the embedded carbon content of steel exported to European markets, creating an estimated per-metric-ton export cost increase of approximately USD 90 to USD 130 for conventional Indian blast furnace steel at projected EU carbon price levels through the late 2020s, that will progressively erode the price competitiveness of India’s steel exports to Europe unless domestic steel producers reduce their production emissions intensity toward EU-comparable levels through green steel investment. India exported approximately 6.7 million metric tons of steel products to the European Union in 2024, representing approximately 14% of total Indian steel exports by volume and a disproportionate share of higher-value flat-rolled and specialty steel export revenue, making EU market access preservation a commercially significant driver of green steel investment for India’s major export-oriented producers including Tata Steel, JSW Steel, and Jindal Stainless. Beyond the European Union, similar carbon border adjustment considerations are emerging in the United Kingdom, which has announced plans for a parallel Carbon Border Adjustment Mechanism aligned with the UK Emissions Trading Scheme, and in Australia, Canada, and Japan, which are each evaluating comparable trade measures, collectively suggesting that carbon border carbon pricing will progressively extend across India’s key export market geography through the forecast period, amplifying the commercial case for green steel investment among Indian steelmakers with diversified export portfolios.

India’s National Green Hydrogen Mission, Declining Renewable Energy Costs, and Production Linked Incentive Policy Support Enabling Competitive Green Hydrogen Supply for Steelmaking

India’s structural advantage in low-cost solar and wind electricity generation, reinforced by the government’s ambitious 500 gigawatt renewable energy capacity target by 2030 and a policy framework that has consistently delivered renewable energy auction tariffs well below global averages, is creating the foundational cost conditions for India to develop among the world’s most competitive green hydrogen production economics by the early 2030s, directly enabling hydrogen-based green steel production at cost levels that can support commercially viable green premium pricing structures within both domestic and export markets. The National Green Hydrogen Mission’s production-linked incentive of approximately USD 0.46 to USD 0.50 per kilogram for domestically produced green hydrogen across a five-year eligibility window is reducing the effective near-term cost of green hydrogen for early-mover Indian steel producers adopting hydrogen blending or full hydrogen-based direct reduced iron operations, supporting investment decisions in advance of standalone commercial competitiveness and allowing the construction of the hydrogen supply infrastructure and operational experience required to benefit from the full cost reduction trajectory projected for Indian green hydrogen through 2030. Strategic green hydrogen supply clusters are emerging in Rajasthan, Gujarat, Andhra Pradesh, and Tamil Nadu, states that combine the highest renewable energy resource quality in India with proximity to coastal export infrastructure and established industrial chemical and energy infrastructure, providing the geographic foundation for dedicated green hydrogen supply chains serving steelmaking facilities in adjacent industrial corridors through dedicated pipeline and logistics networks.

National Steel Policy Capacity Expansion Ambitions, Infrastructure-Led Domestic Steel Demand Growth, and Public Sector Green Procurement Requirements Sustaining Structural Investment in Green Steel

India’s National Steel Policy targets a domestic crude steel production capacity of 300 million metric tons per year by 2030 and 500 million metric tons per year by 2047, representing a more than tripling of 2025 production capacity within the policy horizon, with the government’s explicit commitment to ensuring that a substantial portion of this capacity addition is built on low-emission technology platforms including hydrogen-ready direct reduced iron facilities, renewable electricity-powered electric arc furnaces, and other green steelmaking configurations, creating a structural policy mandate that channels capacity investment toward green steel-compatible infrastructure rather than additional conventional blast furnace capacity. The Indian government’s infrastructure investment program, including the National Infrastructure Pipeline committing approximately USD 1.4 trillion in infrastructure spending through 2030 across roads, railways, ports, urban housing, and renewable energy projects, is generating sustained and large-volume domestic demand for construction steel that is progressively being channeled through public procurement frameworks incorporating embodied carbon assessment requirements, with the Green Rating for Integrated Habitat Assessment green building certification system and the Bureau of Indian Standards low-carbon construction material specifications creating the institutional basis for preferential public procurement of certified green steel in government-funded infrastructure projects, establishing a publicly supported near-term demand base that supports green steel market development independent of private sector premium acceptance.

Key Challenges

High Green Hydrogen Production Cost Relative to Natural Gas and Coal Feedstock Alternatives Creating a Substantial Green Steel Production Premium That Limits Near-Term Market Penetration

The current production cost of green hydrogen in India at approximately USD 4.2 to USD 5.6 per kilogram is approximately four to five times higher than the effective cost of natural gas-derived hydrogen used in existing gas-based direct reduced iron operations, generating a green steel production cost premium of approximately USD 220 to USD 340 per metric ton relative to natural gas-based direct reduced iron steel that substantially restricts green steel market penetration to premium export applications and large corporate sustainability procurement programs willing to pay a certified green premium, while leaving the vast majority of India’s domestic steel consumption in price-sensitive construction, infrastructure, and industrial applications commercially unreachable for green steel at current cost economics. The timeline for green hydrogen cost reduction toward the USD 1.5 to USD 2.0 per kilogram threshold required for broadly competitive green steel production economics in India is highly sensitive to the pace of electrolyzer manufacturing scale-up, renewable energy capacity commissioning, and transmission and distribution infrastructure development that collectively determine the delivered cost of renewable electricity at steel plant and electrolyzer facility locations, each of which involves capital deployment, permitting, land acquisition, and grid integration timelines that create execution risk around the green hydrogen cost reduction pathway. Additionally, India’s coal-based sponge iron and induction furnace sector, which produces approximately 38 million metric tons of steel annually using domestically mined coal at very low input costs, represents a price floor for domestic steel that is structurally difficult for any premium-priced green steel product to compete against within the unregulated domestic commodity steel market in the absence of a domestic carbon price or emissions performance standard for steelmakers.

Inadequate Green Electricity Grid Infrastructure, Transmission Constraints, and Renewable Energy Intermittency Limiting Reliable Clean Power Access for Steel Plant Electrification

The geographic mismatch between India’s highest-quality renewable energy resources, concentrated in the solar-rich states of Rajasthan, Gujarat, and Andhra Pradesh and the wind-rich coastal regions of Tamil Nadu and Karnataka, and the established locations of India’s major steel production clusters in Odisha, Chhattisgarh, Jharkhand, and the eastern industrial belt, creates a fundamental transmission infrastructure challenge for delivering cost-competitive renewable electricity to steel plants at the scale and reliability required for continuous industrial operations, with current inter-state transmission capacity insufficient to support large-scale renewable power procurement by steel plants located in eastern India from renewable generation assets in western and southern states. India’s electric grid infrastructure, while expanding rapidly under the National Transmission Plan and Green Energy Corridors program, faces persistent bottlenecks arising from right-of-way acquisition delays, state distribution company financial constraints, and technical challenges of integrating high proportions of variable renewable energy into grids that must maintain frequency stability for continuous industrial loads, creating reliability risk for steel producers dependent on renewable electricity that can require expensive battery storage, backup power, or grid balancing arrangements that increase the effective cost of green electricity procurement. The open access electricity procurement framework, which allows industrial consumers to procure power directly from renewable generators bypassing state distribution companies, faces state-specific regulatory barriers including high open access charges, wheeling and transmission fees, and cross-subsidy surcharges that vary materially across Indian states and in several major steel-producing states increase the delivered cost of open access renewable power sufficiently to partially or fully erode the cost advantage of renewable electricity relative to conventional coal-based grid power for steel plant applications.

Fragmented Domestic Steel Industry Structure, Dominance of Small-Scale Induction Furnace Producers, and Limited Green Finance Access Constraining Industry-Wide Decarbonization Pace

India’s steel industry is characterized by a highly fragmented production structure in which approximately 60% of total crude steel output originates from small and medium-scale induction furnace, electric arc furnace, and coal-based sponge iron producers that individually lack the capital resources, technical capability, management bandwidth, and access to green finance instruments required to undertake meaningful green steel transition investment programs, creating a structural challenge for achieving industry-wide decarbonization at the pace required by India’s climate commitments and export market carbon compliance requirements that cannot be addressed solely through the investment programs of the large integrated steelmakers. Small induction furnace operators, which collectively account for approximately 28 million metric tons of annual steel production, operate with thin margins, limited balance sheet capacity, and predominantly short-term financing structures that are fundamentally incompatible with the long payback periods and capital intensity of renewable energy procurement agreements, direct reduced iron retrofitting, or electrolyzer installations, and are likely to remain largely outside the green steel transition absent targeted government financial support programs, technology subsidy mechanisms, or green steel cluster development initiatives that aggregate demand for renewable electricity and shared green hydrogen supply across multiple smaller producers. The domestic green finance ecosystem in India, while growing through instruments including green bonds, sustainability-linked loans, and climate finance facilities offered by development finance institutions, remains insufficiently developed in terms of product availability, tenor, and cost to support the estimated USD 180 to USD 220 billion of decarbonization capital investment that the Indian steel sector requires through 2050, necessitating substantial expansion of transition finance instruments, blended finance structures, and concessional capital programs supported by multilateral development banks and domestic financial institutions to bridge the green investment gap.

Market Segmentation

- Segmentation By Production Technology

- Green Hydrogen-Based Direct Reduced Iron and Electric Arc Furnace (H2-DRI-EAF)

- Natural Gas Direct Reduced Iron with Hydrogen Blending and Carbon Capture

- Scrap-Based Electric Arc Furnace with Renewable Electricity

- Coal-Based Sponge Iron with Biomass or Biochar Co-Processing

- Hybrid Transition Technologies (Partial Hydrogen Injection, Top Gas Recycling, Coal Gasification with CCS)

- Others

- Segmentation By Product Type

- Flat-Rolled Green Steel (Hot-Rolled Coil, Cold-Rolled Coil, Galvanized and Pre-Painted Sheet)

- Long Green Steel Products (Reinforcing Bar, Wire Rod, Angles, Channels, and Structural Sections)

- Green Steel Tubes, Pipes, and Hollow Sections

- Green Stainless and Specialty Alloy Steel

- Green Steel Billets, Blooms, and Slabs (Semi-Finished)

- Others

- Segmentation By Carbon Intensity Classification

- Near-Zero Emission Steel (Below 0.4 Metric Tons CO2 per Metric Ton of Steel)

- Low-Carbon Steel (0.4 to 1.0 Metric Tons CO2 per Metric Ton of Steel)

- Transitional Low-Carbon Steel (1.0 to 1.6 Metric Tons CO2 per Metric Ton of Steel)

- Segmentation By Certification and Standard

- Bureau of Indian Standards Low-Carbon Steel Certified

- ResponsibleSteel or Equivalent International Standard Certified

- Science Based Targets Initiative Steel Sector Pathway Aligned

- EU Taxonomy or Carbon Border Adjustment Mechanism Compliant

- Buyer-Specific OEM or Export Market Defined Green Steel Certification

- Others

- Segmentation By End-Use Industry

- Automotive and Light Vehicle Manufacturing

- Commercial Vehicle and Heavy Transport Equipment

- Building and Construction (Reinforcing Bar, Structural Steel, and Roofing)

- Infrastructure (Roads, Railways, Bridges, Ports, and Metro Systems)

- Renewable Energy Infrastructure (Wind Towers, Solar Mounting Structures)

- Mechanical Engineering, Industrial Machinery, and Capital Equipment

- Packaging, Consumer Goods, and Appliances

- Defence and Aerospace

- Others

- Segmentation By Sales Channel

- Long-Term Offtake Agreements and Green Steel Purchase Commitments

- Spot Market and Short-Term Contract Sales

- Export Market Direct Supply (EU CBAM Compliant and Other Export Channels)

- Government and Public Procurement Programs

- Book-and-Claim Certificate-Based Green Steel Attribution

- Others

- Segmentation By Producer Type

- Large Integrated Steel Producers (Tata Steel, JSW Steel, SAIL, Jindal Steel and Power)

- Mid-Scale Electric Arc Furnace and Sponge Iron Producers

- Small Induction Furnace and Secondary Steel Producers

- New Entrant Green Steel Ventures and Joint Ventures

- Others

- Segmentation By Region

- North India

- South India

- East India

- West India

- Central India

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total market valuation of the India Green Steel Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by production technology including hydrogen-based direct reduced iron and electric arc furnace, natural gas direct reduced iron with hydrogen blending and carbon capture, scrap-based electric arc furnace with renewable electricity, and transitional hybrid routes, and by end-use industry including automotive, construction, infrastructure, renewable energy, and export market supply, to enable Indian steel producers, green hydrogen developers, renewable energy companies, export-oriented steel manufacturers, government policy planners, and sustainability-linked investors to identify which production pathways and demand sectors will generate the largest absolute green steel revenue and the most commercially resilient growth trajectory through 2034?

- How is the European Union Carbon Border Adjustment Mechanism implementation timeline, carbon certificate cost trajectory under projected EU Emissions Trading System pricing, and the emerging carbon border adjustment frameworks in the United Kingdom, Australia, and Japan expected to affect the competitive export economics of Indian conventional blast furnace steel in key export markets, and what is the estimated per-metric-ton carbon cost penalty facing Indian steel exporters under each scenario, which Indian steelmakers are most exposed by export volume and product mix, and what green steel investment timeline and production pathway is required for major Indian steel exporters to maintain competitive EU and other regulated market access without bearing prohibitive carbon adjustment costs through 2034?

- What is the green hydrogen production cost reduction trajectory in India through 2034 under the National Green Hydrogen Mission production-linked incentive program, projected solar and wind electricity tariff decline curves, electrolyzer capital cost learning rates applicable to Indian deployment conditions, and emerging green hydrogen supply cluster development in Rajasthan, Gujarat, Andhra Pradesh, and Tamil Nadu, and at what green hydrogen cost level and projected year does hydrogen-based direct reduced iron green steel production in India achieve cost parity with natural gas-based direct reduced iron steel and with conventional blast furnace steel respectively, and what are the key policy, infrastructure, and technology milestones governing the pace of this cost reduction trajectory?

- What are the decarbonization investment programs, green steel technology transition roadmaps, hydrogen procurement and supply chain strategies, renewable energy sourcing approaches, green finance instruments accessed, and export market green steel positioning of India’s major steel producers including Tata Steel, JSW Steel, Steel Authority of India Limited, Jindal Steel and Power, and Jindal Stainless, and how are these producers differentiating their green steel commercial propositions through certified emissions intensity, product grade range, long-term customer supply agreements, and alignment with international green steel certification frameworks that satisfy the procurement requirements of multinational automotive and construction customers and EU CBAM compliance obligations?

- What are the key barriers preventing India’s large population of small and medium-scale induction furnace and electric arc furnace steel producers from participating in the green steel transition, including capital access constraints, renewable electricity procurement limitations arising from state-specific open access regulatory frameworks, technical capability gaps, and green steel certification cost and complexity, and what policy interventions including green steel cluster development programs, aggregated renewable energy procurement frameworks, concessional green transition finance instruments, and technology subsidy mechanisms are required to accelerate decarbonization across the fragmented secondary steel sector that accounts for approximately 60% of India’s total crude steel production volume?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Technology & Commercialisation Risk

- Raw Material & Supply Chain Risk

- Regulatory & Policy Risk

- Market & Demand Risk

- Financial & Investment Risk

- Social & Just Transition Risk

- Regulatory Framework & Standards

- India Green Steel Policy & Classification Framework

- Energy Efficiency & Emission Standards for Indian Steel

- Environmental Clearance & Land Regulations

- Trade, Carbon Border & Export Standards

- Scrap, Circular Economy & Waste Regulations

- India Green Steel Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Million Tonnes of Crude Steel)

- Market Size & Forecast by Production Route / Technology

- Green Hydrogen-Based Direct Reduced Iron + Electric Arc Furnace (H-DRI + EAF)

- Pilot-Scale H-DRI + EAF Plants (Pre-Commercial, 2025-2028)

- Commercial-Scale H-DRI + EAF Plants (2028 Onwards)

- H-DRI Shaft Furnace (Midrex H2, HYL/Energiron H2) Technology Route

- H-DRI Fluidised Bed Reactor Technology Route (HYFOR, Circored)

- Natural Gas / LNG-Based Direct Reduced Iron + EAF (Transition Bridge Route)

- Conventional Gas-DRI (Midrex, HYL) with RE-Powered EAF

- Gas-DRI with Partial Green H2 Blending (H2-Enriched DRI, 5-30% H2)

- Coal-Based DRI (SL/RN Rotary Kiln) + EAF Transitioned to RE Power

- Scrap-Based Electric Arc Furnace (EAF) Powered by Renewable Energy

- EAF with 100% Renewable Energy (Captive Solar/Wind + Storage)

- EAF with Partial Renewable Energy + Grid Power (RE Certificate / REC)

- Induction Furnace (IF) Based Secondary Steel with RE Power (SME Segment)

- Blast Furnace: Basic Oxygen Furnace (BF-BOF) with Carbon Capture, Utilisation & Storage (CCUS)

- BF-BOF + Post-Combustion Carbon Capture (Amine Scrubbing, Chemical Looping)

- Top Gas Recycling Blast Furnace (TGR-BF) with CO2 Separation & Reuse

- Smelting Reduction (HIsarna) + CCS as Zero-Carbon BF Alternative

- Biomass & Biocoal-Based Steelmaking

- Biomass / Torrefied Biomass (Biocoal) as Pulverised Coal Injection (Bio-PCI) Substitute in BF

- Charcoal-Based Mini Blast Furnace (Applicable to Smaller Indian Plants)

- Agricultural Residue Biomass (Rice Husk, Sugarcane Bagasse) Briquette as Reductant in Rotary Kiln DRI

- Electrolysis-Based Steelmaking (Emerging / R&D Stage in India)

- Molten Oxide Electrolysis (MOE): Early R&D Stage at NML Jamshedpur

- Hydrogen Plasma Reduction: CSIR & IIT Research Programmes

- Electrowinning of Iron from Iron Ore Solution: Long-Term Research Pathway

- Market Size & Forecast by Carbon Intensity Category (India Green Steel Taxonomy)

- GS1 Category: Below 1.6 tCO2 per Tonne of Crude Steel (Near-Zero / Deep Green)

- GS2 Category: Between 1.6 and 2.0 tCO2 per Tonne of Crude Steel (Transitional Green)

- GS3 Category: Between 2.0 and 2.5 tCO2 per Tonne of Crude Steel (Low-Carbon Threshold)

- Business-as-Usual (BaU) Benchmark: Above 2.5 tCO2 per Tonne (Conventional Indian Steel)

- Market Size & Forecast by Product Type

- Long Products

- Green Steel Bars & Rods (TMT / HSD Rebars for Infrastructure & Construction)

- Green Steel Wire Rods (Automotive, Fastener & Wire Drawing Applications)

- Green Steel Structural Sections (H-Beams, Channels, Angles for Steel Structures)

- Green Steel Rails (Indian Railways Rolling Stock & Track Applications)

- Flat Products

- Green Steel Hot Rolled Coil (HRC): Automotive, General Engineering

- Green Steel Cold Rolled Coil (CRC): Automotive Body, Appliance & Precision Engineering

- Green Steel Galvanised / Galvalume Coil (Roofing, Pre-Engineered Buildings, Appliances)

- Green Steel Colour Coated Coil (Construction, Appliance & Industrial Applications)

- Green Steel Plates (Shipbuilding, Pressure Vessels, Heavy Engineering, Defence)

- Green Steel Electrical Steel / CRGO (Power Transformer & EV Motor Applications)

- Pipes & Tubes

- Green Steel Seamless Pipes (Oil & Gas, Boiler & High-Pressure Applications)

- Green Steel ERW & Spiral Welded Pipes (Water, Gas Distribution & Structural)

- Green Steel Hollow Section (Construction, Furniture & Agricultural Equipment)

- Stainless Steel & Specialty Green Steel

- Low-Carbon Stainless Steel (300 & 400 Series) from Scrap-Based EAF with RE Power

- Green Alloy Steel (Bearing, Tool, Spring & Case Hardening Grades)

- Green High-Strength Low-Alloy (HSLA) Steel for Automotive Lightweighting

- Market Size & Forecast by End-Use Industry

- Construction & Real Estate

- Residential Building Green Steel Rebar & Structural Sections

- Commercial & Industrial Construction Green Steel (IGBC/LEED Certified Projects)

- Green Building & Net-Zero Energy Building Embodied Carbon Specification

- Infrastructure (Roads, Bridges, Metro Rail, Ports & Airports)

- PM Gati Shakti & NIP: Government Infrastructure Green Steel Procurement

- Metro Rail, RRTS & High-Speed Rail Green Steel for Track & Rolling Stock

- Bridge, Flyover & Elevated Corridor Structural Green Steel

- Automotive & Transportation

- Passenger Vehicle (PV) Body-in-White Green AHSS / UHSS for Lightweighting

- Commercial Vehicle (CV) Frame & Structural Green Steel

- Electric Vehicle (EV) Green Steel: Motor Laminations, Battery Enclosure & Body Structure

- Railways: Wagon, Coach & Locomotive Green Steel Components

- Energy Sector

- Renewable Energy (Wind Tower, Solar Mounting Structure) Green Steel

- Power Transmission Tower & Substation Structure Green Steel

- Oil & Gas Pipeline, Refinery & Upstream Equipment Green Steel

- Nuclear Power Plant Green Steel Components (NPCIL / BHEL Supply Chain)

- General Engineering & Capital Goods

- Industrial Machinery, Fabrication & Agricultural Equipment Green Steel

- Defence & Aerospace Green Steel (HAL, DRDO & OFB Supply Chain)

- Shipbuilding & Offshore Green Steel (Cochin Shipyard, L&T Hazira)

- Consumer Goods & Packaging

- White Goods & Consumer Appliance Green Steel (Refrigerator, Washing Machine Cabinets)

- Steel Packaging (Can, Drum, Container) Green Steel

- Market Size & Forecast by Steel Making Process

- Integrated Route (BF-BOF Based) with Decarbonisation Add-Ons

- EAF-Based Secondary Route (Scrap + RE Power)

- DRI-EAF Route (Coal-Based, Gas-Based & H2-Based DRI)

- Induction Furnace (IF) Based Route (Scrap, RE Power: SME Segment)

- Market Size & Forecast by Certification Standard

- India Ministry of Steel Green Steel Taxonomy Certified (GS1/GS2/GS3)

- ResponsibleSteel International Standard Certified

- ISO 14064 / ISO 14067 Product Carbon Footprint Verified

- SBTi Steel Sector Aligned Producer Certification

- Customer-Specific Green Steel Offtake Agreement Verified (OEM Bilateral)

- Market Size & Forecast by Sales Channel

- Direct OEM & Large Industrial Buyer Supply (B2B Long-Term Offtake Agreements)

- Government & Public Sector Procurement (Railways, Defence, CPWD, NHAI)

- Trader & Stockist Distribution Network

- Export Market Supply (EU, US, Japan, South Korea, Middle East)

- North India Green Steel Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Tonnes)

- By Production Route / Technology

- By Carbon Intensity Category

- By Product Type

- By End-Use Industry

- By Steelmaking Process

- By Certification Standard

- By Sales Channel

- Market Size & Forecast

- West India Green Steel Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Tonnes)

- By Production Route / Technology

- By Carbon Intensity Category

- By Product Type

- By End-Use Industry

- By Steelmaking Process

- By Certification Standard

- By Sales Channel

- Market Size & Forecast

- South India Green Steel Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Tonnes)

- By Production Route / Technology

- By Carbon Intensity Category

- By Product Type

- By End-Use Industry

- By Steelmaking Process

- By Certification Standard

- By Sales Channel

- Market Size & Forecast

- East India Green Steel Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Tonnes)

- By Production Route / Technology

- By Carbon Intensity Category

- By Product Type

- By End-Use Industry

- By Steelmaking Process

- By Certification Standard

- By Sales Channel

- Market Size & Forecast

- Central India Green Steel Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Tonnes)

- By Production Route / Technology

- By Carbon Intensity Category

- By Product Type

- By End-Use Industry

- By Steelmaking Process

- By Certification Standard

- By Sales Channel

- Market Size & Forecast

- State-Wise* India Green Steel Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Tonnes)

- By Production Route / Technology

- By Carbon Intensity Category

- By Product Type

- By End-Use Industry

- By Steelmaking Process

- By Certification Standard

- By Sales Channel

- Market Size & Forecast

*Key States Analyzed: Jharkhand, Odisha, West Bengal, Chhattisgarh, Maharashtra, Gujarat, Andhra Pradesh, Telangana, Karnataka, Tamil Nadu, Uttar Pradesh, Rajasthan, Madhya Pradesh, Haryana, Punjab

- Technology Landscape & Innovation Analysis

- Green Hydrogen-Based DRI (H-DRI) Technology Deep-Dive

- Electric Arc Furnace (EAF) Technology Deep-Dive: India Context

- BF-BOF Decarbonisation Technology Deep-Dive: India Context

- Carbon Capture, Utilisation & Storage (CCUS) Technology: India Assessment

- Renewable Energy & Electrolyser Technology for Green Steel: India

- Scrap Processing & Metallics Technology: India

- Digital, Analytics & Industry 4.0 Technology for Green Steel: India

- Patent & IP Landscape: India Green Steel

- Value Chain & Supply Chain Analysis

- Raw Material Supply Chain: India Green Steel

- Green Steel Technology & Equipment Suppliers

- India Green Steel Producer Landscape

- Downstream Processing & Distribution

- End-of-Life & Circular Economy: India Steel

- Pricing Analysis

- Green Steel vs. Conventional Steel Price Premium Analysis: India

- Production Cost Analysis by Technology Route: India

- Carbon Cost & CBAM Impact on India Steel Pricing

- Capital Expenditure (Capex) Analysis for Green Steel Transition: India

- Green Finance & Incentive Economics: India

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Green Steel Production Routes: India

- GHG Emission Accounting & MRV Framework: India Steel

- Just Transition & Social Sustainability: India Steel Decarbonisation

- Environmental Compliance & Biodiversity: India

- India Net Zero & Climate Policy Alignment

- Competitive Landscape

- Market Structure & Concentration

- India Green Steel Market Consolidation Level: Concentrated (Large Integrated Producers) vs. Fragmented (Mini Mill EAF Segment)

- Top 10 Players Market Share in India Green Steel (Actual & Certified Volume)

- HHI Concentration Analysis by Technology Route, Product Category & Region

- Competitive Intensity Map: Integrated BF-BOF Transitioning Producers vs. EAF-Native Green Players vs. New Greenfield H-DRI Entrants

- Player Classification

- Large Integrated Steel Producers in Green Transition (BF-BOF + Decarbonisation Add-Ons)

- DRI-EAF Based Green Steel Producers (Gas-DRI & H2-DRI Pathway)

- Scrap-Based EAF Green Steel Producers (RE-Powered Mini Mills)

- Public Sector Steel Producers (SAIL, RINL) Under Government Decarbonisation Mandate

- Potential Greenfield H-DRI + EAF New Entrants (Domestic & FDI)

- Secondary Steel Sector (Induction Furnace-Based RE-Powered SME Producers)

- Competitive Analysis Frameworks

- Market Share Analysis by Production Route, Product Type & State

- Company Profile

- Company Overview & India Plant Locations

- Green Steel Technology Portfolio & Certification Status

- Current Carbon Intensity (tCO2/tCS) & Reduction Roadmap

- India Green Steel Installed Capacity & Production Volume

- Revenue (Green Steel Segment) & Financial Performance

- Technology Partnerships, Licensing & EPC Agreements

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Green Steel Milestones, Capex Announcements, Certifications)

- SWOT Analysis: India Green Steel Context

- India Green Steel Strategic Roadmap & 2030 / 2047 Target

- Competitive Positioning Map (Decarbonisation Progress vs. Green Steel Volume)

- Key Company Profiles

- Market Structure & Concentration

- Strategic Opportunity Analysis

- Strategic Output

- White Space Opportunity Analysis

- Strategic Recommendations

- Technology Investment & Green Transition Strategy

- Raw Material & Energy Security Strategy

- Market Development & Commercial Strategy

- Policy Engagement & Regulatory Strategy

- Financing & Capital Structure Strategy

- Sustainability, Just Transition & ESG Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-Term (2025-2028)

- Mid-Term (2029-2032)

- Long-Term (2033-2047)