Market Definition

The India Propylene and Polypropylene Market encompasses the production, import, trade, processing, and end-use consumption of propylene monomer and polypropylene resin across the full petrochemical value chain operating within India, including propylene generation from steam crackers, fluid catalytic cracking units, propane dehydrogenation plants, and on-purpose propylene production routes; the polymerization of propylene monomer into polypropylene homopolymer, random copolymer, and impact copolymer resin grades at domestic polymer manufacturing facilities; the import of propylene and polypropylene from international producers to supplement domestic production shortfalls; and the downstream conversion of polypropylene resin into packaging, automotive components, textiles, healthcare products, consumer goods, pipes, and industrial applications by Indian plastics processing enterprises.

Propylene is a gaseous olefin produced as a co-product of ethylene steam cracking of naphtha and liquefied petroleum gas feedstocks, as a significant refinery by-product from fluid catalytic cracking operations at Indian petroleum refineries, and as the primary product of dedicated propane dehydrogenation facilities that convert liquefied petroleum gas propane into chemical-grade propylene for polymer and derivative production. Polypropylene, produced by Ziegler-Natta or metallocene catalytic polymerization of propylene, is a semi-crystalline thermoplastic resin whose combination of low density, excellent chemical resistance, high stiffness-to-weight ratio, thermal processability, and cost competitiveness relative to alternative engineering plastics has established it as the second most widely consumed synthetic polymer globally and the most versatile commodity plastic in India’s domestic consumption mix. The market encompasses all polypropylene grades produced and consumed in India including injection molding grades for rigid packaging, automotive, and consumer goods applications; film grades for biaxially oriented polypropylene packaging and cast film applications; fiber and filament grades for woven sacks, nonwovens, and textile applications; pipe grades for pressurized piping systems; and specialty compounded and filled grades for engineering and automotive applications. Key participants include Reliance Industries, ONGC Petro Additions, Haldia Petrochemicals, and HPCL-Mittal Energy as domestic producers; international polypropylene exporters from the Middle East, South Korea, China, and Southeast Asia as import supply sources; and the large and diverse Indian plastics processing industry as the primary demand-side participant.

Market Insights

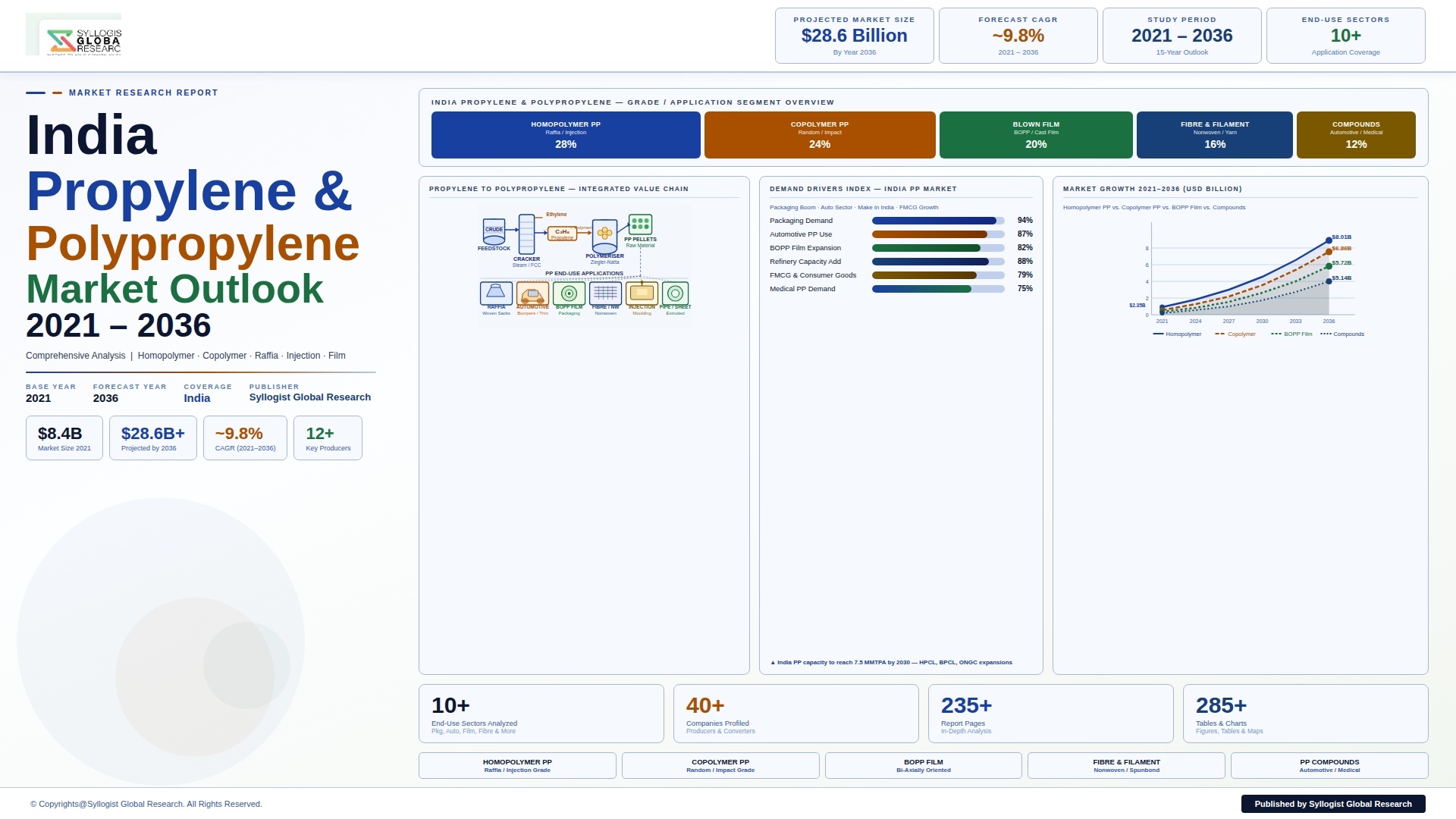

The India propylene and polypropylene market is experiencing a structurally favorable demand environment rooted in India’s expanding manufacturing economy, rising domestic consumption across packaging, automotive, infrastructure, and consumer goods sectors, and the government’s Make in India and PLI scheme initiatives that are progressively attracting both domestic and foreign manufacturing investment into industries that are significant polypropylene consumers. India’s total polypropylene consumption reached approximately 6.8 million metric tonnes in 2025, making it the third-largest polypropylene consuming country globally after China and the United States, and total domestic polypropylene demand is projected to reach approximately 10.6 million metric tonnes by 2034, advancing at a compound annual growth rate of 5.1% over the forecast period from 2027 to 2034. The India propylene and polypropylene market was valued at approximately USD 8.9 billion in 2025 and is projected to reach USD 14.7 billion by 2034, driven by the accelerating growth of flexible and rigid packaging demand from India’s FMCG, food processing, and e-commerce sectors, the ongoing substitution of metal, glass, and paper materials by polypropylene in automotive, appliance, and industrial applications, and the expansion of domestic polypropylene production capacity as Reliance Industries and new entrant producers commission additional polymerization capacity at their integrated petrochemical complexes.

The structural supply-demand imbalance in the Indian polypropylene market, where domestic production capacity has consistently fallen short of the rapidly growing demand generated by India’s downstream plastics processing industry, has made India one of the world’s largest polypropylene importing nations, with net imports of approximately 2.1 million metric tonnes in fiscal year 2024-25 representing approximately 31% of total domestic polypropylene consumption and sourced predominantly from Saudi Arabia, South Korea, United Arab Emirates, Singapore, and China at prices benchmarked to Asian polymer market quotations. The import dependency of the Indian polypropylene market creates a structural foreign exchange expenditure burden and exposes domestic converter industries to global supply chain disruptions, freight cost volatility, and price fluctuations driven by Asian petrochemical market dynamics that are only partially correlated with Indian domestic demand and production cost conditions. Reliance Industries’ Jamnagar integrated petrochemical complex, which operates the largest single-site polypropylene production capacity in India at approximately 2.4 million metric tonnes per year across its two Jamnagar sites, dominates the domestic supply landscape and benefits from the deep integration of propylene supply from the Jamnagar refinery’s FCC units with the adjacent polypropylene polymerization trains, enabling a highly cost-competitive production economics structure that no other Indian producer has been able to replicate at equivalent scale. ONGC Petro Additions’ OPaL complex at Dahej, with a polypropylene capacity of approximately 340,000 metric tonnes per year, and Haldia Petrochemicals’ West Bengal facilities contribute to domestic supply alongside the propylene and polypropylene production from HPCL-Mittal Energy’s Guru Gobind Singh Refinery at Bathinda, but the aggregate domestic capacity from these producers remains substantially below the demand level that India’s polymer processing industry requires, sustaining the structural import requirement.

The packaging segment is the dominant end-use application for polypropylene in India, accounting for approximately 43% of total domestic polypropylene consumption in 2025, and encompasses a wide spectrum of packaging formats including woven polypropylene sacks for cement, fertilizer, grain, and sugar packaging; biaxially oriented polypropylene films for food, snack, biscuit, and confectionery flexible packaging; cast polypropylene films for lamination and overwrapping; rigid polypropylene containers and closures for food, beverage, and personal care packaging; and thermoformed trays and cups for dairy, prepared food, and foodservice applications. India’s food processing sector, which is growing at approximately 8% annually and has attracted over USD 33 billion in foreign direct investment over the past decade under government food processing promotion initiatives, is a primary driver of polypropylene flexible and rigid packaging demand growth, with increasing per capita processed food consumption, expanding organized retail channels, and the formalization of India’s food supply chain progressively increasing the polypropylene packaging intensity per unit of food consumed. The nonwoven polypropylene segment is experiencing above-average growth at approximately 9.4% annually following the dramatic acceleration in Indian healthcare infrastructure investment post the COVID-19 pandemic, which exposed India’s critical dependence on polypropylene spunbond and meltblown nonwovens for personal protective equipment, surgical gowns, face masks, and hygiene products and catalyzed domestic production capacity investment that is now serving both domestic healthcare demand and export markets across Asia, Africa, and the Middle East.

The automotive and infrastructure segments represent the most technically sophisticated polypropylene consumption categories in the Indian market, collectively accounting for approximately 24% of total polypropylene demand in 2025 and growing at above-average rates driven by the expansion of domestic vehicle production, the PLI scheme for automotive and advanced chemistry cell battery manufacturing attracting new entrant vehicle manufacturers, and the substantial public infrastructure investment under the National Infrastructure Pipeline that is generating demand for polypropylene pipes, fittings, and geotextile applications across water supply, irrigation, drainage, and road construction projects. The Indian automotive sector produced approximately 5.1 million passenger vehicles and 1.0 million commercial vehicles in fiscal year 2024-25, with modern vehicle platforms incorporating 8 to 15 kilograms of polypropylene per vehicle in bumper fascias, instrument panels, door trims, underbody shields, and fluid reservoir components, and the progressive tightening of vehicle emission and fuel efficiency standards incentivizing the substitution of heavier metal components with lightweight polypropylene composites and long glass fiber reinforced polypropylene structural components that are expanding polypropylene content per vehicle. The Jal Jeevan Mission and AMRUT 2.0 urban water supply programs are generating substantial demand for polypropylene random copolymer pressure pipes and fittings in potable water distribution applications, with the superior chlorine resistance, low thermal conductivity, and smooth bore flow efficiency of polypropylene pipe systems making them the preferred specification in new water supply infrastructure projects across both urban and rural program geographies.

Key Drivers

India’s Manufacturing Sector Expansion and PLI Scheme Investment Generating Broad-Based Polypropylene Demand Across Multiple End-Use Industries

The Indian government’s Production Linked Incentive scheme, which has committed over INR 1.97 lakh crore in incentive disbursements across fourteen manufacturing sectors including electronics, pharmaceuticals, food processing, textiles, advanced chemistry cells, and automotive components, is catalyzing a structural expansion of India’s manufacturing production base that directly generates growing polypropylene demand across packaging, automotive, appliances, healthcare, and industrial applications as new manufacturing facilities commission production lines whose packaging, component, and infrastructure material requirements include substantial polypropylene consumption. The Make in India initiative’s success in attracting electronics manufacturing investment from Apple, Samsung, and their component supplier ecosystems, pharmaceutical manufacturing capacity expansion from both domestic and international producers targeting India’s position as the pharmacy of the world, and the growth of India’s FMCG manufacturing from both domestic companies and multinational consumer goods producers expanding their Indian production footprint are collectively generating a compounding demand growth dynamic for polypropylene packaging materials, consumer goods components, and industrial applications that is structurally linked to India’s manufacturing GDP growth trajectory rather than dependent on any single sector’s performance. The formalization of India’s retail and consumer supply chain, the expansion of organized grocery retail from the current penetration level of approximately 12% toward an estimated 25% to 30% over the next decade, and the growth of e-commerce packaging requirements generating approximately 5.4 billion polypropylene-intensive packaging units annually from Indian e-commerce shipments are additional demand growth vectors whose compounding effect on polypropylene consumption is structurally tied to India’s consumption economy development rather than being easily reversed by short-term economic fluctuations.

Rapid Growth of India’s Food Processing and FMCG Sectors Accelerating Polypropylene Flexible and Rigid Packaging Consumption

India’s food processing industry, which processes approximately 10% of total agricultural output today compared to 30% to 40% in developed economies, is on a sustained expansion trajectory driven by rising household income levels, increasing urbanization, the growth of nuclear family structures demanding convenience food formats, and the government’s SAMPADA and PLI for food processing schemes that are stimulating investment in food manufacturing capacity across dairy, snack foods, packaged beverages, edible oils, ready-to-eat meals, and confectionery segments, all of which are intensive consumers of polypropylene flexible films, rigid containers, closures, and thermoformed packaging components that are growing their Indian demand base at rates of 8% to 12% annually across specific application segments. The organized dairy sector expansion, including Amul’s capacity investment program targeting INR 5,000 crore in dairy processing infrastructure and the multinational dairy companies including Nestle, Danone, and Lactalis expanding their Indian production footprints, is generating growing demand for polypropylene pails, pouches, closure systems, and crate applications that are standard packaging formats for Indian dairy products distributed through ambient, chilled, and frozen supply chain configurations. The growth of India’s quick service restaurant sector, institutional food service, and ready-to-eat food segments is expanding demand for thermoformed polypropylene trays, clamshell containers, cups, and cutlery whose production has attracted several new domestic thermoforming investment programs targeting the gap between current domestic production capacity and the rapidly growing organized food service market requirement, creating a self-reinforcing demand cycle for polypropylene food contact grades that is growing above the overall polypropylene market average rate.

Announced Domestic Polypropylene Capacity Additions and Petrochemical Integration Investments Progressively Reducing India’s Structural Import Dependency

The significant and commercially consequential gap between India’s domestic polypropylene production capacity and its rapidly growing consumption requirement, which has sustained net import volumes of over two million metric tonnes annually and created a structural foreign exchange expenditure burden, is attracting new domestic capacity investment commitments from both existing Indian petrochemical producers and new entrant investors who recognize the commercial opportunity presented by India’s large and growing polypropylene demand base operating in a structurally supply-constrained domestic market. Reliance Industries has announced and is executing capacity expansion at its Jamnagar petrochemical complex that will add incremental polypropylene production capability integrated with the expansion of its refinery FCC propylene generation, while the proposed greenfield Ratnagiri Refinery and Petrochemicals Limited integrated refinery-petrochemical project, if commissioned as planned, will add substantial new polypropylene production capacity from its integrated propylene generation and polymerization value chain designed to capture the downstream value of India’s growing polymer demand within a domestic manufacturing complex rather than exporting crude oil value and importing finished polymer. HPCL’s Rajasthan Refinery at Barmer, incorporating a polypropylene unit in its downstream petrochemical integration design, represents an additional domestic capacity addition that will serve the polypropylene demand of Northern and Central Indian converter markets currently dependent on either Reliance supply or import product for their polypropylene raw material requirements, and the Assam Petrochemicals expansion program in Northeast India represents a further regional capacity addition targeting the historically underserved northeastern market. The anticipated commissioning of these domestic capacity additions will progressively reduce India’s polypropylene import dependency from the current 31% level toward an estimated 18% to 22% of domestic consumption by 2034, materially improving the domestic supply security of India’s polypropylene converting industry while reducing the foreign exchange expenditure associated with polymer imports.

Key Challenges

Structural Propylene Supply Deficit and Feedstock Cost Competitiveness Constraints Limiting Domestic Polypropylene Production Economics

The economics of domestic polypropylene production in India are fundamentally constrained by the structure of India’s propylene supply landscape, where the majority of propylene is generated as a by-product of naphtha steam cracking and refinery FCC operations rather than from dedicated on-purpose propylene production routes, limiting the ability of Indian polypropylene producers to independently optimize their propylene procurement cost and supply volume in response to market conditions and creating a structural dependency on co-product propylene economics that are governed by ethylene production decisions and refinery crude processing optimization rather than polypropylene market demand signals. The naphtha-based steam cracking economics of Indian producers are structurally disadvantaged relative to the propane dehydrogenation economics of Middle Eastern polypropylene producers who access low-cost associated gas propane feedstocks at prices of USD 200 to USD 350 per metric tonne compared to Indian naphtha prices that imply propylene production costs of USD 550 to USD 750 per metric tonne, creating a landed cost competitiveness gap that enables Middle Eastern exports to reach Indian ports at prices that challenge the margins of domestically produced polypropylene even after accounting for import duties and freight costs. The absence of a developed propane dehydrogenation industry in India, despite several announced projects over the past decade that have not progressed to final investment decision due to feedstock supply uncertainty, financing challenges, and project execution risk concerns, represents a structural gap in India’s on-purpose propylene production capability that will need to be addressed through investment in PDH capacity or alternative on-purpose propylene routes if domestic polypropylene production is to achieve genuine cost competitiveness with import supply across the forecast period.

Competition From Low-Cost Asian and Middle Eastern Polypropylene Imports Creating Price Pressure on Domestic Producers and Converter Margin Compression

The Indian polypropylene market is exposed to sustained competitive import pressure from producers in Saudi Arabia, the United Arab Emirates, South Korea, China, and Singapore whose combination of low feedstock costs, large-scale production economics, proximity to Indian ports, and in some cases government export incentives enables them to supply polypropylene to Indian converters at landed prices that are frequently competitive with or below domestic producer prices even including import duties, creating a commercial environment where Indian polypropylene producers must continuously optimize their production efficiency, product grade portfolio, and customer service proposition to retain market share against import competition that is structurally cost-advantaged at the feedstock level. The reduction of Indian polypropylene import duties from the historical protective level of 7.5% to 5% in recent customs tariff revisions, combined with the duty-free access granted to polypropylene imports from ASEAN member countries under the India-ASEAN Free Trade Agreement, has reduced the tariff protection buffer available to domestic producers and made the Indian polypropylene market more directly exposed to Asian spot market pricing dynamics than was the case under the previous higher-duty regime. The periodic surplus production capacity situations in Chinese and Middle Eastern polypropylene markets, arising from the commissioning of large new PDH and integrated refinery-petrochemical polypropylene capacities in China that have exceeded domestic demand absorption in 2023 and 2024, have generated episodes of aggressive export pricing to India that have created acute margin pressure for domestic producers and price benefit for Indian converter industries that are structurally difficult for domestic producers to counter without temporary production rate reduction or export market diversion of their own output.

Regulatory and Infrastructure Challenges in Plastic Waste Management Creating Uncertainty for Polypropylene End-Use Markets and Downstream Converter Investment

The Indian regulatory environment governing plastic waste management, encompassing the Plastic Waste Management Rules 2016 and their subsequent amendments through 2022, the single-use plastics prohibition notification of 2022, the extended producer responsibility framework mandating plastic waste collection and recycling obligations on producers and importers, and the state-level plastic ban regulations that vary materially in scope, enforcement stringency, and product category coverage across different Indian states, creates a complex and evolving regulatory compliance landscape for Indian polypropylene converter industries whose investment decisions and product development priorities are significantly influenced by regulatory uncertainty about the future permissibility, mandatory recyclability, and EPR obligation structure of specific polypropylene packaging and disposable product applications. The single-use plastics prohibition implemented in July 2022, which banned a defined list of plastic items including cutlery, straws, stirrers, and certain thin carry bags, created immediate demand disruption in several polypropylene application segments and accelerated investment in bioplastic and paper-based material substitution programs by consumer goods companies seeking to de-risk their packaging portfolios from future single-use plastic regulatory expansion. The extended producer responsibility framework, which requires polypropylene packaging producers and importers to collect and recycle a progressively increasing percentage of the polypropylene packaging they place in the Indian market, from 35% in 2024-25 to 70% by 2028-29, is creating a significant and growing operational and financial compliance obligation for the Indian polypropylene value chain whose infrastructure readiness, including collection system capability, sorting technology availability, and recycling capacity, remains substantially below the levels required to achieve the mandated recycling percentages across the national polypropylene packaging waste stream.

Market Segmentation

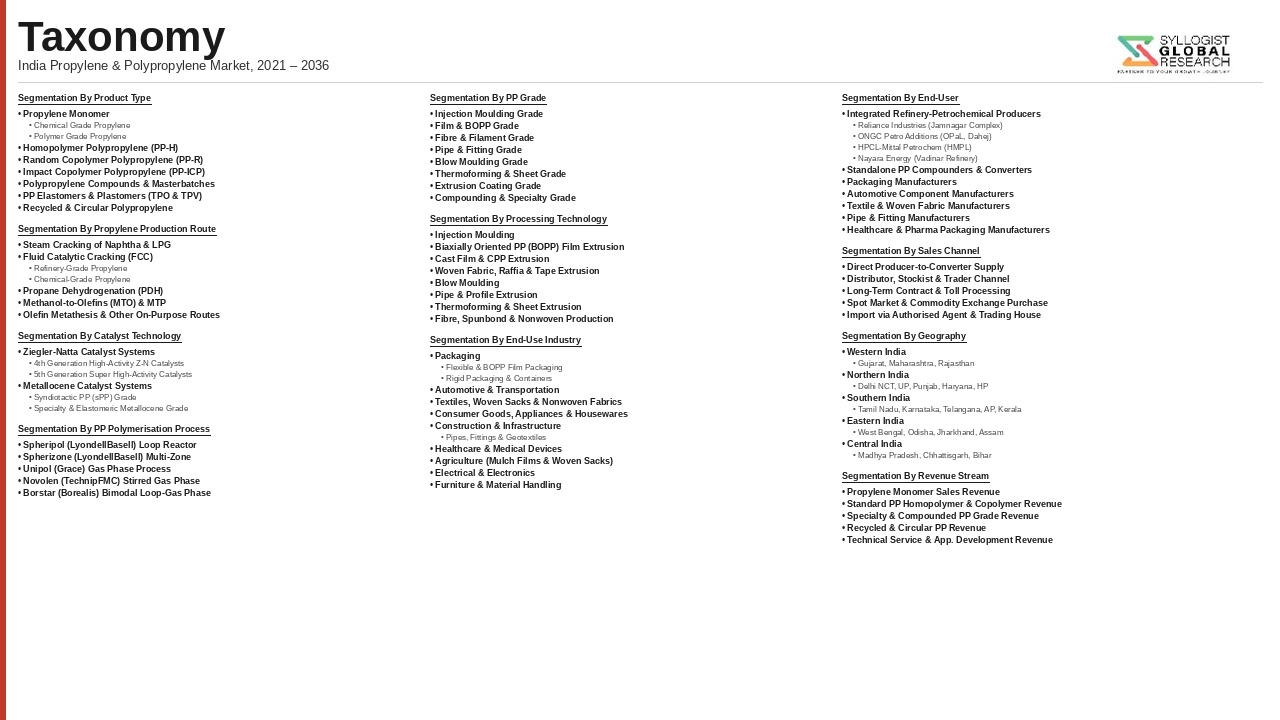

- Segmentation By Product Type

- Propylene Monomer (Chemical Grade and Polymer Grade)

- Polypropylene Homopolymer

- Polypropylene Random Copolymer

- Polypropylene Impact Copolymer (Heterophasic Copolymer)

- Long Glass Fiber and Short Glass Fiber Reinforced Polypropylene Compounds

- Mineral-Filled and Talc-Filled Polypropylene Compounds

- Specialty and Metallocene-Catalyzed Polypropylene Grades

- Others

- Segmentation By Production Route

- Steam Cracker Co-Product Propylene

- Refinery Fluid Catalytic Cracking (FCC) Propylene

- Propane Dehydrogenation (PDH) On-Purpose Propylene

- Imported Propylene and Polypropylene

- Others

- Segmentation By Processing Method

- Injection Molding

- Blow Molding

- Film Extrusion (Cast and Blown Film)

- Biaxially Oriented Polypropylene (BOPP) Film Processing

- Fiber and Filament Spinning

- Pipe and Profile Extrusion

- Thermoforming

- Nonwoven Spunbond and Meltblown Processing

- Others

- Segmentation By End-Use Application

- Flexible Packaging (Films, Pouches, Laminates)

- Rigid Packaging (Containers, Closures, Crates)

- Woven Sacks and FIBC Bags

- Automotive Components (Bumpers, Dashboards, Door Trims)

- Healthcare and Hygiene (Nonwovens, Medical Packaging, PPE)

- Pipes and Fittings (Water Supply, Plumbing, Irrigation)

- Textiles and Fibers (Raffia, Rope, Carpet Backing)

- Consumer Goods and Household Appliances

- Agriculture (Mulch Films, Agrochemical Packaging)

- Others

- Segmentation By End-Use Industry

- Food and Beverage Processing

- FMCG and Consumer Goods Manufacturing

- Automotive and Transportation

- Healthcare and Pharmaceuticals

- Construction and Infrastructure

- Agriculture and Agrochemicals

- E-Commerce and Logistics Packaging

- Textiles and Apparel

- Others

- Segmentation By Supply Source

- Domestic Production (Reliance Industries, OPaL, Haldia Petrochemicals, HPCL-Mittal)

- Middle East Imports (Saudi Arabia, UAE, Iran)

- Asian Imports (South Korea, China, Singapore, Thailand)

- Others

- Segmentation By Region

- Western India (Gujarat, Maharashtra, Rajasthan)

- Northern India (Delhi NCR, Punjab, Haryana, Uttar Pradesh)

- Southern India (Tamil Nadu, Karnataka, Andhra Pradesh, Telangana)

- Eastern India (West Bengal, Odisha, Bihar)

- Central India (Madhya Pradesh, Chhattisgarh)

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total market valuation of the India Propylene and Polypropylene Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by product type, processing method, end-use application, end-use industry, and region, to enable petrochemical producers, downstream polymer converters, import traders, and investors to identify which polypropylene grade categories and application segments will generate the highest absolute demand growth and most commercially attractive market positions across the forecast period?

- What is the current domestic polypropylene production capacity utilization status of Reliance Industries, ONGC Petro Additions, Haldia Petrochemicals, and HPCL-Mittal Energy, and what is the projected trajectory of domestic production capacity additions from announced expansion projects through 2034, how will these additions progressively reduce India’s structural import dependency from the current 31% of domestic consumption toward the forecast period target, and what import volumes by origin country will continue to be required to balance domestic supply with demand across the forecast period?

- How are India’s PLI scheme investment commitments across food processing, pharmaceuticals, electronics, automotive, and textiles manufacturing sectors translating into incremental polypropylene demand by application category and end-use industry through 2034, and what is the projected per capita polypropylene consumption growth trajectory for India compared to peer emerging economy benchmarks in China, Brazil, and Indonesia that helps frame the long-run demand potential of India’s polypropylene market relative to its current underpenetrated consumption level?

- How are the Plastic Waste Management Rules extended producer responsibility obligations, the single-use plastics prohibition, and the potential future expansion of plastic product bans reshaping the investment priorities, product grade development programs, and downstream application development strategies of Indian polypropylene producers and converter industries, and which polypropylene application segments face the greatest regulatory risk of demand displacement relative to alternative materials through 2034?

- Who are the leading domestic polypropylene producers, international exporting producers supplying the Indian import market, polypropylene compounders and specialty grade developers, and major downstream converter industries currently defining the competitive and consumption landscape of the India propylene and polypropylene market, and what are their respective production capacities, product grade portfolios, customer industry relationships, investment plans for capacity expansion or technology upgrades, pricing strategies relative to import competition, and positioning in response to the dual opportunity and challenge presented by India’s large and rapidly growing polypropylene demand base alongside its structurally evolving domestic supply and regulatory environment through the forecast period?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Crude Oil & Naphtha Price Volatility, Feedstock Availability & Propylene Production Cost Risk

- Import Competition, Dumping from China & Middle East & Domestic Price Realisation Risk for Indian Producers

- Plastic Waste Regulation, Single-Use Plastics Ban & Long-Term Polypropylene Demand Impact Risk

- Capacity Oversupply, New Entrant Investment & Margin Compression Risk in Indian Polypropylene Market

- Logistics Cost, Port Congestion & Inland Distribution Bottleneck Risk for Propylene & Polypropylene Supply in India

- Regulatory Framework & Standards

- Petroleum & Chemicals Investment Policies: PCPIRs, Integrated Refinery-Petrochemical Complex Approvals & PLI Scheme for Chemicals

- BIS Standards for Polypropylene Products (IS 10910 & Related Specifications) & Quality Control Order Enforcement

- Plastic Waste Management Rules 2016 (Amended), Extended Producer Responsibility (EPR) & Single-Use Plastic Phase-Out Impact on PP Demand

- Bureau of Indian Standards (BIS) Compulsory Registration, Import Quality Control Orders & Anti-Dumping Duty Frameworks for Polypropylene

- Environment, Health & Safety (EHS) Regulations: MSIHC Rules, Propylene Handling, Storage & Transportation Safety Standards in India

- India Propylene & Polypropylene Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Metric Tonnes)

- Market Size & Forecast by Product Type

- Propylene Monomer (Chemical & Polymer Grade)

- Homopolymer Polypropylene (PP-H)

- Random Copolymer Polypropylene (PP-R)

- Impact Copolymer Polypropylene (PP-ICP / Heterophasic Copolymer)

- Polypropylene Compounds & Masterbatches

- Polypropylene Elastomers & Plastomers (TPO & TPV)

- Recycled & Circular Polypropylene

- Market Size & Forecast by Propylene Production Route

- Steam Cracking of Naphtha & LPG (By-Product Propylene)

- Fluid Catalytic Cracking (FCC) Refinery-Grade & Chemical-Grade Propylene

- Propane Dehydrogenation (PDH)

- On-Purpose Propylene via Methanol-to-Olefins (MTO) & Methanol-to-Propylene (MTP)

- Olefin Metathesis & Other On-Purpose Routes

- Market Size & Forecast by Polypropylene Grade

- Injection Moulding Grade

- Film & BOPP Grade

- Fibre & Filament Grade

- Pipe & Fitting Grade

- Blow Moulding Grade

- Thermoforming & Sheet Grade

- Extrusion Coating Grade

- Compounding & Specialty Grade

- Market Size & Forecast by Processing Technology

- Injection Moulding

- Biaxially Oriented Polypropylene (BOPP) Film Extrusion

- Cast Film & CPP Extrusion

- Woven Fabric, Raffia & Tape Extrusion

- Blow Moulding

- Pipe & Profile Extrusion

- Thermoforming & Sheet Extrusion

- Fibre, Spunbond & Nonwoven Fabric Production

- Market Size & Forecast by End-Use Industry

- Packaging (Flexible, Rigid & BOPP Film Packaging)

- Automotive & Transportation

- Textiles, Woven Sacks & Nonwoven Fabrics

- Consumer Goods, Appliances & Housewares

- Construction & Infrastructure (Pipes, Fittings & Geotextiles)

- Healthcare & Medical Devices

- Agriculture (Mulch Films, Greenhouse Films & Woven Sacks)

- Electrical & Electronics

- Furniture & Material Handling

- Market Size & Forecast by End-User

- Integrated Refinery-Petrochemical Producers

- Standalone Polypropylene Compounders & Converters

- Packaging Manufacturers

- Automotive Component Manufacturers

- Textile & Woven Fabric Manufacturers

- Pipe & Fitting Manufacturers

- Healthcare & Pharma Packaging Manufacturers

- Market Size & Forecast by Sales Channel

- Direct Producer-to-Converter Supply

- Distributor, Stockist & Trader Channel

- Long-Term Contract & Toll Processing Arrangement

- Spot Market & Commodity Exchange Purchase

- Import via Authorised Agent & Trading House

- Western India Propylene & Polypropylene Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Product Type

- By Grade & Application

- By End-Use Industry

- By End-User

- By State / Zone

- By Sales Channel

- Market Size & Forecast

- Northern India Propylene & Polypropylene Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Product Type

- By Grade & Application

- By End-Use Industry

- By End-User

- By State / Zone

- By Sales Channel

- Market Size & Forecast

- Southern India Propylene & Polypropylene Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Product Type

- By Grade & Application

- By End-Use Industry

- By End-User

- By State / Zone

- By Sales Channel

- Market Size & Forecast

- Eastern India Propylene & Polypropylene Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Product Type

- By Grade & Application

- By End-Use Industry

- By End-User

- By State / Zone

- By Sales Channel

- Market Size & Forecast

- Central India Propylene & Polypropylene Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Product Type

- By Grade & Application

- By End-Use Industry

- By End-User

- By State / Zone

- By Sales Channel

- Market Size & Forecast

- State-Wise* Propylene & Polypropylene Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Product Type

- By Grade & Application

- By End-Use Industry

- By End-User

- By State / Zone

- By Sales Channel

- Market Size & Forecast

*Key States & Union Territories Analyzed in the Syllogist Global Research Portfolio: Gujarat, Maharashtra, Rajasthan, Delhi NCT, Uttar Pradesh, Punjab, Haryana, Tamil Nadu, Karnataka, Telangana, Andhra Pradesh, Kerala, West Bengal, Odisha, Madhya Pradesh, Chhattisgarh, Assam, Jharkhand, Bihar, Himachal Pradesh

- Technology Landscape & Innovation Analysis

- Ziegler-Natta & Metallocene Catalyst Technology Deep-Dive: Activity, Stereospecificity & Specialty PP Grade Enablement

- Propane Dehydrogenation (PDH) Technology Platforms: Oleflex, CATOFIN & Star Process for On-Purpose Propylene Production in India

- Advanced Polypropylene Polymerisation Reactor Technology: Spheripol, Spherizone, Unipol & Novolen Process Comparison

- BOPP Film Line Technology: Stenter, MDO & Sequential Stretching Technology for High-Barrier & Speciality Film Production

- Polypropylene Compounding Technology: Twin-Screw Extrusion, Reactive Extrusion & Glass Fibre Reinforcement

- Recycled Polypropylene Processing Technology: Sorting, Washing, Recompounding & Food-Grade Decontamination

- Bio-Based & Circular Polypropylene Technology: Bio-Propylene Routes & Chemical Recycling Pathways

- Patent & IP Landscape in Propylene & Polypropylene Technologies Relevant to India

- Value Chain & Supply Chain Analysis

- Crude Oil, Naphtha & LPG Feedstock Supply Chain for Propylene Production in India

- Propylene Monomer Production, Purification, Storage & Pipeline Distribution Supply Chain

- Polypropylene Polymerisation, Pelletising, Additives & Stabiliser Supply Chain

- Polypropylene Compounding, Masterbatch & Specialty Grade Manufacturing Supply Chain

- Distributor, Stockist, Trader & Import Agent Channel in India

- Converter, Processor & End-Use Industry Procurement Channel

- Post-Consumer Plastic Waste Collection, Sorting, Recycling & Circular Economy Value Chain

- Pricing Analysis

- Propylene Monomer Price Benchmarking: Domestic Contract, Import Parity & Spot Price Analysis in India

- Polypropylene Homopolymer, Copolymer & Specialty Grade Price Differential Analysis

- Polypropylene Import Price vs. Domestic Producer Price & Landed Cost Comparison

- Polypropylene Compound & Masterbatch Pricing: Value Addition & Margin Analysis

- Feedstock-to-Polymer Spread Analysis: Naphtha, Propylene & Polypropylene Price Chain in India

- Total Polypropylene Cost-in-Use per End-Application Across Key Converting Processes

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Propylene & Polypropylene: Carbon Footprint, Energy Intensity & Water Use Across Production Routes

- Polypropylene Recyclability, Mechanical Recycling Rate & Circular Economy Performance vs. Other Polymers

- Extended Producer Responsibility (EPR), Plastic Waste Management & Recycled Content Target Compliance in India

- Bio-Based Polypropylene & Chemical Recycling Pathways: GHG Reduction Potential & Commercial Readiness

- Regulatory-Driven Sustainability, SDG 9 (Industry & Innovation), SDG 12 (Responsible Consumption) & ESG Disclosure Alignment for PP Producers

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Product Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Product Type, Grade & End-Use Industry

- Player Classification

- Integrated Refinery-Petrochemical Propylene & Polypropylene Producers in India

- Standalone Polypropylene Producers & Dedicated PP Plants

- Polypropylene Compounders, Masterbatch & Specialty Grade Manufacturers

- Polypropylene Importers, Trading Companies & Authorised Agents

- Recycled & Circular Polypropylene Processors & Compounders

- BOPP Film & Packaging Manufacturers with Backward Integration

- Automotive & Consumer Goods PP Compound Specialists

- Emerging Bio-Based & Chemical Recycling Technology Ventures

- Competitive Analysis Frameworks

- Market Share Analysis by Product Type, Grade & End-Use Industry

- Company Profile

- Company Overview & Headquarters

- Propylene & Polypropylene Products & Grade Portfolio

- Key Customer Relationships & Reference Accounts in India

- Manufacturing Footprint & Production Capacity in India

- Revenue (India Propylene & Polypropylene Segment) & Order Book

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Capacity Expansion, Grade Launches, Feedstock Agreements)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Product Breadth vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Strategic Opportunity Analysis

- Strategic Output

- Market Opportunity Matrix: By Product Type, Grade, Processing Technology, End-Use Industry & State

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output