Global Satellite Laser Communication Terminals Market By Component, By Orbit, By Laser Type, By Platform, By Data Rate, By Application, By End User, By Region, Competition, Forecast & Opportunities, 2021-2034F

Market Definition

The Global Satellite Laser Communication Terminals Market encompasses the design, development, manufacture, integration, and operational deployment of optical communication terminals (OCTs), pointing-acquisition-tracking modules, modems, signal processors, beam steering assemblies, lasers, and optical ground station infrastructure engineered to enable high-data-rate, low-latency, jamming-resistant laser-based connectivity between satellites in low Earth, medium Earth, geostationary, and cislunar orbits, and between satellites and ground stations, airborne platforms, and naval assets across commercial, defense, civil space, and scientific mission environments globally. Satellite laser communication terminals encompass functional product categories including small-form-factor optical transceiver terminals integrated into LEO broadband constellations, defense-grade SDA-compliant optical crosslinks supporting up to 100 Gbps data rates, optical ground stations equipped with adaptive optics and atmospheric compensation, airborne laser communication terminals for UAVs and high-altitude platforms, and emerging quantum key distribution payloads enabling cryptographically secure inter-satellite communications. The market addresses critical operational requirements including sub-microradian pointing accuracy, atmospheric turbulence compensation, beam acquisition and tracking through high-relative-velocity orbital geometries, multi-Gbps to multi-hundred-Gbps secure throughput, low probability of intercept and detection links resistant to electromagnetic interference and jamming, and seamless interoperability with legacy radio frequency communications infrastructure. End users span LEO mega-constellation operators, geostationary satellite operators, defense ministries, intelligence agencies, civil space agencies, Earth observation satellite providers, deep space mission operators, scientific research institutions, and commercial relay-as-a-service network providers, establishing satellite laser communication terminals as a foundational technology layer underpinning next-generation space-based broadband, secure defense connectivity, real-time Earth observation downlink, and emerging quantum networking ecosystems worldwide.

Market Insights

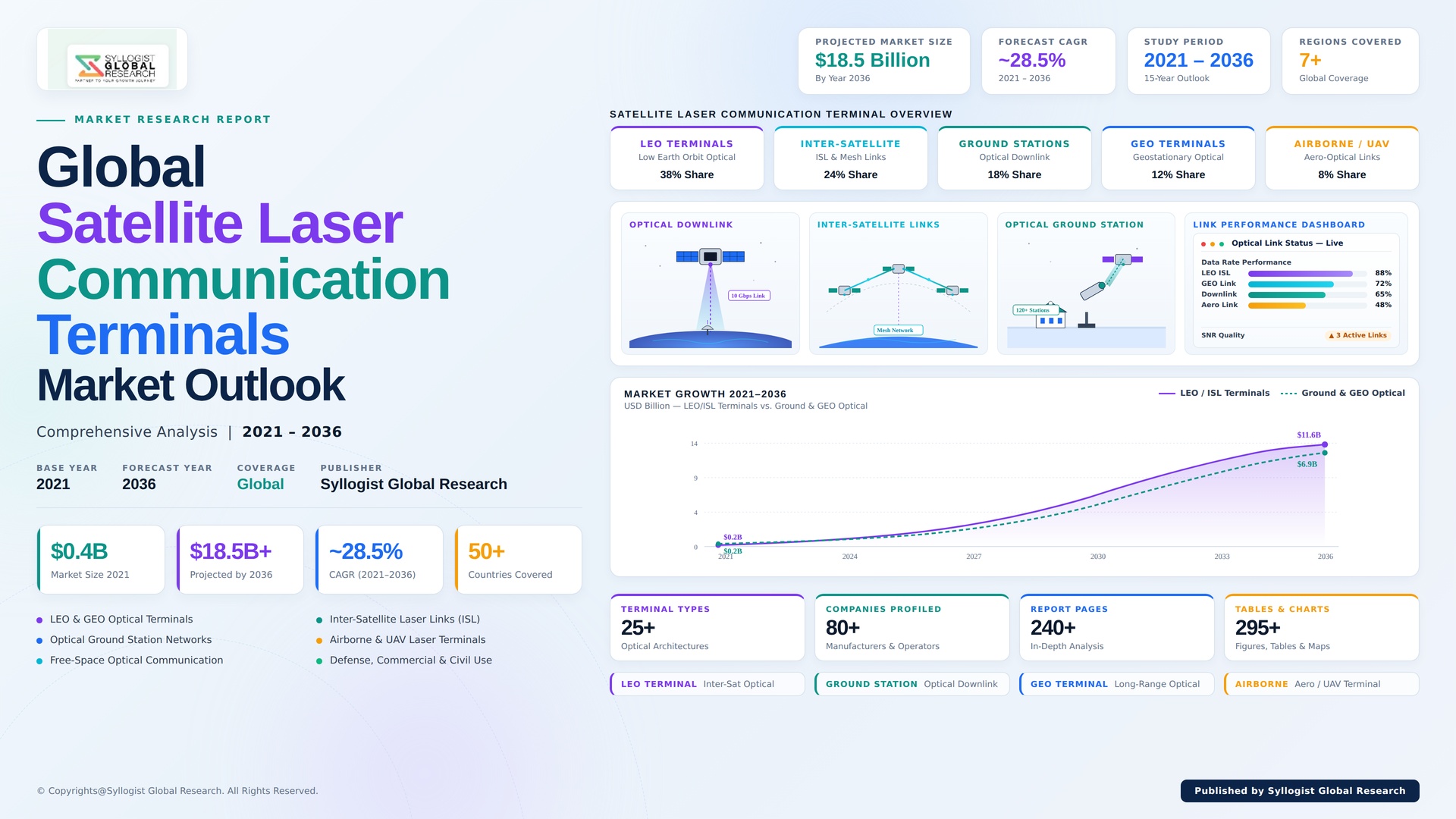

The global satellite laser communication terminals market is moving through an explosive growth phase shaped by accelerating LEO mega-constellation buildout, intensifying defense investment in quantum-ready secure space communications, escalating radio frequency spectrum congestion, and rapid technology maturation across optical transceiver miniaturization, pointing-acquisition-tracking precision, and high-data-rate modem performance enabling Gbps-class to multi-hundred-Gbps optical inter-satellite links across commercial and government space missions globally. The market was valued at USD 1.5 billion in 2025 and is projected to reach USD 14.0 billion by 2034, advancing at a compound annual growth rate of 28.1% through the forecast window, supported by Starlink, Project Kuiper, OneWeb, China Guowang, and IRIS2 broadband constellation rollouts incorporating optical inter-satellite links, accelerating Space Development Agency Tranche 1 and Tranche 2 Transport Layer optical crosslink deployments, and expanding civil and scientific deep space optical communication missions reshaping the global space communication architecture worldwide.

LEO mega-constellation architectural evolution is the strongest secular force restructuring the demand profile for satellite laser communication terminals, as constellation operators progressively recognize that radio frequency inter-satellite links cannot scale to meet the throughput, latency, and resilience requirements of next-generation broadband, Earth observation, and defense networks, compelling architectural redesign toward optical mesh networking spanning entire constellations. The result is a measurable shift in revenue mix from individual demonstration terminal programs toward fleet-scale serial production of small-form-factor optical transceivers compliant with Space Development Agency Optical Communications Terminal standards, supporting interoperability across multi-vendor satellite buses. Constellation operators are simultaneously deploying optical ground station networks delivered as Optical Ground Station as a Service models, restructuring procurement economics in favor of suppliers offering vertically integrated terminal manufacturing, fleet provisioning, and managed network services capable of supporting thousands of satellite endpoints across multi-orbit architectures globally throughout the forecast horizon.

Within the component taxonomy, optical transceiver terminals anchor the highest current revenue concentration, supported by serial production demand from broadband mega-constellation operators and defense-grade Space Development Agency-compliant programs. Pointing, acquisition, and tracking modules represent the highest-engineering-content component category, capturing critical design value owing to the sub-microradian precision required to maintain stable laser links across high relative velocity orbital geometries. Beam steering assemblies and adaptive optics modules are recording the steepest growth trajectories, expanding at rates above 26% annually as ground station networks scale to support fleet downlink demand. Fiber lasers dominate the laser type taxonomy with the largest share owing to high efficiency and proven space heritage, while semiconductor diode lasers are gaining momentum across compact small satellite applications. LEO platforms account for approximately 59% of revenue, while emerging cislunar, deep space, and airborne segments are reshaping competitive differentiation among integrated optical terminal suppliers.

North America anchors the largest absolute revenue share of the global satellite laser communication terminals market, valued near USD 600 million in 2025 and underpinned by Space Development Agency Proliferated Warfighter Space Architecture procurement, NASA optical communication missions, accelerating Starlink and Project Kuiper optical inter-satellite link deployments, and a deep ecosystem of US-based laser terminal manufacturers, photonic integrated circuit foundries, and optical ground station operators. Europe represents a structurally critical share driven by IRIS2 sovereign constellation development, German Space Agency Heinrich Hertz mission, and growing French, Italian, and United Kingdom defense optical communication procurement. Asia-Pacific is positioned to record the highest forecast period CAGR, supported by China Guowang and SatNet mega-constellation programs, expanding Japan JAXA optical mission portfolio, accelerating India ISRO laser communication development, and South Korean defense space communication programs. The Middle East contributes incremental demand through United Arab Emirates and Saudi Arabia space programs, while Latin America anchors regional growth through commercial Earth observation downlink applications.

Key Drivers

LEO Mega-Constellation Buildout and Optical Inter-Satellite Link Proliferation Driving Fleet-Scale Demand for Space-Qualified Laser Communication Terminals

Accelerating LEO mega-constellation buildout across Starlink, Project Kuiper, OneWeb, China Guowang, SatNet, and the European Union IRIS2 sovereign constellation is generating durable fleet-scale demand for space-qualified optical inter-satellite link terminals capable of delivering multi-Gbps secure connectivity across thousands of satellites without dependence on ground station relay. Constellation operators are codifying optical inter-satellite link requirements into satellite bus specifications, anchoring multi-year serial production volume commitments for laser terminal manufacturers across global commercial space supply chains throughout the forecast horizon and beyond.

Defense Space Architecture Modernization and Space Development Agency Proliferated Warfighter Space Architecture Programs Anchoring Premium Demand for Quantum-Ready Optical Crosslinks

Substantial defense investment across the Space Development Agency Tranche 1 and Tranche 2 Transport Layer, US Space Force Proliferated Warfighter Space Architecture, NATO allied military space communication programs, and Japanese, Australian, and South Korean defense space initiatives is anchoring premium demand for quantum-ready, jamming-resistant, low-probability-of-intercept optical communication terminals capable of supporting resilient mission-critical military space communications. Defense procurement urgency around Space Development Agency Optical Communications Terminal standards compliance is driving compressed acquisition timelines and elevated allocation for laser terminal vendors competing for multi-billion-dollar defense space communication contracts globally throughout the forecast horizon.

Radio Frequency Spectrum Congestion, Bandwidth Saturation, and Regulatory Constraints Driving Migration Toward Optical Communications Across Commercial and Civil Space Missions

Persistent radio frequency spectrum congestion across Ka, Ku, and V-band allocations, combined with International Telecommunication Union coordination delays, frequency assignment limitations, and regulatory restrictions on bandwidth expansion, is progressively driving constellation operators, Earth observation providers, and civil space agencies toward optical communications as the only architecturally sustainable path supporting next-generation throughput requirements. Commercial broadband, high-resolution Earth observation downlink, and deep space mission scaling all require optical solutions delivering orders-of-magnitude bandwidth advantages over RF, anchoring durable demand for satellite laser communication terminals across all mission categories worldwide throughout the forecast period.

Key Challenges

Atmospheric Attenuation, Cloud Cover Limitations, and Adaptive Optics Capital Intensity Constraining Optical Ground Station Network Expansion

Persistent atmospheric attenuation, cloud cover availability constraints, scintillation effects, and water vapor absorption fundamentally limit the operational availability of optical ground stations to geographically narrow climatic windows, particularly across tropical and high-latitude regions where weather variability disrupts laser downlink continuity. The substantial capital expenditure required for adaptive optics telescopes, atmospheric compensation hardware, and geographically diverse station siting to ensure aggregate constellation downlink availability constrains the pace of optical ground station network buildout, requiring innovative site diversity strategies, machine-learning-based weather prediction, and hybrid optical-RF backup architectures to address availability gaps throughout the forecast horizon globally.

Sub-Microradian Pointing, Acquisition, and Tracking Precision Requirements Driving Engineering Complexity and Production Scaling Burdens

Sub-microradian pointing, acquisition, and tracking precision requirements across high-relative-velocity LEO inter-satellite link geometries impose extraordinary engineering complexity spanning fine-steering mirror actuation, gimbal stabilization, beacon detection, vibration isolation, and thermal stability that materially elevate development timelines and unit production costs across satellite laser communication terminal manufacturing. Manufacturers face persistent production scaling challenges balancing sub-microradian precision against fleet-scale unit volume targets demanded by mega-constellation operators, requiring substantial automation investment, photonic integrated circuit advancement, and advanced manufacturing capability deployment across global laser terminal supply chains throughout the forecast period.

Critical Photonic Component Supply Chain Concentration, Gallium-Based Laser Diode Sourcing Constraints, and Geopolitical Trade Risk

Critical photonic component supply chain concentration, including gallium-based laser diodes, indium phosphide photonic integrated circuits, specialty optical fibers, and high-precision micro-optics, exposes satellite laser communication terminal manufacturers to material cost inflation, lengthening lead times, and geopolitical trade risk affecting cross-border component sourcing across the United States, Europe, China, and other major space industrial bases. Supply chain disruption risks compound procurement complexity for fleet-scale terminal production programs, while export control restrictions across optical communication technologies further complicate multinational program execution, pressuring delivery schedules and margin performance across both commercial mega-constellation and defense optical terminal production globally throughout the forecast period.

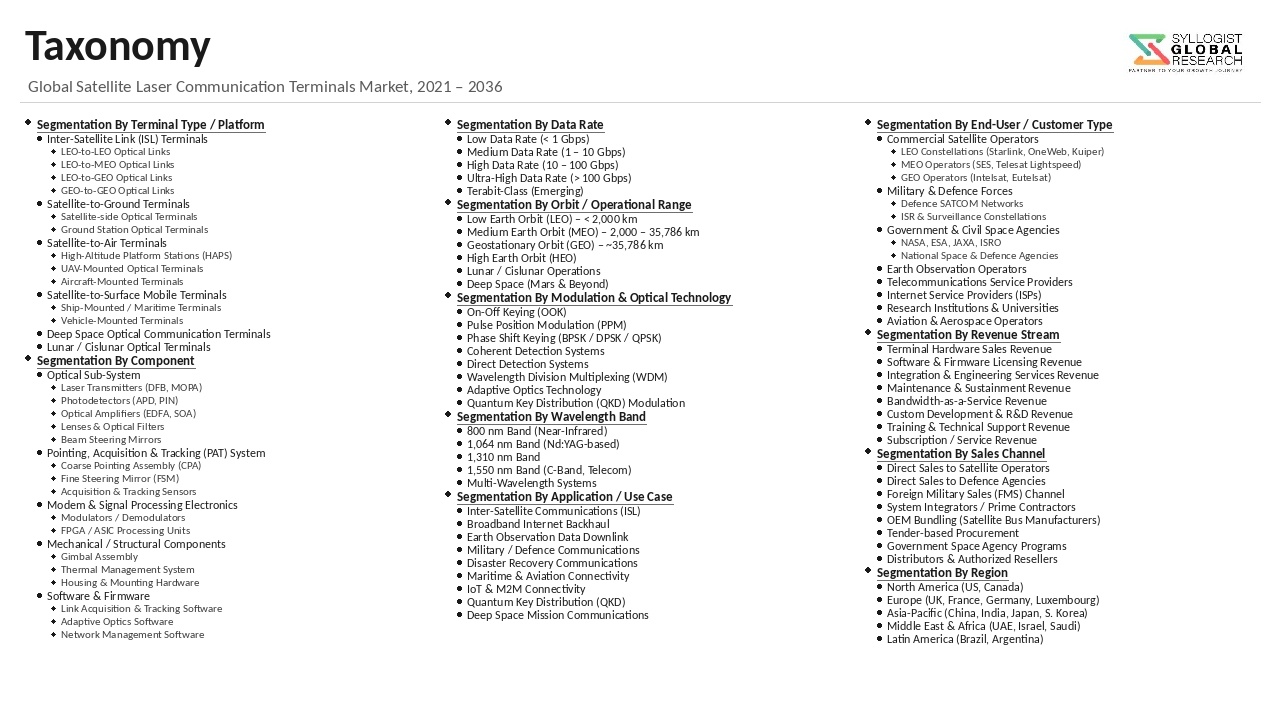

Market Segmentation

- Segmentation By Component

- Optical Transceiver Terminals

- Pointing, Acquisition, and Tracking (PAT) Modules

- Modems and Signal Processors

- Beam Steering Assemblies

- Lasers and Photodetectors

- Optical Ground Stations

- Adaptive Optics Modules

- Others

- Segmentation By Orbit

- Low Earth Orbit (LEO)

- Medium Earth Orbit (MEO)

- Geostationary Orbit (GEO)

- High Elliptical Orbit and Cislunar

- Deep Space

- Segmentation By Laser Type

- Fiber Lasers

- Semiconductor Diode Lasers

- Solid-State Lasers (Nd:YAG and Variants)

- Others

- Segmentation By Platform

- Satellite-Mounted Terminals

- Optical Ground Station Terminals

- Airborne Terminals (UAV, HAPS, Aircraft)

- Naval and Maritime Terminals

- Others

- Segmentation By Data Rate

- Up to 2.5 Gbps

- 5 Gbps to 10 Gbps

- 10 Gbps to 100 Gbps

- Above 100 Gbps

- Segmentation By Application

- Inter-Satellite Links (ISL) and Network Backbone

- Satellite-to-Ground Communications

- Satellite-to-Air and Satellite-to-Naval Communications

- Earth Observation Data Downlink

- Defense and Intelligence Communications

- Deep Space Communications

- Quantum Key Distribution and Secure Communications

- Others

- Segmentation By End User

- Government and Defense

- Commercial Satellite Operators and Mega-Constellations

- Civil Space Agencies

- Earth Observation and Remote Sensing Providers

- Academic and Scientific Research Institutions

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Satellite Laser Communication Terminals Market in 2025, projected through 2034, disaggregated by component, orbit, and application, enabling optical terminal manufacturers, satellite operators, defense contractors, and investors to identify highest-growth segments and most durable revenue opportunities across the global space-based laser communication landscape?

- How are LEO mega-constellation programs including Starlink, Project Kuiper, OneWeb, China Guowang, SatNet, and the European Union IRIS2 sovereign constellation reshaping demand requirements for optical inter-satellite link terminals, and which constellation buildout schedules are setting the technical and procurement benchmarks defining global laser communication terminal demand architecture through 2034?

- How are Space Development Agency Tranche 1 and Tranche 2 Transport Layer programs, US Space Force Proliferated Warfighter Space Architecture initiatives, and NATO allied military space communication priorities reshaping defense optical crosslink demand, quantum-ready encryption requirements, and Optical Communications Terminal standardization across global defense space markets?

- Which satellite laser communication terminal component categories, including optical transceivers, pointing-acquisition-tracking modules, beam steering assemblies, modems, and adaptive optics, are recording the highest forecast period growth rates, and what mission profile, orbit geometry, and data rate factors are shaping demand intensity within each segment?

- How are atmospheric attenuation, cloud cover availability, adaptive optics requirements, and geographic site diversity strategies shaping optical ground station network expansion economics, and what hybrid optical-RF backup architectures and machine-learning weather prediction approaches are most critical to ensuring downlink continuity globally?

- What partnership, vertical integration, photonic foundry investment, and acquisition strategies are dominant satellite laser communication terminal manufacturers using to consolidate market positions, secure critical photonic component supply chains, and deepen long-cycle relationships with mega-constellation operators, defense agencies, and civil space programs across global regions?

- Which regional markets, specifically Asia-Pacific, Europe, and the Middle East, are expected to generate the most substantial incremental satellite laser communication terminal procurement through 2034, and what indigenous constellation development, defense space modernization, and civil space exploration factors are driving capability investment priorities and supplier selection decisions across each market?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Atmospheric Attenuation, Cloud Cover & Site Diversity Reliability Risk for Space-to-Ground Links

- Pointing Accuracy, Microradian Jitter & Acquisition-Tracking-Pointing (ATP) Performance Risk

- Standards Interoperability (CCSDS, SDA OCT v3.x) & Multi-Vendor Crosslink Compatibility Risk

- Critical Component (Space-Qualified Laser, Photonic IC, Beryllium Mirror) Supply Risk

- Defence Procurement Cycle, Constellation Operator Bankruptcy & Programme Cancellation Risk

- Regulatory Framework & Standards

- CCSDS Optical Communications Standards (CCSDS 141.x and 142.x) & International Standardisation Frameworks

- Space Development Agency (SDA) Optical Communications Terminal (OCT) Standard v3.x and Tranche Specifications

- ITU-R, FCC Part 25 & National Spectrum Coordination Standards Applicable to Optical Ground Stations

- ITAR Category XV, EAR Commerce Control List & Wassenaar Export Controls Applicable to Laser Communication Terminals

- ISO 9001, AS9100, ECSS Space Product Assurance & Aviation Laser Safety Standards

- Global Satellite Laser Communication Terminals Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Units)

- Market Size & Forecast by Terminal Type

- Inter-Satellite Link (ISL) Crosslink Terminal

- Space-to-Ground Optical Downlink Terminal

- Space-to-Air and HAPS-to-Space Terminal

- Air-to-Ground and Ground-to-Air Optical Terminal

- Space-to-User Direct-to-Device Optical Terminal

- Optical Ground Station (OGS) Terminal

- Market Size & Forecast by Orbit

- Low Earth Orbit (LEO)

- Medium Earth Orbit (MEO)

- Geostationary Earth Orbit (GEO)

- Highly Elliptical Orbit (HEO)

- Cislunar & Deep Space

- High-Altitude Platform Station (HAPS) & Stratospheric

- Market Size & Forecast by Data Rate

- Below 1 Gbps

- 1 to 10 Gbps

- 10 to 100 Gbps

- Above 100 Gbps (Coherent Multi-Wavelength)

- Market Size & Forecast by Component

- Optical Aperture, Telescope & Coarse Pointing Assembly

- Fine Pointing and Tracking Assembly (FPTA) and Beam Steering (FSM, MEMS)

- Modem (Modulator and Demodulator) & Coherent Signal Processing

- Optical Amplifier (EDFA), Photodetector & Receiver Subsystem

- Acquisition, Tracking and Pointing (ATP) System & Adaptive Optics

- Thermal Management, Control Electronics & FPGA Processing

- Market Size & Forecast by Platform

- CubeSat-Class and SmallSat-Class Spacecraft

- Standard Satellite Bus (LEO, MEO and GEO)

- Optical Ground Station (Fixed and Transportable)

- Airborne Platform (UAV, HAPS and Manned Aircraft)

- Mobile, Vehicular & Maritime Terminal

- Market Size & Forecast by End-User

- Commercial Constellation Operators (Broadband, Connectivity & IoT)

- Earth Observation & Remote Sensing Operators

- Military and Defence (Space Development Agency, US Space Force & Allied Forces)

- Civil Space Agencies (NASA, ESA, JAXA & National Space Agencies)

- Optical Ground Network & Teleport Service Providers

- Quantum Key Distribution (QKD) & Secure Communication Operators

- Market Size & Forecast by Sales Channel

- Direct Defence and Civil Space Procurement (FMS, DCS & National Tender)

- Spacecraft OEM, Bus Integrator & Prime Contractor Channel

- Constellation Operator Direct Award & Long-Term Supply Agreement

- Distributor, Authorised Reseller & Regional Partner Channel

- North America Satellite Laser Communication Terminals Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By Terminal Type

- By Orbit

- By Data Rate

- By Component

- By Platform

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Satellite Laser Communication Terminals Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By Terminal Type

- By Orbit

- By Data Rate

- By Component

- By Platform

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Satellite Laser Communication Terminals Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By Terminal Type

- By Orbit

- By Data Rate

- By Component

- By Platform

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Satellite Laser Communication Terminals Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By Terminal Type

- By Orbit

- By Data Rate

- By Component

- By Platform

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Satellite Laser Communication Terminals Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By Terminal Type

- By Orbit

- By Data Rate

- By Component

- By Platform

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Satellite Laser Communication Terminals Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By Terminal Type

- By Orbit

- By Data Rate

- By Component

- By Platform

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- *Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, United Kingdom, Germany, France, Italy, Spain, Netherlands, Switzerland, Sweden, Norway, Luxembourg, Russia, China, Japan, India, South Korea, Australia, Singapore, Taiwan, Indonesia, Brazil, Argentina, Mexico, Saudi Arabia, UAE, Qatar, Israel, Egypt, South Africa

- Technology Landscape & Innovation Analysis

- Coherent Optical Modulation, DPSK/QPSK and Polarisation-Multiplexed Detection Technology Deep-Dive

- Inter-Satellite Link (ISL) Crosslink Architecture, Mesh Network & Optical Routing Technology

- Acquisition, Tracking and Pointing (ATP), Fine Steering Mirror & Optical Phased Array Technology

- Adaptive Optics, Site Diversity & Atmospheric Compensation Technology for Optical Ground Stations

- Space-Qualified Laser, Erbium-Doped Fiber Amplifier (EDFA), Photonic Integrated Circuit & Coherent Receiver Technology

- Quantum Key Distribution (QKD) over Satellite, Single-Photon Detection & Quantum Network Technology

- Miniaturisation, CubeSat-Class Optical Terminal & Mass-Producible Photonic Module Technology

- Patent & IP Landscape in Satellite Laser Communication Terminal Technologies

- Value Chain & Supply Chain Analysis

- Space-Qualified Laser, Photonic Integrated Circuit & Specialty Optical Component Supply Chain

- Optical Telescope, Beryllium Mirror, Precision Optic & Mechanical Subassembly Supply Chain

- Modem, FPGA, Coherent Signal Processing & Embedded Software Supply Chain

- Tier-1 Optical Terminal System Integrator, Spacecraft Bus Integrator & Prime Contractor Landscape

- Constellation Operator, Defence Agency & Civil Space Agency Procurement Landscape

- Distributor, Authorised Reseller & Regional Partner Channel

- Optical Ground Network Operator, Teleport Service & Lifecycle Support Channel

- Pricing Analysis

- CubeSat and SmallSat-Class Optical Terminal Average Selling Price and Cost per Unit Analysis

- Standard Satellite Bus Optical Terminal Pricing & Total Acquisition Cost Analysis

- Optical Ground Station Capital Cost & Cost per Site Analysis

- Coherent High-Throughput (Above 100 Gbps) Terminal Pricing Analysis

- Long-Term Supply Agreement, Constellation Block Buy & Performance-Based Pricing Analysis

- Total Satellite Laser Communication Programme Economics: Cost per Bit and Throughput Co-Optimisation Analysis

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Satellite Laser Communication Terminals: Energy Intensity, Material Footprint & Critical Mineral Intensity Across Terminal Routes

- Power-Efficient Optical Communications & Pathway to Low-Power, Mass-Producible Terminal Portfolios

- End-of-Life Spacecraft Disposal, Orbital Debris Mitigation & Closed-Loop Material Management for Optical Terminals

- Environmental Compliance, Laser Safety, Aviation Hazard & Optical Ground Site Land Use Consideration

- Regulatory-Driven Sustainability, Space Sustainability Rating Alignment & ESG Disclosure for Space Programmes

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Terminal Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Terminal Type, Orbit & Geography

- Player Classification

- Tier-1 Defence and Space Prime Contractors with Integrated Laser Communications Portfolios

- Specialty Optical Communications Terminal Manufacturers & Pure-Play Producers

- Constellation Operators with Vertically-Integrated Terminal Programmes

- Civil Space Agency-Funded Optical Communications Technology Developers

- Photonic Integrated Circuit, Laser & Optical Component Specialists

- Optical Ground Station, Teleport & Network Operator Specialists

- Quantum Key Distribution & Secure Optical Communications Specialists

- Distributors, Authorised Resellers & Sustainment Service Specialists

- Competitive Analysis Frameworks

- Market Share Analysis by Terminal Type, Orbit & Region

- Company Profile

- Company Overview & Headquarters

- Satellite Laser Communications Products & Technology Portfolio

- Key Customer Relationships & Reference Programme Deployments

- Manufacturing Footprint & Production Capacity

- Revenue (Satellite Laser Communications Segment) & Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Capacity Expansion, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Terminal Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Terminal Type, Orbit, Data Rate, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)