Market Definition

The India Bio-Based Surfactants Market encompasses the production, distribution, and end-use application of surface-active agents derived from renewable biological feedstocks including vegetable oils, sugars, fatty acids, amino acids, starch, and other naturally occurring organic materials, as distinct from conventional surfactants manufactured through petrochemical synthesis routes utilizing fossil fuel-derived intermediates. Bio-based surfactants function through the same fundamental amphiphilic molecular mechanism as their petrochemical counterparts, reducing surface and interfacial tension through the interaction of a hydrophilic head group and a lipophilic tail structure, enabling emulsification, foaming, wetting, dispersing, and solubilizing functions across a broad spectrum of industrial, agricultural, and consumer applications. The market encompasses both microbially produced biosurfactants, including rhamnolipids, sophorolipids, mannosylerythritol lipids, and surfactin produced through microbial fermentation of renewable substrates, and chemically synthesized bio-based surfactants derived from renewable feedstocks such as methyl ester sulfonates, alkyl polyglucosides, sucrose esters, sorbitan esters, and fatty acid derivatives processed from coconut oil, castor oil, palm kernel oil, and sugarcane-derived intermediates that are abundantly cultivated within India’s agricultural economy. The market spans key end-use sectors including personal care and cosmetics, household and institutional cleaning, agricultural crop protection formulation, textile processing, food-grade applications, oilfield chemistry, and pharmaceutical manufacturing. Key participants include oleochemical producers, bio-based surfactant manufacturers, fermentation biotechnology companies, consumer goods formulators, specialty chemical distributors, agricultural input companies, and regulatory bodies including the Bureau of Indian Standards and the Ministry of Chemicals and Fertilizers whose standards, green procurement guidelines, and hazardous substance restriction policies collectively define the operating and compliance environment for bio-based surfactant adoption across India’s industrial and consumer markets.

Market Insights

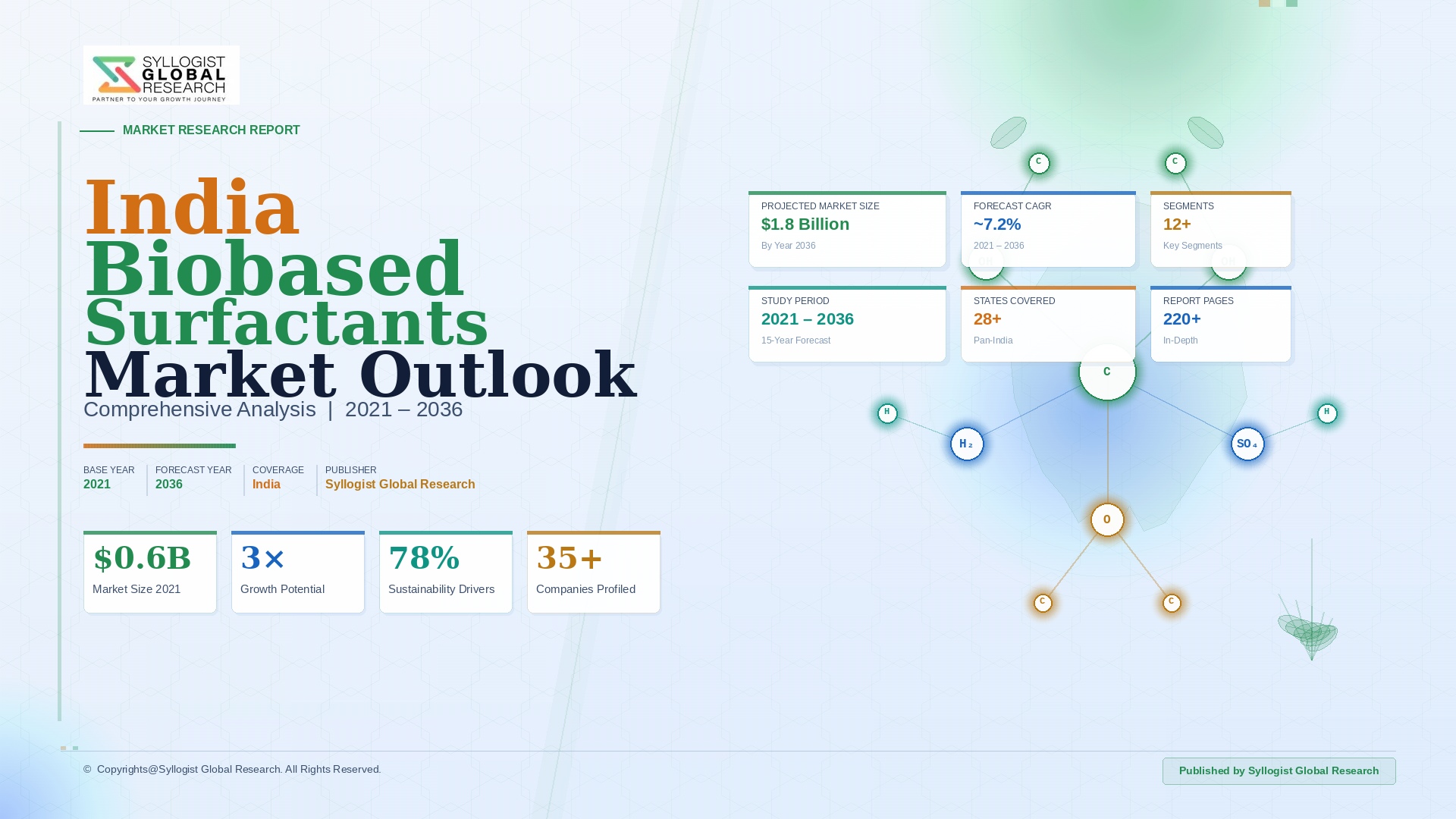

The India bio-based surfactants market was valued at approximately USD 312 million in 2025 and is projected to reach USD 678 million by 2034, advancing at a compound annual growth rate of 8.9% over the forecast period from 2027 to 2034, reflecting a structural shift in surfactant consumption patterns driven by rising consumer awareness of synthetic chemical hazards, accelerating adoption of green chemistry principles by domestic manufacturers, and deepening penetration of natural and organic personal care and home care formulations across urban and semi-urban Indian consumer markets. India’s substantial domestic availability of bio-based feedstocks including coconut oil, castor oil, sugarcane derivatives, and vegetable fatty alcohols provides domestic surfactant manufacturers with a cost-competitive raw material foundation for bio-based surfactant synthesis that partially offsets the historically higher production cost differential relative to conventional petrochemical surfactant grades, enabling a growing number of domestic manufacturers to position bio-based surfactant product lines competitively within the mid-market personal care and institutional cleaning segments. The market’s growth trajectory is further reinforced by India’s expanding organized retail footprint and the proliferation of direct-to-consumer natural beauty and wellness brands that collectively amplify consumer-facing demand for bio-based ingredient-formulated products, establishing a durable and self-reinforcing commercial ecosystem that continues to draw new entrants into bio-based surfactant manufacturing and formulation within the country.

The personal care and cosmetics segment constitutes the dominant application category within the India bio-based surfactants market, accounting for approximately 38% of total market revenue in 2025, propelled by the rapid expansion of India’s natural and organic beauty sector, increasing consumer demand for sulfate-free and mild-cleansing formulations in shampoos, facial cleansers, and body washes, and widespread adoption of alkyl polyglucosides and amino acid-derived surfactants including sodium lauroyl glutamate and sodium cocoyl glycinate as skin-compatible alternatives to conventional anionic surfactants. The household and institutional cleaning segment represents the second-largest application category, with bio-based surfactant adoption in dishwashing liquids, surface cleaners, and laundry formulations gaining measurable momentum among organized branded consumer goods companies and institutional procurement decision-makers in the hospitality, healthcare, and food service sectors seeking to fulfill sustainability procurement commitments and green building certification requirements. The agricultural applications segment, encompassing bio-based adjuvants, emulsifiers, and wetting agents for pesticide and herbicide formulations, is emerging as a rapidly growing demand category driven by increasing regulatory scrutiny of synthetic surfactant adjuvants and the expanding registered crop protection product market in India, creating substitution opportunities for bio-derived alternatives with demonstrably superior ecotoxicological profiles that satisfy both regulatory and commercial requirements.

India’s indigenous oleochemical manufacturing base, concentrated in Kerala, Tamil Nadu, Andhra Pradesh, and Gujarat, provides the bio-based surfactants market with a vertically integrated supply infrastructure extending from agricultural feedstock cultivation through fatty acid fractionation, glycerol recovery, and downstream surfactant synthesis, with coconut oil-derived and castor oil-derived surfactant chemistries representing India-specific bio-based product categories in which domestic manufacturers possess genuine feedstock and process economics advantages relative to import-dependent markets. India’s status as the world’s leading producer and exporter of castor oil, accounting for approximately 85% of global castor oil exports, positions domestic producers favorably to develop castor-derived bio-based surfactant specialties for both domestic consumption and export markets, particularly in the personal care and industrial lubricant formulation segments where castor oil-derived surfactants offer distinctive performance attributes including high temperature stability and compatibility with sensitive formulation systems. The technical foundation for expanded bio-based surfactant production is further supported by India’s growing fermentation biotechnology research ecosystem within institutions including the Council of Scientific and Industrial Research laboratories and the Department of Biotechnology-funded centers of excellence, which are progressively translating biosurfactant fermentation research into commercially scalable production process knowledge accessible to domestic manufacturers.

The regulatory environment governing India’s bio-based surfactants market is evolving toward greater alignment with international green chemistry and sustainable chemistry standards, with the Ministry of Environment, Forest and Climate Change progressively expanding the list of regulated substances in industrial effluent discharge standards to include anionic surfactant load limits that create a compliance-driven substitution incentive for biodegradable bio-based surfactant alternatives across textile processing, pulp and paper, and industrial cleaning applications. Several large domestic chemical conglomerates and multinational specialty chemical companies have established dedicated bio-based surfactant product lines targeting the Indian market, with competitive differentiation increasingly based on bio-based content certification, third-party biodegradability performance data, low aquatic toxicity profiles, and formulation technical support services that align with the procurement criteria of multinational consumer goods companies operating India manufacturing facilities under global corporate sustainability mandates. The Indian government’s Production Linked Incentive scheme for specialty chemicals and the National Chemical Policy’s strategic emphasis on developing India’s green chemistry manufacturing capabilities are collectively improving the investment climate for bio-based surfactant capacity expansion, attracting both domestic capital and foreign direct investment into the sector and supporting the infrastructure development needed to sustain the market’s projected growth trajectory through 2034.

Key Drivers

Escalating Consumer Preference for Natural and Sustainable Personal Care and Cleaning Formulations Driving Accelerated Bio-Based Surfactant Adoption Across India

India’s consumer goods market is experiencing a pronounced and structurally durable shift in purchasing behavior among urban and aspirational middle-class consumers toward personal care, skincare, and household cleaning products formulated with naturally derived, skin-compatible, and environmentally responsible ingredients, creating an expanding demand base for bio-based surfactants as primary active components in sulfate-free, biodegradable, and mild-cleansing formulations across shampoos, body washes, facial cleansers, and liquid detergents. The organized natural and organic personal care segment in India was valued at approximately USD 1.4 billion in 2025 and is growing at over 12% annually, substantially outpacing growth in the broader personal care market, with alkyl polyglucosides, amino acid-derived surfactants, and sucrose ester-based systems emerging as preferred bio-based surfactant chemistries in premium and mid-range formulations targeting health-conscious consumers in metropolitan and Tier-1 city markets. This consumer-driven substitution trend is reinforced by the accelerating influence of social media platforms, dermatologist-led digital content, and ingredient transparency advocacy among Indian consumers, with natural origin claims and clean-label formulation credentials becoming primary brand differentiation parameters for new product launches in the personal care category, compelling large domestic FMCG companies and emerging direct-to-consumer natural beauty brands to reformulate existing product lines and develop new bio-based surfactant-based offerings that capture growing market share in the premiumizing Indian personal care sector.

Abundant Domestic Renewable Feedstock Availability and India’s Established Oleochemical Manufacturing Infrastructure Supporting Cost-Competitive Bio-Based Surfactant Production

India’s position as the world’s leading producer and exporter of castor oil, a significant producer of coconut oil, and a major cultivator of sugarcane-derived intermediates and vegetable fatty alcohols provides the country’s bio-based surfactant manufacturing sector with a structurally advantaged renewable raw material supply chain whose domestic origin and relative price predictability confer a meaningful production cost advantage over bio-based surfactant manufacturers in regions dependent on imported renewable feedstocks. The country’s oleochemical industry, anchored by manufacturing clusters in Kerala, Tamil Nadu, Gujarat, and Andhra Pradesh, has developed substantial accumulated expertise in fatty acid fractionation, methyl ester production, glycerol refining, and sulfonation chemistry processes that provide the technical foundation for upstream bio-based surfactant synthesis, enabling domestic manufacturers to produce methyl ester sulfonates, fatty acid derivatives, and coconut oil-based amphoteric surfactants at production economics that are increasingly competitive with petrochemical surfactant grades as crude oil price volatility periodically narrows the feedstock cost differential between bio-based and petroleum-derived synthesis routes. Government support programs including the Production Linked Incentive scheme for specialty chemicals, state-level oleochemical industry incentive frameworks in Kerala and Tamil Nadu, and the National Biopharma Mission’s fermentation technology infrastructure development initiatives are collectively strengthening the capital investment environment for bio-based surfactant production capacity expansion within India, reducing the infrastructure cost barriers that have historically constrained domestic capacity scaling relative to demand growth.

Strengthening Environmental Regulations and Corporate Sustainability Mandates Accelerating Bio-Based Surfactant Adoption Across Industrial and Institutional Application Segments

The progressive tightening of India’s environmental compliance framework governing industrial effluent discharge, biodegradability requirements for cleaning products in food processing and healthcare facilities, and the expanding scope of green procurement policies adopted by central and state government agencies is creating a structural regulatory pull for bio-based surfactants across industrial cleaning, agricultural formulation, textile processing, and institutional application segments where conventional petrochemical surfactants face increasing scrutiny regarding aquatic toxicity, environmental persistence, and bioaccumulation risk. The Ministry of Environment, Forest and Climate Change has progressively expanded the regulated substances list in industrial wastewater discharge standards to include anionic surfactant load limits that are directly increasing compliance costs for industrial users of conventional synthetic surfactants, creating a formulation substitution incentive for biodegradable bio-based alternatives with demonstrably superior environmental fate profiles and regulatory compliance credentials. Concurrently, multinational consumer goods companies operating India manufacturing facilities under global corporate sustainability mandates have incorporated defined minimum thresholds for bio-based raw material content within their India procurement specifications, directly translating corporate sustainability commitments into supply chain requirements that favor certified bio-based surfactant grades, creating a pull-through demand dynamic that supports domestic bio-based surfactant market development and incentivizes capacity investment among manufacturers seeking qualification within multinational consumer goods supply chains.

Key Challenges

Higher Production Cost Structure of Bio-Based Surfactants Relative to Petrochemical Alternatives Constraining Market Penetration in Price-Sensitive Volume Segments

The most commercially significant barrier to accelerated bio-based surfactant adoption across the India market is the persistent production cost premium that bio-based surfactant grades carry relative to petrochemical-derived equivalents across the majority of surfactant chemistries and application categories, with bio-based surfactant prices typically commanding a 25% to 60% premium over equivalent petrochemical surfactant grades depending on chemistry type, performance specification, and prevailing crude oil and vegetable oil feedstock price differentials, a cost disadvantage that substantially limits bio-based surfactant penetration in the large-volume, price-competitive commodity segments of the Indian detergent, textile processing, and industrial cleaning markets where total formulation cost optimization remains the dominant purchasing criterion for the majority of buyers. The production economics of bio-based surfactants are constrained by the comparatively smaller scale of most domestic bio-based surfactant manufacturing operations relative to world-scale petrochemical surfactant plants of established global producers, limiting the economies of scale available to domestic bio-based manufacturers, while fermentation-based biosurfactant production processes require sterile fermentation infrastructure, downstream purification steps, and precise process control systems that add significant capital and operating cost per unit of surfactant produced. This cost disadvantage structurally restricts bio-based surfactant market penetration predominantly to premium-positioned consumer product applications where higher raw material cost can be absorbed within product pricing, leaving the much larger commodity surfactant volume segments of the Indian market substantially underpenetrated by bio-based alternatives.

Limited Domestic Technical Expertise and Specialized Manufacturing Infrastructure for Advanced Bio-Based Surfactant Chemistries and Fermentation-Based Biosurfactant Production

India’s bio-based surfactant manufacturing base, while growing steadily, remains concentrated in conventional oleochemical-derived surfactant chemistries including fatty acid derivatives, methyl ester sulfonates, and basic alkyl polyglucosides, with limited domestic commercial production capability for technically advanced bio-based surfactant categories including sophorolipids, rhamnolipids, mannosylerythritol lipids, and other glycolipid biosurfactants that command premium pricing in pharmaceutical, cosmetic, and specialty industrial application segments but require sophisticated fermentation biotechnology expertise and bioprocess engineering capabilities currently concentrated primarily in institutional research facilities rather than at commercial production scale within India. The development of domestic commercial-scale fermentation biosurfactant production capability requires significant capital investment in sterile fermentation vessels, downstream recovery and purification equipment, and quality control infrastructure that represents a substantial financial commitment for emerging bio-based surfactant manufacturers operating with limited access to risk capital within India’s specialty chemicals sector. Furthermore, the formulation expertise required to successfully incorporate novel bio-based surfactant chemistries into complex multi-functional personal care, cleaning, and agricultural product formulations while maintaining performance parity with established petrochemical surfactant blends is concentrated among a relatively small number of technically sophisticated formulators in India, creating a knowledge gap that slows bio-based surfactant adoption in technically demanding applications and constrains the ability of domestic surfactant producers to offer fully developed, application-ready formulation solutions to their industrial and consumer goods customers.

Agricultural Feedstock Price Volatility and Supply Chain Vulnerabilities Creating Input Cost Uncertainty for Bio-Based Surfactant Manufacturers

Bio-based surfactant manufacturers in India are exposed to meaningful input cost volatility arising from the agricultural nature of their primary raw material supply chains, with vegetable oil prices, particularly coconut oil and palm kernel oil that serve as primary feedstocks for fatty alcohol and alkyl polyglucoside surfactant production, subject to significant interannual price fluctuations driven by monsoon variability affecting domestic coconut production yields, export demand from international oleochemical markets, and commodity trading dynamics that are fundamentally distinct from and often less predictable than the crude oil-linked price movements governing petrochemical surfactant raw material costs. India’s coconut oil production, heavily concentrated in Kerala and Tamil Nadu, has experienced supply disruptions in multiple years due to cyclonic weather events, drought conditions, and shifting agricultural land use patterns, creating episodes of acute feedstock price escalation that erode production margins of bio-based surfactant manufacturers and temporarily widen the cost competitiveness gap relative to petrochemical surfactant alternatives. The absence of mature financial hedging instruments for domestic vegetable oil prices in India, combined with the relatively short-term fixed-price supply agreements available from agricultural commodity intermediaries, limits the ability of bio-based surfactant producers to provide stable forward pricing commitments to formulator and consumer goods manufacturer customers, creating procurement uncertainty that leads some buyers to maintain blended supply portfolios retaining conventional petrochemical surfactant sourcing as a cost management buffer against bio-based feedstock price spikes.

Market Segmentation

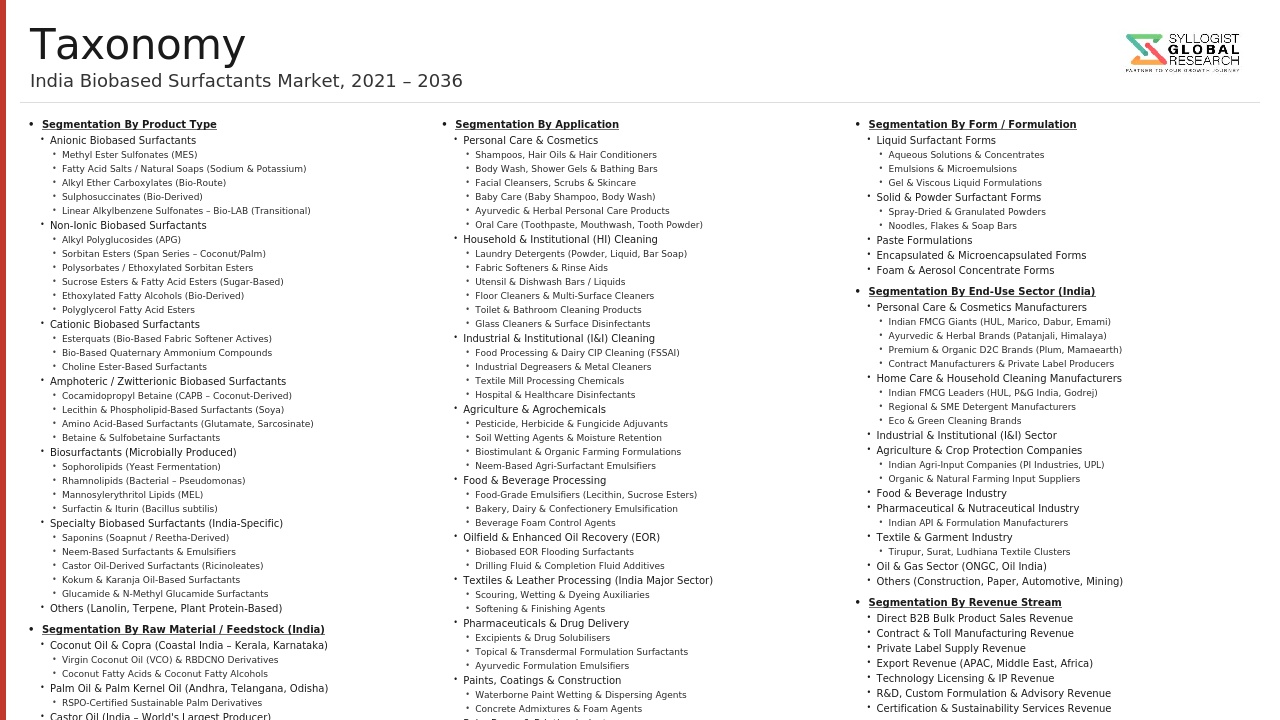

- Segmentation By Product Type

- Alkyl Polyglucosides (APG)

- Methyl Ester Sulfonates (MES)

- Sucrose Esters and Sucrose Fatty Acid Esters

- Amino Acid-Based Surfactants (Sodium Lauroyl Glutamate, Sodium Cocoyl Glycinate, and Others)

- Sorbitan Esters and Ethoxylated Sorbitan Esters

- Sophorolipids

- Rhamnolipids

- Other Glycolipid and Lipopeptide Biosurfactants

- Others

- Segmentation By Feedstock

- Coconut Oil-Derived

- Castor Oil-Derived

- Palm Kernel Oil-Derived

- Sugarcane and Glucose-Derived

- Soybean Oil-Derived

- Others

- Segmentation By Application

- Personal Care and Cosmetics

- Household and Institutional Cleaning

- Agricultural Formulations (Adjuvants, Emulsifiers, and Wetting Agents)

- Textile Processing and Finishing

- Food Processing and Food-Grade Applications

- Oilfield and Enhanced Oil Recovery

- Pharmaceutical and Healthcare

- Industrial Cleaning and Degreasing

- Others

- Segmentation By End-Use Industry

- Personal Care and Beauty Industry

- Fast-Moving Consumer Goods (FMCG) Companies

- Agricultural Input and Crop Protection Companies

- Textile Mills and Processing Facilities

- Food and Beverage Manufacturers

- Oil and Gas Sector

- Healthcare and Pharmaceutical Companies

- Industrial and Institutional Cleaning Service Providers

- Others

- Segmentation By Distribution Channel

- Direct Sales (Business-to-Business)

- Specialty Chemical Distributors and Wholesalers

- Online Platforms and E-Commerce

- Others

- Segmentation By Region

- North India

- South India

- West India

- East India

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total market valuation of the India Bio-Based Surfactants Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by product type including alkyl polyglucosides, methyl ester sulfonates, amino acid-based surfactants, sucrose esters, and glycolipid biosurfactants, and by application including personal care, household cleaning, agriculture, textile processing, and industrial uses, to enable bio-based surfactant manufacturers, oleochemical producers, formulators, specialty chemical distributors, and investors to identify which product chemistries and application segments will generate the highest absolute revenue and the most durable growth trajectory across the forecast period?

- How is the regulatory evolution in India, encompassing industrial effluent discharge standards for anionic surfactant loads, biodegradability requirements for cleaning products in food and healthcare facilities, and the Ministry of Environment, Forest and Climate Change’s progressively expanding hazardous substance restriction framework, expected to drive mandatory and voluntary substitution of conventional petrochemical surfactants by bio-based alternatives across textile processing, agricultural formulation, and institutional cleaning application segments, and what are the estimated compliance-driven market development volumes and revenue opportunities arising from regulatory-mandated bio-based surfactant adoption through 2034?

- What is the current production capacity, feedstock sourcing strategy, key product portfolio, and domestic and export market positioning of leading bio-based surfactant manufacturers operating in India, and how are these players investing in new product development, fermentation biosurfactant scale-up, bio-based content certification, and formulation technical services to compete with both conventional petrochemical surfactant suppliers and multinational bio-based surfactant importers across the personal care, industrial cleaning, and agricultural application segments of the India market?

- How are India’s abundant domestic renewable feedstock resources, specifically castor oil, coconut oil, and sugarcane-derived intermediates, shaping the bio-based surfactant chemistry mix produced and consumed within the country, and which feedstock-derived surfactant categories offer the most commercially viable cost and performance proposition for accelerating penetration into mid-market and volume-sensitive application segments where bio-based surfactants currently compete against substantially lower-cost petrochemical alternatives, and what is the feedstock cost and availability outlook for each primary renewable raw material through the forecast period?

- What are the regional demand distribution patterns within India for bio-based surfactants across the North, South, West, and East geographic zones, considering the concentration of personal care manufacturing in Maharashtra and Himachal Pradesh, oleochemical processing capacity in Kerala and Tamil Nadu, textile processing in Gujarat and Tamil Nadu, and agricultural consumption across major crop-cultivating states, and how are these regional industrial and agricultural concentrations expected to influence geographic demand growth rates, application mix, and competitive supply chain dynamics within the India bio-based surfactants market through 2034?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Raw Material & Supply Chain Risk

- Regulatory & Compliance Risk

- Market & Demand Risk

- Technology & Product Risk

- Environmental & Circular Economy Risk

- Regulatory Framework & Standards

- National Biodegradability & Effluent Standards

- Cosmetics & Personal Care Regulations

- Food, Nutraceutical & Pharmaceutical Standards

- Agricultural Input & Biopesticide Regulations

- Trade, Import & Export Standards

- India Bio-Based Surfactants Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Kilotonnes)

- Market Size & Forecast by Product Type

- Sugar-Based Surfactants

- Alkyl Polyglucosides (APG): C8-C10, C12-C14 & C8-C16 Grades

- Sucrose Esters & Sucrose Fatty Acid Esters

- Methyl Glucoside Esters (MGE)

- Sorbitan Esters (Span Series)

- Polysorbates

- Fatty Acid-Based Surfactants

- Sodium / Potassium Cocoyl Sulphate & Lauryl Sulphate (Bio-Based Grade)

- Sodium Lauroyl / Cocoyl Methyl Isethionate (SLMI / SLCI)

- Cocamidopropyl Betaine (CAPB: Bio-Based & Coconut-Derived)

- Sodium Cocoamphoacetate & Disodium Cocoamphodiacetate

- Amine Oxides (Lauramine Oxide: Coconut-Derived)

- Amino Acid-Based Surfactants

- Sodium Lauroyl Glutamate & Sodium Cocoyl Glutamate

- Potassium Cocoyl Glycinate & Sodium Lauroyl Glycinate

- Sodium Cocoyl Alaninate & N-Acyl Sarcosinates

- Acyl Taurate Surfactants (Sodium Lauroyl Methyl Taurate)

- Glycolipid Biosurfactants (Fermentation-Derived)

- Sophorolipids (Candida bombicola Fermentation: Domestic & Imported)

- Rhamnolipids (Pseudomonas / Non-Pathogenic Host Fermentation)

- Mannosylerythritol Lipids (MEL): Imported & Pilot-Scale Domestic Production

- Lipopeptide Biosurfactants

- Surfactin from Bacillus subtilis: CSIR/DBT Research Commercialisation

- Iturin & Fengycin Complexes for Agricultural Biocontrol Applications

- Lecithin & Phospholipid Surfactants

- Soy Lecithin (Domestic: MP & Maharashtra Origin): Standard & De-Oiled Grades

- Sunflower Lecithin (Non-GMO Premium: Imported & Domestic)

- Saponin-Based Surfactants

- Reetha (Sapindus mukorossi) Saponin Extract: Traditional Indian Bio-Surfactant

- Shikakai (Acacia concinna) Pod Extract: Ayurvedic Hair Care Surfactant

- Quillaja (Soapbark) Saponin Extract: Imported for Food & Cosmetic Applications

- Protein-Based & Polymeric Bio-Surfactants

- Hydrolysed Wheat Protein & Silk Amino Acid Surfactants for Premium Hair Care

- Oat Beta-Glucan & Rice Protein-Based Amphiphilic Extracts for Sensitive Skin Care

- Market Size & Forecast by Raw Material / Feedstock

- Coconut Oil

- Palm Kernel Oil

- Corn & Glucose / Dextrose

- Sugarcane-Derived Feedstocks

- Castor Oil

- Soybean Oil & Lecithin

- Rapeseed & Mustard Oil

- Waste & Second-Generation Feedstocks

- Market Size & Forecast by Application

- Home Care & Laundry

- Liquid Laundry Detergent (Premium & Mid-Range Bio-Based Formulations)

- Powder Laundry Detergent (Partial Bio-Based Surfactant Integration)

- Fabric Conditioner & Softener

- Dishwash Liquid & Bar (Coconut-Derived Surfactant Formulations)

- Hard Surface Cleaner, Bathroom & Toilet Cleaner (Eco-Certified Brands)

- Personal Care & Cosmetics

- Shampoo & Hair Conditioner (Sulphate-Free, Ayurvedic & Premium Natural)

- Body Wash, Shower Gel & Liquid Soap (Baby, Sensitive Skin & Premium Adult Segments)

- Facial Cleanser, Face Wash & Micellar Water

- Skin Moisturiser, Sunscreen & Colour Cosmetics Emulsifiers

- Toothpaste & Oral Care (SLS-Free Bio-Based Surfactant Formulations)

- Industrial & Institutional (I&I) Cleaning

- Food Processing, Dairy & HORECA (Hotels, Restaurants, Catering) CIP Cleaning

- Hospital, Healthcare & Pharmaceutical Facility Surface Cleaning

- Corporate Campus, IT Park & Green Building Cleaning

- Industrial Degreaser & Workshop Cleaning

- Agriculture & Crop Protection

- Biosurfactant Pesticide Adjuvant, Spreader-Sticker & Wetting Agent

- Biostimulant Soil Wetting Agent & Root Zone Conditioner

- Biopesticide & Biofungicide Formulation Active (Surfactin, Rhamnolipid)

- Oilfield & Mining

- Enhanced Oil Recovery (EOR) Bio-Surfactant Application (ONGC, Oil India)

- Froth Flotation Bio-Based Collector & Frother in Indian Mining Operations

- Food & Beverage Processing

- Food Emulsifiers (Lecithin, Sucrose Esters) for Bakery, Dairy & Confectionery

- Beverage Clouding Agents, Foam Stabilisers & Quillaja Extract Applications

- Pharmaceuticals & Healthcare

- Drug Solubilisation & Bioavailability Enhancement (Polysorbates, Lecithin)

- Topical Drug, Wound Care & Ophthalmic Formulation Emulsifiers

- Textile, Leather & Paper Processing

- Textile Scouring, Wetting & Desizing Agents (NPE-Free Alternatives)

- Leather Degreasing & Fatliquoring (Castor-Derived Surfactant Applications)

- Paper Sizing, Coating & Deinking Agents for Indian Paper Industry

- Market Size & Forecast by Function

- Emulsifiers & Solubilisers

- Detergents & Cleansers

- Foaming & Lathering Agents

- Wetting & Spreading Agents

- Dispersants & Suspending Agents

- Conditioning & Softening Agents

- Antimicrobial & Biocidal Agents

- Corrosion Inhibitors & Lubricity Agents

- Market Size & Forecast by Charge Type

- Anionic Bio-Based Surfactants

- Cationic Bio-Based Surfactants

- Non-Ionic Bio-Based Surfactants

- Amphoteric / Zwitterionic Bio-Based Surfactants

- Market Size & Forecast by Source

- Domestically Produced Bio-Based Surfactants

- Imported Bio-Based Surfactants

- Microbially Fermented (Biosurfactant): Domestic Research & Pilot-Scale

- Traditional Indian Botanical Surfactant Extracts

- Market Size & Forecast by End-User

- Large-Scale FMCG Manufacturers (HUL, P&G India, ITC, Dabur, Marico, Godrej Consumer)

- Mid-Size & Regional Personal Care & Home Care Brands

- D2C & Natural Beauty Startups

- Industrial & Institutional Cleaning Formulators

- Pharmaceutical & Nutraceutical Manufacturers

- Agricultural Input Companies & Biocontrol Formulators

- Textile, Leather & Paper Processing Industries

- Market Size & Forecast by Sales Channel

- Direct Supply (B2B: Bulk Formulator & Industrial Account)

- Specialty Chemical Distributor & Trader Network (Pan-India)

- Online B2B Platform (IndiaMART, TradeIndia, Chemical B2B Portals)

- Toll Manufacturing & Custom Processing

- North India Bio-Based Surfactants Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotonnes)

- By Product Type

- By Raw Material / Feedstock

- By Application

- By Function

- By Charge Type

- By Source

- By End-User

- By Sales Channel

- Market Size & Forecast

- West India Bio-Based Surfactants Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotonnes)

- By Product Type

- By Raw Material / Feedstock

- By Application

- By Function

- By Charge Type

- By Source

- By End-User

- By Sales Channel

- Market Size & Forecast

- South India Bio-Based Surfactants Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotonnes)

- By Product Type

- By Raw Material / Feedstock

- By Application

- By Function

- By Charge Type

- By Source

- By End-User

- By Sales Channel

- Market Size & Forecast

- East India Bio-Based Surfactants Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotonnes)

- By Product Type

- By Raw Material / Feedstock

- By Application

- By Function

- By Charge Type

- By Source

- By End-User

- By Sales Channel

- Market Size & Forecast

- Central India Bio-Based Surfactants Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotonnes)

- By Product Type

- By Raw Material / Feedstock

- By Application

- By Function

- By Charge Type

- By Source

- By End-User

- By Sales Channel

- Market Size & Forecast

- State-Wise* India Bio-Based Surfactants Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotonnes)

- By Product Type

- By Raw Material / Feedstock

- By Application

- By Function

- By Charge Type

- By Source

- By End-User

- By Sales Channel

- Market Size & Forecast

*Key States Analyzed in the Syllogist India Research Portfolio: Maharashtra, Gujarat, Uttar Pradesh, Tamil Nadu, Karnataka, Telangana, Andhra Pradesh, Kerala, Delhi NCR, West Bengal, Rajasthan, Madhya Pradesh, Punjab, Haryana, Odisha

- Technology Landscape & Innovation Analysis

- Oleochemical Bio-Based Surfactant Technology in India

- Fermentation & Biosurfactant Technology: India Research & Scale-Up

- Traditional Indian Botanical Surfactant Standardisation Technology

- Formulation Technology for Indian Market Conditions

- Analytical & Quality Technology for Indian Bio-Based Surfactant Manufacturing

- Patent & IP Landscape: India & Indian Players

- Value Chain & Supply Chain Analysis

- Raw Material Supply Chain: India-Specific

- Domestic Bio-Based Surfactant Manufacturer

- Imported Bio-Based Surfactant Suppliers (Key MNCs Operating in India)

- Chemical Distribution & Trading Network

- Formulator & Brand Owner Ecosystem

- End-of-Life & Circular Economy

- Pricing Analysis

- APG & Sugar-Based Surfactant Pricing in India

- Amino Acid-Based Surfactant Pricing in India

- Biosurfactant Pricing in India

- Traditional Indian Botanical Surfactant Pricing

- Lecithin & Oleochemical Emulsifier Pricing in India

- Total System & Formulation Cost Analysis for India Market

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Bio-Based Surfactants in Indian Context

- Biodegradability & Aquatic Safety in Indian Context

- Renewable Carbon & Climate Contribution: India

- Social & Ethical Sustainability: India

- Regulatory-Driven Sustainability in India

- Competitive Landscape

- Market Structure & Concentration

- Player Classification

- Competitive Analysis Frameworks

- Market Share Analysis by Product Type, Application & Region Within India

- Company Profile

- Company Overview & India Headquarters / Manufacturing Location

- India Bio-Based Surfactant Products & Technology Portfolio

- Key Indian Customer Relationships & Application Focus

- India Manufacturing Footprint, Plant Location & Production Capacity

- India Revenue (Bio-Based Surfactant Segment) & Growth Trajectory

- Technology Differentiators & India-Relevant IP Portfolio

- Key Strategic Partnerships, JVs & M&A Activity in India

- Recent Developments in India (Capacity Expansion, New Product Launches, Certifications)

- SWOT Analysis: India Context

- India Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Leadership vs. India Market Penetration)

- Key Company Profiles

- Strategic Opportunity Analysis

- Strategic Output

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic & Market Penetration Strategy within India

- Customer & Brand Owner Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy: India

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-Term (2025-2028)

- Mid-Term (2029-2032)

- Long-Term (2033-2037)