Global Plastic Waste-to-Feedstock Market By Conversion Technology, By Plastic Waste Type, By Feedstock Output, By End Use Application, By Scale of Operation, By End User, By Region, Competition, Forecast & Opportunities, 2021-2036F

Market Definition

The Global Plastic Waste-to-Feedstock Market encompasses the development, deployment, and commercial operation of chemical recycling and thermochemical conversion technologies including pyrolysis, gasification, solvolysis, hydrothermal processing, and catalytic depolymerization that transform post-consumer and post-industrial plastic waste streams into petrochemical feedstocks, monomers, syngas, pyrolysis oil, and recovered chemicals suitable for reintroduction into polymer manufacturing supply chains or utilization as fuel blendstocks, serving petrochemical producers, polymer manufacturers, fuel refiners, and circular economy program operators globally.

Market Insights

The global plastic waste-to-feedstock market is at a decisive commercial inflection point, transitioning from a landscape dominated by pilot demonstration projects and early-stage venture investment toward a phase of first-commercial-scale facility deployment, strategic partnership formation between chemical recycling technology developers and major petrochemical producers, and the progressive integration of chemically recycled feedstocks into certified circular polymer supply chains serving brand owner sustainability commitments and regulatory recycled content mandates. The market was valued at approximately USD 3.4 billion in 2025 and is projected to expand at a compound annual growth rate of 26.8% through 2034, driven by the accelerating implementation of extended producer responsibility legislation, mandatory minimum recycled content requirements in packaging regulations, and the strategic positioning of integrated petrochemical producers who recognize chemical recycling as a necessary complement to mechanical recycling in addressing the large volumes of contaminated, mixed, and multi-layer plastic waste streams that mechanical recycling processes cannot economically convert into value-preserving recyclate.

Pyrolysis technology represents the most commercially advanced chemical recycling pathway within the plastic waste-to-feedstock market, with multiple operators progressing from demonstration and pilot scale to commercial facility construction across Europe, North America, and Asia-Pacific, converting mixed and contaminated polyolefin waste including post-consumer flexible packaging, agricultural film, and industrial plastic waste into pyrolysis oil that can be processed in petroleum refinery fluid catalytic cracking units or steam cracker feedstock preparation systems to yield recycled monomers and intermediates suitable for producing certified circular polyethylene, polypropylene, and petrochemical derivatives. The integration of plastic waste pyrolysis oil into existing refinery infrastructure through co-processing represents a particularly capital-efficient commercialization pathway that leverages existing petroleum processing assets rather than requiring fully dedicated chemical recycling end-use infrastructure, enabling faster time-to-market for pyrolysis technology developers pursuing refinery offtake partnership strategies with major integrated oil and chemical companies.

Solvolysis and catalytic depolymerization technologies targeting specific plastic polymer types including polyethylene terephthalate, polystyrene, polycarbonate, and nylon are demonstrating superior recycled feedstock quality characteristics relative to pyrolysis for their target plastic substrates, producing monomer-grade chemical outputs including terephthalic acid, styrene, bisphenol A, and caprolactam that re-enter polymer manufacturing supply chains as like-for-like monomer substitutes capable of producing virgin-equivalent polymer without the quality or performance compromises that blending of pyrolysis oil co-processing products can introduce in sensitive applications. These depolymerization routes are attracting significant investment from major polyester, polystyrene, and engineering polymer producers who are developing integrated plastic collection, sorting, and chemical recycling supply chains as strategic assets supporting their certified recycled content product offerings and long-term feedstock security under increasingly stringent packaging sustainability obligations from major consumer goods and retail brand owner customers.

Europe leads the global plastic waste-to-feedstock market in regulatory framework maturity and technology deployment investment, driven by the European Union Packaging and Packaging Waste Regulation mandating minimum recycled plastic content in packaging, extended producer responsibility harmonization across member states, and the strategic investment of European petrochemical companies in chemical recycling partnerships and capacity development. North America is the most dynamic market for technology developer activity and investment, anchored by the concentration of chemical recycling startups, the strategic co-investment programs of major United States and Canadian integrated petrochemical producers, and growing state-level extended producer responsibility legislation creating market demand for certified recycled content supply. Asia-Pacific is the fastest-growing regional market, driven by the massive scale of plastic waste generation in China, Japan, South Korea, and Southeast Asia, government circular economy policy mandates, and the growing engagement of Asian petrochemical corporations in chemical recycling technology acquisition and capacity development programs.

Key Drivers

Mandatory Recycled Content Legislation and Extended Producer Responsibility Frameworks Creating Regulatory Demand Pull for Certified Chemically Recycled Feedstock at Scale

The progressive implementation of mandatory minimum recycled plastic content requirements in packaging legislation across the European Union, United Kingdom, and a growing number of national jurisdictions, combined with extended producer responsibility frameworks imposing financial obligations on packaging producers proportional to plastic waste management costs, is creating durable regulatory demand for certified recycled plastic content at volumes that mechanical recycling of high-quality sorted plastic streams alone cannot supply to satisfy mandatory content thresholds across the full range of packaging formats and polymer types covered by emerging legislation. Brand owner and retailer sustainability commitments establishing voluntary recycled content targets in advance of regulatory mandates are simultaneously generating commercial demand pull for certified circular polymer supply that chemical recycling feedstock providers and their petrochemical manufacturing partners are positioning to serve through mass balance attribution and certified circular product programs.

Strategic Petrochemical Industry Investment in Chemical Recycling Capacity and Technology Partnerships Legitimizing the Sector and Accelerating Commercial Scale-Up Beyond Startup Capital

The growing engagement of major integrated petrochemical producers including leading European chemical companies, United States Gulf Coast polymer manufacturers, and Asian petrochemical corporations in chemical recycling technology licensing, equity investment, offtake partnership, and co-investment program formation is providing plastic waste-to-feedstock technology developers with access to the capital, technical expertise, regulatory relationships, and established supply chain infrastructure required to scale from demonstration toward commercial operations at rates that startup capital markets alone could not support. The strategic alignment of chemical recycling technology development with large petrochemical company feedstock security and circular polymer portfolio objectives is establishing a durable co-investment ecosystem that is progressively de-risking chemical recycling project financing and enabling commercial facility development at scales where unit economics can approach viability.

Mechanical Recycling Technical Limitations for Mixed and Contaminated Plastic Waste Creating a Complementary Market Space for Chemical Recycling Technologies Addressing Unrecyclable Waste Streams

The inherent technical constraints of mechanical recycling, which requires sorted, clean, single-polymer waste streams to produce recyclate of sufficient quality for demanding packaging and technical applications, leaves the large fraction of contaminated, multi-layer, mixed polymer, and food-contact flexible packaging waste currently consigned to landfill or energy recovery without a commercially viable closed-loop recycling pathway, creating a structurally defined application space for chemical recycling technologies capable of processing lower-grade and more heterogeneous plastic waste inputs that mechanical recycling facilities routinely reject. The growing policy pressure to divert plastic waste from landfill and incineration under waste hierarchy obligations and landfill tax escalation frameworks is reinforcing the economic case for chemical recycling facility development as a complementary technology tier enabling higher overall plastic circularity performance than mechanical recycling alone can achieve.

Key Challenges

High Capital and Operating Costs of Chemical Recycling Facilities and Competitive Cost Gap with Virgin Petrochemical Feedstocks Limiting Unsubsidized Commercial Project Viability

Chemical recycling facilities for plastic waste conversion currently carry capital and operating cost structures that result in recycled feedstock production costs substantially exceeding those of virgin petroleum-derived petrochemical feedstocks at prevailing crude oil and natural gas prices, requiring either regulatory mandated recycled content premiums, carbon pricing support that monetizes the avoided emission benefit of circular feedstock versus virgin production, or voluntary brand owner sustainability premium payments to generate project economics capable of supporting commercial facility investment and financing. The absence of a well-established and consistently enforced carbon credit or recycled content certificate pricing framework across major markets creates revenue certainty limitations for chemical recycling project financing that constrains the availability of long-term debt capital at terms making project returns acceptable to infrastructure investors.

Plastic Waste Feedstock Quality Inconsistency, Collection Infrastructure Gaps, and Supply Security Risks Creating Input Reliability Challenges for Commercial Chemical Recycling Operations

Chemical recycling facilities require consistent supply of plastic waste feedstock meeting minimum quality thresholds for polymer composition, contamination levels, moisture content, and halogen concentration that determine processing efficiency, product yield, and output quality, but the inconsistency of post-consumer plastic waste composition, the underdevelopment of dedicated plastic waste collection and sorting infrastructure in many regions, and the competition for high-quality sorted plastic waste between mechanical and chemical recyclers creates feedstock supply security and quality variability challenges that complicate facility capacity planning, processing economics, and output product specification consistency at chemical recycling plants dependent on post-consumer waste inputs. Establishing reliable long-term feedstock supply agreements with municipalities, waste management operators, and industrial waste generators requires contractual frameworks and supply chain investment programs that add complexity and cost to chemical recycling project development.

Mass Balance Attribution Methodology Disputes and Certification Framework Fragmentation Creating Market Credibility and Compliance Complexity for Chemically Recycled Feedstock Products

The mass balance accounting methodology used to attribute recycled content certification to polymer products manufactured with chemically recycled feedstock blended into conventional petrochemical production streams is subject to ongoing methodological debate among regulators, environmental advocacy groups, and standards bodies over the appropriate allocation rules, chain of custody verification requirements, and independent audit standards that should govern certified circular polymer claims, creating regulatory uncertainty and market credibility risk for producers and brand owners investing in chemical recycling supply chains whose certified recycled content claims may face legislative challenge or reputational scrutiny if mass balance methodology standards are subsequently revised or restricted in ways that reduce the recycled content percentage attributable to the physical volumes of plastic waste actually processed.

Market Segmentation

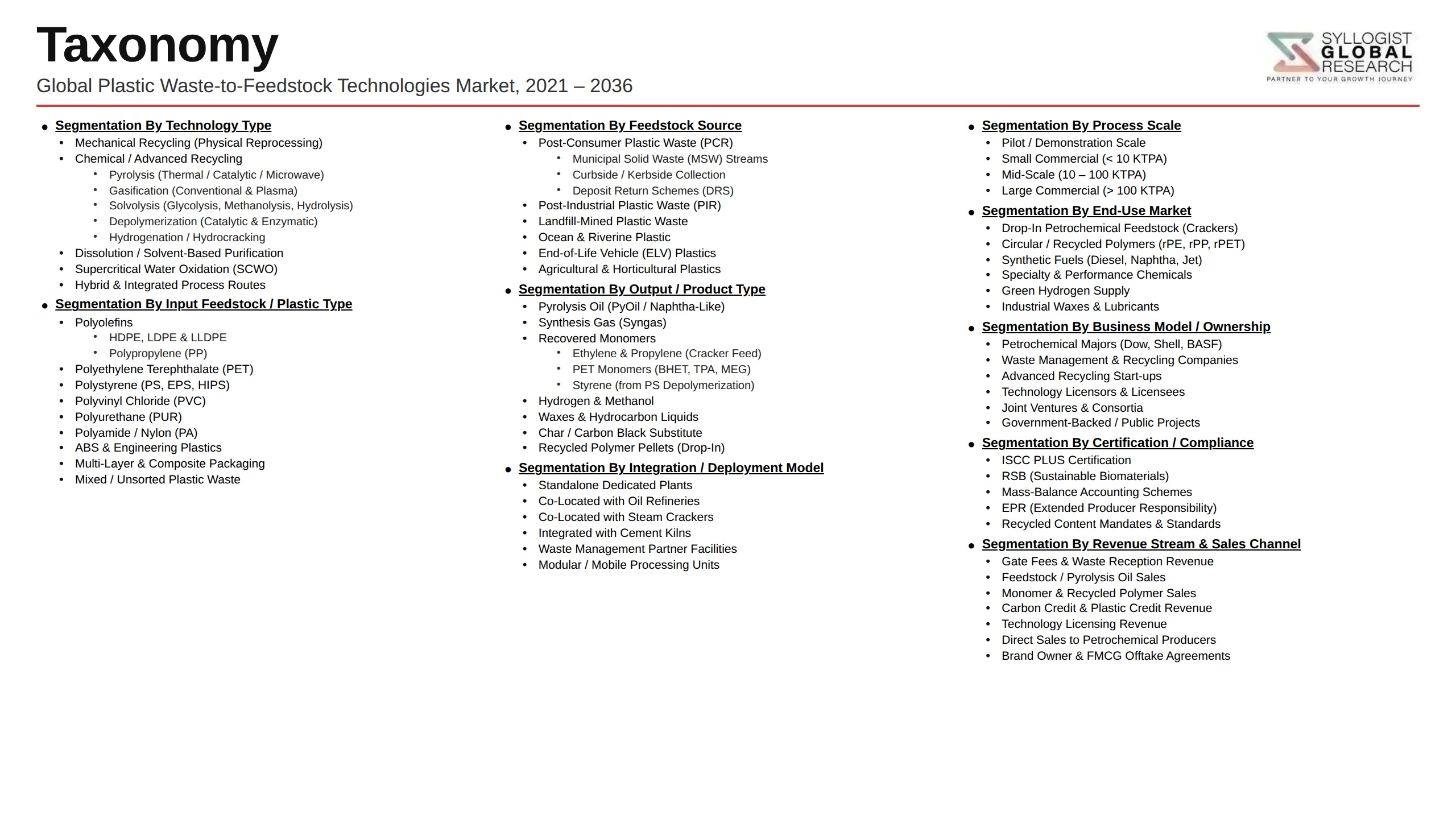

- Segmentation By Conversion Technology

- Pyrolysis (Thermal and Catalytic)

- Gasification and Syngas Production

- Hydrothermal Processing and Liquefaction

- Solvolysis (Glycolysis, Methanolysis, Hydrolysis)

- Catalytic Depolymerization

- Dissolution and Solvent Extraction

- Others

- Segmentation By Plastic Waste Type

- Polyolefins (Polyethylene and Polypropylene)

- Polyethylene Terephthalate and Polyesters

- Polystyrene and Expanded Polystyrene

- Polycarbonate and Engineering Plastics

- Mixed and Contaminated Plastic Waste

- Multi-Layer and Flexible Packaging Waste

- Industrial and Post-Industrial Plastic Scrap

- Others

- Segmentation By Feedstock Output

- Pyrolysis Oil and Naphtha Equivalent

- Recycled Monomers (Ethylene, Propylene, Styrene)

- Syngas and Hydrogen

- Recovered Terephthalic Acid and Glycols

- Fuel Blendstocks and Diesel Equivalents

- Chemical Building Blocks and Intermediates

- Others

- Segmentation By End Use Application

- Certified Circular Polymer Production

- Petrochemical Steam Cracker Feedstock

- Petroleum Refinery Co-Processing

- Fuel and Energy Applications

- Specialty Chemical Manufacturing

- Others

- Segmentation By Scale of Operation

- Small-Scale and Modular Units (Below 10,000 Tonnes per Year)

- Medium-Scale Commercial Facilities (10,000 to 50,000 Tonnes per Year)

- Large-Scale Industrial Plants (Above 50,000 Tonnes per Year)

- Segmentation By End User

- Integrated Petrochemical and Polymer Producers

- Petroleum Refineries and Fuel Blenders

- Independent Chemical Recycling Technology Operators

- Waste Management and Environmental Services Companies

- Consumer Goods and Packaging Brand Owners

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global plastic waste-to-feedstock market valuation in 2025, projected through 2034, segmented by conversion technology, plastic waste type, and feedstock output, enabling technology developers, petrochemical investors, and waste management operators to identify the highest-growth chemical recycling pathways and most strategically significant commercial scale-up opportunities across the global market?

- How are mandatory recycled content packaging regulations, extended producer responsibility frameworks, and voluntary brand owner sustainability commitments creating demand for certified circular polymer supply, and what mass balance methodology standards, chain of custody certification frameworks, and independent audit requirements are governing the credibility and regulatory acceptance of chemically recycled feedstock content claims across major market jurisdictions?

- Which chemical recycling conversion technologies, specifically pyrolysis for mixed polyolefin waste, PET solvolysis for polyester depolymerization, and polystyrene dissolution purification processes, are demonstrating the most commercially viable unit economics, output quality, and scalability characteristics at current technology readiness levels, and what cost reduction pathways and performance improvement milestones are required to achieve commercially self-sustaining operations without sustained regulatory subsidy support?

- How are major integrated petrochemical producers structuring their chemical recycling technology partnerships, equity investments, and offtake agreements with plastic waste-to-feedstock technology developers, and what technology licensing, capacity co-investment, certified circular product portfolio development, and plastic waste supply chain integration strategies are enabling leading petrochemical companies to establish defensible positions in the emerging chemical recycling supply chain?

- What plastic waste collection infrastructure gaps, sorting technology limitations, feedstock quality inconsistency challenges, and supply security risks are most significantly constraining the operational reliability and processing economics of commercial-scale chemical recycling facilities, and what integrated waste management, collection logistics, and feedstock pre-treatment investment programs are chemical recyclers and their supply chain partners developing to address these input availability constraints?

- How are carbon pricing mechanisms, recycled content certificate market development, plastic waste landfill and incineration tax escalation, and producer responsibility financial obligation frameworks combining to improve the commercial project economics of plastic waste-to-feedstock facilities, and what policy instrument configurations in Europe, North America, and Asia-Pacific are proving most effective at bridging the cost gap between chemically recycled and virgin petrochemical feedstock production economics?

- Which regional plastic waste-to-feedstock markets, specifically Europe, North America, and Asia-Pacific, are expected to generate the highest incremental facility investment and feedstock output capacity growth through 2034, and what combinations of regulatory mandates, petrochemical industry co-investment, waste infrastructure development, and brand owner recycled content procurement commitments are defining technology deployment pace and commercial scale-up trajectories in each regional market?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Plastic Waste Feedstock Quality, Contamination & Consistent Supply Availability Risk

- Output Product Yield, Specification Variability & Petrochemical Acceptance Risk

- Technology Scale-Up, First-of-a-Kind Plant Execution & Commercialisation Timeline Risk

- Virgin Plastic Price Competition, Pyrolysis Oil Discount & Project Economics Risk

- Permitting, Waste Classification, Emission Regulation & Community Opposition Risk

- Mass Balance Certification Credibility, Greenwashing Claims & Regulatory Scrutiny Risk

- Regulatory Framework & Standards

- EU End-of-Waste Criteria, Waste Framework Directive & Chemical Recycling Feedstock Classification Frameworks

- Recycled Content Mandates, Packaging & Packaging Waste Regulation (PPWR) & Chemical Recycling Credit Eligibility

- ISCC PLUS, REDcert2 & Mass Balance Certification Standards for Chemically Recycled Plastic Feedstock

- FDA, EFSA & Food Contact Recycled Plastic Feedstock Safety & Approval Standards

- Air Emission, Waste Gas Treatment & Environmental Permitting Standards for Pyrolysis & Gasification Facilities

- UN Global Plastics Treaty, Extended Producer Responsibility (EPR) & Chemical Recycling Role in National Plastic Commitments

- Global Plastic Waste-to-Feedstock Technologies Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Tonnes of Plastic Waste Processed & Feedstock Output, MTPA)

- Market Size & Forecast by Technology

- Pyrolysis (Thermal Pyrolysis, Catalytic Pyrolysis & Flash Pyrolysis)

- Gasification (Plasma Gasification & Conventional High-Temperature Gasification)

- Dissolution & Solvent-Based Purification (Polyolefin Extraction)

- Depolymerisation: Glycolysis, Methanolysis & Hydrolysis for PET & Nylon Recycling

- Hydrocracking & Hydrotreating of Pyrolysis Oil to Naphtha & Diesel Fractions

- Steam Cracking Integration of Pyrolysis Oil & Chemical Recycling Feedstock

- Enzymatic & Biological Depolymerisation of PET & Polyurethane

- Co-Processing of Plastic-Derived Feedstock in Fluid Catalytic Crackers (FCC)

- Market Size & Forecast by Plastic Waste Feedstock Type

- Polyolefin Waste (Polyethylene & Polypropylene Film & Rigid Packaging)

- Polystyrene & Expanded Polystyrene (EPS) Waste

- PET Waste (Post-Consumer Bottles, Trays & Textiles)

- Mixed Plastic Waste Streams

- Difficult-to-Recycle & Multi-Layer Packaging Waste

- Industrial & Commercial Plastic Waste (Off-Spec & Production Scrap)

- Marine, Ocean-Recovered & Contaminated Plastic Waste

- Market Size & Forecast by Output Product

- Pyrolysis Oil (Plastic-Derived Pyrolysis Oil, PO & CPO)

- Naphtha & Gasoline Fraction from Pyrolysis Oil Hydrotreatment

- Syngas (CO & H2 Mix) from Gasification

- Monomer Output: Ethylene, Propylene & Styrene from Depolymerisation & Cracking

- Purified Polymer Pellet from Dissolution Processes (Polyolefin & PVC)

- Recycled PET Monomer: BHET, DMT & TPA from PET Glycolysis & Methanolysis

- Market Size & Forecast by Plant Scale

- Small-Scale & Modular Units (Below 5,000 Tonnes per Year)

- Mid-Scale Plants (5,000 to 50,000 Tonnes per Year)

- Large-Scale & Industrial Plants (50,000 to 200,000 Tonnes per Year)

- Mega-Scale & Integrated Petrochemical Complex Plants (Above 200,000 Tonnes per Year)

- Market Size & Forecast by Application

- Circular Plastics: Recycled Feedstock Supply to Polyolefin & Petrochemical Producers

- Packaging Supply Chain: Brand Owner Recycled Content Target Fulfilment

- Fuel & Energy Recovery from Plastic Waste Pyrolysis Oil

- Textile & Fibre: Recycled PET Monomer for Polyester Fibre Production

- Specialty Chemical & Solvent Production from Plastic-Derived Feedstock

- Market Size & Forecast by End-User

- Integrated Petrochemical & Polymer Producers (Cracker-to-Polymer)

- Independent Chemical Recycling Technology Operators

- Waste Management & Plastic Sorting Companies

- Brand Owners, Consumer Goods & Packaging Companies

- Fuel Blenders & Refineries Processing Pyrolysis Oil

- Government, Municipal Authorities & EPR Scheme Operators

- Market Size & Forecast by Sales Channel

- Technology Licence & Royalty Agreement Channel

- EPC & Turnkey Plant Delivery Channel

- Joint Venture, Co-Investment & Build-Own-Operate Channel

- Feedstock Offtake Agreement & Long-Term Supply Contract Channel

- North America Plastic Waste-to-Feedstock Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Tonnes Processed & Feedstock Output, MTPA)

- By Technology

- By Plastic Waste Feedstock Type

- By Output Product

- By Plant Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Plastic Waste-to-Feedstock Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Tonnes Processed & Feedstock Output, MTPA)

- By Technology

- By Plastic Waste Feedstock Type

- By Output Product

- By Plant Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Plastic Waste-to-Feedstock Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Tonnes Processed & Feedstock Output, MTPA)

- By Technology

- By Plastic Waste Feedstock Type

- By Output Product

- By Plant Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Plastic Waste-to-Feedstock Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Tonnes Processed & Feedstock Output, MTPA)

- By Technology

- By Plastic Waste Feedstock Type

- By Output Product

- By Plant Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Plastic Waste-to-Feedstock Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Tonnes Processed & Feedstock Output, MTPA)

- By Technology

- By Plastic Waste Feedstock Type

- By Output Product

- By Plant Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Plastic Waste-to-Feedstock Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Tonnes Processed & Feedstock Output, MTPA)

- By Technology

- By Plastic Waste Feedstock Type

- By Output Product

- By Plant Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- *Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Germany, France, United Kingdom, Netherlands, Belgium, Spain, Italy, Sweden, Norway, Japan, South Korea, China, India, Australia, Singapore, Malaysia, Brazil, Chile, Saudi Arabia, UAE, South Africa

- Technology Landscape & Innovation Analysis

- Pyrolysis Technology Deep-Dive: Reactor Design (Rotary Kiln, Screw, Auger, Fluidised Bed), Catalyst Systems & Oil Quality

- Hydrocracking & Hydrotreating of Pyrolysis Oil Technology: Contaminant Removal, Yield Optimisation & Naphtha Specification

- PET Chemical Recycling Technology Comparison: Glycolysis, Methanolysis, Hydrolysis & Enzymatic (Carbios) Routes

- Dissolution & Solvent-Based Polyolefin Purification Technology: Newcycling, PureCycle & CreaSolv Process Design

- Plasma Gasification & High-Temperature Gasification Technology for Mixed & Contaminated Plastic Waste Streams

- Steam Cracker & FCC Co-Processing of Pyrolysis Oil: Integration Challenges, Yield Impact & Cracker Acceptance Specifications

- AI-Based Sorting, Automated Feedstock Preparation & Digital Twin Technology for Chemical Recycling Plant Operations

- Patent & IP Landscape in Plastic Waste-to-Feedstock Technologies

- Value Chain & Supply Chain Analysis

- Post-Consumer Plastic Waste Collection, Sorting & Pre-Treatment Supply Chain

- Industrial & Commercial Plastic Scrap Aggregation & Feedstock Preparation Supply Chain

- Chemical Recycling Reactor, Process Equipment & Engineering Supply Chain

- Catalyst, Solvent, Process Chemical & Consumable Supply Chain for Chemical Recycling

- Pyrolysis Oil, Naphtha & Output Feedstock Storage, Blending & Logistics Supply Chain

- Technology Licensor, EPC Contractor & Plant Integration Channel

- Petrochemical Offtaker, Polymer Producer & Brand Owner Certification Channel

- Pricing Analysis

- Pyrolysis Oil & Chemical Recycling Output Feedstock Price vs. Virgin Naphtha Benchmark Analysis

- Chemical Recycling Plant Capital Cost (Capex) & Operating Cost (Opex) Analysis by Technology & Scale

- Levelised Cost of Chemical Recycling (LCOCR) Analysis by Technology Route & Plastic Waste Feedstock Type

- Plastic Waste Feedstock Gate Fee, Negative Cost & Tipping Fee Economics Analysis

- Recycled Content Premium: Brand Owner Willingness-to-Pay & Certified Circular Polymer Price Premium Analysis

- Technology Licence Fee, Royalty Rate & EPC Cost Structure Analysis by Leading Technology Providers

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Plastic Waste-to-Feedstock Technologies: GHG Emissions vs. Incineration, Landfill & Mechanical Recycling

- Carbon Footprint of Chemical Recycling: Process Energy, Hydrogen Use & Net GHG Reduction Quantification

- Mass Balance Accounting, ISCC PLUS Certification & Circular Polymer Attribution Methodology

- Plastic Waste Diversion, Ocean Plastic Leakage Reduction & SDG 14 (Life Below Water) Contribution

- Role of Chemical Recycling in National Plastic Waste Reduction Targets, EPR Scheme Compliance & Circular Economy Goals

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Technology & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Technology, Output Product & Geography

- Player Classification

- Dedicated Chemical Recycling Technology Developers & Licensors

- Integrated Petrochemical Majors Investing in Chemical Recycling Capacity

- Waste Management Companies Deploying Chemical Recycling Technologies

- PET Chemical Recycling Specialists (Glycolysis, Methanolysis & Enzymatic Route)

- Dissolution & Solvent-Based Purification Technology Companies

- Pyrolysis Oil Hydrotreatment & Upgrading Technology Providers

- Competitive Analysis Frameworks

- Market Share Analysis by Technology, Output Product & Region

- Company Profile

- Company Overview & Headquarters

- Plastic Waste-to-Feedstock Technology Portfolio & Process Description

- Key Customer Relationships, Offtake Agreements & Brand Owner Partnerships

- Plant Footprint, Operational Capacity & Annual Plastic Waste Processing Volume

- Revenue (Chemical Recycling Segment) & Funding Raised

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Plant Commissioning, Licensing Deals, Scale-Up Milestones)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Maturity vs. Processing Scale)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Technology, Feedstock Type, Output Product, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Technology Development, Scale-Up & Commercialisation Strategy

- Feedstock Procurement, Waste Supply Chain & Pre-Treatment Strategy

- Geographic Expansion & New Market Entry Strategy

- Offtake Partner, Brand Owner & Petrochemical Customer Engagement Strategy

- Partnership, Licensing, JV & Ecosystem Strategy

- Regulatory Engagement, Certification & Policy Advocacy Strategy

- Sustainability, LCA & Circular Economy Communication Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output