Global Sustainable Mining Technologies Market By Technology Type, By Mining Type, By Application, By Component, By End User, By Region, Competition, Forecast & Opportunities, 2021-2036F

Market Definition

The Global Sustainable Mining Technologies Market encompasses the development, integration, and commercial deployment of environmentally responsible extraction systems, energy-efficient mineral processing equipment, mine rehabilitation technologies, water recycling infrastructure, real-time emissions monitoring platforms, tailings management solutions, and digital operational tools designed to minimize the environmental and social footprint of mining activities across metallic, non-metallic, coal, and energy mineral extraction segments, procured by integrated mining corporations, contract miners, equipment manufacturers, and state-owned mining enterprises worldwide.

Market Insights

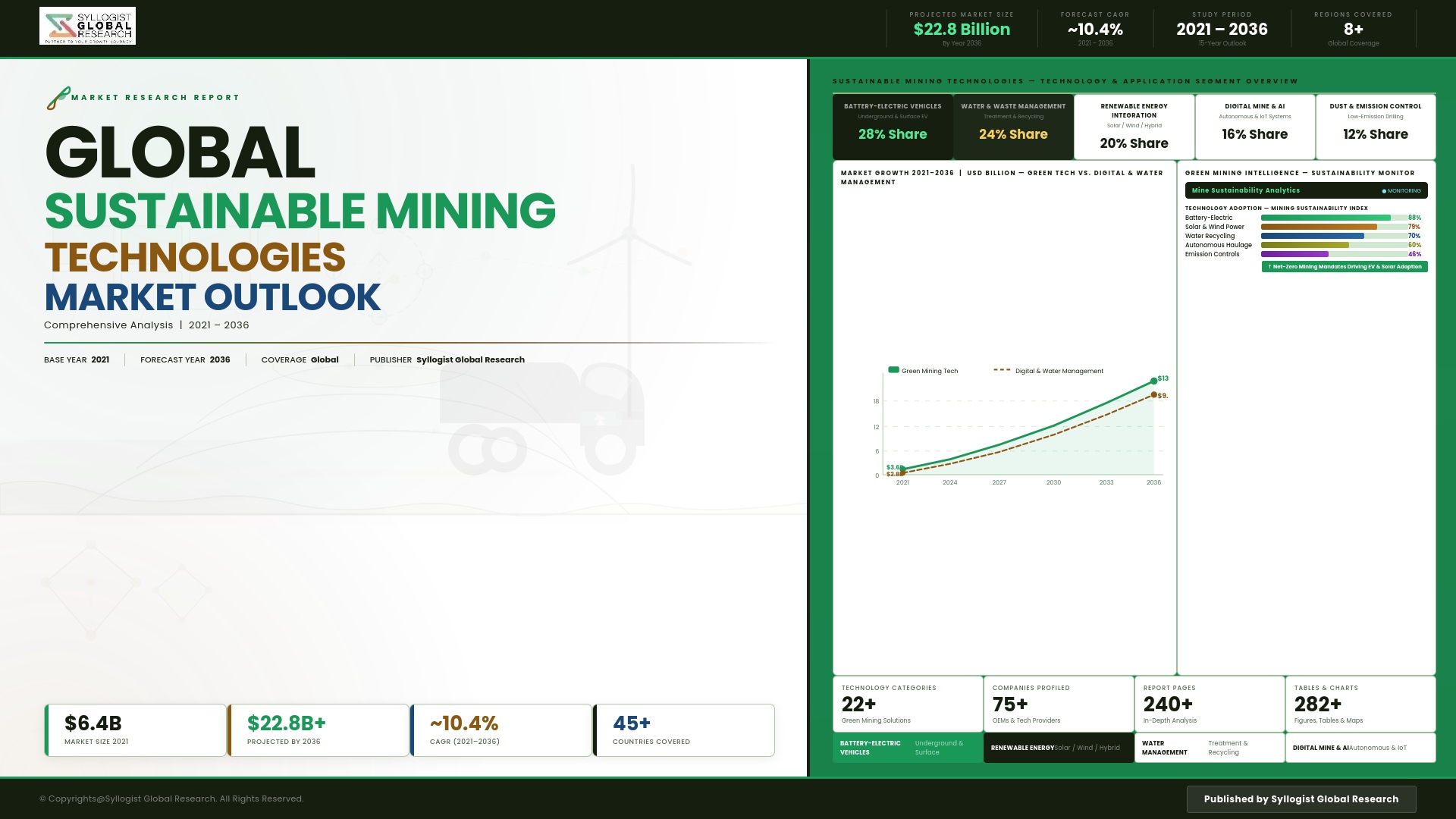

The global sustainable mining technologies market is undergoing a structural transformation, driven by the convergence of tightening environmental regulations, accelerating corporate decarbonization commitments, and the rapid maturation of electrification, automation, and digital monitoring technologies that are reshaping operational standards across the extractive industries. The market was valued at approximately USD 14.7 billion in 2025 and is projected to expand at a compound annual growth rate of 11.3% through 2034, as mining operators worldwide transition from compliance-oriented adoption of environmental controls to proactive integration of sustainable technologies as core operational and competitive differentiators.

The impetus for this shift is reinforced by an evolving investor and regulatory landscape in which ESG performance metrics directly influence access to capital, permitting approvals, and social license to operate in major mining jurisdictions including Australia, Canada, Chile, South Africa, and the European Union. Greenhouse gas reduction obligations under national climate commitments are compelling mining corporations to accelerate electrification of underground and surface haulage fleets, replace diesel-powered equipment with battery electric and hydrogen fuel cell alternatives, and integrate renewable energy microgrids into mine site power infrastructure. These investments are generating durable procurement demand for electric mining vehicles, onsite power storage systems, and energy management software platforms capable of optimizing consumption across complex mine site operations.

The water management and tailings technology segment represents one of the most rapidly growing application categories within the broader sustainable mining market, reflecting heightened regulatory scrutiny of tailings storage facility safety following high-profile failures and mounting freshwater scarcity pressures in key mining regions including the Atacama Desert, southern Africa, and arid zones of Australia. Dry stack tailings systems, paste thickeners, and advanced water recirculation infrastructure are registering accelerating procurement activity as operators upgrade legacy tailings management infrastructure to meet revised safety and environmental standards. Digital technologies encompassing AI-powered geological modeling, real-time environmental sensor networks, and autonomous mine monitoring platforms are simultaneously generating strong investment as operators seek to improve resource recovery rates, reduce waste generation, and demonstrate environmental compliance to regulators and investors with granular operational data.

Asia-Pacific is projected to register the highest regional growth rate through 2034, driven by substantial mining sector investment in Australia, China, Indonesia, and India, where governments are progressively tightening environmental standards for mining operations while simultaneously expanding mineral production capacity to satisfy growing battery metals and critical minerals demand from the electric vehicle and clean energy transition supply chains. North America maintains its position as the largest absolute market for sustainable mining technologies by revenue, supported by stringent federal and state-level environmental regulatory frameworks, active capital markets for mining ESG investment, and significant research and development activity across mining technology and clean energy innovation programs. Latin America, and specifically Chile and Peru, represents the third major regional market underpinned by copper and lithium production scale and intensifying water stewardship obligations in water-constrained mining regions.

Key Drivers

Tightening Environmental Regulations and Mandatory Emissions Reduction Obligations Accelerating the Adoption of Clean Technologies Across Global Mining Operations

National and sub-national governments across leading mining jurisdictions are progressively tightening environmental compliance requirements for mine site emissions, water use, land rehabilitation, and tailings management, establishing binding regulatory obligations that compel operators to invest in sustainable technology upgrades irrespective of commodity price cycles. Carbon pricing mechanisms, greenhouse gas reduction targets embedded in mine permitting conditions, and mandatory water stewardship reporting frameworks are creating durable, policy-driven procurement demand for emissions monitoring platforms, electrified equipment fleets, mine water recycling infrastructure, and biodiversity restoration technologies that extends across the full operational lifecycle of mining projects and cannot be deferred without triggering material regulatory and licensing risk.

Critical Minerals Demand Surge from Clean Energy and Electric Vehicle Supply Chains Creating Structural Incentives for Environmentally Responsible and Socially Licensed Mining Expansion

The accelerating global transition to electric vehicles, utility-scale battery storage, solar photovoltaic systems, and wind energy infrastructure is generating unprecedented demand for lithium, cobalt, nickel, copper, manganese, and rare earth elements, driving a substantial expansion of mining investment in minerals essential to clean energy supply chains. This structural demand imperative is simultaneously reinforcing procurement of sustainable mining technologies, as downstream clean energy manufacturers, automotive original equipment manufacturers, and technology companies impose supply chain traceability requirements, responsible sourcing standards, and environmental due diligence obligations on mining suppliers as preconditions for long-term offtake relationships, creating commercial incentives for sustainable technology adoption that complement regulatory compliance mandates.

Operational Efficiency and Cost Reduction Benefits of Mine Electrification, Automation, and Digital Monitoring Technologies Strengthening the Business Case for Sustainable Mining Investment

Beyond regulatory and reputational drivers, mine electrification, autonomous equipment deployment, and AI-enabled process optimization technologies deliver quantifiable operational advantages including reduced energy consumption per tonne of ore processed, lower maintenance costs associated with electric versus diesel powertrains in underground environments, improved ventilation economics from reduced diesel exhaust emissions, and enhanced resource recovery rates from precision extraction and processing technologies. These productivity and cost efficiency benefits are strengthening the internal rate of return justification for sustainable mining technology investment and accelerating adoption among cost-focused operators who may otherwise deprioritize environmental expenditure during periods of commodity price compression.

Key Challenges

High Capital Expenditure Requirements and Long Payback Periods of Sustainable Technology Retrofits Constraining Adoption Among Mid-Tier and Junior Mining Operators

The upfront capital investment required to electrify mobile equipment fleets, install renewable energy microgrids, deploy dry stack tailings systems, and implement enterprise-wide environmental monitoring infrastructure imposes significant financial barriers for mid-tier and junior mining companies operating with constrained balance sheets, limited access to low-cost sustainability-linked financing, and shorter mine-life horizons that reduce the discounted payback value of long-lived sustainable technology assets. This capital constraint is particularly pronounced in developing country mining jurisdictions where financing markets for green mining infrastructure remain underdeveloped and project economics are more sensitive to cost escalation from technology upgrades.

Technology Integration Complexity and Operational Continuity Risks Associated with Transitioning Existing Mine Infrastructure to Electrified and Digitally Enabled Operating Platforms

Transitioning operating mines from legacy diesel-powered and manually managed systems to electrified, autonomous, and digitally instrumented operating platforms entails significant technical integration complexity, including retrofitting underground infrastructure for electrical charging networks, re-engineering ventilation systems for battery electric vehicle operating requirements, retraining workforce competencies for autonomous equipment operation and maintenance, and integrating heterogeneous sensor and monitoring data streams into unified mine management platforms. These integration challenges introduce operational continuity risks that mine operators are reluctant to accept during periods of high production demand, creating implementation delays that constrain the pace of sustainable technology adoption relative to market potential.

Shortage of Specialized Engineering and Technical Expertise in Sustainable Mining Technology Development, Deployment, and Operational Optimization Limiting Market Scalability

The sustainable mining technology sector faces a structural skills deficit at the intersection of mining engineering, environmental science, electrical systems design, data analytics, and autonomous systems integration, where the available talent pool is materially insufficient to support the scale and pace of technology deployment programs being pursued by mining operators, technology developers, and equipment manufacturers globally. This talent constraint is further compounded by geographical concentration of skilled professionals in a limited number of established mining technology hubs, creating resource bottlenecks that extend implementation timelines, elevate engineering service costs, and limit the technical sophistication of deployed sustainable mining solutions particularly in emerging market mining jurisdictions.

Market Segmentation

- Segmentation By Technology Type

- Mine Electrification and Battery Electric Vehicle Systems

- Renewable Energy and Microgrid Power Infrastructure

- Water Recycling and Tailings Management Technologies

- AI-Powered Environmental Monitoring and Compliance Platforms

- Autonomous Haulage and Robotic Extraction Systems

- Carbon Capture and Emissions Reduction Technologies

- Others

- Segmentation By Mining Type

- Underground Mining

- Open-Pit Surface Mining

- Placer Mining

- In-Situ Leaching and Solution Mining

- Offshore and Seabed Mining

- Others

- Segmentation By Application

- Ore Extraction and Haulage

- Mineral Processing and Beneficiation

- Tailings and Waste Management

- Water Treatment and Recirculation

- Mine Site Energy Management

- Environmental Monitoring and Reporting

- Land Rehabilitation and Mine Closure

- Others

- Segmentation By Component

- Hardware and Equipment

- Software and Analytics Platforms

- Services and Maintenance

- Segmentation By End User

- Integrated Major Mining Corporations

- Mid-Tier and Junior Mining Companies

- Contract Mining Operators

- State-Owned Mining Enterprises

- Mining Equipment and Technology Developers

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Sustainable Mining Technologies Market in 2025, projected through 2034, segmented by technology type and application, enabling mining operators, technology investors, and equipment manufacturers to identify highest-growth solution categories and most durable procurement opportunities across the sustainable mining landscape?

- How are leading mining jurisdictions including Australia, Canada, Chile, South Africa, and the European Union evolving environmental regulatory requirements, carbon pricing mechanisms, and tailings management standards, and how are these regulatory developments reshaping capital allocation priorities and technology procurement timelines across the global mining sector?

- Which technology categories, specifically mine electrification, dry stack tailings systems, renewable energy microgrids, and AI-enabled environmental monitoring platforms, are generating the highest adoption rates and investment activity through 2034, and what operational, financial, and regulatory factors are driving differential uptake across mining type and operator scale?

- How is the competitive landscape structured among mining equipment original equipment manufacturers, specialist sustainable technology developers, and digital solutions providers pursuing the sustainable mining market, and what partnership, acquisition, and joint development strategies are enabling new entrants to compete against established mining technology incumbents?

- What are the primary capital expenditure barriers, technology integration risks, and workforce capability constraints limiting the pace of sustainable mining technology adoption among mid-tier and junior mining operators, and what financing structures, modular deployment models, and managed service arrangements are emerging to address these adoption barriers?

- Which regional mining markets, specifically Asia-Pacific, Latin America, and Africa, are expected to generate the highest incremental sustainable mining technology procurement through 2034, and what combinations of regulatory pressure, critical minerals demand growth, and infrastructure investment are driving technology adoption priorities in each regional market?

- How is the growing demand for critical minerals essential to electric vehicle and clean energy supply chains reshaping the strategic relationship between sustainable mining technology adoption and long-term offtake security, and what responsible sourcing standards and traceability requirements from downstream manufacturers are accelerating environmental technology investment among upstream mining producers?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Regulatory, Permitting & Social License to Operate Risk

- Commodity Price Cyclicality, Capital Discipline & Project Financing Risk

- Technology Maturity, Pilot-to-Commercial Scale-Up & Integration Risk

- Climate, Water Scarcity & Physical Environmental Risk

- Community, Indigenous Rights & ESG Reputational Risk

- Regulatory Framework & Standards

- National Mining Code, Environmental Impact Assessment & Permitting Frameworks

- Tailings Dam Safety, Global Industry Standard on Tailings Management (GISTM) & Geotechnical Regulations

- Emission, Air Quality, Water Discharge & Waste Management Environmental Regulations

- Critical Mineral Sourcing, ESG Reporting, EU Critical Raw Materials Act & US Inflation Reduction Act Frameworks

- Green Finance, ICMM, IRMA Certification & Sustainable Mining Procurement Standards

- Global Sustainable Mining Technologies Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Equipment Units Deployed and Installed Capacity, MW)

- Market Size & Forecast by Technology Category

- Electrification & Battery-Electric Mining Equipment (BEV Haul Trucks, LHDs & Drills)

- Hydrogen Fuel Cell & Alternative Fuel Mining Equipment Technology

- Renewable Energy Integration (Solar PV, Wind & Microgrid) at Mine Sites

- Water Recycling, Dry Processing & Zero Liquid Discharge Technology

- Tailings Management (Dry Stack, Filtered Tailings & Paste Backfill) Technology

- Autonomous Haulage, Automated Drilling & Remote Operation Technology

- Energy-Efficient Comminution, HPGR & Advanced Grinding Technology

- Bioleaching, In-Situ Leaching & Alternative Extraction Technology

- Digital Twin, AI, IoT & Mine Optimisation Platform Technology

- Market Size & Forecast by Technology

- Battery Electric & Trolley-Assist Haulage Technology

- Hydrogen Fuel Cell, Green Ammonia & Alternative Fuel Combustion Technology

- Solar PV, Wind & Hybrid Renewable Mining Microgrid Technology

- High-Pressure Grinding Rolls (HPGR), Stirred Mill & Comminution Efficiency Technology

- Dry Stack Tailings, Filter Press & Paste Thickening Technology

- Sensor-Based Ore Sorting, XRF & Hyperspectral Sorting Technology

- Autonomous Vehicle, Autonomous Haulage Systems (AHS) & Robotics Technology

- Bioleaching, Bio-Oxidation & Microbial Mineral Processing Technology

- Digital Twin, Machine Learning, IoT & Predictive Maintenance Platform

- Market Size & Forecast by Sustainability Output Type

- Greenhouse Gas Emission Reduction & Decarbonisation Output (CO2e Tonnes Avoided)

- Water Consumption & Freshwater Savings Output

- Energy Efficiency & Electricity Demand Reduction Output

- Tailings Volume & Solid Waste Reduction Output

- Critical Mineral Recovery & Circular Material Yield Output

- Market Size & Forecast by Project Scale

- Large-Scale Tier-1 Mines (Above 50 Million Tonnes per Annum Throughput)

- Medium-Scale Mines (5 to 50 Million Tonnes per Annum Throughput)

- Small-Scale & Artisanal Mine Formalisation (Below 5 Million Tonnes per Annum)

- Market Size & Forecast by Application

- Copper, Gold & Precious Metal Mining

- Iron Ore, Nickel & Base Metal Mining

- Critical & Battery Mineral Mining (Lithium, Cobalt, Rare Earths & Graphite)

- Coal & Industrial Minerals Mining

- Uranium & Radioactive Mineral Mining

- Construction Aggregates, Quarrying & Building Materials

- Underground Mining & Deep-Ore Body Operations

- Market Size & Forecast by End-User

- Major Mining Company & Tier-1 Operator

- Mid-Tier & Junior Mining Company

- Critical Mineral & Battery Supply Chain Developer

- Mining Service Contractor, EPC & Fleet Operator

- Government Mining Authority & State-Owned Enterprise

- Market Size & Forecast by Sales Channel

- Direct Equipment Supply & OEM Fleet Contract

- EPC & Turnkey Project Contract (Engineering, Procurement & Construction)

- Technology Licensing, Joint Venture & Co-Development Partnership

- Operations & Maintenance (O&M), Leasing & Performance Contract

- North America Sustainable Mining Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Equipment Units Deployed and Installed Capacity, MW)

- By Technology Category

- By Technology

- By Sustainability Output Type

- By Project Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Sustainable Mining Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Equipment Units Deployed and Installed Capacity, MW)

- By Technology Category

- By Technology

- By Sustainability Output Type

- By Project Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Sustainable Mining Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Equipment Units Deployed and Installed Capacity, MW)

- By Technology Category

- By Technology

- By Sustainability Output Type

- By Project Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Sustainable Mining Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Equipment Units Deployed and Installed Capacity, MW)

- By Technology Category

- By Technology

- By Sustainability Output Type

- By Project Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Sustainable Mining Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Equipment Units Deployed and Installed Capacity, MW)

- By Technology Category

- By Technology

- By Sustainability Output Type

- By Project Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Sustainable Mining Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Equipment Units Deployed and Installed Capacity, MW)

- By Technology Category

- By Technology

- By Sustainability Output Type

- By Project Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- *Countries Analysed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Italy, Norway, Sweden, China, Japan, India, Australia, South Korea, Singapore, Brazil, Chile, Saudi Arabia, UAE, Egypt, South Africa, Israel

- Market Size & Forecast

- Technology Landscape & Innovation Analysis

- Battery-Electric Haulage, Trolley-Assist & Charging Infrastructure Technology Deep-Dive

- Hydrogen Fuel Cell, Green Ammonia & Alternative Fuel Mining Equipment Technology

- Renewable Energy Integration, Solar PV, Wind & Mining Microgrid Technology

- Water Recycling, Dry Processing & Zero Liquid Discharge Technology for Mine Sites

- Dry Stack, Filtered Tailings & Paste Backfill Tailings Management Technology

- Autonomous Haulage Systems (AHS), Automated Drilling & Remote Operations Centre Technology

- Sensor-Based Ore Sorting, HPGR & Energy-Efficient Comminution Technology

- Patent & IP Landscape in Sustainable Mining Technologies

- Value Chain & Supply Chain Analysis

- Mining Equipment OEM, Battery-Electric Vehicle & Specialty Machinery Manufacturing Supply Chain

- Renewable Energy Equipment (Solar PV, Wind Turbine & BESS) Supply Chain for Mine Sites

- Water Treatment, Thickener, Filter Press & Tailings Equipment Supply Chain

- Automation, Robotics, Sensor & Digital Platform Technology Supply Chain

- EPC Contractor, Mining Engineer & System Integrator Procurement Landscape

- Mining Operator, Government Authority & Offtake Partner Channel

- Mine Closure, Rehabilitation & Legacy Site Reprocessing Supply Chain

- Pricing Analysis

- Battery-Electric Haulage Fleet Capital and Total Cost of Ownership (TCO) Analysis

- Renewable Energy Mine Microgrid Capex and Levelised Cost of Electricity (LCOE) Analysis

- Water Recycling, Dry Processing & ZLD Capital and Operating Cost Analysis

- Dry Stack Tailings & Filter Press Capital and Lifecycle Cost Analysis

- Autonomous Haulage, Robotics & Digital Platform TCO and Productivity Analysis

- Total Sustainable Mine Project Economics: Cost per Tonne Mined & Learning Curve Analysis

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Sustainable Mining Technologies: Carbon Footprint, Energy Intensity & Water Footprint Across Technology Routes

- Carbon Neutrality & Net Zero Contribution: Pathway to Diesel-Free, Renewable-Powered and Scope 1 and 2 Emission-Free Mining

- Responsible Sourcing, Critical Mineral Traceability & IRMA/ICMM Certification

- Environmental Compliance, Tailings Safety, Water Discharge & Biodiversity Consideration at Mine Sites

- Regulatory-Driven Sustainability, GISTM, SDG 12 (Responsible Consumption) & SDG 13 (Climate Action) Alignment & Green Finance Eligibility

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Technology Category & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Technology Category, Sub-Technology & Geography

- Player Classification

- Mining Equipment OEM & Battery-Electric Vehicle Manufacturer

- Autonomous Haulage, Robotics & Automation Technology Provider

- Renewable Energy & Mining Microgrid System Integrator

- Water Treatment, Dry Processing & ZLD Technology Specialist

- Tailings Management, Filter Press & Paste Backfill Specialist

- Sensor-Based Sorting, HPGR & Comminution Efficiency Provider

- Digital Twin, AI, IoT & Mine Optimisation Software Vendor

- Mine Closure, Rehabilitation & Legacy Site Reprocessing Specialist

- Competitive Analysis Frameworks

- Market Share Analysis by Technology Category, Sub-Technology & Region

- Company Profile

- Company Overview & Headquarters

- Sustainable Mining Products & Technology Portfolio

- Key Customer Relationships & Reference Mine Deployments

- Manufacturing Footprint & Production Capacity

- Revenue (Sustainable Mining Segment) & Order Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Capacity Expansion, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Technology Category, Sub-Technology, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output