Market Definition

The Aluminium Cans market comprises a wide range of lightweight, recyclable metal packaging formats, including beverage cans, aerosol cans, food cans, energy drink cans, craft beer cans, RTD cans, and specialty aluminium packaging, used extensively across the beverage, food, personal care, household, and industrial sectors. Aluminium cans are valued for their superior barrier properties, infinite recyclability, durability, and cost-effective mass production. These cans play a critical role in ensuring product safety, shelf stability, flavor retention, and convenience across global consumer markets. Over the past two years, the aluminium cans industry has been significantly influenced by shifts in sustainability regulations, volatility in aluminium prices, beverage consumption trends, supply-chain disruptions in raw materials (primary aluminium, can sheets), and rapid growth in ready-to-drink (RTD) and craft beverage segments.

Market Insights

Global demand for aluminium cans has been strongly shaped by rising consumption of carbonated soft drinks, energy drinks, beer, sparkling water, iced tea, RTD cocktails, and functional beverages. A major driver has been the accelerating global transition from PET bottles and glass containers to aluminium-based formats due to environmental concerns, higher recycling rates, and growing restrictions on single-use plastics. However, fluctuations in aluminium ingot and can-sheet prices, largely driven by geopolitical tensions, energy price volatility, and global supply tightness, affected production costs and pricing cycles in 2021–2023.

In 2023, demand stabilized with improved raw material availability and operational efficiencies across rolling mills and can manufacturing plants. However, industry consumption remains robust, supported by rising beverage volumes, premium packaging trends, and strong adoption by craft and niche beverage brands. The sector is increasingly shaped by sustainability priorities, such as circular packaging, recycled content mandates, carbon-neutral production, and closed-loop collection systems. Manufacturers are responding through lightweighting, alloy optimization, digital printing, and expansion of recycling infrastructure.

Industry projections indicate that the global aluminium cans market will grow at a steady CAGR of 6.80% between 2026 and 2035, with North America, Europe, and Asia-Pacific continuing to be the largest consumption hubs. Growth is further accelerated by bans on plastic packaging in many countries, increasing brand commitments to 100% recyclable packaging, and growing investments in new can manufacturing lines and recycling plants. Meanwhile, emerging markets in Latin America, ASEAN, and the Middle East are witnessing rapid penetration driven by rising disposable incomes, urbanization, and growing beverage consumption.

Regulatory tightening, particularly around packaging waste, extended producer responsibility (EPR), recycled content mandates, and CO₂ emissions, continues to reshape industry strategies. Manufacturers are investing heavily in low-carbon aluminium, closed-loop recycling, and next-generation can sheet technologies to remain competitive. However, the market remains vulnerable to aluminium price fluctuations, energy cost pressures, and supply bottlenecks at smelters and rolling mills.

Market Dynamics: Drivers

Rising demand for sustainable and recyclable packaging, growth of beverage categories (energy drinks, beer, sparkling water, RTD cocktails), and global push toward reducing plastic waste are the primary factors driving aluminium can adoption. Aluminium’s 100% recyclability, lower carbon footprint (especially with recycled content), and superior product preservation capabilities are accelerating brand transitions from PET/glass to cans. In addition, rapid expansion of the craft beverage industry, e-commerce demand for lightweight packaging, and brand preference for premium metallic aesthetics strengthen market momentum. Government policies that promote recyclable packaging formats and circular economy models further support long-term industry growth.

Market Dynamics: Challenges

The aluminium cans industry faces significant challenges such as raw material cost volatility, dependency on primary aluminium supply from energy-intensive smelters, and periodic shortages in can-sheet availability. High energy prices and geopolitical risks can lead to price spikes, impacting margins for can manufacturers and beverage brands. Recycling infrastructure gaps in emerging markets, contamination of scrap streams, and lack of standardized collection systems restrict the availability of high-quality recycled aluminium. Additionally, growing competition from PET innovations, glass reinvention, and refillable packaging models poses long-term strategic threats. Capital-intensive manufacturing lines, transportation costs, and the need for rapid production scalability also remain key operational constraints.

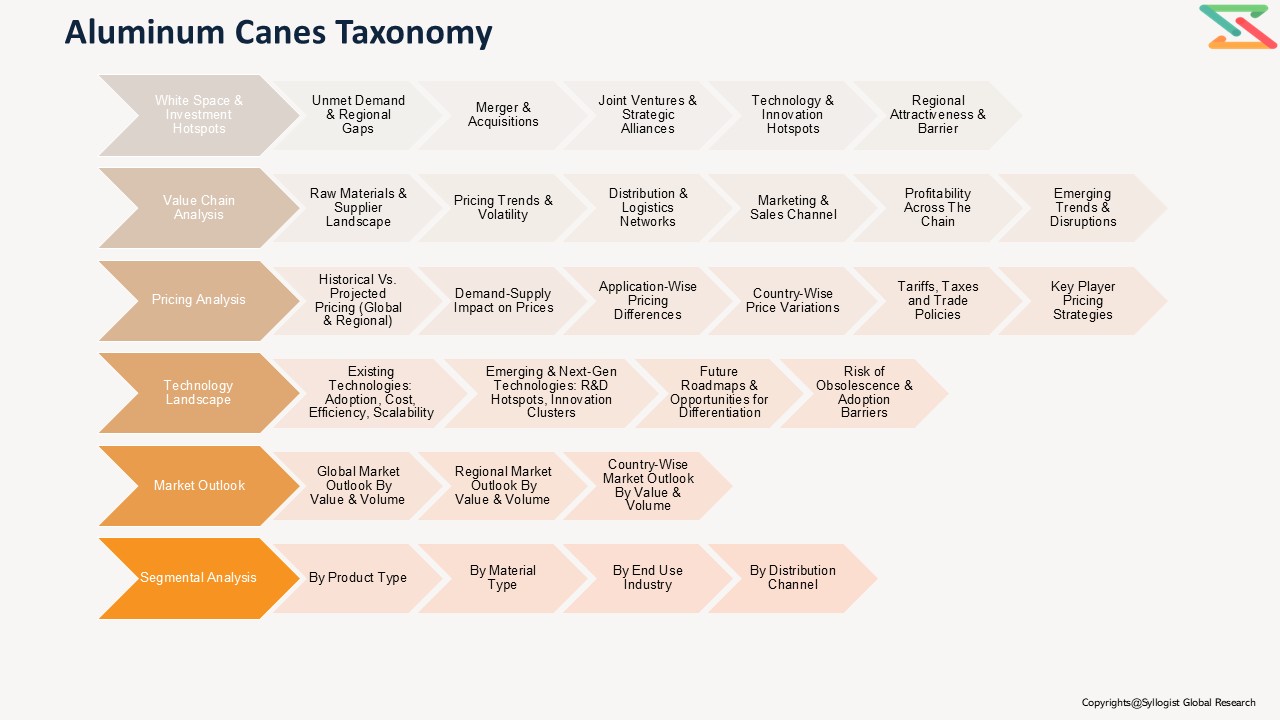

Market Segmentation

Based on Product Type, the Global Aluminium Cans Market is segmented into:

- Standard Beverage Cans (250–500 ml)

• Beer & Craft Beverage Cans

• Energy Drink Cans

• RTD & Functional Beverage Cans

• Food Cans

• Aerosol Cans

• Specialty / Shaped Aluminium Cans

• Others

Based on Can Structure & Technology:

- Two-Piece Draw & Ironed (D&I) Cans

• Three-Piece Cans

• Lacquered / Lined Cans

• Light-Weighting / Thin-Gauge Can Sheet

• Digital / Customized Printed Cans

• Recycled Content / Low-Carbon Aluminium Cans

Based on Application:

- Beverages (CSD, Beer, Energy Drinks, RTD Cocktails, Juices, Water)

• Food Packaging

• Personal Care (Deodorants, Sprays)

• Household Products

• Industrial & Chemical Aerosols

Based on Distribution Channel:

- Beverage Manufacturers & Bottlers

• Food Processing Companies

• Personal Care & Home Care Brands

• Contract Packaging Companies

• Wholesale & Distribution Networks

All market revenues are presented in USD, with volumes expressed in billion cans.

Historical Year: 2020–2025 | Base Year: 2026 | Estimated Year: 2027 | Forecast Period: 2028–2035

Key Questions this Study Will Answer

- What are the key market statistics and forecasts (market size by value & volume, product shares, manufacturing trends) for the Global Aluminium Cans Market?

- What are the regional demand patterns, growth drivers, challenges, and sustainability-led transition trends?

- What technological innovations, recycling developments, regulatory shifts, and environmental mandates are shaping the aluminium cans ecosystem?

- Who are the leading competitors, and how do they benchmark across capacity, product range, geographic reach, sustainability commitments, and pricing?

- What insights emerge from beverage brand interviews, supply chain assessments, and recycling ecosystem evaluations conducted during the market study?

- Market Foundations & Dynamics

- Introduction

- Product Overview (Definition & Scope of Aluminium Cans: Beverage Cans, Food Cans, Aerosol Cans, Specialty & Lightweight Cans)

- Aluminium Can Value Chain Overview (Bauxite → Alumina → Aluminium Smelting → Rolling → Can Sheet → Can Manufacturing → Filling → Distribution → Recycling)

- Research Methodology

- Executive Summary

- Major Trends Shaping the Market (Sustainability Push, Lightweighting, High Recycling Demand, Shift from Plastics to Aluminium)

- Short-Term vs. Long-Term Opportunities

- Comparison of Key Can Types (Beverage Cans, Food Cans, Aerosol Cans, Specialty Cans)

- Scenario Planning (Base, Optimistic, Conservative Demand for Aluminium Packaging)

- Sensitivity Analysis (Aluminium Prices, Energy Costs, Recycling Rates, Regulatory Changes)

- Identification of Regional Growth Hotspots

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Ecosystem & Value Chain

- Overview of Value Chain Participants

- Raw Material Suppliers (Bauxite, Alumina, Primary Aluminium)

- Rolling Mills & Can Sheet Producers

- Can Manufacturers (Body, End, Tab Manufacturers)

- Technology Providers (Coatings, Printing, Lightweighting Technologies)

- Distribution Channels (Beverage Companies, Food Processors, Retailers, FMCG)

- Recycling & Scrap Collection Networks

- Raw Material & Equipment Suppliers

- Flow of Value & Material Through the Chain

- Value Addition & Margins at Each Stage

- Rolling & Sheet Production

- Can Manufacturing & Printing

- Filling & Distribution

- Recycling & Re-melting

- Integration Trends (Vertical Integration by Beverage Companies & Aluminium Producers)

- Impact of Vertical Integration

- Mapping of Roles & Interdependencies

- Market Trends & Developments

- White Space Analysis

- Demand Supply Analysis

- Demand–Supply Gaps (Recycling Shortages, Can Sheet Capacity Constraints)

- Unmet Needs (High-Purity Scrap, Lightweighting, Sustainable Coatings)

- Risk Assessment Framework

- Political / Geopolitical Risk (Bauxite/Alumina Trade Disruptions, Energy Geopolitics)

- Operational Risk (Plant Downtime, High Energy Costs)

- Environmental Risk (Carbon Footprint, Waste Generation)

- Financial Risk (Aluminium Price Volatility, High CAPEX)

- Regulatory Framework & Standards

- Global Regulatory Overview

- Packaging & Food Safety Standards (FDA, EU Regulations)

- Recycling & Circular Economy Norms (EPR, Deposit Return Schemes)

- Carbon Emissions & ESG Reporting Standards

- Local Country Regulations (Packaging Waste Rules, Import Norms)

- Manufacturing & Coating Compliance Standards

- Safety & Quality Standards (Coating Quality, Material Purity)

- Environmental Compliance (Recycling Mandates, Emission Norms)

- Liability & Insurance Requirements

- Digital Traceability (QR Coding, Recycling Tracking Technologies)

- Technology Landscape

- Lightweighting Technologies

- High-Speed Can Manufacturing Innovations

- Coating & Printing Technologies (BPA-Free, Enhanced Durability)

- Automation & Smart Manufacturing Systems

- Recycling Technologies (Closed-Loop Aluminium Recycling)

- Future Outlook (Next-Gen Can Sheet Alloys, Energy-Efficient Smelting, AI-Enabled QC)

- Global, Regional & Country Forecasts (2019–2029)

- Global Aluminium Cans Market Outlook (Value & Volume)

- Market Share by:

- Product Type: Beverage Cans, Food Cans, Aerosol Cans, Specialty Cans

- Material Type (Primary Aluminium, Recycled Aluminium)

- End-Use Industry (Beverages, Food, Personal Care, Industrial)

- Distribution Channel (Beverage Companies, Retailers, FMCG)

- Price Range (Standard, Premium, Specialty)

- Ownership Model (Contract Manufacturing, In-House Production)

- Company

- Regional Outlook (North America, Europe, Asia-Pacific, Latin America, Middle East & Africa)

- Pricing Analysis

- Overview of Pricing Structures (Per Ton, Per Thousand Cans)

- Price Trends by Product Type (Beverage Cans, Food Cans, Aerosol Cans)

- Cost Benchmark

- Primary vs Recycled Aluminium Cost Comparison

- Imported vs Domestic Can Sheet

- Price Sensitivity (Energy Costs, Aluminium Prices, Transportation)

- Historical Pricing (2019–2023)

- Forecast Pricing (2024–2029)

- Factors Influencing Price

- Raw Material Availability

- Energy Costs

- Logistics

- Regulatory Burden

- R&D & Certification Costs

- Regional Pricing Differentiation

- Impact of Sustainability Transition

- Competition Outlook

- Market Concentration vs Fragmentation

- Company Market Shares

- Competitive Strategies

- Capacity Expansion

- Product Diversification (Lightweighting, Specialty Cans)

- Recycling Integration

- Technology Collaborations

- Benchmarking Matrix (Technology vs Price vs Sustainability)

- Recent Developments (M&A, New Plants, Sustainability Initiatives)

- Cost Structure & Margin Analysis

- Detailed Cost Breakdown

- Average Cost per Stage

- Profitability & Margin Distribution

- Sensitivity Analysis (Aluminium Prices, Energy Prices)

- Cost Reduction Opportunities (Recycling, Automation, Efficient Coatings)

- Business Models & Strategic Insights

- Integrated Aluminium Producers

- Contract Can Manufacturers

- Beverage Company In-House Can Production

- Circular Economy & Recycling-Driven Models

- PPP Models for Recycling Infrastructure

- SWOT of Leading Business Models

- Investment & Financial Analysis

- CAPEX & OPEX Benchmarks for Can Sheet & Can Manufacturing

- Payback & IRR Sensitivity

- Financial Modeling Assumptions

- Revenue Streams: Can Sales, Contract Manufacturing, Recycling Credits

- Investment Case Studies

- Funding Landscape (Manufacturing Funds, ESG Investors, Private Equity)

- Sales & Distribution Channel Analysis

- GTM Channels (Beverage Producers, Food Processors, FMCG)

- Channel Share by Region

- Typical Channel Flow Diagram (Aluminium Producer → Can Manufacturer → Filler → Retail)

- Sales Process & Customer Engagement

- Distribution Strategy of Leading Players

- Emerging Trends (Sustainable Packaging Commitments, E-commerce Growth)

- Strategic Recommendations & Roadmap

- Competitor Strategic Initiatives

- Future Outlook (2024–2029: High Recycling Adoption, Premium Cans, Sustainability)

- Strategic Recommendations for Stakeholders

- Adoption Roadmap for High-Recycled-Content Cans

- Tailored Recommendations (Aluminium Producers, Can Makers, Beverage Companies, Regulators)

- Key Success Factors (Recycling Efficiency, Scale, Sustainability, Cost Competitiveness)

- Introduction