Market Definition

The Global Digital Twin Technologies in Mining Market encompasses the development, deployment, integration, and operation of virtual replication systems that create dynamic, data-synchronized digital representations of physical mining assets, geological formations, processing facilities, underground and surface mine environments, equipment fleets, and supply chain networks, enabling mining operators to simulate, monitor, optimize, predict, and control physical mining operations through their continuously updated virtual counterparts. A digital twin in the mining context is a physics-informed, data-driven computational model that integrates real-time sensor data streams, geological survey inputs, equipment telemetry, process measurements, and operational data from Internet of Things networks, autonomous equipment systems, advanced drilling and blasting instrumentation, and plant control systems to generate a living digital replica whose fidelity and synchronization with the physical asset enables simulation-based decision support, predictive maintenance, production optimization, safety scenario modelling, and remote operation capability that are not achievable through conventional static modelling or retrospective data analysis approaches. The market spans digital twin applications across the complete mining value chain from exploration and resource modelling through mine planning and design, open pit and underground mining operations, ore haulage and materials handling, processing plant operations, tailings and waste management, environmental monitoring, and mine closure planning. Technology components encompassed by the market include three-dimensional geological and geotechnical modelling platforms, mine planning and scheduling simulation software, process plant dynamic simulation systems, equipment health monitoring and predictive maintenance digital twin modules, autonomous and remote operations control platforms, environmental and geotechnical monitoring twin systems, and the underlying data integration middleware, cloud computing infrastructure, artificial intelligence and machine learning analytics engines, and industrial Internet of Things connectivity frameworks that enable the data ingestion, synchronization, and computational processing required to operate high-fidelity mining digital twin systems at production scale. Key participants include mining software specialists, industrial automation and control system providers, cloud infrastructure and platform companies, artificial intelligence and analytics developers, mining original equipment manufacturers integrating digital twin capability into connected equipment offerings, and the mining operators whose operational improvement imperatives and capital productivity requirements are driving digital twin technology adoption across the global mining industry.

Market Insights

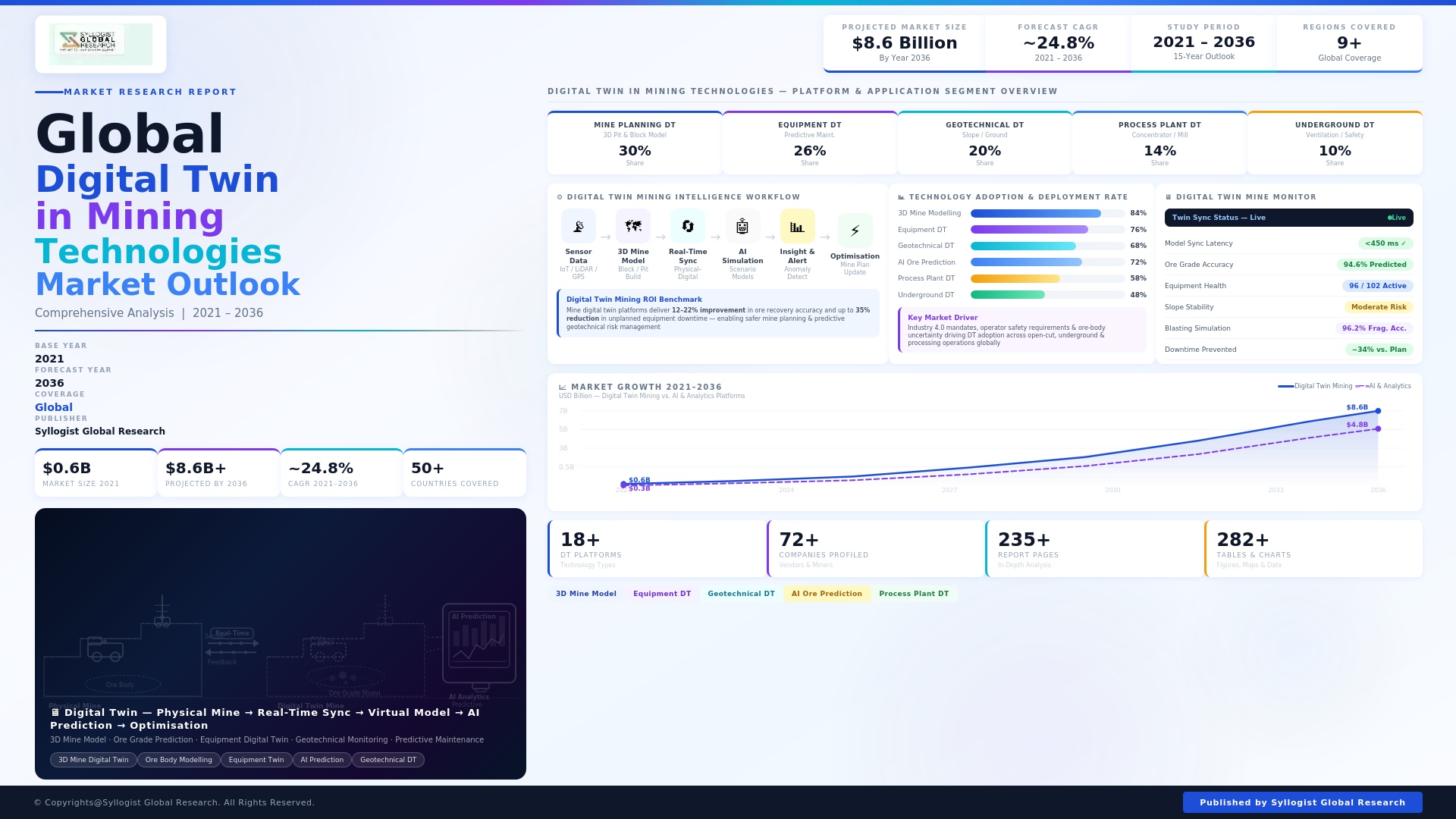

The global digital twin technologies in mining market was valued at approximately USD 2.1 billion in 2025 and is projected to reach USD 7.8 billion by 2034, advancing at a compound annual growth rate of 15.7% over the forecast period from 2027 to 2034, driven by the mining industry’s intensifying imperative to improve capital productivity, reduce operational costs, enhance worker safety, and accelerate the transition to autonomous and remotely operated mining operations across an asset base whose increasing geological complexity, ore grade decline, and deeper mine development are driving up production costs at rates that only systematic digitalization can offset. The adoption of digital twin technology in mining is transitioning from isolated pilot program implementations at flagship operations toward systematic enterprise-scale deployment across major mining company asset portfolios, as the demonstrable return on investment achieved by early adopters in terms of equipment availability improvement, energy consumption reduction, processing plant throughput optimization, and unplanned downtime elimination creates the internal business case validation required for broader capital allocation approval across mid-tier and smaller mining operations globally.

Processing plant digital twins represent the most commercially mature and highest-return application segment within the mining digital twin market, with comminution circuit optimization twins delivering documented energy consumption reductions of 6% to 12% per tonne of ore processed, throughput improvements of 4% to 9%, and grinding media consumption reductions of 8% to 15% at operations where high-fidelity dynamic simulation models of crushing, grinding, classification, and flotation circuits are continuously calibrated against real-time process measurements and used to generate model-predictive control setpoints that conventional regulatory control systems cannot achieve. Autonomous mining equipment fleets, encompassing autonomous haulage systems, automated drilling rigs, and remotely operated underground load-haul-dump machines, are generating rapidly expanding demand for equipment-level digital twins that model the physical and operational state of individual machines in real time, enabling predictive maintenance interventions based on component degradation models calibrated against fleet-wide operating data, route optimization algorithms informed by continuously updated pit or drive condition models, and remote supervision interfaces that allow certified operators to monitor and override multiple autonomous machines simultaneously from operations control centres thousands of kilometres from the physical mine site. Underground mine digital twins integrating real-time geotechnical monitoring, ventilation system modelling, production scheduling simulation, and personnel and equipment location tracking are advancing from research-stage demonstration toward commercial deployment at hard rock underground operations in Australia, Canada, and Scandinavia, where the safety, productivity, and energy management benefits of integrated underground mine twins are most clearly quantifiable and where the regulatory and workforce environments are most conducive to digital technology adoption at scale.

The geographic concentration of digital twin technology adoption in mining follows the distribution of technologically progressive mining companies and the regulatory environments most actively incentivising mining digitalization, with Australia emerging as the world’s most advanced national market for mining digital twin deployment, driven by the combination of the country’s large autonomous equipment fleet base, the Minerals Council of Australia’s industry digitalization programs, proximity to leading mining technology vendors, and the operational imperative to reduce labour costs in remote locations that has made autonomous and remotely operated mining a strategic priority for Australian iron ore, coal, gold, and lithium producers. North America, led by Canadian and American base metal and gold mining operations, represents the second-largest regional market, with adoption driven by deep underground metal mine safety improvement requirements, energy cost management imperatives at energy-intensive processing operations, and the active digital mining programs of major copper and gold producers whose corporate sustainability commitments include quantified energy efficiency and greenhouse gas reduction targets that digital twin-enabled operational optimization contributes to achieving. Latin America’s copper mining industry, concentrated in Chile and Peru, is generating significant digital twin investment driven by the operational complexity and energy intensity of large-scale porphyry copper mining and processing operations where marginal improvements in comminution efficiency and concentrator recovery deliver substantial revenue impact at scale, with Chilean copper producers having invested approximately USD 340 million in digital operational technology programs across their operations in the three years preceding 2025.

Geological and resource model digital twins, which integrate borehole assay data, geophysical survey results, structural geological interpretation, and geostatistical modelling within continuously updated three-dimensional geological models that evolve in real time as new drilling and production data are incorporated, are emerging as a strategically important application segment that extends digital twin value from operational optimization into the exploration, resource estimation, and mine planning domains where improved geological model fidelity directly improves reserve classification confidence, reduces exploration capital risk, and enables more precise mine design and production scheduling optimization. The integration of artificial intelligence and machine learning capabilities within mining digital twin platforms is expanding the analytical value delivered beyond deterministic physics-based simulation toward probabilistic scenario analysis, anomaly detection, and autonomous optimization recommendation systems that can process the scale of sensor data generated by large mining operations, typically exceeding one terabyte of operational data per day at a major processing complex, at speeds and analytical depths that human operators and conventional data analysis workflows cannot achieve. Battery and energy storage system digital twins for electrified mining equipment fleets, including battery electric haul trucks, underground battery electric vehicles, and mine-site renewable energy and storage microgrid systems, represent an emerging application sub-segment growing at approximately 22.4% annually as the mining industry’s transition from diesel-powered equipment toward electrified and hydrogen-powered alternatives creates new asset monitoring, energy management, and predictive degradation modelling requirements that dedicated digital twin systems are being developed to address.

Key Drivers

Autonomous Mining Equipment Proliferation and Remote Operations Centre Development Creating Structural Digital Twin Integration Demand Across Global Mining Operations

The accelerating deployment of autonomous haulage systems, automated drilling equipment, and remotely operated underground mining machines across global mining operations is creating a structural and non-optional requirement for equipment-level and site-level digital twin systems that provide the real-time asset state awareness, predictive maintenance intelligence, and simulation-based fleet optimization capability that autonomous mining operations require to achieve their safety and productivity objectives without direct human presence at the machine. Global autonomous haulage system deployments exceeded 830 units across iron ore, copper, coal, and oil sands operations in 2025, with the fleet projected to surpass 1,800 units by 2034 as mid-tier mining companies follow the lead of early-adopting majors in commissioning autonomous truck fleets at new and retrofitted open pit operations, each autonomous vehicle requiring digital twin support for health monitoring, route optimization, and interaction management with other autonomous and manually operated equipment in mixed-fleet environments. The development of integrated remote operations centres, where geographically dispersed mining operations are monitored and optimized by centralized teams of specialists, requires enterprise-level digital twin platforms that aggregate real-time operational data from multiple mine sites into unified visualization and decision support environments, with the remote operations model generating efficiency benefits including labour productivity improvement, specialist expertise leverage across multiple assets, and 24-hour operational continuity that justify the digital infrastructure investment required to implement high-fidelity site twins across entire mining company asset portfolios.

Energy Transition Imperatives and Greenhouse Gas Emission Reduction Commitments Driving Digital Twin Adoption for Mining Energy Management and Decarbonisation Optimization

The mining industry’s growing exposure to carbon pricing mechanisms, scope one and scope two greenhouse gas emission reduction commitments embedded in corporate climate strategies, and the energy cost management imperative driven by electricity and diesel price volatility are creating a powerful commercial driver for digital twin-enabled energy optimization across the highly energy-intensive mining and mineral processing operations that collectively account for approximately 2% to 3% of global primary energy consumption and represent one of the most significant operational cost and carbon footprint management challenges in the industry. Comminution operations, encompassing crushing and grinding circuits at processing plants, consume approximately 36% of total mining industry electricity consumption globally, making the deployment of dynamic process simulation digital twins that optimize comminution circuit operating parameters for minimum specific energy consumption per tonne of product the single highest-return digital twin investment category available to mining companies pursuing simultaneous cost reduction and carbon footprint improvement objectives. Mine ventilation systems at underground hard rock operations represent the second-largest energy consumption category, accounting for approximately 40% to 50% of total underground mine energy consumption, with ventilation-on-demand digital twin systems that model real-time air quality, personnel location, equipment emission sources, and airflow distribution enabling ventilation fan speed optimization that reduces ventilation energy consumption by 25% to 45% relative to fixed-schedule ventilation operation, delivering annual energy cost savings of USD 2 million to USD 8 million per underground mine depending on mine size and current ventilation operating practices.

Ore Grade Decline, Increasing Mining Depth, and Geological Complexity Escalating the Value of Simulation-Based Planning and Operational Optimization Digital Twins

The structural deterioration of global ore grades across copper, gold, and base metal deposits, the progressive deepening of underground mining operations as shallow high-grade resources are depleted, and the increasing geological and geotechnical complexity of the ore bodies being developed are collectively escalating the operational and capital productivity challenges confronting the global mining industry in ways that create compelling and quantifiable economic justification for digital twin investment whose returns are most significant precisely at the complex, deep, and low-grade operations where conventional operational management approaches are least adequate. Global average copper ore grades have declined from approximately 1.2% copper in 2000 to approximately 0.65% in 2025, requiring the processing of progressively larger volumes of ore to produce equivalent metal output, placing an increasing premium on processing plant optimization digital twins that can extract the maximum recoverable metal from each tonne of ore processed through continuous real-time optimization of flotation circuit performance, reagent addition control, and grind size management. Underground mine digital twins that integrate real-time geotechnical monitoring data from ground movement sensors, extensometers, and microseismic networks with continuum and discrete element geomechanical simulation models are delivering measurable safety and productivity improvements at deep underground metal mines by providing advance warning of ground instability conditions, optimizing support installation schedules, and enabling the recovery of ore from ground conditions that would otherwise be declared unsafe under conservative empirical ground support design approaches based on static geotechnical models.

Key Challenges

Data Integration Complexity, Legacy System Incompatibility, and Operational Technology Cybersecurity Risk Constraining Mining Digital Twin Implementation

The implementation of high-fidelity digital twin systems across mining operations is fundamentally constrained by the complexity of integrating real-time data from heterogeneous operational technology environments comprising decades-old process control systems, multiple generations of equipment monitoring platforms from different original equipment manufacturers, proprietary mine planning software with limited application programming interface connectivity, and bespoke geological modelling tools whose data schemas are incompatible with modern cloud-based digital twin platform architectures, creating data integration challenges that require substantial software engineering investment and specialized industrial data integration expertise before meaningful digital twin functionality can be delivered. The coexistence of operational technology systems controlling physical mining and processing equipment with the information technology networks required to operate digital twin platforms creates cybersecurity vulnerability surfaces whose exploitation could result in physical equipment damage, production disruption, or safety system compromise, with the mining industry having experienced a significant increase in targeted ransomware attacks against operational technology infrastructure since 2020, compelling mining operators to implement network segmentation, access control, and continuous monitoring measures that constrain the real-time data connectivity required for high-fidelity digital twin operation and require substantial cybersecurity investment as a prerequisite for digital twin deployment. The absence of industry-wide data standardization for mining equipment telemetry, geological data exchange, and process measurement formats means that digital twin implementations at multi-vendor equipment environments require bespoke data translation, normalization, and quality management infrastructure whose development and maintenance cost is frequently underestimated in digital twin project business cases, contributing to implementation delays and budget overruns that damage organizational confidence in digital twin investment returns.

Skilled Workforce Shortage in Mining Data Science, Digital Twin Engineering, and Operational Technology Integration Limiting Deployment Capacity and Value Realization

The successful deployment and sustained value realization of mining digital twin systems requires a workforce combining deep mining domain expertise with advanced competencies in data science, machine learning, physics-based simulation, industrial Internet of Things integration, and cloud platform engineering, a combination of skills that is acutely scarce globally and represents one of the most significant practical constraints on the pace at which mining companies can implement, operate, and extract value from digital twin investments across their asset portfolios. Mining companies report that the difficulty of attracting and retaining data scientists, digital twin engineers, and operational technology integration specialists with mining domain knowledge is among their top three digital transformation constraints, with competition for these professionals from technology industry employers offering superior compensation packages, more flexible working conditions, and more varied career development opportunities than the remote mine site locations and hierarchical organizational structures characteristic of traditional mining company employment environments. The organizational change management requirement associated with digital twin adoption, including retraining operational personnel to interpret and act on digital twin insights, redesigning workflows to incorporate simulation-based decision support tools, and building the trust among experienced mining engineers and operators required for them to rely on model-generated recommendations rather than intuition and experience, represents a sustained investment in human capability development that typically extends over three to five years per operation and whose neglect is the most common cause of digital twin implementations that deliver technical functionality but fail to generate the operational improvement outcomes that justified the initial investment.

Connectivity Infrastructure Limitations at Remote Mining Sites and the High Cost of Real-Time Data Transmission in Geographically Isolated Operations

The operational value of mining digital twins is directly proportional to the frequency, completeness, and latency of the real-time data streams that synchronize the virtual model with its physical counterpart, creating a fundamental dependency on communications infrastructure whose adequacy at remote and underground mining locations is frequently insufficient for the data transmission requirements of production-grade digital twin systems without substantial and costly connectivity infrastructure investment that is not always commercially justified by the scale of individual mining operations. Underground mines present particularly challenging connectivity environments, where the radio frequency propagation characteristics of rock mass create coverage gaps, signal attenuation, and bandwidth limitations that constrain the density of wireless sensor networks and equipment telemetry systems whose data is required to synchronize underground equipment, geotechnical, and ventilation digital twins at the update frequencies required for real-time operational decision support. Remote open pit and surface mining operations in geographically isolated locations across Western Australia, the Atacama region of Chile, northern Canada, and Central Africa face high-latency and limited-bandwidth satellite communications constraints that restrict the volume of raw sensor data that can be transmitted to cloud-hosted digital twin platforms in real time, requiring edge computing architectures that perform local data processing and model computation at the mine site before transmitting compressed results to central platforms, adding architectural complexity and capital cost to digital twin implementations that must function effectively within the connectivity envelope achievable at specific mine locations without the benefit of the high-bandwidth fibre or terrestrial cellular infrastructure available at industrially developed locations.

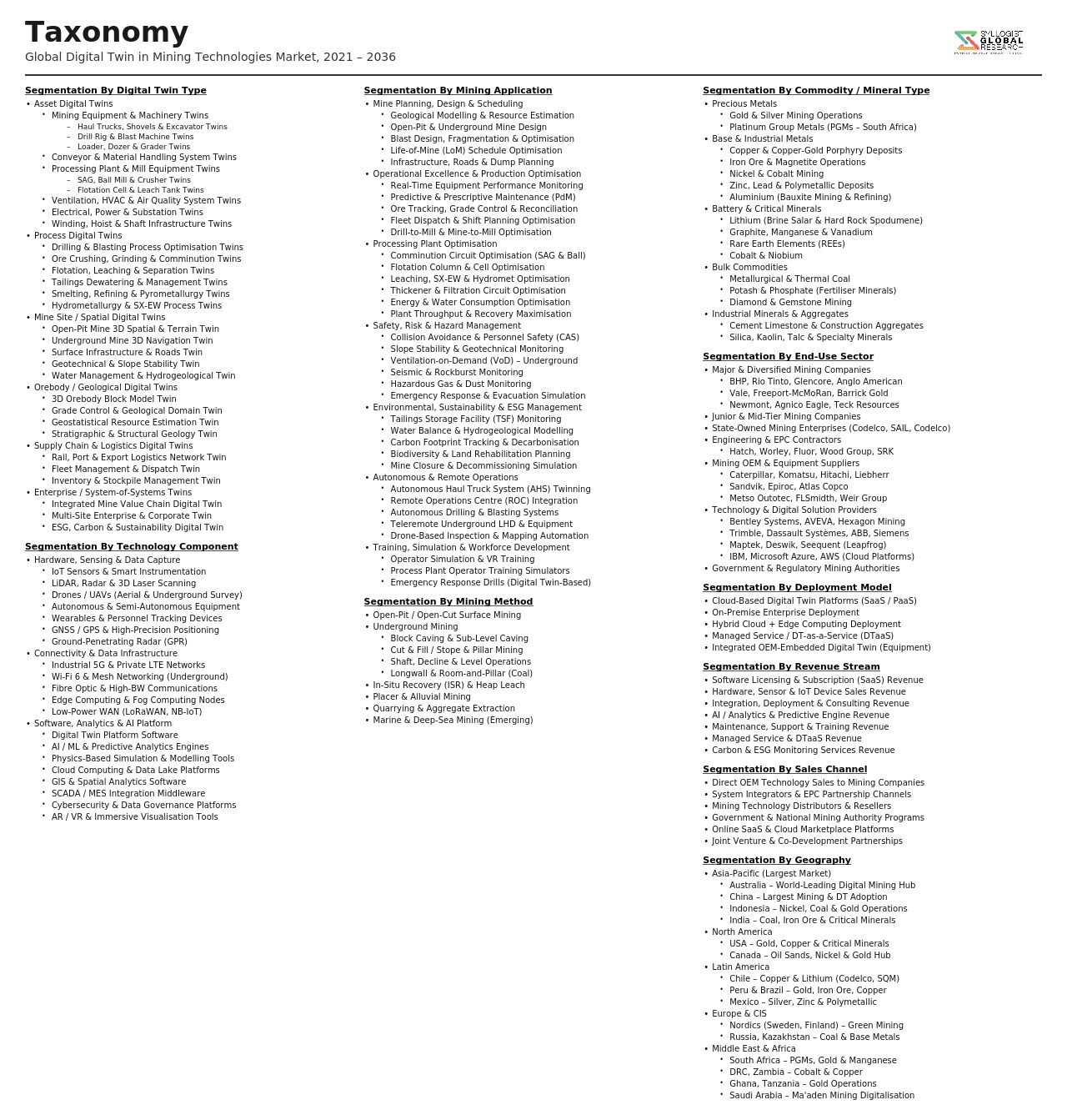

Market Segmentation

- Segmentation By Application Type

- Geological and Resource Model Digital Twins

- Mine Planning and Production Scheduling Simulation Twins

- Processing Plant and Comminution Circuit Optimization Twins

- Equipment Health Monitoring and Predictive Maintenance Twins

- Autonomous and Remote Mining Operations Twins

- Underground Ventilation and Environmental Management Twins

- Geotechnical Monitoring and Ground Stability Twins

- Tailings and Waste Management Twins

- Mine Closure and Rehabilitation Planning Twins

- Others

- Segmentation By Mining Type

- Open Pit Surface Mining

- Underground Hard Rock Mining

- Underground Coal Mining

- Placer and Alluvial Mining

- In-Situ Leach and Solution Mining

- Offshore and Seabed Mining

- Others

- Segmentation By Commodity

- Copper

- Gold and Silver

- Iron Ore

- Coal (Thermal and Metallurgical)

- Battery Metals (Lithium, Cobalt, and Nickel)

- Potash and Fertilizer Minerals

- Diamonds and Precious Stones

- Bauxite and Aluminium

- Others

- Segmentation By Technology Component

- Three-Dimensional Geological Modelling and Visualization Software

- Physics-Based Process Simulation and Dynamic Modelling Platforms

- Industrial Internet of Things Sensor Networks and Edge Computing

- Artificial Intelligence and Machine Learning Analytics Engines

- Cloud Computing Infrastructure and Digital Twin Platform Services

- Autonomous Equipment Integration and Fleet Management Systems

- Real-Time Data Integration Middleware and Operational Technology Connectors

- Augmented and Virtual Reality Visualization Interfaces

- Others

- Segmentation By Deployment Model

- On-Premise Deployment

- Cloud-Hosted Software-as-a-Service

- Hybrid On-Premise and Cloud Deployment

- Edge Computing and Distributed Architecture Deployment

- Segmentation By End User

- Large Diversified Mining Majors

- Mid-Tier Mining Companies

- Junior and Exploration Stage Mining Companies

- State-Owned National Mining Enterprises

- Engineering, Procurement, and Construction Contractors

- Mining Technology and Software Vendors

- Others

- Segmentation By Value Chain Stage

- Exploration and Resource Delineation

- Mine Feasibility and Design

- Active Mining Operations

- Mineral Processing and Beneficiation

- Tailings and Environmental Management

- Mine Closure and Rehabilitation

- Segmentation By Region

- Asia-Pacific (Australia, China, Indonesia, and Others)

- Latin America (Chile, Peru, Brazil, and Others)

- North America (United States and Canada)

- Europe (Scandinavia, Finland, and Eastern Europe)

- Middle East and Africa (South Africa, Democratic Republic of Congo, and Others)

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of Digital Twin Technologies in Mining in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by application type, geological modelling, processing plant optimization, equipment health monitoring, autonomous operations, and environmental management, by mining commodity, copper, gold, iron ore, coal, lithium, and others, and by deployment model, on-premise, cloud-hosted, and hybrid, to enable mining technology vendors, mining companies, investors, and equipment manufacturers to identify which application segments and commodity markets will generate the highest absolute revenue and most commercially significant technology adoption momentum across the forecast period?

- How is the proliferation of autonomous haulage systems, automated drilling equipment, and remotely operated underground mining machinery expected to drive digital twin platform investment and vendor competitive positioning through 2034, which digital twin technology components, equipment health monitoring, fleet optimization simulation, and remote operations visualization, are generating the highest return on investment at currently operating autonomous mining deployments, and what are the projected digital twin software and services revenue streams associated with the global autonomous mining equipment fleet expansion forecast to exceed 1,800 units by 2034?

- What is the projected commercial trajectory of artificial intelligence and machine learning integration within mining digital twin platforms through 2034, encompassing predictive maintenance model performance improvement, real-time process optimization recommendation systems, geological anomaly detection, and autonomous control loop integration, which mining application segments are generating the most commercially significant artificial intelligence-augmented digital twin value propositions, and how are the leading mining digital twin platform vendors differentiating their artificial intelligence capabilities relative to point-solution competitors and general-purpose industrial digital twin platforms seeking to enter the mining vertical?

- How are mining industry greenhouse gas emission reduction commitments, carbon pricing exposure, and energy cost management imperatives expected to shape digital twin investment priorities, specifically in comminution circuit energy optimization, ventilation-on-demand underground management, electrified equipment fleet energy modelling, and mine-site renewable energy and storage microgrid optimization, through 2034, and what are the quantified energy cost savings and carbon emission reduction outcomes that mining digital twin deployments in these application categories are delivering at currently operating reference sites across Australia, Chile, Canada, and Scandinavia?

- Who are the leading mining digital twin technology platform vendors, industrial automation and control system providers, mining software specialists, cloud infrastructure providers, and mining original equipment manufacturers integrating digital twin capability into connected equipment offerings, and what are their respective product portfolio breadth across geological, operational, equipment, and environmental twin application categories, customer reference site deployments and documented operational improvement outcomes, partnership and ecosystem development strategies, research and development investment in physics-based simulation and artificial intelligence integration, and competitive positioning responses to the data integration complexity, workforce capability, and connectivity infrastructure challenges constraining mining digital twin adoption across the global mining industry through 2034?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Data Security, Cybersecurity & Digital Infrastructure Risk

- Technology Integration, Interoperability & Legacy System Risk

- Regulatory, Permitting & Mining Compliance Risk

- Operational Disruption, Connectivity & Remote Site Risk

- Financing, ROI Uncertainty & Implementation Risk

- Regulatory Framework & Standards

- Mining Safety Regulations & Digital Monitoring Compliance Frameworks

- Environmental Monitoring, Emissions Reporting & Regulatory Digital Requirements

- Data Sovereignty, Cross-Border Data Transfer & Mining Data Governance Standards

- Cybersecurity Standards & Critical Infrastructure Protection Regulations for Mining

- Green Mining, ESG Disclosure & Sustainability Reporting Standards

- Global Digital Twin Technologies in Mining Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Number of Deployments & Licenses)

- Market Size & Forecast by Component

- Software Platforms & Simulation Engines

- Hardware (Sensors, IoT Devices & Edge Computing)

- Services (Integration, Implementation & Managed Services)

- Market Size & Forecast by Technology

- 3D Modelling & Geological Simulation

- AI & Machine Learning-Enabled Predictive Analytics

- IoT & Real-Time Sensor Data Integration

- Cloud & Edge Computing Platforms

- Augmented Reality (AR) & Virtual Reality (VR) Integration

- GIS & Spatial Intelligence Platforms

- Autonomous Equipment & Robotics Integration

- Market Size & Forecast by Mining Type

- Surface Mining (Open Pit & Strip Mining)

- Underground Mining

- In-Situ Leaching & Solution Mining

- Offshore & Seabed Mining

- Market Size & Forecast by Application

- Mine Planning & Geological Modelling

- Asset Performance Monitoring & Predictive Maintenance

- Workforce Safety & Remote Operations Management

- Environmental Monitoring & Tailings Management

- Production Optimisation & Process Simulation

- Energy & Water Management

- Supply Chain & Logistics Optimisation

- Market Size & Forecast by Mineral Segment

- Coal Mining

- Iron Ore Mining

- Copper Mining

- Gold Mining

- Lithium & Battery Minerals Mining

- Potash & Fertiliser Minerals Mining

- Other Metals & Industrial Minerals

- Market Size & Forecast by End-User

- Large-Scale Mining Corporations

- Mid-Tier & Junior Mining Companies

- Mining Equipment, Technology & Services (METS) Companies

- Government & Regulatory Mining Authorities

- Market Size & Forecast by Sales Channel

- Direct Sales & Enterprise Licensing

- System Integrators & Technology Partners

- Cloud Marketplace & SaaS Subscription

- Managed Service & Outcome-Based Contracts

- North America Digital Twin Technologies in Mining Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Deployments & Licenses)

- By Component

- By Technology

- By Mining Type

- By Application

- By Mineral Segment

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Digital Twin Technologies in Mining Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Deployments & Licenses)

- By Component

- By Technology

- By Mining Type

- By Application

- By Mineral Segment

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Digital Twin Technologies in Mining Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Deployments & Licenses)

- By Component

- By Technology

- By Mining Type

- By Application

- By Mineral Segment

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Digital Twin Technologies in Mining Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Deployments & Licenses)

- By Component

- By Technology

- By Mining Type

- By Application

- By Mineral Segment

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Digital Twin Technologies in Mining Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Deployments & Licenses)

- By Component

- By Technology

- By Mining Type

- By Application

- By Mineral Segment

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Digital Twin Technologies in Mining Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Deployments & Licenses)

- By Component

- By Technology

- By Mining Type

- By Application

- By Mineral Segment

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- *Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Italy, Norway, Sweden, China, Japan, India, Australia, South Korea, Singapore, Brazil, Chile, Saudi Arabia, UAE, Egypt, South Africa, Israel

- Technology Landscape & Innovation Analysis

- 3D Geological Modelling & Mine Simulation Platform Technology Deep-Dive

- AI-Powered Predictive Maintenance & Asset Performance Digital Twin Technology

- IoT Sensor Networks, Edge Computing & Real-Time Data Integration Technology

- Autonomous & Semi-Autonomous Equipment Integration with Digital Twin Platforms

- AR/VR & Immersive Visualisation Technology for Mining Operations

- Environmental & Tailings Digital Monitoring Platform Technology

- Cloud-Native & Hybrid Digital Twin Architecture & Cybersecurity Technology

- Patent & IP Landscape in Digital Twin Technologies for Mining

- Value Chain & Supply Chain Analysis

- Digital Twin Software Development & Platform Provider Supply Chain

- Hardware, Sensor & IoT Device Manufacturing Supply Chain

- Telecommunications & Connectivity Infrastructure Supply Chain for Mining

- System Integrator, Implementation Partner & Consulting Services Channel

- Mining Equipment OEM & Original Technology Provider Channel

- Cloud & Data Centre Infrastructure Provider Channel

- Mining Operator & End-User Procurement & Decision-Making Channel

- Pricing Analysis

- Digital Twin Platform Licensing & Subscription Pricing Analysis

- Hardware, Sensor & IoT Device Capital Cost Analysis

- Implementation, Integration & Professional Services Cost Analysis

- Managed Service & Outcome-Based Contract Pricing Analysis

- Total Cost of Ownership (TCO) & ROI Analysis for Mining Digital Twin Deployments

- SaaS vs. On-Premise vs. Hybrid Deployment Cost Comparison Analysis

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Digital Twin Technology Deployments in Mining: Carbon Footprint, Energy Consumption & Electronic Waste

- Digital Twin Contribution to Carbon Neutrality & Net Zero Mining Targets: Emissions Monitoring & Reduction Pathway

- Environmental Monitoring, Tailings Risk Reduction & Ecosystem Protection Enabled by Digital Twin Technology

- Energy & Water Efficiency Gains Achieved Through Digital Twin Optimisation in Mining Operations

- Regulatory-Driven Sustainability, SDG Alignment & ESG Reporting Enabled by Digital Twin Platforms

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Component, Technology & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Component, Technology & Geography

- Player Classification

- Integrated Mining Technology & Digital Twin Platform Companies

- Specialist Geological Modelling & Mine Simulation Software Providers

- Industrial IoT & Asset Performance Management Platform Providers

- Cloud, AI & Data Analytics Companies Serving Mining

- Mining Equipment OEMs with Integrated Digital Twin Capabilities

- System Integrators & Implementation Partners Specialising in Mining Digital Transformation

- Telecommunications & Connectivity Infrastructure Providers for Mining

- Competitive Analysis Frameworks

- Market Share Analysis by Component, Technology & Region

- Company Profile

- Company Overview & Headquarters

- Digital Twin Products & Technology Portfolio for Mining

- Key Customer Relationships & Reference Mining Project Installations

- R&D Investment & Innovation Pipeline

- Revenue (Mining Digital Twin Segment) & Contracted Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Product Launches, Capacity Expansion)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Component, Technology, Application, Mineral Segment & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output