Market Definition

The Global Adhesives and Sealants Market encompasses the research, formulation, manufacturing, distribution, and application of chemical bonding and sealing compounds used across a broad spectrum of industrial, commercial, and consumer end-use sectors, including automotive and transportation, construction and infrastructure, packaging, electronics and electrical, woodworking and furniture, medical devices, aerospace, and general assembly operations. Adhesives are functional chemical systems engineered to join two or more substrates through surface adhesion and internal cohesion, transmitting structural or non-structural loads across the bond interface, and are formulated across diverse chemistries including epoxies, polyurethanes, acrylics, cyanoacrylates, silicones, hot melts, pressure-sensitive systems, and reactive structural adhesive platforms tailored to specific substrate, performance, and processing requirements. Sealants are compliant chemical compounds applied to gaps, joints, seams, and interfaces to prevent the passage of air, water, gases, dust, or other media, providing environmental barrier performance, thermal and acoustic insulation contribution, and substrate protection across static and dynamic joint configurations in construction, automotive, aerospace, and industrial assembly applications. The market encompasses the complete value chain from raw material supply of base polymers, resins, crosslinkers, fillers, tackifiers, and specialty additives, through compounding and formulation operations, to packaging, distribution, and application system supply. Key participants include diversified specialty chemical manufacturers, focused adhesive and sealant formulators, raw material polymer producers, packaging and dispensing equipment suppliers, and end-user industries whose design and manufacturing process specifications define the performance, processing, and regulatory requirements governing adhesive and sealant formulation development across major global manufacturing and construction markets.

Market Insights

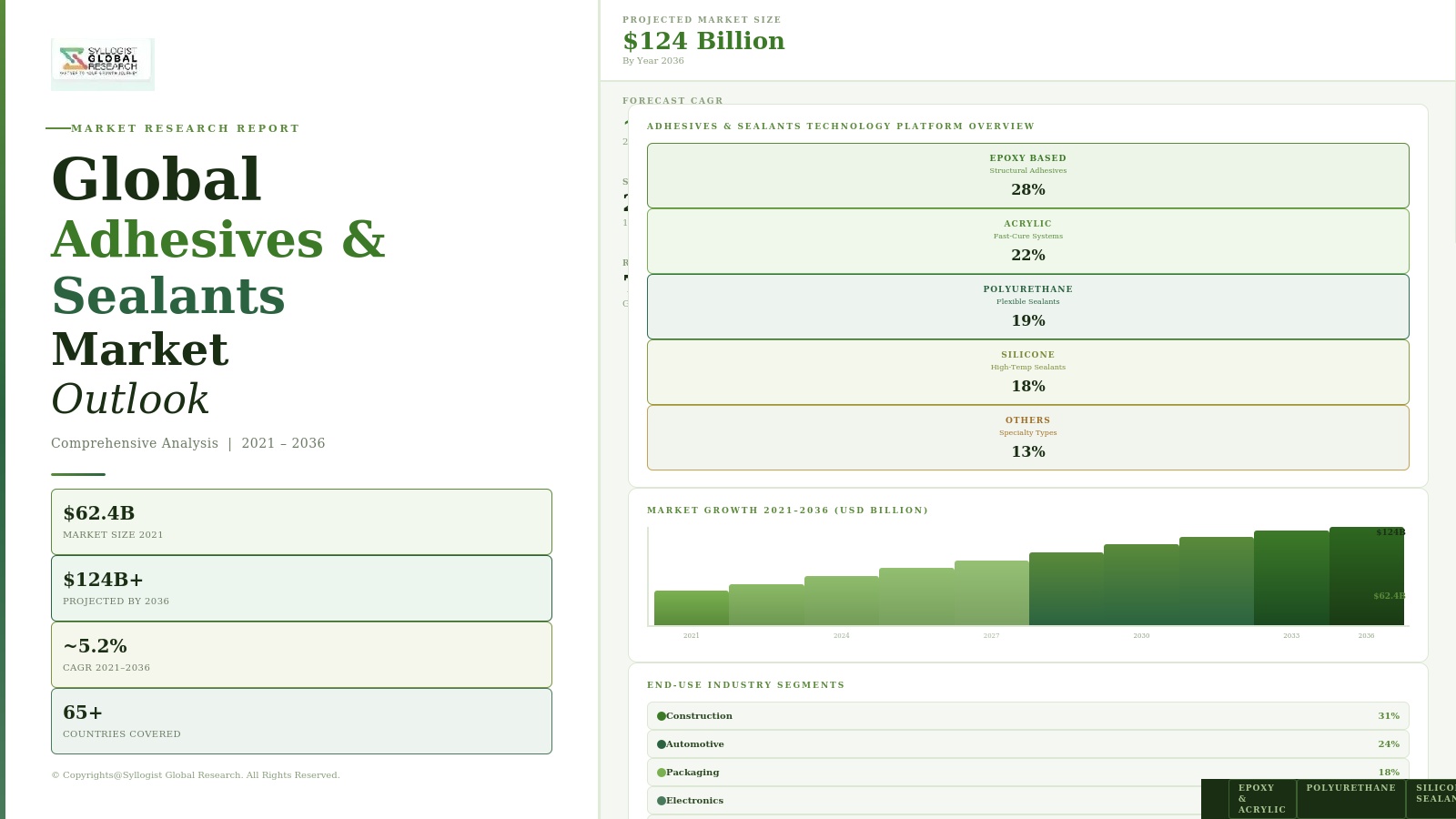

The global adhesives and sealants market was valued at approximately USD 71.4 billion in 2025 and is projected to reach USD 104.2 billion by 2034, advancing at a compound annual growth rate of 4.3% over the forecast period from 2027 to 2034. Growth is underpinned by the structural expansion of lightweight multi-material assembly in automotive and aerospace manufacturing, accelerating construction activity across emerging economies, and the increasing substitution of mechanical fastening and welding methods by structural adhesive bonding in applications where weight reduction, vibration damping, and galvanic corrosion prevention between dissimilar metal substrates deliver measurable design and performance benefits. The rising adoption of electric vehicles is reshaping adhesive demand composition within the automotive segment, where battery module assembly, thermal management interface bonding, structural body reinforcement, and acoustic management applications collectively generate adhesive content per vehicle that is significantly higher than the corresponding content in conventional internal combustion engine vehicles, creating a durable structural uplift in automotive adhesive market value even as vehicle production mix evolves.

Sustainability imperatives and regulatory pressure on volatile organic compound emissions are driving a technology transition within the adhesives and sealants market away from solvent-borne formulations toward waterborne, hot melt, radiation-curable, and reactive solvent-free systems across multiple end-use segments including packaging, woodworking, footwear, and general industrial assembly. Waterborne adhesives accounted for approximately 31% of global adhesive volume in 2025 and continue to gain share as formulators improve the wet-tack performance, heat resistance, and substrate compatibility of water-based systems to levels approaching those of incumbent solvent-borne technologies. Radiation-curable adhesives, encompassing ultraviolet and electron beam cure systems, are growing at approximately 7.8% annually, driven by electronics assembly, optical bonding, medical device manufacturing, and flexible packaging applications where instant cure, minimal thermal exposure, and solvent-free chemistry deliver process efficiency and substrate protection advantages unavailable from thermally activated or solvent-borne alternatives.

Asia-Pacific represents the largest and fastest-growing regional market for adhesives and sealants, accounting for approximately 46% of global consumption by volume in 2025, driven by China’s position as the world’s dominant manufacturing economy and construction market, India’s rapidly expanding automotive, packaging, and infrastructure sectors, and the combined industrial output of Japan, South Korea, Thailand, Indonesia, and Vietnam whose manufacturing supply chains generate broad-based adhesive and sealant demand across electronics, automotive, furniture, and general industrial assembly segments. China’s domestic adhesives and sealants market is experiencing strong demand growth in the electric vehicle battery assembly segment, flexible packaging sector, and infrastructure construction segment, while simultaneously undergoing formulation technology upgrading as Chinese manufacturers invest in waterborne and reactive adhesive capability to meet tightening environmental standards. North America and Europe together account for approximately 42% of global market revenue, with disproportionate revenue contribution from high-value structural adhesives, specialty sealants, and advanced reactive systems serving automotive OEM, aerospace, medical device, and electronics assembly applications.

The competitive landscape of the global adhesives and sealants market is characterized by a tiered structure in which a small number of diversified multinational specialty chemical companies command leading positions in technically differentiated product segments while a large and fragmented base of regional and local formulators compete primarily on price and service in commodity adhesive categories. Raw material cost volatility, particularly in base polymer feedstocks including polyurethane MDI and TDI isocyanates, epoxy resins, vinyl acetate monomer, and acrylate monomers, represents a persistent margin management challenge for adhesive formulators operating within contractually constrained customer pricing frameworks. Merger and acquisition activity has remained elevated as large adhesive manufacturers pursue technology portfolio expansion, geographic market entry, and application segment diversification through targeted acquisitions of specialty formulators with proprietary chemistry platforms and established customer qualification positions in high-growth segments including electric vehicle assembly, advanced electronics, and medical device bonding.

Key Drivers

Accelerating Multi-Material Lightweight Design in Automotive and Aerospace Manufacturing Structurally Expanding Adhesive Bonding Demand

The imperative to reduce vehicle and aircraft structural weight in order to improve fuel efficiency, extend electric vehicle driving range, and meet progressively stringent emissions regulations is compelling automotive and aerospace manufacturers to adopt multi-material design architectures that combine advanced high-strength steels, aluminum alloys, carbon fiber reinforced polymers, and glass fiber composites within a single structural assembly, creating bonding challenges that mechanical fasteners alone cannot adequately address and that structural adhesives are uniquely positioned to resolve by distributing load across the full bond area, preventing galvanic corrosion at dissimilar metal interfaces, and providing vibration damping and noise reduction contribution unavailable from riveted or bolted joints. The average structural adhesive content per passenger vehicle has increased from approximately USD 18 per vehicle in 2015 to approximately USD 47 per vehicle in 2025, driven by the proliferation of adhesive-bonded roof panel hem flanges, pillar reinforcements, door surround bonds, underbody acoustic pads, and powertrain mount isolators in both conventional and electric vehicle platforms. Electric vehicle platforms intensify this trend further, as battery enclosure sealing, cell-to-module bonding, thermal interface material application, and structural reinforcement of battery pack housings collectively require adhesive and sealant content of approximately USD 120 to USD 180 per vehicle, representing a step-change uplift in automotive adhesive value intensity that will sustain above-market revenue growth for structural and functional adhesive suppliers through the forecast period.

Construction Activity Expansion Across Emerging Economies and Building Envelope Performance Regulations Driving Sealant and Construction Adhesive Demand

Urbanization, infrastructure investment, and residential construction activity across Asia-Pacific, the Middle East, Africa, and Latin America are generating sustained and growing demand for construction adhesives and sealants spanning tile and stone installation, flooring adhesives, facade and curtain wall joint sealants, insulating glass unit edge seal systems, HVAC duct sealing, roofing membrane adhesives, and structural glazing sealants that collectively constitute the largest single end-use segment for the global sealants market by volume. Building energy efficiency regulations across the European Union, North America, China, and India are raising the technical performance requirements for building envelope sealing systems, compelling the adoption of high-performance polyurethane, silicone, and hybrid sealant formulations capable of maintaining air and water barrier integrity across wide temperature and movement cycles over design service lives of 20 to 30 years, generating a technology upgrade cycle in construction sealants that benefits premium formulation suppliers at the expense of commodity product manufacturers. The growing adoption of prefabricated modular construction and offsite building assembly methods is expanding the use of structural adhesives and elastic bonding sealants in factory assembly environments where process control, cure speed, and joint design flexibility offer workflow efficiency advantages over traditional wet-trade jointing methods, creating an incremental adhesive demand stream whose growth trajectory is closely linked to the global adoption rate of industrialized construction methods.

Flexible Packaging Industry Growth and Sustainability-Driven Lamination Adhesive Innovation Expanding Packaging Adhesive Market Value

The global flexible packaging industry is the largest single end-use segment for adhesives by volume, generating sustained demand for solvent-based, solvent-free, and waterborne lamination adhesives, heat-seal lacquers, cold-seal release and cohesive coating systems, and pressure-sensitive label adhesives across food, beverage, pharmaceutical, personal care, and industrial product packaging applications. The structural growth of flexible packaging relative to rigid packaging formats, driven by consumer preference for convenience, portion control, and reduced material weight, is generating a durable volume demand foundation for packaging adhesives even as individual pack sizes evolve and substrate combinations change. Sustainability mandates from consumer goods brand owners requiring mono-material recyclable flexible packaging structures are simultaneously creating a major technology transition opportunity for packaging adhesive formulators, as the shift from multi-layer multi-material laminate constructions to polyethylene or polypropylene mono-material films requires new lamination adhesive chemistries specifically engineered to bond similar polyolefin substrates with adequate peel strength, heat resistance, and optical clarity while maintaining compatibility with mechanical recycling streams, generating qualification and supply opportunities for specialty lamination adhesive developers who can deliver compliant chemistry ahead of regulatory and voluntary recyclability deadline commitments by major brand owners.

Key Challenges

Raw Material Price Volatility Across Polymer, Isocyanate, Epoxy Resin, and Monomer Supply Chains Compressing Adhesive Formulator Margins

Adhesive and sealant formulators operate at the intersection of multiple commodity and specialty chemical supply chains whose price dynamics are governed by petrochemical feedstock costs, production capacity utilization, and supply concentration at individual raw material manufacturing facilities, creating persistent and often correlated raw material cost volatility that is structurally difficult to pass through to end-use customers within the annual or multi-year pricing contracts that characterize adhesive supply relationships in automotive, packaging, and construction segments. Polyurethane adhesive and sealant formulations depend on methylene diphenyl diisocyanate and toluene diisocyanate supply from a globally concentrated producer base, where capacity shutdowns at individual facilities can trigger rapid and severe price escalation across the polyurethane adhesive formulation cost structure with limited short-term substitution options available. Epoxy resin feedstocks are subject to bisphenol-A and epichlorohydrin price cycles that can compress epoxy adhesive formulator margins by several percentage points within a single quarter during peak feedstock price events. Vinyl acetate monomer price volatility directly impacts the cost of waterborne polyvinyl acetate and vinyl acetate ethylene copolymer emulsion adhesives, the dominant technology in woodworking, packaging, and construction segment applications, where formulator pricing flexibility is most constrained by commodity competitive dynamics and price-sensitive end-user purchasing behavior that limits cost pass-through capability even during acute raw material cost spike events.

Regulatory Compliance Complexity Across Volatile Organic Compound Restrictions, Substance Restrictions, and Food Contact Approvals in Global Markets

Adhesive and sealant manufacturers serving global markets must simultaneously navigate a fragmented and continuously evolving regulatory landscape governing volatile organic compound emission limits, restricted substance lists, food contact material safety, occupational exposure standards, and transportation classification requirements whose specifics vary materially across the European Union, United States, China, Japan, India, and other major regulatory jurisdictions, imposing compliance infrastructure costs and formulation localization requirements that disproportionately burden mid-size and smaller adhesive manufacturers with limited regulatory affairs resources. The European Union REACH regulation and its candidate list of substances of very high concern has required the reformulation of numerous adhesive and sealant product lines containing phthalate plasticizers, certain epoxy curing agents, and bisphenol-A derived materials, generating development and re-qualification investment that must be completed within regulatory timelines regardless of commercial demand levels for the affected products. Food contact adhesive regulations in the European Union, United States Food and Drug Administration, and Chinese national standard frameworks impose compositional and migration testing requirements on packaging lamination adhesives, label adhesives, and cap liner sealants that require extensive analytical validation, supply chain ingredient disclosure, and periodic re-assessment as regulatory frameworks evolve, creating ongoing compliance management obligations that add cost and administrative complexity to the packaging adhesives business.

Substrate Diversity Proliferation and Application Process Complexity Increasing Technical Service Demands and New Product Development Investment Requirements

The proliferation of new substrate materials in automotive, electronics, and consumer product manufacturing, including engineered thermoplastics, low-surface-energy polyolefins, carbon fiber composites, coated metals, and ceramic and glass materials whose surface chemistry and mechanical properties differ fundamentally from the steel and wood substrates that defined adhesive application requirements in earlier decades, is compelling adhesive formulators to continuously invest in new product development programs that generate technically differentiated adhesive solutions for substrate combinations and application process constraints that existing product lines cannot adequately address. The growing complexity of automotive and electronics assembly process requirements, including demands for extended open time combined with rapid fixture strength development, single-component room-temperature-cure capability, compatibility with robotic dispensing systems at high throughput cycle rates, and performance stability through paint bake ovens at elevated temperatures, requires adhesive formulation platforms that must satisfy multiple simultaneously optimized technical parameters whose combination is not achievable through incremental modification of existing product chemistry. Customer qualification timelines in automotive OEM and electronics manufacturing segments extend from 12 to 36 months from initial technical submission to production approval, requiring adhesive suppliers to commit research and development resources to customer programs whose commercial volume outcome is uncertain at the time of investment, creating an innovation investment risk profile that favors large diversified adhesive manufacturers with broad program portfolios over smaller single-chemistry specialists with limited resources to sustain extended qualification pipelines across multiple concurrent customer development programs.

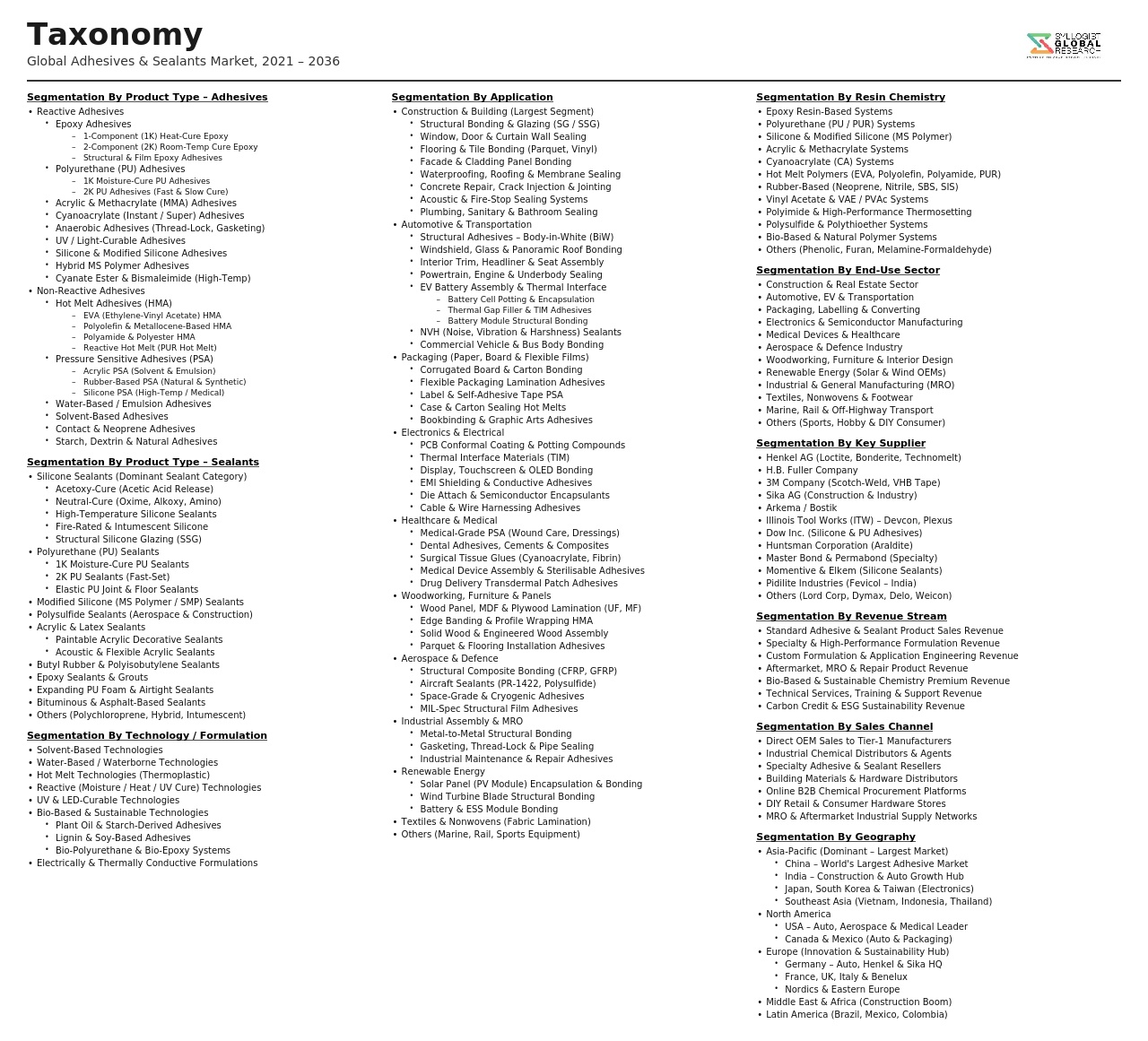

Market Segmentation

- Segmentation By Resin Type

- Epoxy Adhesives and Sealants

- Polyurethane Adhesives and Sealants

- Acrylic and Methacrylate Adhesives

- Silicone Sealants and Adhesives

- Hot Melt Adhesives (EVA, Polyolefin, and Reactive Hot Melt)

- Cyanoacrylate Adhesives

- Pressure-Sensitive Adhesives

- Polysulfide and Polyether Sealants

- Vinyl Acetate and VAE Emulsion Adhesives

- Others

- Segmentation By Technology

- Solvent-Borne Adhesives and Sealants

- Waterborne Adhesives and Sealants

- Hot Melt Systems

- Radiation-Curable (UV and EB) Adhesives

- Reactive and Two-Component Systems

- Pressure-Sensitive Adhesive Systems

- Others

- Segmentation By End-Use Industry

- Automotive and Transportation

- Construction and Infrastructure

- Flexible and Rigid Packaging

- Electronics and Electrical

- Woodworking and Furniture

- Medical Devices and Healthcare

- Aerospace and Defense

- Footwear and Leather Goods

- Textiles and Apparel

- General Industrial Assembly

- Others

- Segmentation By Application

- Structural Bonding and Load-Bearing Assembly

- Lamination and Film Bonding

- Sealing and Gasketing

- Acoustic and Vibration Damping

- Thermal Interface and Heat Management

- Potting and Encapsulation

- Labeling and Tape

- Others

- Segmentation By Substrate

- Metal and Aluminum

- Plastics and Composites

- Glass and Ceramics

- Wood and Engineered Wood Products

- Flexible Films and Foils

- Rubber and Elastomers

- Paper and Paperboard

- Others

- Segmentation By Cure Mechanism

- Heat-Activated Cure

- Moisture Cure

- UV and Radiation Cure

- Two-Component Reactive Cure

- Pressure-Activated Bond

- Anaerobic Cure

- Others

- Segmentation By Sales Channel

- Direct Sales to Industrial Manufacturers and OEMs

- Specialty Distributors and Wholesalers

- DIY Retail and Home Improvement Chains

- E-Commerce Platforms

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Adhesives and Sealants Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by resin type, epoxy, polyurethane, acrylic, silicone, and hot melt, and by end-use industry, automotive, construction, packaging, electronics, and woodworking, to enable adhesive manufacturers, raw material suppliers, end-use industry procurement functions, and investors to identify which chemistry platforms and application segments will generate the highest absolute revenue and the most durable growth trajectory across the forecast period in the context of multi-material lightweight design adoption, sustainability-driven technology transitions, and electric vehicle production scaling?

- How is the global transition to electric vehicle platforms expected to reshape the composition, volume, and value of automotive adhesive and sealant demand through 2034, including the relative demand trajectories for battery module bonding adhesives, thermal interface materials, structural body adhesives, and acoustic management sealants in battery electric versus hybrid electric versus internal combustion engine vehicle architectures, and which adhesive chemistry platforms and supplier profiles are best positioned to capture the incremental content uplift associated with battery pack assembly and electric drivetrain integration across major global automotive manufacturing regions?

- What is the projected market size, compound annual growth rate, and technology transition roadmap of the sustainable and low-VOC adhesive and sealant segment through 2034, encompassing waterborne, hot melt, radiation-curable, and reactive solvent-free systems, and how are brand owner recyclable packaging commitments, building energy efficiency regulations, and occupational health standards reshaping formulation technology investment priorities, qualification timelines, and competitive positioning across packaging lamination, construction sealant, and industrial assembly adhesive segments?

- How are raw material cost dynamics across polyurethane isocyanate, epoxy resin, vinyl acetate monomer, and acrylate feedstock supply chains expected to influence adhesive formulator margin trajectories, pricing strategies, and vertical integration or supply chain localization investment decisions through 2034, and what is the competitive differentiation impact of raw material cost management capability between diversified multinational adhesive manufacturers and regionally focused mid-size formulators serving the same end-use market segments?

- Who are the leading adhesive and sealant manufacturers, specialty formulation technology developers, and application system suppliers currently defining the competitive landscape of the global market, and what are their respective product portfolio breadth across resin chemistry platforms and end-use segments, manufacturing footprint and regional capacity expansion strategies, merger and acquisition activity and technology acquisition priorities, customer qualification status in automotive OEM and electronics assembly programs, and strategic roadmaps for addressing the sustainability, electrification, and substrate diversification megatrends reshaping adhesive demand composition and formulation requirements through 2034?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Raw Material Volatility, Petrochemical Feedstock Dependency & Supply Disruption Risk

- Volatile Organic Compound (VOC) Regulation, REACH Compliance & Hazardous Substance Risk

- End-Market Cyclicality: Construction, Automotive & Electronics Demand Sensitivity Risk

- Substitution Risk from Mechanical Fastening, Welding & Alternative Joining Technologies

- Counterfeit Products, Quality Assurance & Liability Risk in Critical Application Segments

- Regulatory Framework & Standards

- VOC Emission Limits, Solvent Restriction Regulations & Low-VOC Reformulation Requirements Across Key Geographies

- REACH, GHS/SDS, TSCA & Hazardous Chemical Classification Frameworks Applicable to Adhesive and Sealant Formulations

- Food Contact, Indirect Food Contact & Packaging Adhesive Regulations (FDA, EU 10/2011 & National Equivalents)

- Construction Product Regulation (CPR), Building Codes & Structural Adhesive Certification Standards

- Automotive OEM Approval, Aerospace Qualification & Medical Device Biocompatibility Standards for Adhesives & Sealants

- Global Adhesives & Sealants Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Kilotons)

- Market Size & Forecast by Product Type

- Adhesives

- Sealants

- Market Size & Forecast by Technology

- Water-Based (Waterborne) Adhesives & Sealants

- Solvent-Based Adhesives & Sealants

- Hot Melt Adhesives & Sealants

- Reactive Adhesives & Sealants (Epoxy, Polyurethane, Acrylic, Cyanoacrylate and Silicone)

- Pressure-Sensitive Adhesives (PSA)

- UV and Radiation-Curable Adhesives & Sealants

- Other Technologies (Anaerobic, Plastisol and Bio-Based)

- Market Size & Forecast by Resin Type

- Polyurethane (PU)

- Epoxy

- Acrylic and Methacrylate

- Silicone

- Vinyl Acetate Ethylene (VAE) and Polyvinyl Acetate (PVAc)

- Styrenic Block Copolymers (SBC: SIS, SBS and SEBS)

- Cyanoacrylate

- Polyolefin and Ethylene Vinyl Acetate (EVA)

- Natural Rubber and Bio-Based Resins

- Other Resin Types

- Market Size & Forecast by End-Use Industry

- Construction (Structural, Flooring, Roofing, Glazing and General Building & Construction)

- Automotive and Transportation (OEM Assembly, Aftermarket and EV Battery Assembly)

- Packaging (Flexible Packaging, Rigid Packaging, Labels and Case & Carton Sealing)

- Electronics and Electrical (Consumer Electronics, PCB Assembly and Semiconductor Packaging)

- Woodworking, Furniture and Flooring

- Medical and Healthcare (Medical Device Assembly, Wound Care and Drug Delivery)

- Aerospace and Defence

- Textiles, Nonwovens and Footwear

- Paper and Bookbinding

- Marine, Energy and Industrial MRO

- Market Size & Forecast by Application

- Structural Bonding and Load-Bearing Assembly

- Surface Lamination and Film Bonding

- Gap Filling, Sealing and Weatherproofing

- Pressure-Sensitive Labelling and Taping

- Potting, Encapsulation and Underfill

- Threadlocking, Retaining and Gasketing

- Market Size & Forecast by Substrate

- Metal and Metal Alloys

- Plastics and Composites

- Wood and Cellulosic Substrates

- Glass and Ceramics

- Rubber and Elastomers

- Concrete, Stone and Masonry

- Flexible Films and Foils

- Market Size & Forecast by Sales Channel

- Direct Sales to OEMs and Industrial End-Users

- Specialty Distributors and Chemical Wholesalers

- Retail and DIY Channels

- E-Commerce and Online Marketplaces

- North America Adhesives & Sealants Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotons)

- By Product Type

- By Technology

- By Resin Type

- By End-Use Industry

- By Application

- By Substrate

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Adhesives & Sealants Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotons)

- By Product Type

- By Technology

- By Resin Type

- By End-Use Industry

- By Application

- By Substrate

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Adhesives & Sealants Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotons)

- By Product Type

- By Technology

- By Resin Type

- By End-Use Industry

- By Application

- By Substrate

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Adhesives & Sealants Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotons)

- By Product Type

- By Technology

- By Resin Type

- By End-Use Industry

- By Application

- By Substrate

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Adhesives & Sealants Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotons)

- By Product Type

- By Technology

- By Resin Type

- By End-Use Industry

- By Application

- By Substrate

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Adhesives & Sealants Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotons)

- By Product Type

- By Technology

- By Resin Type

- By End-Use Industry

- By Application

- By Substrate

- By Country

- By Sales Channel

- Market Size & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Italy, Spain, Poland, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel

- Technology Landscape & Innovation Analysis

- Waterborne Adhesive & Sealant Formulation Technology Deep-Dive

- Reactive Polyurethane (PUR and STP) Hot Melt Technology

- Structural Epoxy and Hybrid Adhesive Technology for Automotive and Aerospace Lightweighting

- UV and Radiation-Curable Adhesive Chemistry Innovations

- Bio-Based and Sustainable Adhesive Resin Technology

- Electrically Conductive and Thermally Conductive Adhesive Technology for Electronics

- Smart Adhesives: Reversible, Debondable and Stimuli-Responsive Bonding Systems

- Patent & IP Landscape in Adhesive & Sealant Technologies

- Value Chain & Supply Chain Analysis

- Petrochemical and Bio-Based Raw Material Supply Chain (Monomers, Resins and Polymers)

- Specialty Chemical and Additive Supply Chain (Crosslinkers, Plasticisers, Tackifiers and Fillers)

- Adhesive and Sealant Formulation and Compounding

- Packaging, Labelling and Regulatory Compliance for Finished Products

- Distribution Network: Specialty Distributors, Wholesale and Retail Channels

- Industrial End-User and OEM Procurement Landscape

- Waste Management, VOC Recovery and Circular Economy in Adhesive Manufacturing

- Pricing Analysis

- Raw Material Cost Structure: Petrochemical Feedstock and Polymer Price Trends

- Waterborne Adhesive Pricing Trends by End-Use Industry

- Hot Melt and Reactive Hot Melt Adhesive Pricing Analysis

- Structural and Engineering Adhesive Price Benchmarking (Epoxy, PU and Acrylic)

- Sealant Pricing Analysis by Resin Type and Application Segment

- Pricing Dynamics, Contract Structures and Volume Discount Frameworks

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Adhesives & Sealants: Carbon Footprint, VOC Emissions and Waste Generation Across Technology Routes

- Transition to Low-VOC, Solvent-Free and Waterborne Technologies: Regulatory Drivers and Market Adoption

- Bio-Based Adhesive Adoption: Feedstock Sourcing, Carbon Sequestration Benefits and Commercial Readiness

- Circular Economy in Adhesives: Debondable Systems, Substrate Recyclability and End-of-Life Considerations

- Regulatory-Driven Sustainability, REACH, SDG Alignment and ESG Disclosure in Adhesive & Sealant Supply Chains

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Technology, End-Use and Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Technology, End-Use Industry and Geography

- Player Classification

- Global Integrated Adhesive and Sealant Manufacturers

- Specialty Structural and Engineering Adhesive Companies

- Hot Melt and Pressure-Sensitive Adhesive Specialists

- Silicone and Specialty Sealant Manufacturers

- Waterborne and Sustainable Adhesive Producers

- Regional and Private Label Adhesive Manufacturers

- Competitive Analysis Frameworks

- Market Share Analysis by Technology, End-Use Industry and Region

- Company Profile

- Company Overview & Headquarters

- Adhesive & Sealant Product Portfolio and Technology Platforms

- Key Customer Relationships & Reference Accounts

- Manufacturing Footprint & Production Capacity

- Revenue (Adhesives & Sealants Segment) and R&D Spend

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Product Launches, Capacity Expansions and Approvals)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Breadth vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Strategic Outlook & Opportunity Analysis

- Strategic Output

- Market Opportunity Matrix: By Technology, Resin Type, End-Use Industry, Application and Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output