Market Definition

Pigments are insoluble particulate solids that are physically dispersed in a medium, such as polymers, resins, or solvents, to provide color, opacity, durability, and specialized functional properties. Unlike dyes, which dissolve into the substrate, pigments remain as discrete particles, offering superior resistance to UV radiation, chemical degradation, and extreme weather conditions. The market is broadly categorized into inorganic pigments (e.g., Titanium Dioxide, Iron Oxides), which dominate by volume due to their opacity and low cost; organic pigments (e.g., Azo, Phthalocyanine), valued for their vibrant hues and transparency; and specialty pigments, including metallic, pearlescent, and high-performance varieties that offer unique light-interference effects or specialized thermal stability.

Market Insights

One of the most profound shifts in the current landscape is the rapid ascent of High-Performance Pigments (HPPs) and specialty effect colorants. As consumers demand more sophisticated finishes in the automotive and electronics sectors, manufacturers are moving beyond basic reds and blues to angle-dependent, multi-layered pigments that provide chameleon effects and metallic lusters. These high-value colorants are no longer just aesthetic choices; they are increasingly integrated with functional benefits, such as Infrared (IR)-reflective properties that help reduce the heat island effect in urban architecture and improve the battery efficiency of electric vehicles by lowering cabin cooling requirements.

Geographically, the Asia-Pacific region continues to serve as the global engine for both production and consumption, accounting for over 45% of the market share. The center of gravity for pigment manufacturing has decisively shifted toward China and India, fueled by massive domestic infrastructure projects and their roles as the world’s primary hubs for plastic and textile manufacturing. While North American and European markets are characterized by high-value, low-volume specialty procurement driven by strict environmental standards, the APAC market is defined by its sheer scale and the rapid adoption of localized, high-precision blending facilities that bring supply chains closer to major industrial clusters.

The primary growth engine for the market remains the robust expansion of the global construction and automotive industries. Urbanization in emerging economies has created a massive, non-negotiable demand for architectural coatings that require long-lasting, weather-resistant pigments like Iron Oxide and Titanium Dioxide. Simultaneously, the rise of smart cities is driving a need for functional pigments that provide more than just color, such as anti-corrosive and antimicrobial coatings. However, these drivers are frequently balanced against the significant challenge of stringent environmental regulations, such as Europe’s REACH and new bans on PFAS and certain heavy metals. These mandates are forcing expensive reformulations and future-proofing of product lines, which can squeeze margins for smaller players. Furthermore, the market is highly sensitive to raw material price volatility, specifically in the petrochemical intermediates and mineral ores (like cobalt and copper) used for high-end inorganic types, and the ongoing digitalization of media, which continues to erode demand for traditional publication inks.

Key Drivers

- The primary engine propelling the market in 2026 is the aggressive expansion of global infrastructure and the automotive renaissance. With the construction sector projected to reach new heights, particularly in the Asia-Pacific region and emerging Middle Eastern hubs, there is a non-negotiable demand for high-durability inorganic pigments like Titanium Dioxide (TiO2) and Iron Oxides. These materials are essential for architectural coatings that must withstand extreme weather, UV degradation, and urban pollutants. Simultaneously, the automotive sector is shifting toward Electric Vehicles (EVs), which require specialized high-performance pigments (HPPs) for battery pack insulation and cool IR-reflective coatings that help manage cabin temperatures. This industrial synergy ensures that pigments remain a critical, physics-based asset in the global supply chain, far beyond mere aesthetic application.

- Beyond heavy industry, the market is being revitalized by the Green Chemistry revolution and functional intelligence. As consumer awareness regarding environmental footprints peaks, manufacturers are pivoting toward bio-based colorants and high-purity organic pigments that comply with zero-VOC mandates. Innovation is no longer just about color vibrancy; it is about functional performance, such as antimicrobial pigments for healthcare environments and laser-sensitive pigments for high-speed digital packaging. The rise of e-commerce has also necessitated a surge in food-contact-safe and UV-curable inkjet pigments, turning the packaging industry into a high-value growth corridor. This shift from commodity colorants to value-added, sustainable solutions is allowing leading players to command premium pricing in a historically margin-sensitive landscape.

Key Challenges

- Despite these growth catalysts, the industry faces significant headwinds from an increasingly complex regulatory landscape and raw material volatility. Stringent environmental protocols, such as the EU’s REACH and the evolving PFAS-free mandates, are forcing manufacturers into costly R&D cycles to replace established but hazardous chemistries. Furthermore, the market remains highly sensitive to the fluctuating prices of petrochemical intermediates and mineral ores (like cobalt and copper), which can lead to sudden cost-push inflation for end-users. Trade tensions and newly imposed tariffs on critical inputs like TiO2 have further fragmented the supply chain, forcing a strategic near-shoring of production. For many smaller players, the high CAPEX required to upgrade to eco-friendly, high-precision manufacturing processes creates a formidable barrier to entry, favoring larger, vertically integrated consolidators.

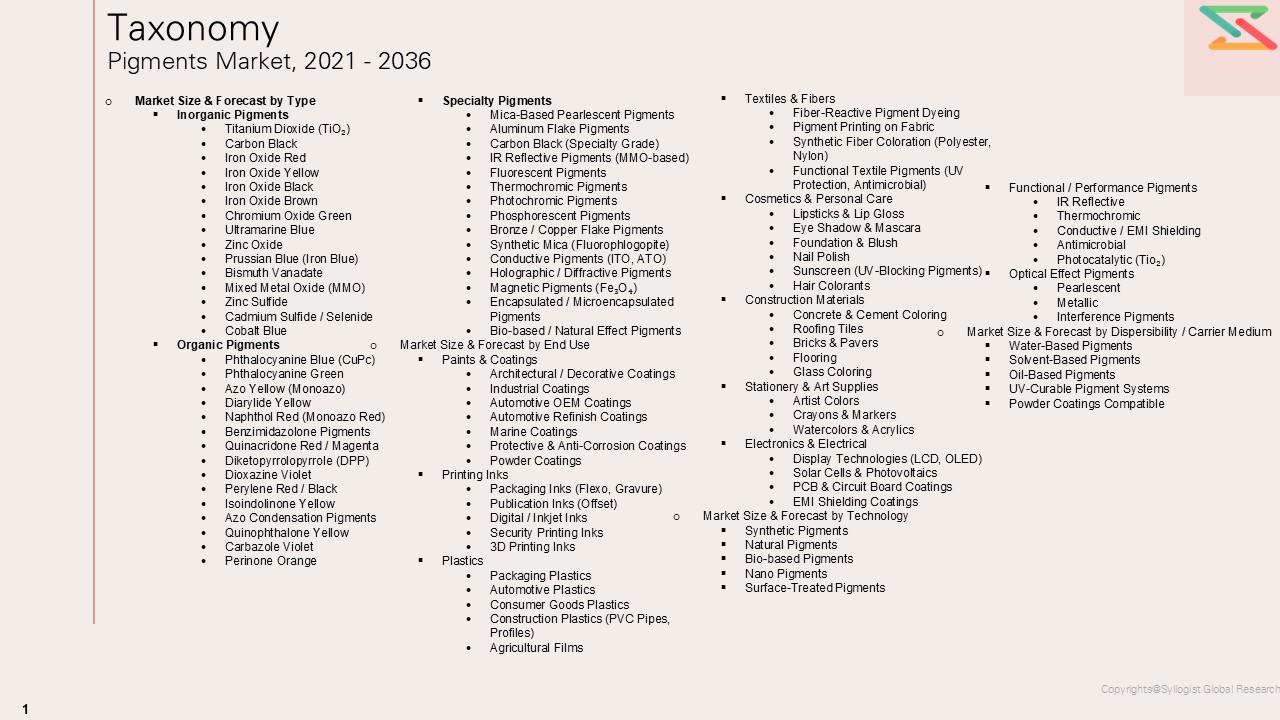

Market Segmentation

- Segmentation by Type

- Inorganic Pigments

- Titanium Dioxide (TiO₂)

- Carbon Black

- Iron Oxide Red

- Iron Oxide Yellow

- Iron Oxide Black

- Iron Oxide Brown

- Chromium Oxide Green

- Ultramarine Blue

- Zinc Oxide

- Prussian Blue (Iron Blue)

- Bismuth Vanadate

- Mixed Metal Oxide (MMO)

- Zinc Sulfide

- Cadmium Sulfide / Selenide

- Cobalt Blue

- Organic Pigments

- Phthalocyanine Blue (CuPc)

- Phthalocyanine Green

- Azo Yellow (Monoazo)

- Diarylide Yellow

- Naphthol Red (Monoazo Red)

- Benzimidazolone Pigments

- Quinacridone Red / Magenta

- Diketopyrrolopyrrole (DPP)

- Dioxazine Violet

- Perylene Red / Black

- Isoindolinone Yellow

- Azo Condensation Pigments

- Quinophthalone Yellow

- Carbazole Violet

- Perinone Orange

- Specialty Pigments

- Mica-Based Pearlescent Pigments

- Aluminum Flake Pigments

- Carbon Black (Specialty Grade)

- IR Reflective Pigments (MMO-based)

- Fluorescent Pigments

- Thermochromic Pigments

- Photochromic Pigments

- Phosphorescent Pigments

- Bronze / Copper Flake Pigments

- Synthetic Mica (Fluorophlogopite)

- Conductive Pigments (ITO, ATO)

- Holographic / Diffractive Pigments

- Magnetic Pigments (Fe₃O₄)

- Encapsulated / Microencapsulated Pigments

- Bio-based / Natural Effect Pigments

- Inorganic Pigments

- Segmentation by End Use

- Paints & Coatings

- Architectural / Decorative Coatings

- Industrial Coatings

- Automotive OEM Coatings

- Automotive Refinish Coatings

- Marine Coatings

- Protective & Anti-Corrosion Coatings

- Powder Coatings

- Printing Inks

- Packaging Inks (Flexo, Gravure)

- Publication Inks (Offset)

- Digital / Inkjet Inks

- Security Printing Inks

- 3D Printing Inks

- Plastics

- Packaging Plastics

- Automotive Plastics

- Consumer Goods Plastics

- Construction Plastics (PVC Pipes, Profiles)

- Agricultural Films

- Textiles & Fibers

- Fiber-Reactive Pigment Dyeing

- Pigment Printing on Fabric

- Synthetic Fiber Coloration (Polyester, Nylon)

- Functional Textile Pigments (UV Protection, Antimicrobial)

- Cosmetics & Personal Care

- Lipsticks & Lip Gloss

- Eye Shadow & Mascara

- Foundation & Blush

- Nail Polish

- Sunscreen (UV-Blocking Pigments)

- Hair Colorants

- Construction Materials

- Concrete & Cement Coloring

- Roofing Tiles

- Bricks & Pavers

- Flooring

- Glass Coloring

- Stationery & Art Supplies

- Artist Colors

- Crayons & Markers

- Watercolors & Acrylics

- Electronics & Electrical

- Display Technologies (LCD, OLED)

- Solar Cells & Photovoltaics

- PCB & Circuit Board Coatings

- EMI Shielding Coatings

- Paints & Coatings

- Segmentation by Technology

- Synthetic Pigments

- Natural Pigments

- Bio-based Pigments

- Nano Pigments

- Surface-Treated Pigments

- Segmentation by Functional Property

- Decorative / Coloring Pigments

- Protective Pigments

- Anti-Corrosion

- UV Protection

- Functional / Performance Pigments

- IR Reflective

- Thermochromic

- Conductive / EMI Shielding

- Antimicrobial

- Photocatalytic (Tio₂)

- Optical Effect Pigments

- Pearlescent

- Metallic

- Interference Pigments

- Segmentation by Dispersibility / Carrier Medium

- Water-Based Pigments

- Solvent-Based Pigments

- Oil-Based Pigments

- UV-Curable Pigment Systems

- Powder Coatings Compatible

- Segmentation by Type

All market revenues are presented in USD and volume in tons

Historical Year: 2021–2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027–2036

Key Questions this Study Will Answer

- What are the critical market metrics and forward-looking projections for the Global Pigments Market, including revenue size, volume sales, and average selling prices, with performance segmentation across Pigment Type (Organic, Inorganic, Specialty, High-Performance Pigments), Product Category (Titanium Dioxide, Iron Oxide, Carbon Black, Chromium Compounds, Complex Inorganic Color Pigments, Phthalocyanine, Azo Pigments, Quinacridone, Others), Form (Powder, Granules, Dispersions), Color Group (White, Black, Red, Yellow, Blue, Green, Brown, Others), Application (Paints & Coatings, Plastics, Printing Inks, Construction Materials, Paper, Textiles, Cosmetics, Others), and End-Use Industry (Automotive, Construction, Packaging, Consumer Goods, Industrial, Textile, Personal Care)?

- How do supply–demand fundamentals vary across key regions and major consuming industries, and what role do construction activity, automotive production, packaging demand, infrastructure investments, sustainability mandates, and industrial output trends play in shaping regional competitiveness, alongside local manufacturing capability in ore processing, calcination, surface treatment, micronization, dispersion technology, and downstream color formulation, as well as procurement structures across direct industrial buyers, formulators, distributors, and contract manufacturers?

- In what ways are raw material and energy price volatility and lead-time constraints (Titanium feedstock, ilmenite, rutile, petrochemical intermediates, iron ore derivatives, chromium compounds, specialty additives, solvents, and packaging materials) influencing production costs, converter pricing, supplier margins, delivery schedules, and profitability, especially for high-performance pigments, specialty color concentrates, and regulated heavy-metal-free formulations?

- Who are the leading global and regional pigment manufacturers, processors, and distributors, and how do they benchmark across color strength, opacity, tinting performance, dispersion quality, weather resistance, heat stability, chemical resistance, regulatory compliance, sustainability profile, and portfolio breadth across standalone pigment supply versus value-added solutions such as masterbatches, dispersions, customized shade development, technical service, and application support?

- What strategic insights emerge from primary discussions with pigment producers, coatings formulators, plastic compounders, ink manufacturers, distributors, and OEM-linked procurement teams regarding demand shifts toward high-performance and eco-friendly pigments, specification changes driven by low-VOC and non-toxic requirements, substitution trends between organic and inorganic pigments, regional sourcing strategies, inventory and lead-time management, and key purchase criteria such as cost competitiveness, shade consistency, regulatory compliance, supply assurance, application performance, and long-term formulation stability?

- Market Overview

- Product Overview

- Research Methodology

- Executive Summary

- Market Dynamics

- Market Dynamics (Drivers, Restraints, Opportunities, Challenges, Porter’s Five Forces Analysis, PESTLE Analysis)

- Market Trends & Developments

- Risk Assessment Framework

- Political / Geopolitical Risk

- Feedstock Supply Risk

- Environmental and Regulatory Risk

- Financial / Market Risk

- Regulatory Framework & Standards

- Global Regulatory Overview

- Key Regulations by Region

- EU: REACH, RoHS, F-Gas, EU Green Deal

- USA: EPA, FDA, TSCA

- China: GB Standards, MEE regulations

- India: BIS, CPCB norms

- Restricted & Banned Substances

- Heavy Metal Restrictions (Lead, Cadmium, Mercury, Chromium VI)

- Carcinogenic Azo Pigments Ban

- APEO-Free Requirements

- Food Contact & Cosmetic Grade Regulations

- FDA 21 CFR

- EU Cosmetics Regulation (EC) 1223/2009

- Sustainability & ESG Compliance

- Carbon footprint reporting

- Extended Producer Responsibility (EPR)

- ZDHC (Zero Discharge of Hazardous Chemicals)

- Regulatory Impact on Market — Opportunities & Threats

- Global Pigments Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume

- Market Size & Forecast by Type

- Inorganic Pigments

- Titanium Dioxide (TiO₂)

- Carbon Black

- Iron Oxide Red

- Iron Oxide Yellow

- Iron Oxide Black

- Iron Oxide Brown

- Chromium Oxide Green

- Ultramarine Blue

- Zinc Oxide

- Prussian Blue (Iron Blue)

- Bismuth Vanadate

- Mixed Metal Oxide (MMO)

- Zinc Sulfide

- Cadmium Sulfide / Selenide

- Cobalt Blue

- Organic Pigments

- Phthalocyanine Blue (CuPc)

- Phthalocyanine Green

- Azo Yellow (Monoazo)

- Diarylide Yellow

- Naphthol Red (Monoazo Red)

- Benzimidazolone Pigments

- Quinacridone Red / Magenta

- Diketopyrrolopyrrole (DPP)

- Dioxazine Violet

- Perylene Red / Black

- Isoindolinone Yellow

- Azo Condensation Pigments

- Quinophthalone Yellow

- Carbazole Violet

- Perinone Orange

- Specialty Pigments

- Mica-Based Pearlescent Pigments

- Aluminum Flake Pigments

- Carbon Black (Specialty Grade)

- IR Reflective Pigments (MMO-based)

- Fluorescent Pigments

- Thermochromic Pigments

- Photochromic Pigments

- Phosphorescent Pigments

- Bronze / Copper Flake Pigments

- Synthetic Mica (Fluorophlogopite)

- Conductive Pigments (ITO, ATO)

- Holographic / Diffractive Pigments

- Magnetic Pigments (Fe₃O₄)

- Encapsulated / Microencapsulated Pigments

- Bio-based / Natural Effect Pigments

- Inorganic Pigments

- Market Size & Forecast by End Use

- Paints & Coatings

- Architectural / Decorative Coatings

- Industrial Coatings

- Automotive OEM Coatings

- Automotive Refinish Coatings

- Marine Coatings

- Protective & Anti-Corrosion Coatings

- Powder Coatings

- Printing Inks

- Packaging Inks (Flexo, Gravure)

- Publication Inks (Offset)

- Digital / Inkjet Inks

- Security Printing Inks

- 3D Printing Inks

- Plastics

- Packaging Plastics

- Automotive Plastics

- Consumer Goods Plastics

- Construction Plastics (PVC Pipes, Profiles)

- Agricultural Films

- Textiles & Fibers

- Fiber-Reactive Pigment Dyeing

- Pigment Printing on Fabric

- Synthetic Fiber Coloration (Polyester, Nylon)

- Functional Textile Pigments (UV Protection, Antimicrobial)

- Cosmetics & Personal Care

- Lipsticks & Lip Gloss

- Eye Shadow & Mascara

- Foundation & Blush

- Nail Polish

- Sunscreen (UV-Blocking Pigments)

- Hair Colorants

- Construction Materials

- Concrete & Cement Coloring

- Roofing Tiles

- Bricks & Pavers

- Flooring

- Glass Coloring

- Stationery & Art Supplies

- Artist Colors

- Crayons & Markers

- Watercolors & Acrylics

- Electronics & Electrical

- Display Technologies (LCD, OLED)

- Solar Cells & Photovoltaics

- PCB & Circuit Board Coatings

- EMI Shielding Coatings

- Paints & Coatings

- Market Size & Forecast by Technology

- Synthetic Pigments

- Natural Pigments

- Bio-based Pigments

- Nano Pigments

- Surface-Treated Pigments

- Market Size & Forecast by Functional Property

- Decorative / Coloring Pigments

- Protective Pigments

- Anti-Corrosion

- UV Protection

- Functional / Performance Pigments

- IR Reflective

- Thermochromic

- Conductive / EMI Shielding

- Antimicrobial

- Photocatalytic (Tio₂)

- Optical Effect Pigments

- Pearlescent

- Metallic

- Interference Pigments

- Market Size & Forecast by Dispersibility / Carrier Medium

- Water-Based Pigments

- Solvent-Based Pigments

- Oil-Based Pigments

- UV-Curable Pigment Systems

- Powder Coatings Compatible

- Asia-Pacific Pigments Market Outlook

- Market Size & Forecast

- By Value

- By Volume

- By Type

- By End Use

- By Technology

- By Functional Property

- By Dispersibility / Carrier Medium

- Market Size & Forecast

- Europe Pigments Market Outlook

- Market Size & Forecast

- By Value

- By Volume

- By Type

- By End Use

- By Technology

- By Functional Property

- By Dispersibility / Carrier Medium

- Market Size & Forecast

- North America Pigments Market Outlook

- Market Size & Forecast

- By Value

- By Volume

- By Type

- By End Use

- By Technology

- By Functional Property

- By Dispersibility / Carrier Medium

- Market Size & Forecast

- Latin America Pigments Market Outlook

- Market Size & Forecast

- By Value

- By Volume

- By Type

- By End Use

- By Technology

- By Functional Property

- By Dispersibility / Carrier Medium

- Market Size & Forecast

- Middle East & Africa Pigments Market Outlook

- Market Size & Forecast

- By Value

- By Volume

- By Type

- By End Use

- By Technology

- By Functional Property

- By Dispersibility / Carrier Medium

- Market Size & Forecast

- Country Wise* Pigments Market Outlook

- Market Size & Forecast

- By Value

- By Volume

- By Type

- By End Use

- By Technology

- By Functional Property

- By Dispersibility / Carrier Medium

- Market Size & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: United States, China, Germany, United Kingdom, Japan, Australia, France, The Netherlands, Singapore, India, Canada, Brazil, South Korea, UAE, Sweden, Ireland, Malaysia, Indonesia, Italy, Poland, Mexico, South Africa, Saudi Arabia, Finland, Thailand, Chile, Norway, Kenya, Vietnam, Qatar

- Technology Analysis

- Conventional Vs Advanced Pigment Technologies

- Technology Readiness Levels (TRL) By Pigment Type

- Emerging Technologies

- Value Chain & Supply Chain Analysis

- Raw Material Suppliers

- Pigment Manufacturers

- Formulators & Dispersers

- Distributors & Traders

- End-Use Industries

- Ecosystem Map

- Supply Chain Analysis

- Key Raw Materials (TiO₂ Ore, Copper, Iron Ore, Petrochemicals)

- Supply Chain Risks & Disruptions

- China Dependency Analysis

- Trade Flow Analysis

- Major Exporting Countries

- Major Importing Countries

- Import-Export Dynamics

- Pricing Analysis

- Global Average Selling Price by Pigment Type

- Inorganic pigments pricing ($/kg)

- Organic pigments pricing ($/kg)

- Specialty pigments pricing ($/kg)

- Price Tier Analysis

- Commodity Pigments (Tio₂, Carbon Black, Iron Oxide)

- Mid-Range Pigments

- High-Performance Pigments (HPP)

- Specialty / Effect Pigments

- Global Average Selling Price by Pigment Type

- Sustainability & Energy Efficiency

- Go-to-Market & Distribution

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented Vs Consolidated)

- Top 5 Players Market Share

- HHI (Herfindahl–Hirschman Index) Concentration Analysis

- Competitive Intensity Map

- Player Classification

- Market Leaders

- Strong Challengers

- Specialist / Niche Players

- Emerging Players

- Regional Players

- Competitive Analysis Frameworks

- Market Share Analysis

- Company Profile

- Company Overview & HQ

- Products & Solutions Portfolio

- Revenue & Cooling Segment Revenue

- Geographic Presence

- Recent Developments (M&A, Launches, Partnerships)

- SWOT Analysis

- Strategic Focus Areas

- Competitive Positioning Map

- Market Structure & Concentration

- Strategic Recommendations

- For Pigment Manufacturers

- Product & Technology Strategy

- Portfolio Strategy

- Go-to-Market Strategy

- Sustainability Strategy

- M&A & Partnership Strategy

- For End-Use Industries

- Paints & Coatings manufacturers

- Automotive OEMs

- Cosmetics companies

- Packaging manufacturers

- For Investors & Private Equity

- High-priority investment themes

- M&A opportunity map

- Geographic investment priorities

- Risk considerations

- For Governments & Regulators

- Policy recommendations

- R&D support initiatives

- Supply chain resilience

- White Space & Opportunity Analysis

- Unmet market needs

- Emerging business models

- Technology white spaces

- Strategic Priority Matrix & Roadmap

- Near-term (2025–2028)

- Mid-term (2029–2032)

- Long-term (2023–2036)

- For Pigment Manufacturers