Global Power Cables Market By Voltage Range, By Installation Type, By Conductor Material, By Insulation Type, By End Use Application, By End User, By Region, Competition, Forecast & Opportunities, 2021-2036F

Market Definition

The Global Power Cables Market encompasses the design, manufacture, and commercial supply of insulated electrical conductors used to transmit and distribute electrical power across low, medium, high, and extra-high voltage applications, including overhead transmission lines, underground and submarine cable systems, building wiring, industrial power distribution, and renewable energy grid connection infrastructure, fabricated from copper and aluminum conductors with polymeric, cross-linked polyethylene, paper, and rubber insulation systems, procured by utilities, construction contractors, industrial operators, and renewable energy developers globally.

Market Insights

The global power cables market is entering a period of historically elevated and structurally sustained demand, driven by the simultaneous requirements of expanding grid infrastructure to accommodate accelerating renewable energy capacity additions, replacing ageing transmission and distribution cable networks approaching end of operational life across developed economies, electrifying transportation and industrial systems that previously relied on fossil fuel energy, and connecting offshore wind farms and remote solar generation assets to load centers through subsea and underground high-voltage cable systems. The market was valued at approximately USD 198.4 billion in 2025 and is projected to advance at a compound annual growth rate of 7.6% through 2034, as the global energy transition imposes unprecedented cable infrastructure investment requirements that are straining the manufacturing and installation capacity of the global power cable supply chain across virtually every voltage class and installation environment.

High-voltage direct current cable systems are registering the most dynamic investment growth within the global power cable market, driven by the construction of long-distance offshore wind transmission corridors, cross-border electricity grid interconnections between national power markets, and point-to-point renewable energy export links connecting resource-rich generation zones to distant consumption centers, all of which require the low line losses, controllable power flow, and submarine installation suitability of high-voltage direct current technology over the alternating current transmission alternatives. The offshore wind sector is the single most transformative demand driver for high-voltage cable manufacturers, as each gigawatt of offshore wind capacity requires multiple hundred kilometers of inter-array medium voltage cables and high-voltage export cables connecting wind turbine arrays to onshore grid connection points, with the accelerating deployment of floating offshore wind platforms at greater water depths and distances from shore further amplifying cable length, technical specification, and material quantity requirements per unit of installed capacity.

The underground cable segment is gaining procurement share relative to overhead transmission lines across multiple markets, driven by urban density constraints that preclude overhead line installation in built environments, growing public and regulatory opposition to visual and electromagnetic impact of overhead lines in sensitive landscapes, and the superior resilience of underground cables to storm damage and extreme weather events that is increasingly prioritized by transmission system operators managing grid reliability under more frequent climate-related disruption scenarios. Cross-linked polyethylene insulation has established its position as the dominant insulation technology across medium, high, and extra-high voltage underground and submarine cables, displacing paper-insulated lead-sheathed cable in legacy grid replacement programs through its combination of superior electrical performance at elevated operating temperatures, reduced environmental liability from lead elimination, lower installed weight, and compatibility with modern splicing and termination techniques. The distribution cable segment serving last-mile residential and commercial power delivery is experiencing growing procurement volumes driven by grid densification for electric vehicle charging infrastructure integration, residential rooftop solar and battery storage system connection, and smart grid sensor and communication equipment power supply across expanding distribution network automation programs.

Europe is the largest and most investment-intensive regional market for high-voltage and submarine power cables, driven by the scale of offshore wind development across the North Sea and Baltic Sea, the accelerating buildout of pan-European grid interconnections supporting cross-border renewable energy trading under the European Union energy transition policy framework, and the replacement of ageing high-voltage transmission infrastructure installed during the mid-twentieth century electricity system expansion. Asia-Pacific represents the largest regional market by total cable volume, anchored by the scale of Chinese power grid investment, the pace of Indian transmission and distribution infrastructure expansion, and the growing offshore wind development programs across South Korea, Taiwan, Japan, and Vietnam. North America is registering an accelerating procurement cycle driven by long-deferred grid modernization investment, federal transmission permitting reform advancing large-scale interstate transmission projects, and the scale of renewable energy interconnection queue volumes that require transmission infrastructure expansion to reach commercial operation.

Key Drivers

Renewable Energy Grid Integration and Offshore Wind Transmission Infrastructure Investment Generating Unprecedented High-Voltage and Submarine Cable Procurement Demand Across Global Markets

The accelerating deployment of utility-scale solar, onshore wind, and offshore wind generation capacity across Europe, North America, Asia-Pacific, and the Middle East is creating massive cable infrastructure investment requirements for connecting generation assets to transmission grids, constructing inter-array collection systems within wind and solar farms, and building long-distance high-voltage direct current transmission links that enable renewable energy to be transported from resource-rich generation zones to population and industrial load centers across distances of hundreds to thousands of kilometers. Offshore wind development in particular is generating exceptional cable procurement volumes, as each project requires submarine inter-array medium voltage cables, high-voltage export cables, and onshore cable landing infrastructure whose combined length and material requirements substantially exceed those of equivalent capacity onshore generation projects connected to proximate grid infrastructure.

Grid Modernization, Transmission Capacity Expansion, and Ageing Infrastructure Replacement Programs Sustaining Multi-Decade Cable Procurement Cycles Across Both Developed and Developing Economy Markets

Electricity transmission and distribution infrastructure across North America, Europe, Japan, and Australia includes substantial inventories of cables installed during the mid-to-late twentieth century grid expansion period that are approaching or exceeding design operational lifespans, exhibiting insulation degradation, increased fault rates, and declining capacity margins that require systematic replacement programs generating sustained cable procurement demand independent of new capacity additions. In developing economies across Asia, Africa, and Latin America, rapid urbanization, industrial development, and rural electrification programs are driving primary grid capacity expansion investment that requires extensive cable procurement across all voltage levels, with transmission infrastructure development pacing ahead of electricity demand growth to support economic expansion ambitions that require reliable, adequate, and affordable electricity supply as a foundational enabling infrastructure.

Transportation Electrification and Industrial Decarbonization Creating New Low and Medium Voltage Cable Demand Vectors Across Electric Vehicle Charging, Rail Electrification, and Industrial Load Conversion

The accelerating adoption of battery electric vehicles is generating growing demand for low and medium voltage cables in electric vehicle charging infrastructure, including charging station supply cables, smart charging aggregation network wiring, and distribution network reinforcement cables required to support elevated residential and commercial electricity loads from large-scale electric vehicle charging activity. Railway electrification programs converting diesel locomotive operations to overhead catenary and third-rail electric power supply across South Asia, Southeast Asia, Africa, and parts of Europe are creating additional medium voltage cable procurement demand, while the electrification of industrial process heating, motor drives, and material handling systems in decarbonizing manufacturing facilities is expanding the industrial low voltage cable market beyond its historical growth trajectory driven primarily by new construction activity.

Key Challenges

Copper and Aluminum Conductor Raw Material Price Volatility and Supply Chain Concentration Risks Creating Cost Uncertainty and Margin Pressure Across Power Cable Manufacturing Operations

Copper is the primary conductor material in medium, high, and extra-high voltage power cables and the dominant conductor in low voltage building and industrial wiring applications, and its price is subject to significant volatility driven by global copper mining production dynamics, inventory cycle fluctuations on commodity exchanges, speculative trading activity, and structural demand growth from the energy transition creating persistent long-term supply tightness that threatens to sustain elevated copper prices throughout the forecast period. The geographic concentration of copper mining in Chile, Peru, the Democratic Republic of Congo, and China creates supply chain vulnerability to operational, geopolitical, and environmental disruption that can propagate price shocks through cable manufacturing supply chains with limited ability to substitute lower-cost aluminum conductors in applications where copper conductivity, jointing characteristics, or installation space constraints make aluminum substitution technically impractical.

High-Voltage and Submarine Cable Manufacturing Capacity Constraints and Long Lead Times Creating Supply Bottlenecks That Risk Delaying Offshore Wind and Transmission Infrastructure Programs

The global manufacturing capacity for high-voltage direct current submarine power cables and high-voltage alternating current export cables is concentrated among a small number of specialized cable manufacturers with limited production facilities capable of producing the continuous cable lengths, high voltage ratings, and specialized armoring required for offshore wind and long-distance submarine interconnection projects, creating a supply bottleneck that is already manifesting in extended delivery lead times of three to five years for large submarine cable contracts and project procurement competition that is driving cable price escalation across the offshore wind supply chain. The capital investment required to establish new high-voltage submarine cable manufacturing capacity is substantial and the construction timeline for new facilities extends three to five years from investment decision, constraining the pace at which supply capacity can expand to meet the accelerating project pipeline.

Permitting Delays and Right-of-Way Acquisition Complexity for Underground and Submarine Cable Transmission Projects Extending Project Timelines and Increasing Development Cost Uncertainty

Underground power cable transmission projects require obtaining land access rights, environmental impact assessment approvals, local authority consenting, and in many jurisdictions lengthy public inquiry processes that can extend total project development timelines by multiple years beyond the cable procurement and installation period, creating development cost uncertainty and investment decision delays that affect the offtake revenues and financing structures of renewable energy projects dependent on transmission connection. Submarine cable projects face additional complexity from seabed survey requirements, marine protected area routing constraints, fisheries stakeholder consultations, port access and cable-laying vessel availability limitations, and international maritime boundary crossing approvals that further complicate project scheduling and can introduce schedule dependencies beyond the direct control of project developers.

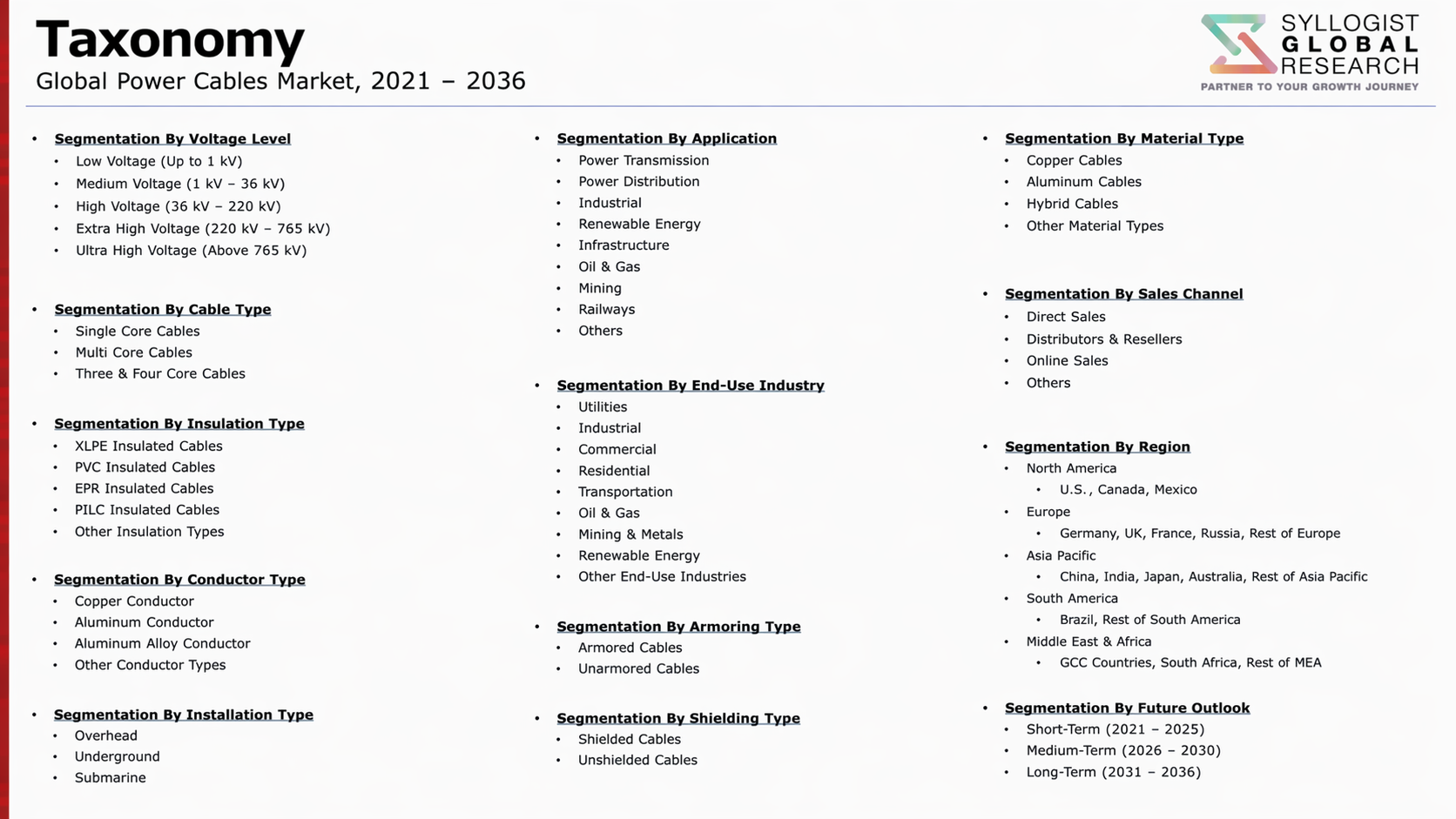

Market Segmentation

- Segmentation By Voltage Range

- Low Voltage Cables (Below 1 kV)

- Medium Voltage Cables (1 kV to 36 kV)

- High Voltage Cables (36 kV to 220 kV)

- Extra-High Voltage Cables (Above 220 kV)

- High Voltage Direct Current Cables

- Segmentation By Installation Type

- Overhead Transmission Lines and Conductors

- Underground Land Cables

- Submarine and Subsea Cables

- Building and Indoor Wiring Cables

- Industrial Plant and Tray Cables

- Others

- Segmentation By Conductor Material

- Copper Conductor Cables

- Aluminum Conductor Cables

- Aluminum Conductor Steel-Reinforced Cables

- Optical Fiber Composite Power Cables

- Others

- Segmentation By Insulation Type

- Cross-Linked Polyethylene Insulated Cables

- Polyvinyl Chloride Insulated Cables

- Ethylene Propylene Rubber Insulated Cables

- Paper and Oil-Insulated Cables

- Gas-Insulated Cables

- Others

- Segmentation By End Use Application

- Electricity Transmission and Grid Interconnection

- Power Distribution and Last-Mile Delivery

- Offshore Wind Farm Inter-Array and Export

- Building and Construction Wiring

- Industrial Power Distribution and Process Facilities

- Electric Vehicle Charging Infrastructure

- Rail and Transportation Electrification

- Others

- Segmentation By End User

- Electric Utilities and Transmission System Operators

- Renewable Energy Project Developers

- Construction and Engineering Contractors

- Industrial and Manufacturing Corporations

- Government and Public Infrastructure Agencies

- Oil, Gas, and Petrochemical Operators

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global power cables market valuation in 2025, projected through 2034, segmented by voltage range, installation type, and end use application, enabling cable manufacturers, utility procurement teams, and infrastructure investors to identify the highest-growth cable categories and most durable procurement demand opportunities across the global power cable landscape?

- How are offshore wind farm expansion programs, long-distance high-voltage direct current interconnection projects, and cross-border electricity trading infrastructure investments shaping submarine and high-voltage cable procurement volumes, technical specification requirements, and delivery lead time expectations across European, Asia-Pacific, and North American markets through 2034?

- What manufacturing capacity constraints, delivery lead time extensions, and supply bottlenecks are affecting the high-voltage and submarine cable segment, and what new factory investment programs, capacity expansion timelines, and supply chain development initiatives among leading cable manufacturers are being pursued to address the growing gap between project pipeline demand and available production capacity?

- How is the competitive landscape structured among global integrated cable manufacturers, regional cable producers, and specialty high-voltage cable suppliers, and what technology development, manufacturing capacity investment, project financing capability, vertical integration of conductor and insulation materials, and geographic market expansion strategies are enabling leading cable companies to capture share in the highest-value cable segments?

- How are copper and aluminum conductor raw material price dynamics, supply chain concentration risks from geographically constrained mining production, and the long-term structural demand growth for copper from energy transition applications shaping cable manufacturer procurement strategies, conductor material substitution decisions, and raw material hedging and pricing mechanism structures in long-term cable supply agreements?

- What transmission permitting reform initiatives, right-of-way acquisition frameworks, environmental impact assessment streamlining programs, and offshore cable route planning coordination mechanisms are governments and transmission system operators implementing to accelerate cable infrastructure project development timelines and reduce the permitting-related schedule delays that are constraining grid expansion and renewable energy connection programs?

- Which regional cable markets, specifically Asia-Pacific, Europe, and North America, are expected to generate the highest incremental procurement growth through 2034, and what combinations of renewable energy integration investment, grid modernization and replacement programs, transportation electrification demand, and industrial load growth are defining cable procurement volume trajectories and technology specification priorities in each regional market?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Copper & Aluminium Price Volatility, Raw Material Cost Fluctuation & Commodity Cycle Risk

- Supply Chain Bottleneck, Long Lead Time & Order Backlog Risk for High-Voltage & Subsea Cable Projects

- Cable Installation Complexity, Offshore Weather Delay & Subsea Project Execution Risk

- Regulatory Permitting, Grid Connection Delay & Transmission Corridor Rights-of-Way Risk

- Technology Transition, HVDC Market Shift & Stranded HVAC Asset Risk

- Regulatory Framework & Standards

- IEC 60228, IEC 60502 & IEC 60840 Power Cable Design, Testing & Performance Standards

- HVDC Cable Standards: IEC 62895, CIGRE Technical Brochures & Qualification Test Protocols for Extruded HVDC Cables

- Submarine & Offshore Cable Standards: IEC 60287 Ampacity, DNV-ST-0359 & IEEE 1580 Subsea Cable Requirements

- Fire Performance & Low-Smoke Halogen-Free (LSZH) Cable Standards: IEC 60332, EN 50575 & CPR Construction Products Regulation

- Grid Connection, Transmission Network Planning & Offshore Wind Cable Regulatory Frameworks by Jurisdiction

- Environmental, RoHS, REACH & Restricted Substance Standards for Power Cable Materials & Insulation

- Global Power Cables Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (km & Tonnes of Conductor)

- Market Size & Forecast by Voltage Level

- Low Voltage (LV) Power Cables (Below 1 kV)

- Medium Voltage (MV) Power Cables (1 kV to 36 kV)

- High Voltage (HV) Power Cables (36 kV to 150 kV)

- Extra High Voltage (EHV) Power Cables (150 kV to 500 kV)

- Ultra High Voltage (UHV) Power Cables (Above 500 kV)

- Market Size & Forecast by Technology

- HVAC (High Voltage Alternating Current) Cables

- HVDC (High Voltage Direct Current) Cables

- Mass-Impregnated Non-Draining (MIND) HVDC Cables

- Cross-Linked Polyethylene (XLPE) Insulated Power Cables

- Ethylene Propylene Rubber (EPR) Insulated Power Cables

- Low-Smoke Zero-Halogen (LSZH) & Fire-Resistant Power Cables

- Superconducting Power Cables

- Market Size & Forecast by Conductor Material

- Copper Conductor Power Cables

- Aluminium Conductor Power Cables

- Aluminium Alloy Conductor Power Cables

- Composite & Specialty Conductor Power Cables

- Market Size & Forecast by Installation Type

- Underground & Direct Buried Power Cables

- Overhead Power Cables & Aerial Bundled Conductors (ABC)

- Submarine & Subsea Power Cables

- Cable Duct, Tray & Conduit Installed Power Cables

- Market Size & Forecast by Application

- Transmission Grid Infrastructure & Interconnection Links

- Distribution Network Upgrades, Grid Expansion & Smart Grid Projects

- Offshore Wind Farm Array & Export Cables

- Onshore Renewable Energy (Solar PV & Wind) Grid Connection Cables

- Industrial, Oil & Gas & Petrochemical Facility Power Cables

- Data Centre & Critical Infrastructure Power Cables

- Railway, Metro & Transportation Electrification Cables

- Building, Construction & Commercial Real Estate Power Cables

- EV Charging Infrastructure & E-Mobility Power Cables

- Market Size & Forecast by End-User

- Electric Utilities, Transmission System Operators (TSOs) & Distribution Network Operators (DNOs)

- Renewable Energy Developers (Wind, Solar & Hybrid)

- Oil & Gas, Petrochemical & Mining Companies

- Industrial & Manufacturing Facilities

- Construction, Real Estate & Commercial Building Contractors

- Railway, Transport & Infrastructure Authorities

- Data Centre & Hyperscale Technology Companies

- Government & Public Sector Infrastructure Programmes

- Market Size & Forecast by Sales Channel

- Direct OEM & Cable Manufacturer Sales

- EPC Contractor & Project Developer Channel

- Electrical Distributor & Wholesaler Network

- Government Tender & Public Utility Procurement Channel

- Online & Digital Procurement Platform Channel

- North America Power Cables Market Outlook

- Market Size & Forecast

- By Value

- By Volume (km & Tonnes of Conductor)

- By Voltage Level

- By Technology

- By Conductor Material

- By Installation Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Power Cables Market Outlook

- Market Size & Forecast

- By Value

- By Volume (km & Tonnes of Conductor)

- By Voltage Level

- By Technology

- By Conductor Material

- By Installation Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Power Cables Market Outlook

- Market Size & Forecast

- By Value

- By Volume (km & Tonnes of Conductor)

- By Voltage Level

- By Technology

- By Conductor Material

- By Installation Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Power Cables Market Outlook

- Market Size & Forecast

- By Value

- By Volume (km & Tonnes of Conductor)

- By Voltage Level

- By Technology

- By Conductor Material

- By Installation Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Power Cables Market Outlook

- Market Size & Forecast

- By Value

- By Volume (km & Tonnes of Conductor)

- By Voltage Level

- By Technology

- By Conductor Material

- By Installation Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Power Cables Market Outlook

- Market Size & Forecast

- By Value

- By Volume (km & Tonnes of Conductor)

- By Voltage Level

- By Technology

- By Conductor Material

- By Installation Type

- By Application

- By End-User

- By Country

- By Sales Channel

- *Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Italy, Denmark, Norway, Sweden, China, Japan, South Korea, India, Australia, Singapore, Brazil, Chile, Saudi Arabia, UAE, Egypt, South Africa, Israel

- Market Size & Forecast

- Technology Landscape & Innovation Analysis

- Extruded HVDC Cable Technology Deep-Dive: XLPE Insulation, Long-Length Manufacturing, Jointing & Qualification Testing

- Submarine Cable Technology: Armoured Design, Dynamic Riser Cables, Umbilicals & Offshore Wind Array Cable Systems

- LSZH, Halogen-Free & Fire-Resistant Cable Technology: Compound Development, Performance Testing & Building Regulation Compliance

- Superconducting Cable Technology: HTS Materials, Cryogenic Cooling & Urban Grid Congestion Relief Applications

- Cable Monitoring, Partial Discharge Detection & Digital Asset Management Technology for Transmission & Distribution Cables

- Recyclable, Bio-Based & Sustainable Cable Insulation & Sheathing Material Technology

- High-Ampacity Conductor Technology: ACSS, ACCC, Gap Conductor & Compacted Stranded Conductor Innovations

- Patent & IP Landscape in Power Cable Technologies

- Value Chain & Supply Chain Analysis

- Copper & Aluminium Rod, Wire Rod & Refined Metal Supply Chain

- XLPE, EPR, LSZH & Specialty Polymer Insulation Compound Supply Chain

- Steel Wire Armour, Lead Sheath, Tape & Metallic Screen Supply Chain

- Cable Stranding, Extrusion, Insulation & Sheathing Manufacturing Supply Chain

- Cable Drum, Reel, Packaging & Logistics Supply Chain

- Cable Accessories: Joints, Terminations, Connectors & Hardware Supply Chain

- EPC Contractor, Cable Laying Vessel & Installation Services Channel

- Utility, Developer & Industrial End-User Procurement Channel

- Pricing Analysis

- Power Cable Unit Price Analysis by Voltage Level, Conductor Material & Cross-Section

- Copper vs. Aluminium Conductor Price Parity & Cost Comparison Analysis

- HVDC vs. HVAC Cable System Total Installed Cost & Levelised Transmission Cost Comparison

- Subsea & Offshore Wind Export Cable Project Cost Analysis: Supply, Installation & Commissioning

- Impact of Copper & Aluminium LME Price Movements on Power Cable Pricing

- Cable Accessories, Jointing & Termination System Cost Structure Analysis

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Power Cables: Carbon Footprint, Copper & Aluminium Extraction Impact & End-of-Life Recyclability

- Role of Power Cables in Enabling Grid Decarbonisation: Offshore Wind, Solar & HVDC Interconnector Infrastructure

- Halogen-Free, Recyclable & Bio-Based Cable Material Development for Reduced Environmental Impact

- Subsea Cable Environmental Impact: Benthic Habitat, EMF Effects & Marine Ecology Mitigation Measures

- SDG 7 (Affordable Clean Energy), SDG 9 (Infrastructure) & SDG 13 (Climate Action) Alignment & Green Finance Eligibility

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Voltage Level & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Voltage Level, Application & Geography

- Player Classification

- Global Integrated Cable Manufacturers (Full Voltage Range & Subsea Capability)

- Specialist High Voltage & Extra High Voltage Cable Manufacturers

- Specialist Submarine & Offshore Cable Manufacturers

- Low & Medium Voltage Cable Specialists & Regional Manufacturers

- Cable Accessories, Joints & Termination System Providers

- Cable Installation, Marine Laying & Offshore Services Companies

- Competitive Analysis Frameworks

- Market Share Analysis by Voltage Level, Technology & Region

- Company Profile

- Company Overview & Headquarters

- Power Cable Products & Technology Portfolio

- Key Customer Relationships & Reference Project Installations

- Manufacturing Footprint & Production Capacity

- Revenue (Power Cable Segment) & Order Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Capacity Expansion, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Voltage Level, Technology, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing Capacity Expansion & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output