Product Overview: Aniline as a Strategic Intermediate for Polyurethanes, Rubber Chemicals, and Specialty Chemicals

Aniline is a fundamental aromatic amine widely used as a key intermediate in the production of methylene diphenyl diisocyanate (MDI), rubber-processing chemicals, dyes and pigments, agrochemicals, and select pharmaceutical intermediates. In China, its consumption pattern is heavily oriented toward large-scale industrial applications, particularly polyurethane production. This reflects the country’s strong presence in downstream sectors such as construction insulation, furniture, appliances, footwear, automotive components, and industrial manufacturing. Consequently, aniline in China functions not just as a specialty intermediate but as a high-volume upstream feedstock embedded in several major manufacturing value chains.

Demand, Supply, and Consumption: China as the Global Hub of Aniline Production and Usage

China represents the largest aniline market globally, supported by substantial domestic production capacity and strong downstream demand. The country hosts multiple large-scale chemical complexes producing aniline primarily for captive use in MDI manufacturing and other industrial applications. Because of its scale advantage, China is both a major producer and an exporter, supplying aniline to international markets when global supply conditions tighten. Domestic demand continues to rise due to expansion in polyurethane manufacturing, automotive production, appliances, and construction materials. Overall, China’s aniline market is large and mature but continues to grow steadily, supported by expanding downstream industrial sectors.

Market Dynamics: Polyurethane Expansion Drives Demand While Industrial Cycles Influence Market Stability

The primary growth engine for China’s aniline market is the expansion of polyurethane demand, especially rigid and flexible foam used in insulation materials, refrigeration equipment, furniture, automotive seating, and footwear manufacturing. The rubber industry also represents a significant consumption segment through the production of rubber-processing chemicals used in tire manufacturing and industrial rubber products. However, the market remains sensitive to industrial cycles, particularly those affecting construction and manufacturing. When downstream polyurethane demand weakens, it can quickly impact aniline production rates and pricing. Export competition and fluctuations in feedstock prices can also influence market stability.

Technology and Raw Materials: Nitrobenzene Hydrogenation Dominates Production

The predominant production route for aniline in China involves the nitration of benzene to produce nitrobenzene, followed by catalytic hydrogenation of nitrobenzene to yield aniline. This process remains the industry standard due to its efficiency, scalability, and cost effectiveness. Benzene serves as the primary raw material, with hydrogen and nitric acid used in the manufacturing chain. Technological improvements in China are focused on catalyst efficiency, process optimization, energy reduction, and environmental compliance. New catalyst systems and improved reactor technologies are helping producers enhance yield, reduce by-products, and lower operating costs while maintaining high product purity.

Growth Hotspots: Eastern Chemical Clusters and MDI Applications Lead Market Expansion

China’s aniline demand is concentrated in major chemical manufacturing clusters located in eastern and coastal regions where integrated petrochemical complexes and polyurethane production facilities are located. These regions benefit from strong infrastructure, export connectivity, and proximity to downstream industries. By application, MDI production remains the dominant and fastest-growing consumption segment for aniline. Rubber-processing chemicals and dye intermediates provide additional demand support, although their growth is slower compared with polyurethane-linked applications. High-consistency industrial grades designed for large-scale manufacturing processes represent the most commercially attractive product segment in the market.

Recent Trends and Conclusion: Shift Toward Integrated Chemical Production and Efficiency Improvements

Recent developments indicate that China’s aniline market is evolving toward greater integration with downstream polyurethane and specialty chemical production. Rather than relying solely on commodity chemical production, many manufacturers are focusing on integrated value chains that combine feedstock processing, intermediate production, and downstream material manufacturing. At the same time, environmental regulations and efficiency requirements are encouraging investments in cleaner production technologies and improved process optimization. Overall, China will likely remain the central hub of the global aniline value chain due to its scale, strong downstream industries, and continued investment in integrated chemical manufacturing infrastructure.

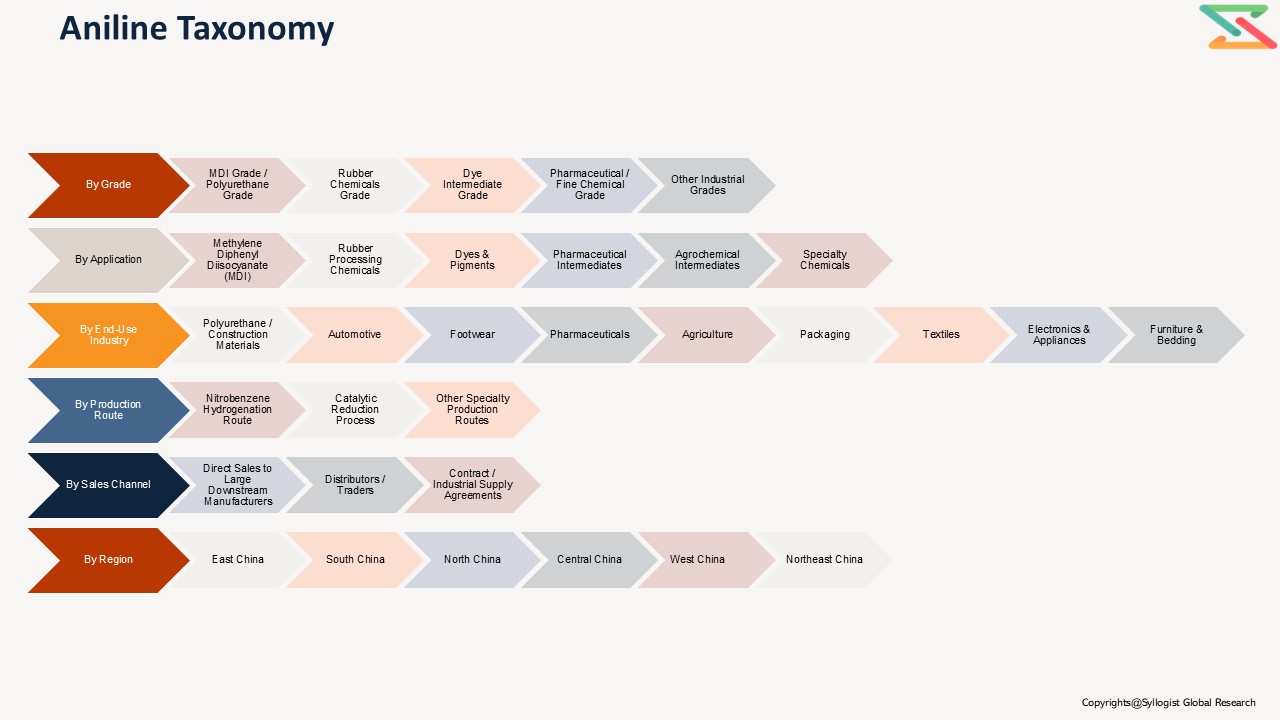

Market Segmentation

- Segmentation by Grade

- MDI Grade / Polyurethane Grade

- Rubber Chemicals Grade

- Dye Intermediate Grade

- Pharmaceutical / Fine Chemical Grade

- Other Industrial Grades

- Segmentation by Application

- Methylene Diphenyl Diisocyanate (MDI)

- Rubber Processing Chemicals

- Antioxidants

- Accelerators

- Dyes & Pigments

- Pharmaceutical Intermediates

- Agrochemical Intermediates

- Specialty Chemicals

- Segmentation by End Use Industry

- Polyurethane / Construction Materials

- Automotive

- Footwear

- Furniture & Bedding

- Electronics & Appliances

- Textiles

- Packaging

- Agriculture

- Pharmaceuticals

- Segmentation by Production Route

- Nitrobenzene Hydrogenation Route

- Catalytic Reduction Process

- Other Specialty Production Routes

- Segmentation by Sales Channel

- Direct Sales to Large Downstream Manufacturers

- Distributors / Traders

- Contract / Industrial Supply Agreements

- Segmentation by Region

- East China

- South China

- North China

- Central China

- West China

- Northeast China

- Introduction (Product Definition, Taxonomy and Research Methodology)

- Executive Summary

- Global Aniline Demand Supply Analysis

- Global Aniline Market Assessment, 2021-2036

- Global Market Outlook (Value, Volume and Segmental Analysis)

- China Aniline Market Assessment, 2021-2036

- Market Size & Forecast by Value

- Market Size & Forecast by Volume

- Market Size & Forecast by Grade

- MDI Grade / Polyurethane Grade

- Rubber Chemicals Grade

- Dye Intermediate Grade

- Pharmaceutical / Fine Chemical Grade

- Other Industrial Grades

- Market Size & Forecast by Application

- Methylene Diphenyl Diisocyanate (MDI)

- Rubber Processing Chemicals

- Antioxidants

- Accelerators

- Dyes & Pigments

- Pharmaceutical Intermediates

- Agrochemical Intermediates

- Specialty Chemicals

- Market Size & Forecast by End Use Industry

- Polyurethane / Construction Materials

- Automotive

- Footwear

- Furniture & Bedding

- Electronics & Appliances

- Textiles

- Packaging

- Agriculture

- Pharmaceuticals

- Market Size & Forecast by Production Route

- Nitrobenzene Hydrogenation Route

- Catalytic Reduction Process

- Other Specialty Production Routes

- Market Size & Forecast by Sales Channel

- Direct Sales to Large Downstream Manufacturers

- Distributors / Traders

- Contract / Industrial Supply Agreements

- Market Size & Forecast by Region

- East China

- South China

- North China

- Central China

- West China

- Northeast China

- White Space & Emerging Investment Hotspot

- Market White Space Opportunities

- Mergers & Acquisitions (M&A)

- Joint Ventures & Strategic Alliances

- Technology & Innovation Hotspots

- Regional Investment Attractiveness

- Barriers & Risks in Investment

- China Aniline Market Value Chain Analysis

- Raw Material Sourcing & Suppliers

- Key Raw Materials & Inputs

- Supplier Landscape & Concentration

- Pricing Trends & Volatility

- Dependence on Imports vs Domestic Availability

- Distribution & Logistics

- Marketing & Sales Channels

- Value Addition & Profitability across Chain

- Emerging Trends & Disruptions

- Raw Material Sourcing & Suppliers

- China Aniline Market Pricing Analysis

- Historical Vs Projected Pricing Analysis

- Demand-Supply Impact on Prices

- Application-wise Pricing Differences

- Impact of Tariffs, Taxes, and Trade Policies

- Key Player Pricing Strategies

- China Aniline Technology Landscape

- Key Existing Technologies

- Emerging & Next-gen Technologies

- Strategic Insights

- Future Technology Roadmap

- Opportunities for Differentiation via Technology

- Risks of Obsolescence & Barriers to Adoption

- Policy & Regulatory landscape

- Competition Outlook (Leading 10 Companies)

- Competition Benchmarking

- Market Leaders Vs New Entrants

- Strategic Recommendations