India Indene Market: Strategic Aromatic Intermediate Supporting Specialty Resin Growth

Enabling Performance Adhesives, Rubber Compounds & Industrial Coatings

The India indene market operates within a specialized segment of the aromatic hydrocarbons value chain, closely linked to domestic coal tar processing and C9 aromatic streams from steam crackers. As a key intermediate derived primarily from coal tar light oil generated by integrated steel plants, indene plays a critical role in the production of coumarone-indene resins, C9 hydrocarbon resins, and modified tackifier systems. In India, rising demand for high-performance adhesives, infrastructure-linked construction chemicals, tire compounding materials, and packaging inks is strengthening the strategic importance of indene-based resin systems. Manufacturers are increasingly investing in improved distillation efficiency, separation technologies, and hydrogenation capabilities to enhance product purity and performance characteristics. While indene remains a niche aromatic compared to benzene or toluene, its relevance is steadily increasing within India’s expanding specialty materials ecosystem.

Mapping the Indian Value Chain: From Coal Tar & C9 Streams to Resin Applications

In India, indene production is primarily linked to coal tar availability from integrated steel producers and coke oven operations. As steel production cycles fluctuate, coal tar generation directly influences indene feedstock supply. Limited volumes also arise from C9 aromatic streams associated with petrochemical crackers, though coal tar remains the dominant source domestically.

Upstream, indene is extracted via fractional distillation and refining of coal tar light oil fractions. Midstream, producers convert indene into:

- Coumarone-indene resins

- C9 hydrocarbon resins

- Modified tackifier resins

- Specialty aromatic derivatives

These derivatives feed into downstream industries such as:

- Adhesives & sealants (laminates, plywood, packaging, construction)

- Rubber & tire manufacturing (tackifiers for compounding efficiency)

- Printing inks (packaging and commercial printing)

- Industrial coatings

Unlike larger aromatics, the Indian indene ecosystem is relatively integrated, with several resin producers maintaining backward linkages into coal tar distillation to secure feedstock and stabilize margins. Increasingly, manufacturers are focusing on product customization, low-color resin development, and hydrogenated grades to meet the evolving performance demands of domestic and export markets.

Balancing Demand and Supply Dynamics in India

Demand for indene in India is structurally aligned with industrial resin consumption, infrastructure growth, packaging expansion, and automotive manufacturing cycles. Rapid growth in plywood, laminates, flexible packaging, and tire production is creating incremental demand for tackifier and hydrocarbon resins. The construction sector, supported by urbanization and infrastructure investments, further drives adhesive consumption.

On the supply side, availability remains inherently constrained by upstream steel production cycles. Any slowdown in steel output affects coal tar availability, thereby tightening indene supply. Additionally, environmental regulations on coke ovens and coal tar processing are influencing operating rates and compliance costs. India’s indene capacity expansion remains limited due to its by-product nature, making feedstock security a key strategic factor.

Key challenges include:

- Volatility in domestic steel production

- Environmental compliance pressures in coal tar distillation

- Limited standalone indene capacity additions

- Increasing purity and consistency requirements for specialty resins

These structural linkages underscore the importance of integration and operational flexibility within the Indian market.

Pricing Dynamics: Feedstock Sensitivity in a By-Product Market

Indene pricing in India is largely driven by coal tar light oil valuations, steel production volumes, and broader C9 aromatic stream economics. Because indene is a fractionated by-product rather than a primary petrochemical output, its pricing closely follows feedstock cost trends rather than independent demand fundamentals.

Regions with strong steel clusters, particularly in eastern and western India, often maintain relative cost advantages due to proximity to coke oven operations. However, fluctuations in steel output, seasonal maintenance shutdowns, and logistics constraints can create temporary tightness in supply and pricing volatility. High-purity or hydrogenated indene derivatives command premium pricing, particularly in applications requiring improved color stability, odor control, and enhanced performance characteristics. Increasing specialization in resin formulations is gradually shifting pricing dynamics toward value-driven differentiation rather than purely feedstock-linked economics.

White Space & Growth Opportunities in India

Several structural opportunities are shaping the Indian indene market outlook. Growth in e-commerce and flexible packaging is accelerating demand for high-performance adhesives and tackifier resins. The expanding domestic tire industry, driven by automotive production and replacement demand, is supporting tackifier consumption in rubber compounding. Additionally, investments in hydrogenation technologies are enabling the production of low-color and high-stability resin grades suitable for premium packaging and export-oriented applications.

Sustainability is also emerging as a long-term theme, with improved coal tar valorization, by-product optimization, and enhanced recovery efficiency strengthening circularity within steel-linked chemical ecosystems. While India remains smaller in scale compared to China in indene processing, its expanding infrastructure, packaging sector, and automotive growth position it as a structurally rising demand center.

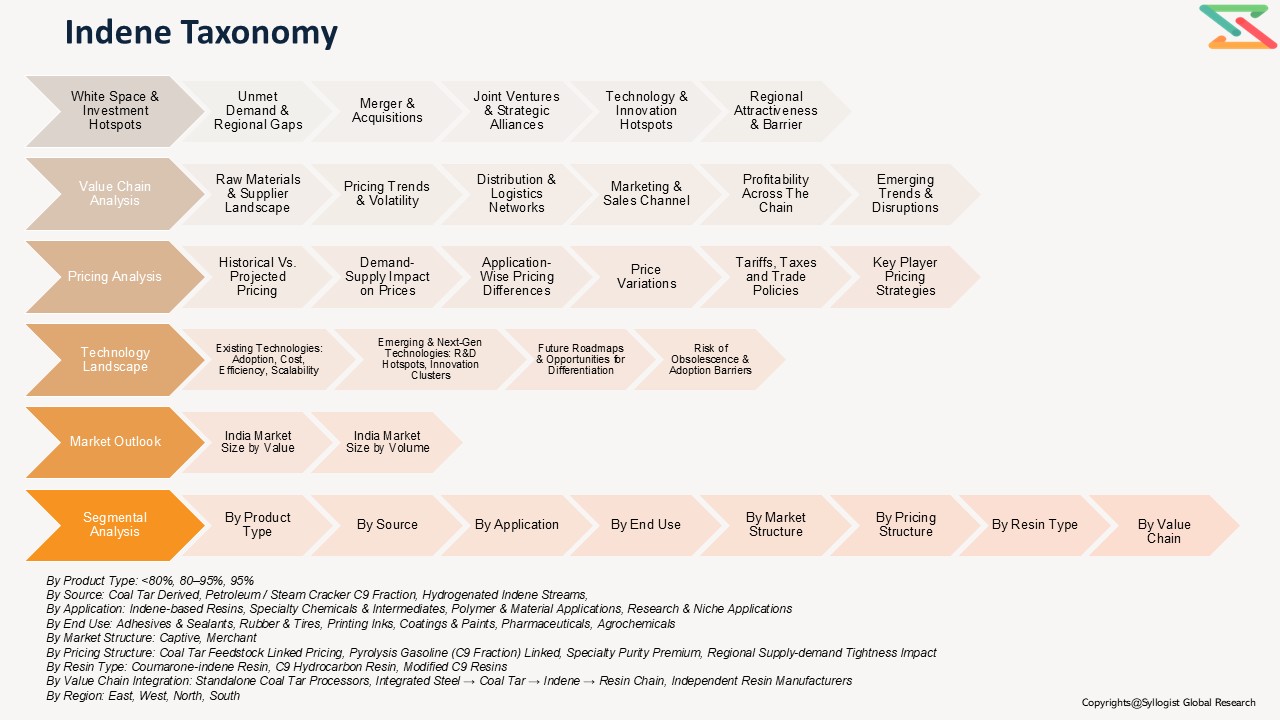

- Introduction (Product Definition, Taxonomy and Research Methodology)

- Executive Summary

- India Indene Demand Supply Analysis

- Global Indene Market Assessment, 2021-2031

- India Indene Market Assessment, 2021-2031

- India Market Outlook (Value, Volume and Segmental Analysis)

- Indene Market Value Chain Analysis

- Raw Material Sourcing & Suppliers

- Key Raw Materials & Inputs

- Supplier Landscape & Concentration

- Pricing Trends & Volatility

- Dependence on Imports vs Domestic Availability

- Distribution & Logistics

- Marketing & Sales Channels

- Value Addition & Profitability Across Chain

- Emerging Trends & Disruptions

- Raw Material Sourcing & Suppliers

- Indene Market Pricing Analysis

- Historical Vs Projected Pricing Analysis

- Demand-Supply Impact on Prices

- Application-wise Pricing Differences

- Impact of Tariffs, Taxes, and Trade Policies

- Key Player Pricing Strategies

- Indene Technology Landscape

- Key Existing Technologies

- Technology Overview

- Advantages & Limitations

- Cost, Efficiency, and Scalability Aspects

- Emerging & Next-gen Technologies

- Pipeline & Under-development Technologies

- R&D Hotspots & Innovation Clusters

- Potential Disruption to Existing Methods

- Strategic Insights

- Future Technology Roadmap

- Opportunities for Differentiation via Technology

- Risks of Obsolescence & Barriers to Adoption

- Policy & Regulatory landscape

- Competition Outlook (Leading 10 Companies)

- Competition Benchmarking

- Market Leaders Vs New Entrants

- Strategic Recommendations

- Key Existing Technologies