Market Definition

Sustainable Packaging refers to the development and use of packaging solutions that have a reduced environmental impact and footprint. It encompasses materials derived from renewable sources (such as bio-based plastics, paper, and plant fibers) as well as optimized designs that utilize recycled content (PCR), minimize material usage (lightweighting), and support circular lifecycles. Through processes such as mechanical recycling, chemical recycling, composting, and responsible sourcing (FSC/PEFC), these materials are converted into key packaging formats: biodegradable films, recycled molded fiber, corrugated board, glass, and reusable metal containers.

These eco-friendly solutions are integral to a wide range of downstream applications including food & beverage, personal care & cosmetics, pharmaceuticals, e-commerce logistics, and industrial shipping. As global industries shift toward a Circular Economy, eliminating single-use virgin plastics and reducing carbon emissions, sustainable packaging has emerged as an essential alternative to traditional fossil-fuel-based packaging systems.

The industry is undergoing a structural transformation driven by Extended Producer Responsibility (EPR) mandates, plastic waste reduction targets, and the rise of “Green Consumerism.” This positions sustainable packaging not merely as a container, but as a critical enabler in the global transition toward waste-free, low-carbon, and regenerative supply chains.

Market Insights

The Sustainable Packaging industry represents a massive, multi-billion-dollar global market anchored by stringent regulations in Europe and North America, and rapidly expanding manufacturing capabilities in Asia-Pacific. The market is projected to witness robust growth through 2035, supported by aggressive corporate sustainability goals across FMCG, retail, and food service sectors.

Paper and Paperboard remain the largest material categories due to high recyclability rates and established infrastructure. However, Recycled Plastics (rPET, rHDPE) are witnessing the fastest growth as brands race to meet “recycled content” quotas. Concurrently, Bioplastics (PLA, PHA) and Molded Fibers (bagasse, bamboo) are gaining traction in food service and niche retail applications as compostable alternatives to polystyrene.

Sustainability-led procurement is transforming the value chain. Global brands like Nestlé, Unilever, and Amazon are prioritizing packaging that is 100% reusable, recyclable, or compostable. As environmental regulations tighten (e.g., EU Packaging and Packaging Waste Regulation), sustainable packaging is shifting from a niche marketing differentiator to a strategic, compliance-linked operational necessity.

Market Dynamics: Drivers

Stringent Regulatory Frameworks & Plastic Bans

Governments worldwide are implementing strict policies to curb plastic waste. The European Union’s Green Deal bans on single-use plastics in major economies (India, Canada, parts of the U.S.), and tax penalties on non-recycled packaging are forcing manufacturers to adopt sustainable alternatives immediately.

Rising Consumer Preference for “Green” Brands

Eco-conscious consumerism is accelerating. Modern shoppers are increasingly willing to pay a premium for products in eco-friendly packaging and punish brands that use excessive plastic. This demand is compelling manufacturers in the personal care, food, and fashion sectors to redesign product portfolios to incorporate biodegradable, minimalist, or refillable packaging solutions.

Technological Innovation in Material Science

The industry is seeing a surge in innovation, including edible packaging, water-soluble films, and barrier coatings that allow paper to replace plastic in wet applications. Advancements in Chemical Recycling are also unlocking the ability to recycle complex, multi-layer materials that were previously destined for landfills, broadening the scope of what is considered “sustainable.”

Market Dynamics: Challenges

High Cost of Sustainable Materials

Bio-based polymers, compostable films, and high-quality Post-Consumer Recycled (PCR) plastics often carry a significant “green premium” compared to cheap virgin plastics. These higher input costs can squeeze margins, particularly for small and mid-sized enterprises (SMEs) operating in price-sensitive markets.

Lack of Standardized Recycling Infrastructure

A major bottleneck is the inconsistency of global waste management infrastructure. While a package may be theoretically “compostable” or “recyclable,” the lack of accessible industrial composting facilities or advanced sorting centers in many regions leads to “wish-cycling,” where sustainable materials still end up in landfills.

Market Segmentation

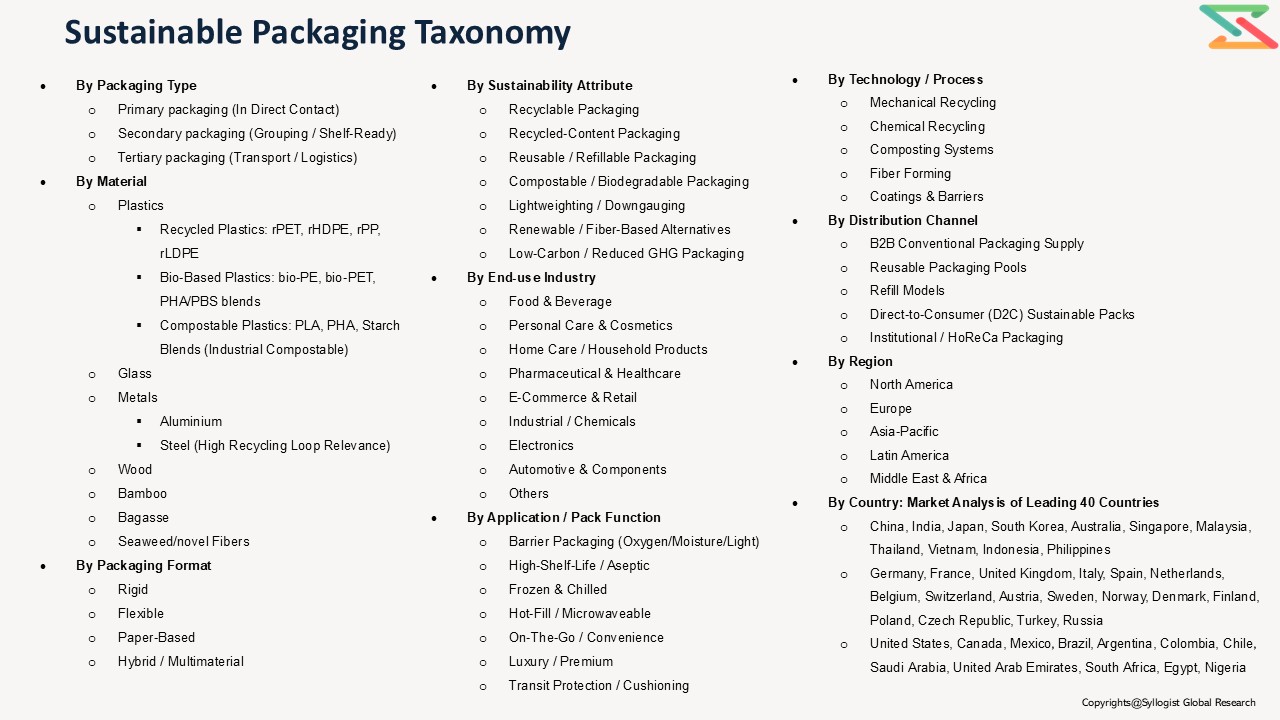

- By Packaging Type

- Primary packaging (In Direct Contact)

- Secondary packaging (Grouping / Shelf-Ready)

- Tertiary packaging (Transport / Logistics)

- By Material

- Plastics

- Recycled Plastics: rPET, rHDPE, rPP, rLDPE

- Bio-Based Plastics: bio-PE, bio-PET, PHA/PBS blends

- Compostable Plastics: PLA, PHA, Starch Blends (Industrial Compostable)

- Glass

- Metals

- Aluminium

- Steel (High Recycling Loop Relevance)

- Wood

- Bamboo

- Bagasse

- Seaweed/novel Fibers

- Plastics

- By Packaging Format

- Rigid

- Flexible

- Paper-Based

- Hybrid / Multimaterial

- By Sustainability Attribute

- Recyclable Packaging

- Recycled-Content Packaging

- Reusable / Refillable Packaging

- Compostable / Biodegradable Packaging

- Lightweighting / Downgauging

- Renewable / Fiber-Based Alternatives

- Low-Carbon / Reduced GHG Packaging

- By End-use Industry

- Food & Beverage

- Personal Care & Cosmetics

- Home Care / Household Products

- Pharmaceutical & Healthcare

- E-Commerce & Retail

- Industrial / Chemicals

- Electronics

- Automotive & Components

- Others

- By Application / Pack Function

- Barrier Packaging (Oxygen/Moisture/Light)

- High-Shelf-Life / Aseptic

- Frozen & Chilled

- Hot-Fill / Microwaveable

- On-The-Go / Convenience

- Luxury / Premium

- Transit Protection / Cushioning

- By Technology / Process

- Mechanical Recycling

- Chemical Recycling

- Composting Systems

- Fiber Forming

- Coatings & Barriers

- By Distribution Channel

- B2B Conventional Packaging Supply

- Reusable Packaging Pools

- Refill Models

- Direct-to-Consumer (D2C) Sustainable Packs

- Institutional / HoReCa Packaging

- By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East & Africa

- By Country: Market Analysis of Leading 40 Countries

- Asia-Pacific: China, India, Japan, South Korea, Australia, Singapore, Malaysia, Thailand, Vietnam, Indonesia, Philippines

- Europe: Germany, France, United Kingdom, Italy, Spain, Netherlands, Belgium, Switzerland, Austria, Sweden, Norway, Denmark, Finland, Poland, Czech Republic, Turkey, Russia

- North America: United States, Canada, Mexico

- Latin America: Brazil, Argentina, Colombia, Chile

- Middle East & Africa: Saudi Arabia, United Arab Emirates, South Africa, Egypt, Nigeria

Revenue: USD Billion

Historical Years: 2020–2024

Base Year: 2025

Estimated: 2026

Forecast: 2027–2035

Key Questions this Study will Answer

- What are the key overall market statistics or market estimates (Market Overview, Market Size- By Value, Market Size-By Volume, Forecast Numbers, Market Segmentation, Market Shares) of Global Sustainable Packaging Market?

- What is the region wise industry size, growth drivers and challenges key market trends?

- What are the key innovations, opportunities, current and future trends and regulations in the Global Sustainable Packaging Market?

- Who are the key competitors, what are their key strengths and weaknesses and how they perform in Global Sustainable Packaging Market based on competitive benchmarking matrix?

- What are the key results derived from the market surveys conducted during Global Sustainable Packaging Market study?

- Market Foundations & Dynamics

- Introduction

- Product Overview (Definition & Scope of Sustainable Packaging)

- Packaging Life-Cycle Overview (Raw Material Sourcing → Conversion → Use → End-of-Life / Circularity)

- Research Methodology

- Executive Summary

- Major Trends Shaping the Market

- Short-Term vs. Long-Term Opportunities

- Comparison of Linear vs. Circular Packaging Pathways

- Scenario Planning (Base, Optimistic, Conservative)

- Sensitivity Analysis

- Identification of regional investment hotspots

- Market Dynamics (Drivers, Restraints, Opportunities, Challenges, Porter’s Five Forces Analysis, PESTLE Analysis)

- Market Ecosystem & Value Chain

- Overview of Value Chain Participants

- Raw Material Suppliers

- Packaging Converters & Manufacturers

- End-Use Brands

- Waste Management & Recycling Facilities

- Flow of Value and Material Through the Chain

- Value Addition and Margins at Each Stage

- Integration Trends

- White Market Space Analysis

- Demand–Supply Gaps

- Investment Hotspots

- Unmet Needs

- Overview of Value Chain Participants

- Risk Assessment Framework

- Political/geopolitical risk

- Operational risk

- Environmental risk

- Financial risk

- Regulatory Framework & Standards

- Global Regulatory Overview

- EU Packaging and Packaging Waste Regulation (PPWR) & Single-Use Plastics Directive

- U.S. State-Level Extended Producer Responsibility (EPR) & FTC Green Guides

- Global Plastics Treaty & UNEP Initiatives

- Compliance & Certification Requirements

- Food-Contact Safety & Quality Standards for Recycled/Bio-Materials (EFSA, FDA)

- Environmental & Liability Considerations (Plastic Taxes, EPR Fees)

- Digital Traceability & Eco-Labeling Initiatives

- Technology Landscape

- Material Innovations

- Advanced Conversion Technologies

- End-of-Life Technologies

- Standardization & Eco-Design Trends

- Global Market Outlook & Forecasts (2020–2035)

- Global Sustainable Packaging Market Outlook (Value in USD Billion, Volume in Kilotons)

- Market Share by Packaging Type

- Primary packaging (In Direct Contact)

- Secondary packaging (Grouping / Shelf-Ready)

- Tertiary packaging (Transport / Logistics)

- Market Share by Material

- Plastics (Recycled Plastics: rPET, rHDPE, rPP, rLDPE; Bio-Based Plastics: bio-PE, bio-PET, PHA/PBS blends; Compostable Plastics: PLA, PHA, Starch Blends)

- Glass

- Metals (Aluminium, Steel – High Recycling Loop Relevance)

- Wood

- Bamboo

- Bagasse

- Seaweed/novel Fibers

- Market Share by Packaging Format

- Rigid

- Flexible

- Paper-Based

- Hybrid / Multimaterial

- Market Share by Sustainability Attribute

- Recyclable Packaging

- Recycled-Content Packaging

- Reusable / Refillable Packaging

- Compostable / Biodegradable Packaging

- Lightweighting / Downgauging

- Renewable / Fiber-Based Alternatives

- Low-Carbon / Reduced GHG Packaging

- Market Share by End-use Industry

- Food & Beverage

- Personal Care & Cosmetics

- Home Care / Household Products

- Pharmaceutical & Healthcare

- E-Commerce & Retail

- Industrial / Chemicals

- Electronics

- Automotive & Components

- Others

- Market Share by Application / Pack Function

- Barrier Packaging (Oxygen/Moisture/Light)

- High-Shelf-Life / Aseptic

- Frozen & Chilled

- Hot-Fill / Microwaveable

- On-The-Go / Convenience

- Luxury / Premium

- Transit Protection / Cushioning

- Market Share by Technology / Process

- Mechanical Recycling

- Chemical Recycling

- Composting Systems

- Fiber Forming

- Coatings & Barriers

- Sales & Distribution Channel Analysis

- Market Share by Distribution Channel

- B2B Conventional Packaging Supply

- Reusable Packaging Pools

- Refill Models

- Direct-to-Consumer (D2C) Sustainable Packs

- Institutional / HoReCa Packaging

- Overview of Go-to-Market Channels

- Partnership Models (Converter + FMCG, Innovator + Retailer)

- Market Share by Distribution Channel

- Regional & Country Outlook (2020-2035)

- Asia-Pacific: China, India, Japan, South Korea, Australia, Singapore, Malaysia, Thailand, Vietnam, Indonesia, Philippines

- Europe: Germany, France, United Kingdom, Italy, Spain, Netherlands, Belgium, Switzerland, Austria, Sweden, Norway, Denmark, Finland, Poland, Czech Republic, Turkey, Russia

- North America: United States, Canada, Mexico

- Latin America: Brazil, Argentina, Colombia, Chile

- Middle East & Africa: Saudi Arabia, United Arab Emirates, South Africa, Egypt, Nigeria

- Pricing Analysis

- Overview of Pricing Structures (per ton / per unit basis)

- Average Selling Price (ASP) Trends by Material Type

- Cost Benchmark: Virgin Plastics vs. Recycled Plastics (PCR) vs. Bioplastics/Fiber

- Price Sensitivity by End-use Industry

- Historical Price Evolution & Forecast Pricing Curve (2025–2035)

- Factors Influencing Price

- Regional Pricing Differentiation

- Competition Outlook

- Market Concentration and Fragmentation Level

- Company Market Shares (Top 10 Players)

- Competitive Strategies

- Benchmarking Matrix

- Recent Developments

- Cost Structure & Margin Analysis

- Detailed Cost Breakdown

- Profitability and Margin Distribution Along Value Chain (Resin Producer → Converter → Brand)

- Cost Reduction Opportunities via Process Intensification & Scalability

- Business Models & Strategic Insights

- FMCG-Led Circular Models

- Packaging-as-a-Service (PaaS) & Reusable Pools

- Closed-Loop Retailer Take-Back Programs

- Economic Viability Comparison of Models

- SWOT Analysis of Leading Sustainable Packaging Models

- Strategic Recommendations & Roadmap

- Competitors’ Strategic Initiatives

- Future Outlook

- Technology Advancements to Watch

- Circular Economy Integration Roadmap

- Sustainable Packaging Acceleration Roadmap

- Short-term

- Mid-term

- Long-term

- Tailored recommendations for:

- Material Innovators & Resin Producers

- Packaging Converters

- End Users (FMCG & Retail)

- Recommendations on Key Success Factors