Market Definition

The Global Green Steel Market encompasses the production, processing, distribution, and commercial application of steel manufactured through production pathways that achieve substantial reductions in carbon dioxide and greenhouse gas emissions relative to the conventional blast furnace and basic oxygen furnace steelmaking route, which is responsible for approximately 7% to 9% of global anthropogenic carbon dioxide emissions and relies on metallurgical coking coal as both a reductant and energy source. Green steel is defined across the industry by a spectrum of low-emission production technologies and decarbonization pathways, with the most widely recognized approach being hydrogen-based direct reduced iron production using green hydrogen generated from electrolysis powered by renewable electricity, coupled with electric arc furnace melting and refining of the resulting direct reduced iron into finished steel products. The market additionally encompasses steel produced through other low-emission pathways including electric arc furnace steelmaking using high proportions of recycled scrap charged with renewable electricity, direct reduced iron production using natural gas with carbon capture, utilization and storage, electrochemical ironmaking technologies utilizing molten oxide electrolysis and other electrolytic reduction processes, and biomass or biochar-based reduction technologies that substitute renewable carbon sources for fossil coking coal in adapted blast furnace configurations. Commercial definitions of green steel vary across voluntary certification schemes, with emissions intensity thresholds applied by certification frameworks including the ResponsibleSteel standard, the SteelZero initiative, and the Science Based Targets initiative’s steel sector pathway differentiating low-emission from conventional steel production. Key participants include integrated steel producers, electric arc furnace steelmakers, green hydrogen producers and suppliers, renewable energy developers, direct reduced iron technology licensors, automotive and construction steel consumers, green steel certification bodies, and financial institutions providing transition finance and green bond capital for steelmaking decarbonization investments.

Market Insights

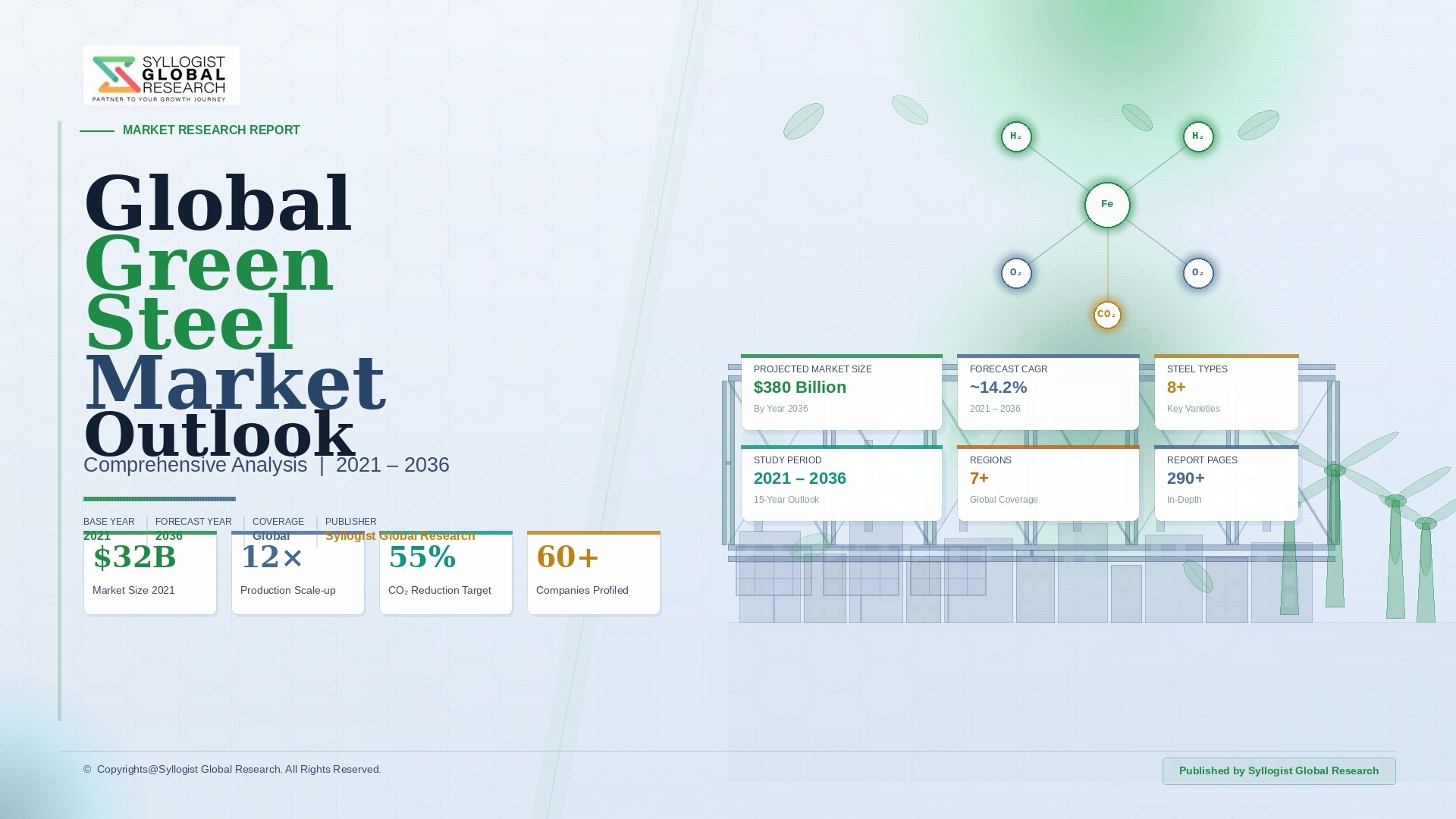

The global green steel market was valued at approximately USD 11.2 billion in 2025 and is projected to reach USD 98.6 billion by 2034, advancing at a compound annual growth rate of 27.4% over the forecast period from 2027 to 2034, representing one of the most rapid value creation trajectories within the global industrial materials sector as coordinated pressure from carbon pricing mechanisms, corporate net-zero procurement commitments, financial market sustainability requirements, and government industrial decarbonization policy frameworks converges to transform green steel from a premium niche product into a structurally necessary component of global steel supply chains. Global crude steel production reached approximately 1.89 billion metric tons in 2025, of which green steel produced through hydrogen-based, scrap-electric, or carbon-capture-enabled pathways accounted for approximately 3.8% by volume, a share that is projected to expand to approximately 24.7% by 2034 as the capital investment programs announced by leading steelmakers across Europe, North America, and Asia Pacific progressively commission hydrogen-based direct reduced iron and electric arc furnace capacity at commercial scale. The production cost premium of green hydrogen-based steel relative to conventional blast furnace steel, currently estimated at approximately USD 180 to USD 240 per metric ton depending on renewable electricity cost, electrolyzer efficiency, and regional carbon pricing levels, represents the central commercial challenge governing the pace of green steel market expansion, with cost parity projections dependent on continued reductions in electrolyzer capital cost, scaling of renewable electricity generation, and the progressive strengthening of carbon pricing mechanisms that increase the effective cost of conventional steelmaking.

Europe constitutes the most commercially advanced regional market for green steel, accounting for approximately 44% of global green steel revenue in 2025, driven by the European Union Emissions Trading System carbon price which reached approximately USD 68 per metric ton of carbon dioxide in 2025 and is projected to exceed USD 130 per metric ton by 2030 under the EU Carbon Border Adjustment Mechanism implementation trajectory, directly improving the economic competitiveness of green steel relative to conventional production and creating a carbon cost environment that is accelerating steelmaker investment decisions on hydrogen-based production infrastructure. SSAB in Sweden has produced fossil-free steel through its HYBRIT joint venture process using green hydrogen-based direct reduced iron and electric arc furnace steelmaking since pilot scale operations commenced in 2021, delivering commercial volumes of fossil-free steel to automotive customers including Volvo Group and Epiroc under long-term supply agreements that represent the first commercially contracted green steel transactions globally. Thyssenkrupp Steel in Germany has committed EUR 2.0 billion to converting its first blast furnace to direct reduction technology with hydrogen capability, with the first direct reduced iron unit expected to commence production in 2026 using initially natural gas transitioning to green hydrogen as renewable supply scales, illustrating the phased transition pathway being pursued by integrated steelmakers balancing capital investment scale with hydrogen availability timelines. ArcelorMittal, the world’s second-largest steelmaker, has announced green steel production programs across multiple European sites under its XCarb brand, committing to 30% carbon intensity reduction by 2030 and net-zero steelmaking by 2050 through a combination of hydrogen-based direct reduction, electric arc furnace expansion, and carbon capture deployment.

The automotive sector represents the most commercially active and strategically significant demand category for green steel, with major global vehicle manufacturers including Volkswagen Group, Mercedes-Benz, BMW, Volvo Cars, Ford, and General Motors having issued formal procurement commitments or signed offtake agreements for green steel supply as part of Scope 3 emissions reduction strategies that require decarbonization of purchased materials as well as direct manufacturing operations. Automotive original equipment manufacturers are willing to pay a meaningful green premium for certified low-carbon steel, with buyer surveys and concluded supply agreements indicating premium acceptance levels of approximately USD 50 to USD 150 per metric ton for automotive-grade certified green steel relative to equivalent conventional steel grades, providing sufficient commercial signal for steelmakers to advance green steel investment programs targeting automotive customers in the near to medium term before broader market carbon pricing mechanisms fully close the production cost gap. The construction sector, which consumes approximately 52% of global steel production by volume, represents the largest potential long-term demand category for green steel, with green building certification standards including LEED, BREEAM, and the WELL Building Standard incorporating embodied carbon assessment requirements that are progressively incentivizing construction material specifiers to select low-emission steel products, while public procurement frameworks in the European Union, United Kingdom, Sweden, and the Netherlands have introduced mandatory or voluntary low-carbon steel procurement requirements for government infrastructure projects that are creating a publicly funded near-term demand base for green steel in structural and reinforcing bar applications.

The hydrogen supply chain infrastructure required to enable large-scale hydrogen-based green steel production represents the most capital-intensive and logistically complex enabler of the global green steel market, with a single large integrated green steel facility of 4 million metric tons annual capacity requiring approximately 400,000 metric tons of green hydrogen per year, equivalent to approximately 6.4 gigawatts of dedicated electrolysis capacity powered by approximately 32 terawatt-hours of renewable electricity annually, a supply chain scale that currently exceeds total installed global electrolysis capacity and requires coordinated investment in renewable energy generation, transmission infrastructure, electrolyzer manufacturing scale-up, and hydrogen storage and distribution systems to achieve reliable commercial supply. Green hydrogen production cost reduction is progressing along a steep learning curve, with electrolyzer capital costs declining from approximately USD 1,400 per kilowatt in 2020 to approximately USD 720 per kilowatt in 2025 and projected to reach approximately USD 280 per kilowatt by 2032 as manufacturing scale, technology maturation, and supply chain development compound, enabling green hydrogen production costs to decline from approximately USD 4.8 per kilogram in 2025 toward USD 1.5 to USD 2.0 per kilogram in regions with the most favorable renewable electricity resources by the early 2030s, a cost trajectory that makes hydrogen-based green steel production economics progressively more competitive with fossil-based alternatives across the forecast period. The competitive landscape of the global green steel market includes not only established integrated steelmakers pursuing green transition programs but also new entrant green steel ventures including Boston Metal with its molten oxide electrolysis technology, H2 Green Steel in Sweden developing a greenfield hydrogen-based steel facility with 5 million metric ton annual capacity at full scale, and Stegra in Sweden building one of the world’s largest green hydrogen and green steel production complexes, collectively representing a new category of green steel pure-play companies whose technology differentiation and capital market access are reshaping competitive dynamics in the nascent green steel market.

Key Drivers

Strengthening Carbon Pricing Mechanisms and the European Union Carbon Border Adjustment Mechanism Fundamentally Altering the Cost Economics of Conventional Versus Green Steelmaking

The progressive strengthening of carbon pricing frameworks across the European Union, United Kingdom, Canada, and other major economies is systematically increasing the operating cost of conventional blast furnace steelmaking while improving the relative cost competitiveness of low-emission green steel production routes, creating a carbon cost-driven economic incentive for steelmaker investment in green production technology that compounds with each incremental increase in carbon price and progressively accelerates the financial case for green steel capital investment programs. The European Union Emissions Trading System carbon price, which averaged approximately USD 68 per metric ton of carbon dioxide equivalent in 2025, directly increases the production cost of conventional blast furnace steel by approximately USD 110 to USD 140 per metric ton given the approximately 1.8 to 2.1 metric tons of carbon dioxide emitted per metric ton of steel produced through the conventional integrated route, while hydrogen-based direct reduced iron steel production emits approximately 0.1 to 0.3 metric tons of carbon dioxide per metric ton of steel using green hydrogen, generating a carbon cost advantage of approximately USD 100 to USD 130 per metric ton under current EU ETS pricing that substantially narrows the overall green premium. The Carbon Border Adjustment Mechanism, which entered its transitional phase in October 2023 and will become fully operative in 2026, extends this carbon cost signal to steel imports entering the European Union by requiring importers to surrender carbon certificates equivalent to the embedded carbon content of imported steel products, effectively applying the EU ETS carbon cost to competing steel imports and preventing carbon leakage while simultaneously expanding the market incentive for green steel investment by domestic and international steel suppliers seeking to maintain European market access competitively.

Corporate Net-Zero Procurement Commitments and Scope 3 Emissions Reduction Obligations Generating Structural Long-Term Demand Pull for Certified Green Steel Across Key End-Use Industries

The science-based net-zero commitments adopted by major global corporations across automotive, construction, consumer goods, and industrial equipment manufacturing sectors are creating a structural and commercially durable demand pull for green steel as a critical Scope 3 emissions reduction lever, given that steel is typically the highest-emission purchased material in the supply chains of vehicle manufacturers, construction companies, and capital equipment producers, and cannot be substituted with alternative materials in the majority of structural, safety-critical, and high-strength applications where steel’s performance characteristics remain technically irreplaceable. The Science Based Targets initiative steel sector guidance requires companies with steel-intensive value chains to engage with steel suppliers on decarbonization roadmaps and set supplier emissions reduction expectations aligned with a 1.5-degree Celsius warming pathway, translating corporate sustainability commitments directly into procurement specification requirements that favor certified green steel supply. The automotive sector’s Scope 3 decarbonization imperative is particularly commercially significant for the green steel market, as vehicle manufacturers have publicly committed to specific carbon intensity reduction targets for purchased steel that require greener steel supply at commercial scale by the late 2020s, with Volkswagen Group targeting a 45% reduction in supply chain emissions per vehicle by 2030 relative to 2018, Mercedes-Benz committing to carbon-neutral new vehicle sales by 2039, and Volvo Cars having already signed the world’s first commercial green steel supply agreement with SSAB in 2021, collectively representing a pipeline of contracted and anticipated green steel demand from the automotive sector alone that is sufficient to justify multiple large-scale green steel production investments through the forecast period.

Government Industrial Decarbonization Policy Support, Green Hydrogen Investment Programs, and Transition Finance Mechanisms Enabling Commercial-Scale Green Steel Infrastructure Investment

Government industrial policy support for green steel and green hydrogen infrastructure investment has emerged as an essential demand-side and supply-side enabler of the global green steel market, with major economies including the European Union, United States, Germany, Sweden, Japan, South Korea, India, and Australia deploying substantial public financing, production subsidies, grant funding, and regulatory frameworks that de-risk private investment in first-of-kind commercial scale green steel facilities whose capital cost, technology risk, and hydrogen supply chain dependency create investment barriers that market pricing signals alone are insufficient to overcome in the near term. The United States Inflation Reduction Act provides production tax credits of USD 3.00 per kilogram for clean hydrogen production meeting a 0.45 kilogram carbon dioxide equivalent per kilogram hydrogen threshold, directly reducing the effective cost of green hydrogen for steel producers investing in hydrogen-based direct reduced iron facilities within the United States, while the USD 6.0 billion Industrial Demonstrations Program administered by the Department of Energy has allocated funding specifically for steel sector decarbonization demonstrations. The European Union Innovation Fund and national hydrogen strategies within Germany, Netherlands, and Sweden have committed cumulative grant funding exceeding EUR 4.2 billion specifically for green hydrogen production and green steel pilot and first commercial scale projects, reducing the equity risk for steelmakers advancing investment decisions on hydrogen-based production infrastructure. In India, the National Green Hydrogen Mission has allocated approximately USD 2.3 billion in production-linked incentive support for green hydrogen production that is specifically designed to enable downstream industrial applications including green steel, positioning India as a strategically important emerging green steel production location for export to decarbonization-committed markets in Asia and Europe.

Key Challenges

Green Hydrogen Supply Scarcity, High Production Cost, and Infrastructure Development Timelines Constraining the Pace of Hydrogen-Based Green Steel Capacity Deployment

The availability of green hydrogen at the scale, cost, purity specification, and reliability of supply required for commercial hydrogen-based direct reduced iron steelmaking represents the most critical near-term constraint on global green steel market expansion, as current global green hydrogen production capacity of approximately 0.8 million metric tons per year falls profoundly short of the estimated 35 million metric tons of green hydrogen annually that would be required to decarbonize global steel production through the hydrogen-based direct reduction pathway at full deployment, highlighting the scale of renewable energy generation, electrolyzer manufacturing, and hydrogen infrastructure investment that must be mobilized in parallel with steelmaking decarbonization investment to enable the green steel market to reach its long-term potential. The current green hydrogen production cost of approximately USD 4.5 to USD 6.0 per kilogram in most markets adds approximately USD 340 to USD 450 per metric ton of steel produced through hydrogen-based direct reduced iron and electric arc furnace routes relative to green hydrogen’s eventual cost parity target of USD 1.5 to USD 2.0 per kilogram, creating a green steel production cost premium that is commercially manageable within automotive and premium industrial applications but remains prohibitive for price-sensitive construction and commodity steel end uses that collectively represent the majority of global steel consumption volume. The physical infrastructure required for large-scale green hydrogen supply to steelmaking facilities, encompassing electrolyzer installations, hydrogen compression and storage systems, pipeline or tube trailer distribution networks, and port or terminal unloading infrastructure for imported hydrogen, requires long development lead times and coordinated multi-stakeholder investment that creates execution risk and timeline uncertainty for green steel projects dependent on third-party hydrogen supply.

Exceptionally High Capital Investment Requirements for Green Steel Facility Construction and the Financing Risk of First-of-Kind Commercial Scale Decarbonization Projects

The transition from conventional blast furnace and basic oxygen furnace steelmaking to hydrogen-based direct reduced iron and electric arc furnace production requires capital investment of approximately USD 800 million to USD 1.4 billion per million metric tons of annual green steel capacity, with a single large integrated green steel facility of 4 million metric ton annual capacity requiring total capital expenditure of approximately USD 3.5 billion to USD 5.5 billion including direct reduced iron shaft furnace units, electric arc furnaces, ancillary processing and finishing equipment, on-site electrolyzer and renewable energy infrastructure, and associated hydrogen storage and logistics systems, representing capital commitments of a scale that concentrate risk within individual steelmaker balance sheets and require extensive external financing from green bonds, sustainability-linked loans, government grant funding, and development bank instruments to achieve bankable financing structures. The technology risk profile of first-of-kind commercial scale hydrogen-based steelmaking operations, which have not been demonstrated at full industrial scale with consistent operational performance and product quality data across the range of steel grades demanded by automotive and construction customers, creates lender and equity investor risk aversion that increases the cost of capital and restricts the financing terms available for green steel project developers, requiring government loan guarantee programs, first-loss capital instruments, and credit enhancement mechanisms to bridge the bankability gap between private market risk appetite and the investment scale required. Existing integrated steelmakers face the additional capital allocation challenge of managing stranded asset risk on conventional blast furnace infrastructure with remaining book value and operational life, creating balance sheet pressure that competes with green transition capital requirements for corporate investment capacity within organizations simultaneously managing ongoing steel production operations.

Scrap Steel Quality Constraints, Geographic Scrap Supply Imbalances, and Grid Electricity Carbon Intensity Limiting the Decarbonization Potential of Electric Arc Furnace Expansion Strategies

The electric arc furnace steelmaking pathway, which uses recycled steel scrap as its primary iron input and renewable electricity as its energy source, offers a lower capital cost and nearer-term decarbonization option relative to hydrogen-based direct reduced iron investment, but faces structural constraints arising from the limited global availability of high-quality steel scrap in the quantities and specifications required for producing flat-rolled automotive and appliance grades, the geographic mismatch between scrap availability concentrated in mature industrialized economies and steel demand growth concentrated in developing economies with limited scrap generation, and the carbon intensity of national electricity grids in major steel-producing countries that substantially reduces the emissions reduction achievable through electric arc furnace steelmaking absent access to dedicated renewable power purchase agreements or on-site generation. High-quality scrap availability is projected to remain structurally constrained in developing markets through the forecast period, as the relatively young average age of the steel-containing infrastructure and vehicle parc in China, India, Southeast Asia, and Africa limits near-term scrap generation volumes from end-of-life recovery, while the long-term structural shift in steel production toward electric arc furnace routes in mature markets will itself increase competition for available high-quality scrap and support scrap price levels that compress electric arc furnace producer margins and limit the financial benefit of transitioning from integrated blast furnace and basic oxygen furnace production. The carbon intensity of electricity supply remains a critical determinant of electric arc furnace steel emissions performance, with countries dependent on coal-fired grid electricity generating electric arc furnace steel with lifecycle emissions that can approach or exceed those of conventional blast furnace production when upstream power sector emissions are fully allocated, creating the requirement for dedicated renewable energy infrastructure investment alongside electric arc furnace capacity as a prerequisite for green steel certification under rigorous lifecycle assessment-based standards.

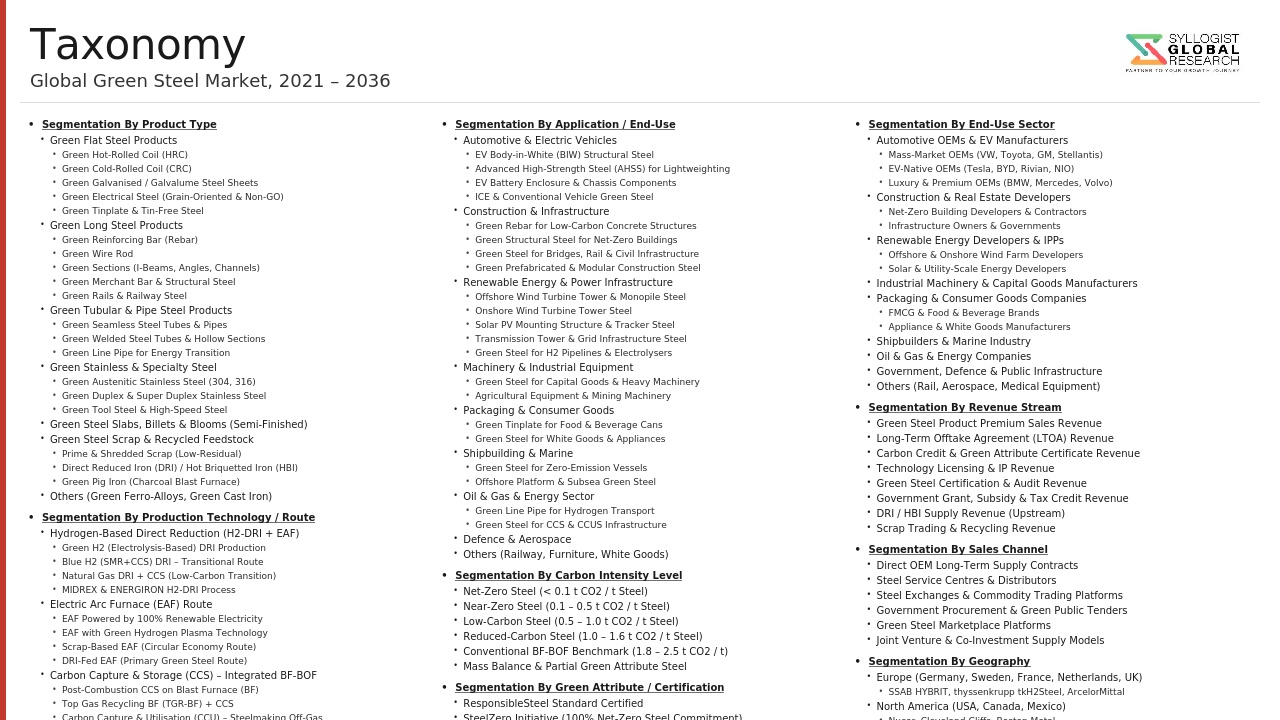

Market Segmentation

- Segmentation By Production Technology

- Hydrogen-Based Direct Reduced Iron and Electric Arc Furnace (H2-DRI-EAF)

- Scrap-Based Electric Arc Furnace with Renewable Electricity

- Natural Gas Direct Reduced Iron with Carbon Capture, Utilization and Storage

- Molten Oxide Electrolysis and Electrochemical Ironmaking

- Biomass and Biochar-Based Blast Furnace Steelmaking

- Hybrid Transition Technologies (Partial Hydrogen Injection, Top Gas Recycling)

- Others

- Segmentation By Product Type

- Flat-Rolled Green Steel (Hot-Rolled Coil, Cold-Rolled Coil, Galvanized Sheet)

- Long Green Steel Products (Reinforcing Bar, Wire Rod, Structural Sections, Rails)

- Green Steel Tubes, Pipes, and Hollow Sections

- Green Stainless and Specialty Alloy Steel

- Green Steel Billets and Slabs (Semi-Finished)

- Others

- Segmentation By Carbon Intensity Classification

- Near-Zero Emission Steel (Below 0.4 Metric Tons CO2 per Metric Ton of Steel)

- Low-Carbon Steel (0.4 to 1.0 Metric Tons CO2 per Metric Ton of Steel)

- Transitional Low-Carbon Steel (1.0 to 1.4 Metric Tons CO2 per Metric Ton of Steel)

- Segmentation By Certification and Standard

- ResponsibleSteel Certified

- Science Based Targets Initiative Aligned

- SteelZero Compliant Supply

- EU Taxonomy Aligned Green Steel

- Buyer-Specific Certified Green Steel (OEM or Offtaker Defined)

- Others

- Segmentation By End-Use Industry

- Automotive and Light Vehicle Manufacturing

- Commercial Vehicle and Heavy Transport Manufacturing

- Building and Construction (Structural Steel and Reinforcing Bar)

- Mechanical Engineering and Industrial Machinery

- Energy Infrastructure (Wind Towers, Solar Mounting, Transmission)

- Shipbuilding and Offshore Structures

- Packaging and Consumer Appliances

- Railways and Transportation Infrastructure

- Others

- Segmentation By Sales Model

- Long-Term Offtake Agreements and Green Steel Purchase Commitments

- Spot Market and Short-Term Contract Sales

- Book-and-Claim Certificate-Based Green Steel Attribution

- Integrated Value Chain Supply (Captive Green Steel Production)

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Green Steel Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by production technology including hydrogen-based direct reduced iron and electric arc furnace, scrap-based electric arc furnace with renewable electricity, natural gas direct reduced iron with carbon capture, and emerging electrochemical ironmaking routes, and by end-use industry including automotive, construction, energy infrastructure, and industrial machinery, to enable steel producers, green hydrogen developers, automotive and construction companies, sustainability-linked investors, and government industrial policy planners to identify which production pathways and demand sectors will generate the largest green steel market volumes and the most commercially durable revenue growth across the forecast period to 2034?

- How are carbon pricing mechanisms including the European Union Emissions Trading System and the Carbon Border Adjustment Mechanism, corporate Scope 3 emissions reduction commitments aligned with Science Based Targets initiative steel sector guidance, and public procurement low-carbon steel mandates in the European Union, United Kingdom, and Nordic markets expected to drive green premium compression, demand volume growth, and supply chain green steel certification adoption on a region-by-region and end-use sector basis through 2034, and at what carbon price levels and green hydrogen production cost thresholds does hydrogen-based green steel achieve full production cost parity with conventional blast furnace steel across major steelmaking geographies?

- What is the current production capacity, technology platform, hydrogen supply strategy, customer offtake portfolio, certification approach, capital investment program, and competitive positioning of the leading green steel producers globally including SSAB, H2 Green Steel, Stegra, Thyssenkrupp Steel, ArcelorMittal, Salzgitter, Tata Steel Europe, and emerging pure-play green steel ventures pursuing molten oxide electrolysis and other novel electrolytic ironmaking technologies, and how are these market participants differentiating their commercial propositions through certified emissions intensity, product grade breadth, long-term supply agreement structures, and collaborative decarbonization partnerships with major automotive and construction customers?

- What is the green hydrogen supply availability outlook, production cost reduction trajectory, and infrastructure development pipeline required to support hydrogen-based green steel production capacity scaling through 2034 across the key green steel production regions in Europe, North America, the Middle East, and Asia-Pacific, and how are steelmakers managing the hydrogen supply chain risk and cost uncertainty of transitional periods when green hydrogen supply is insufficient to meet full direct reduced iron operational requirements, including the assessment of natural gas and blue hydrogen bridge strategies, long-term renewable power purchase agreements, and on-site electrolysis investment as alternative hydrogen sourcing models?

- What are the regional green steel market development trajectories across Europe, North America, Asia-Pacific, the Middle East, and Latin America, considering the distinct carbon regulatory environments, renewable electricity cost and availability, scrap steel supply adequacy, government industrial policy support frameworks, domestic steel industry structure, and green steel demand maturity in each region, and which geographic markets are expected to transition from early commercial green steel activity to large-scale low-emission production at the fastest pace, and where are the most strategically significant greenfield and brownfield green steel investment opportunities expected to emerge through 2034 for steelmakers, green hydrogen developers, technology licensors, and infrastructure investors?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Technology & Commercialisation Risk

- Raw Material & Supply Chain Risk

- Regulatory & Policy Risk

- Market & Demand Risk

- Financial & Investment Risk

- Regulatory Framework & Standards

- Green Steel Classification & Taxonomy Frameworks

- Carbon Pricing, Emissions Trading & Border Carbon Adjustment Regulations

- Energy Efficiency & Environmental Emission Standards for Steel Plants

- Trade, Export & Carbon Border Standards

- Quality, Certification, MRV & Reporting Standards

- Global Green Steel Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Million Tonnes of Crude Steel)

- Market Size & Forecast by Production Route / Technology

- Green Hydrogen-Based Direct Reduced Iron + Electric Arc Furnace (H-DRI + EAF)

- Scrap-Based Electric Arc Furnace (EAF) Powered by Renewable Energy

- Natural Gas / LNG-Based DRI + EAF (Transitional Bridge Route)

- Blast Furnace – Basic Oxygen Furnace (BF-BOF) with Carbon Capture, Utilisation & Storage (CCUS)

- Biomass & Biocoal-Based Steelmaking (Bio-PCI, Charcoal BF, Agricultural Residue DRI)

- Electrolysis-Based Steelmaking: Molten Oxide Electrolysis (MOE), Hydrogen Plasma & Electrowinning (Emerging)

- Market Size & Forecast by Carbon Intensity Category

- Near-Zero Green Steel (Below 0.4 tCO2 per Tonne of Crude Steel)

- Low-Carbon Green Steel (0.4 to 1.0 tCO2 per Tonne of Crude Steel)

- Transitional Green Steel (1.0 to 2.0 tCO2 per Tonne of Crude Steel)

- Conventional Steel Benchmark: Business-as-Usual (Above 2.0 tCO2 per Tonne of Crude Steel)

- Market Size & Forecast by Product Type

- Long Products (Bars, Rods, Wire Rods, Structural Sections & Rails)

- Flat Products (Hot Rolled Coil, Cold Rolled Coil, Galvanised Coil, Plates & Electrical Steel)

- Pipes & Tubes (Seamless, Welded ERW / LSAW / SSAW & Hollow Sections)

- Stainless & Specialty Green Steel (Low-Carbon Stainless, Alloy Steel & HSLA Steel)

- Market Size & Forecast by End-Use Industry

- Construction & Infrastructure (Residential, Commercial, Industrial Buildings, Bridges & Transport Infrastructure)

- Automotive & Transportation (Passenger Vehicles, Commercial Vehicles, Electric Vehicles & Railways)

- Energy Sector (Renewable Energy Structures, Oil & Gas Pipelines & Nuclear Power Components)

- General Engineering & Capital Goods (Industrial Machinery, Defence, Aerospace & Shipbuilding)

- Consumer Goods & Packaging (White Goods, Appliances & Steel Packaging)

- Market Size & Forecast by Steelmaking Process

- Integrated Route: Blast Furnace Basic Oxygen Furnace (BF-BOF) with Decarbonisation Add-Ons

- Electric Arc Furnace (EAF) Based Secondary Route: Scrap + Renewable Power

- Direct Reduced Iron – Electric Arc Furnace (DRI-EAF) Route: Coal-Based, Gas-Based & H2-Based DRI

- Induction Furnace (IF) Based Route: Scrap Melting with Renewable Power (SME Segment)

- Market Size & Forecast by Certification Standard

- ResponsibleSteel International Standard Site Certified

- Science-Based Targets Initiative (SBTi) Steel Sector Aligned

- ISO 14064 GHG Quantification & ISO 14067 Product Carbon Footprint Verified

- National / Regional Green Steel Taxonomy Certified (India GS1/GS2/GS3, EU, Japan, Korea, etc.)

- Customer-Specific Bilateral Green Steel Offtake Agreement Verified

- Market Size & Forecast by Sales Channel

- Direct OEM & Large Industrial Buyer Supply (Long-Term Offtake Agreement)

- Government & Public Sector Procurement (Infrastructure, Defence & Railways)

- Steel Service Centre & Trader / Distributor Network

- Export Market Supply (Cross-Border Trade & CBAM-Compliant Export Channels)

- North America Green Steel Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Tonnes of Crude Steel)

- By Production Route / Technology

- By Carbon Intensity Category

- By Product Type

- By End-Use Industry

- By Steelmaking Process

- By Certification Standard

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Green Steel Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Tonnes of Crude Steel)

- By Production Route / Technology

- By Carbon Intensity Category

- By Product Type

- By End-Use Industry

- By Steelmaking Process

- By Certification Standard

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Green Steel Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Tonnes of Crude Steel)

- By Production Route / Technology

- By Carbon Intensity Category

- By Product Type

- By End-Use Industry

- By Steelmaking Process

- By Certification Standard

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Green Steel Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Tonnes of Crude Steel)

- By Production Route / Technology

- By Carbon Intensity Category

- By Product Type

- By End-Use Industry

- By Steelmaking Process

- By Certification Standard

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Green Steel Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Tonnes of Crude Steel)

- By Production Route / Technology

- By Carbon Intensity Category

- By Product Type

- By End-Use Industry

- By Steelmaking Process

- By Certification Standard

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Green Steel Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Tonnes of Crude Steel)

- By Production Route / Technology

- By Carbon Intensity Category

- By Product Type

- By End-Use Industry

- By Steelmaking Process

- By Certification Standard

- By Country

- By Sales Channel

- Market Size & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Italy, Spain, Poland, Sweden, Russia, China, Japan, South Korea, India, Australia, Brazil, Argentina, Saudi Arabia, UAE, South Africa, Turkey, Taiwan

- Technology Landscape & Innovation Analysis

- Green Hydrogen-Based DRI (H-DRI) Technology Deep-Dive

- Midrex H2 Shaft Furnace Technology: Process Description, H2 Purity Requirements & Commercial Scale-Up Status

- HYL / Energiron ZR H2-DRI Technology: Self-Reforming Capability & NG-to-H2 Blend Transition Pathway

- HYFOR & Circored Fluidised Bed H2-Reduction Technology: Fine Ore Processing & Pilot-to-Commercial Outlook

- H-DRI Hot Briquetted Iron (HBI) Production & Long-Distance Export Logistics Technology

- Green Hydrogen Supply Chain Technology for Steel: Electrolyser Integration, H2 Compression, Storage & Pipeline Delivery

- Electric Arc Furnace (EAF) Technology for Green Steel

- Blast Furnace – Basic Oxygen Furnace (BF-BOF) Decarbonisation Technology

- Carbon Capture, Utilisation & Storage (CCUS) Technology for Steel Plants

- Biomass & Alternative Reductant Technology for Steelmaking

- Electrolysis-Based & Next-Generation Zero-Carbon Steelmaking Technology

- Digital, Analytics & Simulation Technology for Green Steel Development

- Patent & IP Landscape in Green Steelmaking

- Green Hydrogen-Based DRI (H-DRI) Technology Deep-Dive

- Value Chain & Supply Chain Analysis

- Raw Material Supply Chain (Iron Ore, Pellets, Scrap & Coking Coal Transition)

- Green Steel Technology & Equipment Supplier Chain

- Green Hydrogen & Renewable Energy Supply Chain for Steel

- Green Steel Producer & Integrated Mill Landscape

- Downstream Processing, Service Centre & Distribution

- Certification, MRV & Third-Party Verification Infrastructure

- End-of-Life & Circular Economy (Scrap Recovery, Slag Utilisation & By-Product Valorisation)

- Pricing Analysis

- H-DRI + EAF Green Steel Production Cost Analysis

- Scrap-Based EAF (Renewable-Powered) Green Steel Pricing Analysis

- BF-BOF + CCUS Green Steel Production Cost Analysis

- Green Steel Price Premium Analysis by Region & Product Category

- Carbon Cost & Carbon Border Adjustment Mechanism (CBAM) Financial Impact Analysis

- Capital Expenditure (Capex) & Green Finance Economics for Green Steel Transition

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Green Steelmaking Production Routes

- Carbon Footprint & GHG Emission Accounting (Scope 1, 2 & 3) for Green Steel

- Social & Just Transition Analysis for Coal-Dependent Steel Communities

- Environmental Compliance, Water Use & Biodiversity Impact of Green Steel Value Chain

- Net Zero Alignment, Climate Policy Contribution & Green Finance Classification

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Production Route & Region)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Production Route, Product Type & Geography

- Player Classification

- Large Integrated Steel Producers in Green Transition (BF-BOF + Decarbonisation Pathway)

- EAF-Native & Scrap-Based Green Steel Producers

- DRI-EAF Green Steel Specialists (Gas-DRI & H2-DRI Pathway)

- Greenfield H-DRI + EAF New Entrants & Pioneer Projects

- Technology Licensors & EPC Contractors for Green Steel Plants

- Green Hydrogen & Renewable Energy Suppliers to Steel Sector

- Public Sector Steel Producers Under Government Decarbonisation Mandate

- Steel Scrap Recycling & Secondary Steel Sector Players

- Competitive Analysis Frameworks

- Market Share Analysis by Production Route, Product Type & Region

- Company Profile

- Company Overview & Headquarters

- Green Steel Technology Portfolio & Certification Status

- Key Customer Relationships & Green Steel Offtake Agreements

- Manufacturing Footprint & Green Steel Production Capacity

- Revenue (Green Steel Segment) & Financial Performance

- Technology Differentiators & IP Portfolio

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Green Steel Milestones, Capex Announcements, Certifications)

- SWOT Analysis

- Strategic Focus Areas & Net Zero Roadmap

- Competitive Positioning Map (Decarbonisation Progress vs. Green Steel Volume)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Production Route, Product Type, End-Use Industry & Geography

- White Space Opportunity Analysis

- Strategic Output

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Market Development Strategy

- Customer & OEM Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Net Zero Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025–2028)

- Mid-term (2029–2032)

- Long-term (2033–2037)