Market Definition

The Global Battery Metals Supply Chain Market encompasses the end-to-end network of exploration, mining, beneficiation, metallurgical processing, chemical refining, precursor active material synthesis, and battery-grade material production operations that collectively supply the critical mineral inputs required for the manufacture of rechargeable lithium-ion, solid-state, sodium-ion, and next-generation electrochemical battery cells deployed across electric vehicles, utility-scale and distributed stationary energy storage systems, consumer electronics, industrial uninterruptible power supplies, aerospace, and defence applications. The market spans the complete upstream-to-downstream value chain for the principal battery metals comprising lithium, cobalt, nickel, manganese, graphite, copper, and emerging candidates including vanadium, titanium, and rare earth elements used in permanent magnet electric motors, from geological resource characterisation and reserve delineation through mine construction and ore extraction, primary processing and concentration, hydrometallurgical and pyrometallurgical refining, chemical conversion to battery-grade sulphate, carbonate, hydroxide, and oxide compounds, precursor cathode active material synthesis, and cathode and anode active material manufacturing. The value chain encompasses brine and hard rock lithium extraction and conversion, lateritic and sulphide nickel processing, cobalt recovery from polymetallic ore systems and artisanal sources, electrolytic manganese dioxide and manganese sulphate production, natural and synthetic graphite anode material processing, copper cathode refining, and the increasingly strategic battery material recycling and secondary supply streams that are progressively contributing recovered battery metals to primary supply chains. Key participants include diversified global mining majors, national mining enterprises, junior exploration companies, integrated chemical processors, battery material specialist manufacturers, automotive original equipment manufacturers pursuing vertical supply chain integration, battery cell manufacturers, sovereign wealth fund investment vehicles, and the multilateral development finance institutions and private capital providers whose investment decisions collectively govern the pace, geography, and configuration of global battery metals supply chain development through the current decade and beyond.

Market Insights

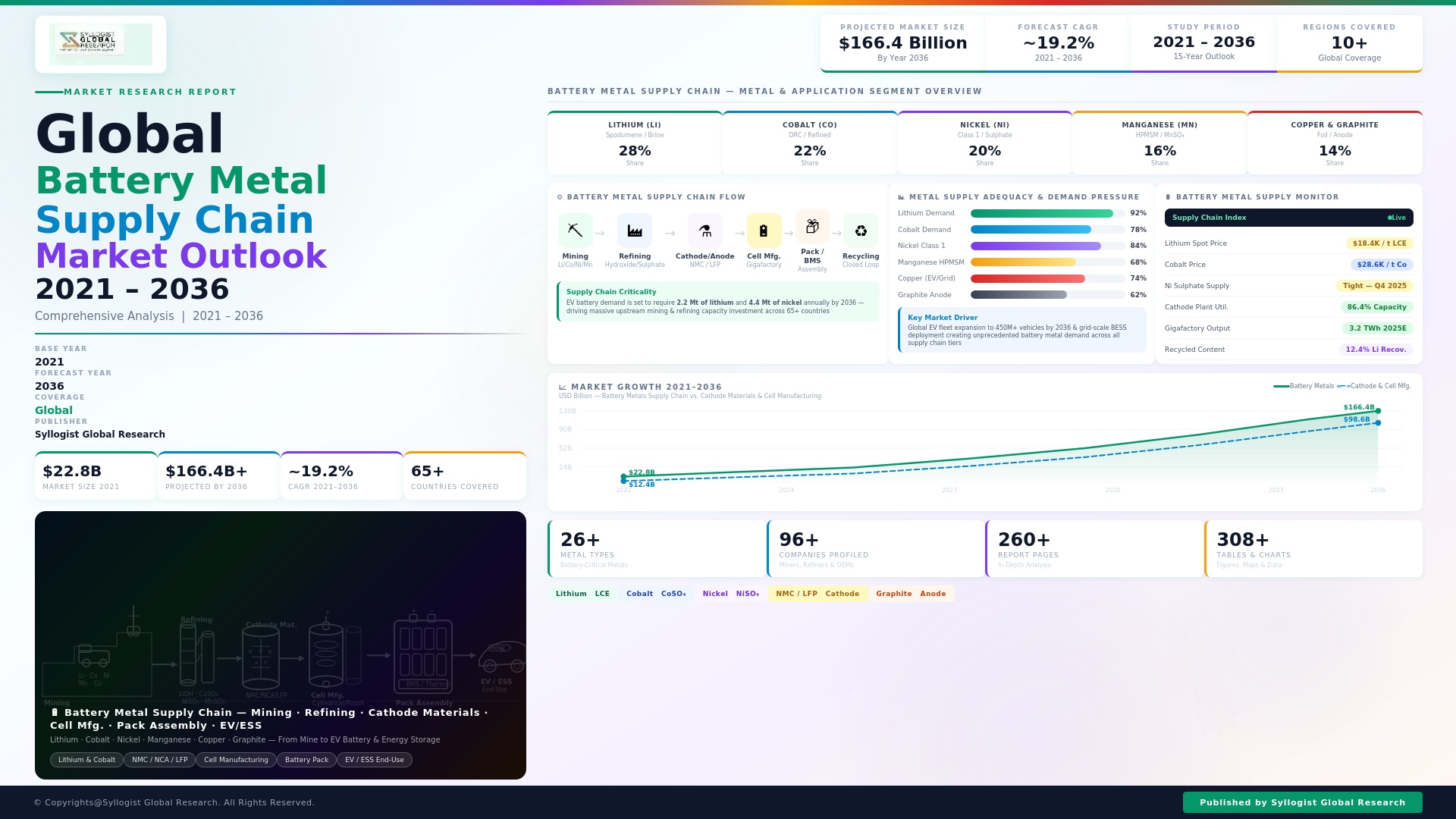

The global battery metals supply chain market was valued at approximately USD 82.6 billion in 2025 and is projected to reach USD 196.4 billion by 2034, advancing at a compound annual growth rate of 10.1% over the forecast period from 2027 to 2034, driven by the accelerating electrification of the global transportation sector, the exponential growth of utility-scale energy storage deployment, and the structural inadequacy of current global battery metal mining and processing capacity to satisfy the demand trajectory implied by national and corporate net-zero carbon emission commitments across the world’s major economies. Global electric vehicle sales reached approximately 17.1 million units in 2025, representing approximately 20% of new light vehicle sales globally, and are projected to reach approximately 45 million units annually by 2034, with each battery electric vehicle requiring approximately 8 to 10 kilograms of lithium carbonate equivalent, 25 to 40 kilograms of nickel, 5 to 15 kilograms of cobalt depending on cathode chemistry, approximately 15 kilograms of manganese, and 83 kilograms of copper across the battery pack, motor, and charging system, creating a compound demand growth rate for battery metals whose aggregate magnitude represents a supply challenge of historically unprecedented scale for the global mining and materials industry.

The lithium segment is the most structurally significant and commercially dynamic sub-market within the global battery metals supply chain, with global lithium production reaching approximately 930,000 metric tons of lithium carbonate equivalent in 2025 and projected demand requiring approximately 2.4 million metric tons of lithium carbonate equivalent annually by 2034, implying a requirement to more than double current global production capacity within the forecast period from a supply base whose project development timelines of 7 to 14 years from discovery to first production create a structural supply-demand tension that will define lithium price dynamics and investment priorities throughout the decade. Australia remains the world’s largest lithium producing nation with hard rock spodumene output of approximately 340,000 metric tons of lithium carbonate equivalent in 2025, followed by Chile at approximately 210,000 metric tons, Argentina at approximately 47,000 metric tons, and China at approximately 133,000 metric tons, while the midstream processing of spodumene concentrate to battery-grade lithium hydroxide and lithium carbonate is dominated by Chinese converters who process the majority of Australian and African spodumene output, creating a structural midstream concentration that consuming nations are actively seeking to diversify through domestic processing facility investment programs. The nickel market is simultaneously experiencing a structural oversupply condition in the class-one nickel sulphate segment following the rapid scaling of Indonesian high-pressure acid leach laterite processing capacity, with Indonesian nickel production reaching approximately 1.8 million metric tons in 2025 and suppressing nickel prices to levels that have curtailed investment in sulphide nickel development and forced temporary production suspensions at higher-cost nickel operations across Australia, Canada, and the Philippines.

The geopolitical restructuring of global battery metals supply chains has emerged as the dominant strategic market theme since 2022, with the United States Inflation Reduction Act, the European Union Critical Raw Materials Act, Japan’s Critical Minerals Strategy, South Korea’s National Resource Security Program, and equivalent policy frameworks in the United Kingdom, Canada, and Australia collectively deploying hundreds of billions of dollars in incentives, concessional financing, and offtake support to accelerate the development of battery metals supply chains that reduce the participating nations’ dependence on Chinese midstream processing dominance, which encompasses approximately 80% of global cobalt refining capacity, approximately 65% of global lithium hydroxide conversion capacity, approximately 70% of global precursor cathode active material production, and approximately 75% of global cathode active material manufacturing. The Minerals Security Partnership, a multilateral framework convening the United States, European Union, Japan, South Korea, Canada, Australia, the United Kingdom, and Finland, is coordinating government financing and technical assistance to accelerate critical mineral project development outside of China-controlled supply chains, with priority projects spanning lithium brine development in Chile and Argentina, cobalt and copper processing in the Democratic Republic of Congo and Zambia, nickel sulphide development in Canada and Australia, and graphite anode material processing in North America, Europe, and Africa. Battery material recycling is emerging as a structurally significant and rapidly scaling secondary supply stream, with global lithium-ion battery recycling capacity processing approximately 480,000 metric tons of end-of-life batteries in 2025 and projected to recover battery metal volumes equivalent to approximately 12% of primary lithium demand, 18% of cobalt demand, and 9% of nickel demand by 2034 as the first wave of electric vehicle batteries reaches end-of-life and dedicated hydrometallurgical recycling facilities commissioned since 2020 reach full operational capacity.

Battery chemistry evolution is reshaping the relative demand trajectories of individual battery metals in ways that introduce both commercial risk and strategic opportunity into the global battery metals supply chain, with the accelerating commercial penetration of lithium iron phosphate chemistry in the electric vehicle market progressively reducing cobalt and nickel demand intensity per kilowatt hour of deployed battery capacity, while simultaneously increasing absolute lithium and manganese demand as lithium iron phosphate adoption expands the total volume of battery capacity installed globally. Lithium iron phosphate accounted for approximately 43% of global electric vehicle battery installations by capacity in 2025, up from approximately 26% in 2021, driven by cost reduction to approximately USD 53 per kilowatt hour at the cell level, improved energy density, and the validated long cycle life of lithium iron phosphate chemistry in high-utilisation fleet and commercial vehicle applications, while nickel-rich cathode chemistries including nickel-manganese-cobalt 811 and nickel-cobalt-aluminium retain dominance in premium passenger vehicle applications where energy density and driving range performance justify higher cathode material cost. The emerging commercialisation of sodium-ion battery technology, with Chinese cell manufacturers having commenced volume production of sodium-ion cells for low-speed electric vehicles and energy storage applications in 2024, introduces a longer-term structural disruption risk for lithium demand from the entry-level electric vehicle and stationary storage segments, though the energy density limitations of current sodium-ion chemistry constrain its near-term addressable market to applications where the absence of critical lithium, cobalt, and nickel materials represents a more compelling commercial advantage than performance parity with lithium-ion alternatives.

Key Drivers

Accelerating Global Electric Vehicle Adoption and Gigafactory Capacity Expansion Creating Historically Unprecedented Battery Metal Demand Growth

The global electric vehicle market is generating a demand growth trajectory for battery metals whose aggregate magnitude and pace are without precedent in the history of the mining and materials industries, with the compound annual demand growth rates projected for lithium, nickel, cobalt, and manganese through 2034 requiring the simultaneous development of multiple world-class mining projects, processing facilities, and chemical conversion plants across multiple continents within development timelines that are structurally constrained by the 7-to-14-year mine development cycle, environmental permitting complexity, and capital financing requirements of major battery metal projects. Battery gigafactory construction programs announced or under development globally exceed 6.5 terawatt hours of cumulative nameplate cell production capacity as of 2025, distributed across China, the United States, European Union, South Korea, Japan, India, and emerging manufacturing nations, each requiring committed long-term battery metal supply agreements whose fulfilment demands the development of incremental mining and processing capacity beyond what existing operational assets can deliver. The energy storage sector is amplifying electric vehicle-driven battery metal demand with an independent and structurally durable demand stream, as utility-scale lithium iron phosphate battery installations for renewable energy grid integration and peak load management reached approximately 310 gigawatt hours of new deployment globally in 2025 and are projected to exceed 850 gigawatt hours annually by 2034, generating incremental lithium, manganese, iron, and phosphate demand that reinforces the structural supply growth imperative facing the global battery metals industry across the forecast period.

Government Industrial Policy and Critical Mineral Security Frameworks Mobilising Unprecedented Public and Private Capital Into Battery Metal Supply Chain Development

The convergence of energy security imperatives, net-zero carbon commitment timetables, and geopolitical competition over clean energy technology supply chains is driving the largest coordinated government investment mobilisation in the history of the mining and materials sector, with national and multilateral policy frameworks deploying incentive structures, concessional financing mechanisms, offtake guarantees, and strategic stockpile programs that are materially reducing the commercial risk profile of battery metal project investment and accelerating the development of supply chain assets that would otherwise require longer lead times under purely commercial capital allocation conditions. The United States Inflation Reduction Act’s battery mineral content requirements, which mandate progressively increasing proportions of qualifying domestic or free trade agreement partner nation sourcing for electric vehicle tax credit eligibility, have created a powerful demand-side incentive for battery metal supply chain localisation that is driving billions of dollars of investment into North American lithium, nickel, cobalt, and graphite project development, processing facility construction, and battery material recycling capacity installation. The European Union Critical Raw Materials Act’s binding strategic autonomy targets, requiring the EU to source at least 10% of annual consumption from domestic extraction, process at least 40% domestically, and ensure that no single third country supplies more than 65% of any strategic raw material by 2030, are generating equivalent investment mobilisation pressure across European battery metal processing, recycling, and supply chain diversification programs, with the EU-funded European Battery Alliance coordinating public and private investment across the complete battery value chain from mining to cell manufacturing across member state jurisdictions.

Battery Material Recycling Scale-Up and Secondary Supply Development Complementing Primary Mining to Meet Growing Battery Metal Demand

The rapid scaling of lithium-ion battery recycling capacity represents a structurally important and increasingly commercially significant complement to primary mining in the global battery metals supply chain, with the growing volume of end-of-life electric vehicle batteries, manufacturing scrap from gigafactory production processes, and stationary storage system replacements creating a secondary battery metal feedstock stream whose recovery economics are improving rapidly as hydrometallurgical recycling technology matures and recovered battery metal specifications achieve full qualification equivalence with primary battery-grade material in cathode active material manufacturing processes. Global lithium-ion battery recycling capacity processed approximately 480,000 metric tons of end-of-life battery material in 2025, recovering lithium, cobalt, nickel, manganese, and copper at recovery efficiencies of 85% to 95% for cobalt and nickel and 70% to 80% for lithium in advanced hydrometallurgical processes, with total secondary battery metal recovery values generating recycling revenue streams that are approaching economic self-sufficiency independent of gate fee income for facilities processing high-cobalt legacy battery chemistries. The regulatory environment governing battery recycling is becoming progressively more prescriptive and commercially enabling, with the European Union Battery Regulation imposing mandatory minimum recycled content requirements of 16% for cobalt, 85% for lead, 6% for lithium, and 6% for nickel in new batteries by 2031, rising to 26% for cobalt, 10% for lithium, and 15% for nickel by 2036, creating guaranteed demand for recycled battery materials that supports the investment case for large-scale hydrometallurgical recycling facility construction across European battery manufacturing jurisdictions.

Key Challenges

Structural Supply-Demand Imbalances, Mine Development Timeline Constraints, and Price Volatility Across Multiple Battery Metal Markets Simultaneously

The global battery metals supply chain faces a historically unprecedented challenge of simultaneously developing adequate production capacity across six or more structurally distinct metal supply chains, each governed by different geological resource geographies, mining technology requirements, processing chemistry platforms, capital cost structures, and development timeline constraints, within a compressed timeframe defined by the electric vehicle adoption and energy storage deployment trajectories of national net-zero programs whose battery metal demand implications are arriving faster than the mining industry’s structural development cycle can accommodate. Lithium faces a near-term supply adequacy risk from the insufficient number of funded and construction-committed mining and processing projects to satisfy projected 2028 to 2032 demand, while nickel faces the opposite challenge of a current structural oversupply condition in Indonesia-sourced class-one nickel whose price depression is curtailing investment in the sulphide nickel projects that the post-2030 supply balance will require. Cobalt market dynamics are governed by the dual uncertainty of Democratic Republic of Congo production concentration risk and the accelerating commercial adoption of cobalt-free battery chemistries that may reduce long-term demand materially below current projections, creating investment hesitancy in new cobalt project development precisely when supply security from the Congo is most geopolitically uncertain. These divergent and simultaneously occurring supply-demand dynamics across multiple battery metal markets impose complex multi-commodity portfolio management requirements on battery manufacturers, automotive original equipment manufacturers, and mining investors whose supply chain strategies must hedge across correlated and uncorrelated risk dimensions within a single integrated battery metals procurement framework.

Chinese Midstream Processing Dominance and the Geopolitical Risk of Single-Source Dependency in Battery Material Conversion and Cathode Active Material Production

China’s dominance of battery material midstream processing represents the most acute supply chain concentration risk in the global battery metals industry, with Chinese operators controlling approximately 80% of global cobalt chemical refining, 65% of lithium hydroxide conversion, 70% of precursor cathode active material synthesis, and 75% of cathode active material manufacturing capacity as of 2025, meaning that a significant proportion of globally mined battery metal output must pass through Chinese processing operations before reaching battery cell manufacturers in any part of the world, creating a structural geopolitical vulnerability that consuming nations are actively but slowly working to reduce through domestic processing investment programs whose development timelines extend well beyond the near-term supply security horizon. The risk of Chinese export restrictions on processed battery materials, battery cell components, or battery manufacturing equipment, analogous to the graphite and gallium export licensing measures implemented in 2023 and the rare earth processing export restrictions maintained since 2010, represents a systemic supply chain disruption risk for electric vehicle manufacturers and energy storage developers outside China whose battery supply chains retain material Chinese processing dependencies. Developing ex-China battery material processing capacity requires not only capital investment but also the transfer of proprietary process chemistry knowledge, the recruitment and training of specialist metallurgical and chemical engineering workforces, the qualification of new processing facilities against demanding battery manufacturer material specifications, and the negotiation of long-term offtake agreements that provide the commercial certainty required to support project financing, all of which impose development timelines of five to ten years from investment decision to qualified production supply that constrain the pace at which Chinese midstream processing dependency can be structurally reduced.

Environmental, Social, and Governance Compliance Complexity and Community Opposition Constraining Mine Development Timelines Across Key Battery Metal Jurisdictions

Battery metal mine development is facing progressively more demanding environmental, social, and governance compliance requirements across the jurisdictions hosting the world’s most significant battery metal resources, with permitting timelines for new mines in the United States, Canada, Australia, and European Union member states extending to 10 to 20 years from initial application to production commencement due to the cumulative requirements of environmental impact assessment, indigenous community consultation and consent processes, water management plan approval, biodiversity offset program design, and judicial review procedures that can be initiated by community or environmental advocacy groups at multiple stages of the permitting process. The responsible sourcing imperative, driven by automotive original equipment manufacturer and battery manufacturer supply chain due diligence obligations, investor environmental, social, and governance screening criteria, and regulatory frameworks including the EU Corporate Sustainability Due Diligence Directive, is imposing supply chain transparency, audit, and reporting requirements on battery metal supply chains that extend from battery cell manufacturer back to individual mine site operations, creating compliance infrastructure investment requirements across the complete supply chain whose cumulative cost burden is disproportionate for small and mid-tier mining operators supplying into complex multi-tier battery metal value chains. Water scarcity conflicts, tailings storage facility safety requirements following catastrophic failures at iron ore and gold mining operations globally, air quality impacts of sulphide ore smelting, and community opposition to mining development in proximity to inhabited areas are generating project delays, litigation risk, and social licence constraints across battery metal mining projects in Chile, Argentina, the United States, Australia, and Central Africa that collectively impose a structural timing tax on the battery metals supply chain’s capacity to expand production at the pace required by clean energy transition demand trajectories.

Market Segmentation

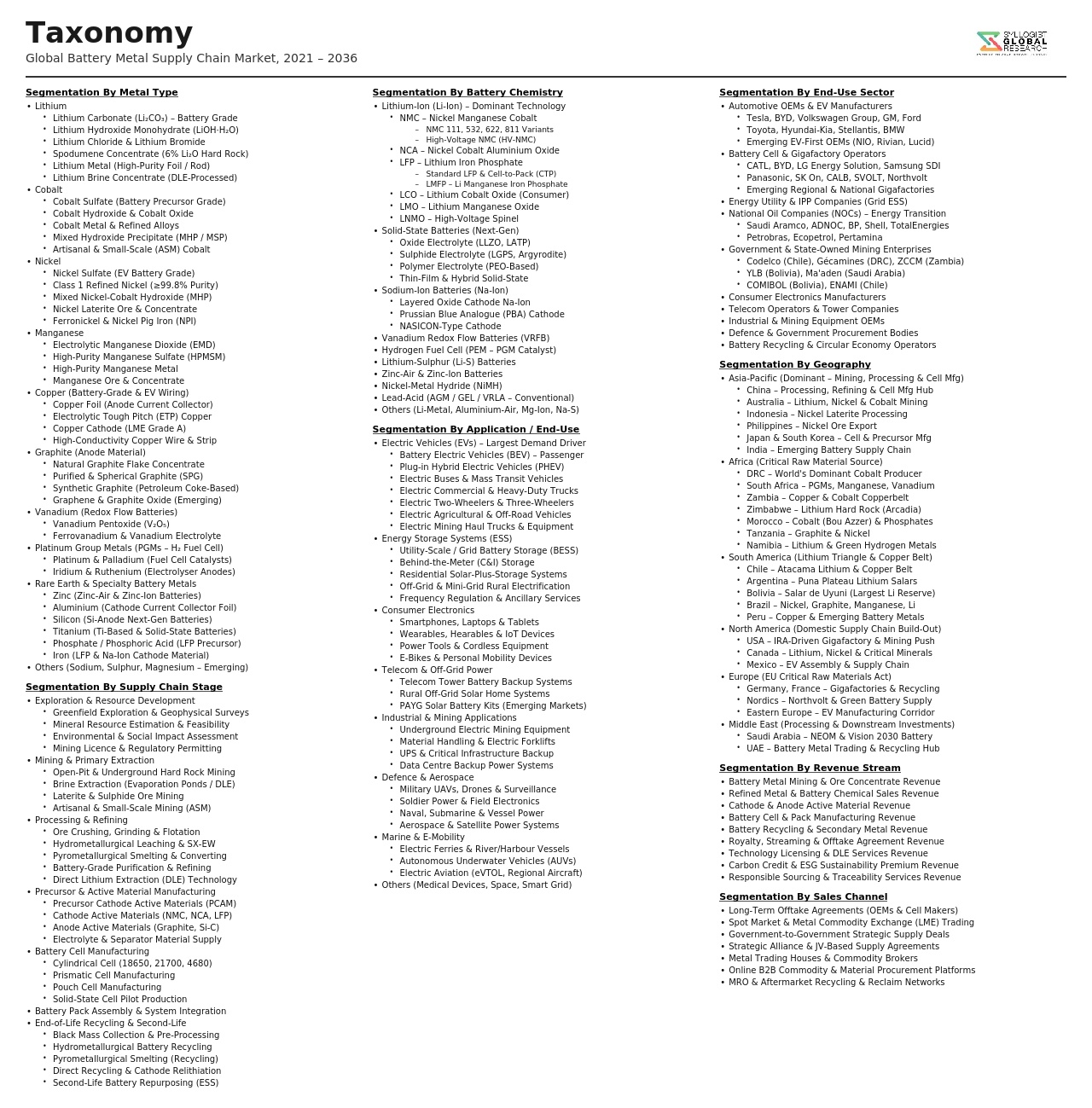

- Segmentation By Metal Type

- Lithium (Spodumene, Lithium Carbonate, and Lithium Hydroxide)

- Cobalt (Cobalt Hydroxide, Cobalt Sulphate, and Refined Cobalt)

- Nickel (Mixed Hydroxide Precipitate, Nickel Sulphate, and Class-One Nickel)

- Manganese (Battery-Grade Manganese Sulphate and Electrolytic Manganese Dioxide)

- Copper (Refined Copper Cathode and Copper Sulphate)

- Natural and Synthetic Graphite (Anode-Grade Spherical Graphite)

- Vanadium (Vanadium Pentoxide and Vanadium Electrolyte)

- Rare Earth Elements (Neodymium-Praseodymium and Dysprosium for Motor Magnets)

- Others

- Segmentation By Value Chain Stage

- Geological Exploration and Resource Delineation

- Mining and Primary Extraction (Open Pit, Underground, and Brine)

- Ore Beneficiation and Concentrate Production

- Hydrometallurgical and Pyrometallurgical Refining

- Battery-Grade Chemical Material Conversion

- Precursor Cathode Active Material Synthesis

- Cathode and Anode Active Material Manufacturing

- Battery Material Recycling and Secondary Supply

- Segmentation By Battery Chemistry Served

- Lithium Nickel Manganese Cobalt Oxide (NMC) Batteries

- Lithium Nickel Cobalt Aluminium Oxide (NCA) Batteries

- Lithium Iron Phosphate (LFP) Batteries

- Lithium Cobalt Oxide (LCO) Batteries

- Lithium Manganese Oxide (LMO) Batteries

- Solid-State Battery Chemistries

- Sodium-Ion Battery Chemistries

- Others

- Segmentation By End-Use Application

- Passenger Electric Vehicles

- Commercial Electric Vehicles (Trucks, Buses, and Vans)

- Two-Wheeler and Three-Wheeler Electric Mobility

- Utility-Scale Grid Energy Storage

- Distributed and Behind-the-Meter Energy Storage

- Consumer Electronics and Portable Devices

- Aerospace and Defence Applications

- Industrial and Uninterruptible Power Supply Applications

- Others

- Segmentation By Extraction and Processing Technology

- Solar Evaporation Brine Lithium Extraction

- Direct Lithium Extraction (Ion Exchange, Solvent, and Membrane)

- Hard Rock Spodumene Mining and Calcination

- High-Pressure Acid Leach Laterite Nickel Processing

- Sulphide Nickel Smelting and Refining

- Cobalt Hydroxide Precipitation and Chemical Conversion

- Hydrometallurgical Battery Recycling (Black Mass Processing)

- Pyrometallurgical Battery Recycling (Smelting)

- Others

- Segmentation By Supply Chain Origin

- Primary Mined Supply

- Secondary Recycled Supply

- Co-Product and By-Product Recovery

- Artisanal and Small-Scale Mining Supply

- Synthetic and Manufactured Alternatives

- Segmentation By Ownership Structure

- Diversified International Mining Majors

- State-Owned and National Mining Enterprises

- Mid-Tier and Junior Exploration Companies

- Integrated Battery Material Chemical Companies

- Automotive OEM and Battery Manufacturer Vertical Investments

- Sovereign Wealth Fund and Strategic Investment Vehicles

- Joint Ventures and Public-Private Partnerships

- Segmentation By Region

- Asia-Pacific (China, Australia, Indonesia, and Others)

- South America (Chile, Argentina, Brazil, and Bolivia)

- Middle East and Africa (Democratic Republic of Congo, Zambia, Morocco, and Gulf States)

- North America (United States, Canada, and Mexico)

- Europe (Norway, Finland, Portugal, and Others)

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Battery Metals Supply Chain Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by metal type, lithium, cobalt, nickel, manganese, copper, and graphite, by value chain stage, mining, primary processing, chemical refining, and battery material manufacturing, and by geography, to enable mining companies, battery manufacturers, automotive original equipment manufacturers, energy storage developers, and investors to identify which metal categories, supply chain stages, and regional markets will generate the highest absolute revenue and most strategically significant supply contributions across the forecast period?

- How is the competitive supply-demand balance across the lithium, nickel, cobalt, manganese, copper, and graphite markets expected to evolve through 2034 on a metal-by-metal basis, which metals face structural supply deficit risk requiring accelerated mine development investment, which face structural oversupply conditions that will suppress prices and curtail new project development, and how will the simultaneous evolution of battery chemistry, energy storage deployment growth, and battery material recycling secondary supply interact to reshape the demand intensity and market price trajectory of each individual battery metal through the forecast period?

- What is the projected trajectory of ex-China battery material processing capacity development across North America, Europe, Australia, South Korea, Japan, and emerging processing hub locations in the Middle East and Africa through 2034, which processing value chain stages, lithium hydroxide conversion, nickel sulphate refining, cobalt chemical processing, precursor cathode active material synthesis, and cathode active material manufacturing, represent the most commercially viable near-term investment opportunities for non-Chinese operators, and what are the technology transfer, workforce, permitting, and commercial offtake requirements for new processing facility development to achieve competitive production economics relative to established Chinese operations?

- How are national and multilateral government policy frameworks, including the United States Inflation Reduction Act qualifying mineral requirements, the European Union Critical Raw Materials Act strategic autonomy targets, and equivalent programs in Japan, South Korea, Canada, and Australia, expected to reshape battery metal supply chain investment flows, project development priorities, and trade patterns through 2034, and what are the implications for mining companies, processing operators, battery manufacturers, and automotive original equipment manufacturers in terms of supply chain restructuring requirements, compliance investment, and competitive positioning within the emerging regionally bifurcated global battery metals supply chain architecture?

- Who are the leading mining companies, battery material chemical processors, precursor and cathode active material manufacturers, battery recycling operators, and sovereign investment fund participants currently defining the competitive and strategic landscape of the global battery metals supply chain market, and what are their respective resource portfolios and production capacity positions across the principal battery metals, project development and capacity expansion timelines through 2034, vertical integration strategies from mining through battery material production, responsible sourcing and environmental, social, and governance program investments, technology development commitments in direct lithium extraction and next-generation processing platforms, and strategic responses to the geopolitical, regulatory, and competitive dynamics reshaping the global battery metals supply chain?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Mining, Processing & Refining Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Geographic Supply Concentration Risk: Critical Dependency on DRC Cobalt, Chilean and Argentine Lithium, Indonesian Nickel and Chinese Refining Capacity

- Geopolitical and Trade Policy Risk: US-China Technology Competition, Export Controls, Critical Mineral Strategies and Supply Chain Decoupling

- Resource Nationalism, Royalty Regime Changes and Government Intervention Risk Across Key Battery Metal Mining Jurisdictions

- ESG and Responsible Sourcing Risk: Artisanal Mining, Indigenous Rights, Water Stress and Community Opposition Affecting Supply Continuity

- Commodity Price Volatility Risk: Lithium, Cobalt, Nickel, Manganese and Graphite Price Cycle Exposure for Supply Chain Participants

- Regulatory Framework & Standards

- EU Battery Regulation (2023/1542): Carbon Footprint Declaration, Due Diligence, Recycled Content Mandates and Digital Battery Passport Requirements

- US Inflation Reduction Act (IRA) Critical Mineral and Battery Component Sourcing Requirements and Foreign Entity of Concern (FEOC) Restrictions

- National Critical Mineral Strategies: US, EU, Japan, South Korea, Australia, Canada and India Comparative Policy Framework Analysis

- Mining Jurisdiction Regulatory Frameworks: DRC, Chile, Argentina, Indonesia, Australia and South Africa Mining Codes, Royalty and Export Policy

- OECD Responsible Minerals Guidance, RMI Responsible Sourcing Standards, IRMA and Conflict Minerals Reporting Obligations for Battery Metal Supply Chains

- Global Battery Metals Supply Chain Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Metric Tons of Metal Content)

- Market Size & Forecast by Metal Type

- Lithium (Brine-Derived and Hard Rock Spodumene)

- Cobalt (Primary and By-Product)

- Nickel (Sulphide, Laterite and Mixed Hydroxide Precipitate)

- Manganese (High-Purity Manganese Sulphate)

- Copper (Battery and EV Wiring Enabler Metal)

- Graphite (Natural Flake, Synthetic and Spherical)

- Rare Earth Elements (REEs for Battery and EV Motor Applications)

- Other Battery Metals (Vanadium, Titanium, Aluminium and Silicon)

- Market Size & Forecast by Supply Chain Stage

- Mining and Ore Extraction

- Ore Processing and Beneficiation

- Smelting, Refining and Hydrometallurgical Processing

- Battery-Grade Chemical Production (Lithium Carbonate, Lithium Hydroxide, Cobalt Sulphate, Nickel Sulphate and MnSO4)

- Precursor Cathode Active Material (PCAM) Manufacturing

- Cathode Active Material (CAM) Manufacturing

- Anode Material Manufacturing (Natural and Synthetic Graphite, Silicon Anode)

- Battery Cell and Pack Assembly

- Battery Recycling and Secondary Supply

- Market Size & Forecast by Battery Chemistry

- Lithium Iron Phosphate (LFP)

- Nickel Manganese Cobalt (NMC: 111, 532, 622 and 811)

- Nickel Cobalt Aluminium (NCA)

- Nickel Manganese (LNMO and High-Manganese Chemistries)

- Solid-State and Next-Generation Battery Chemistries

- Other Battery Chemistries (LMO, NiMH and Vanadium Redox Flow)

- Market Size & Forecast by Application

- Electric Vehicles (Passenger EVs, Commercial EVs and Two and Three Wheelers)

- Energy Storage Systems (Grid-Scale BESS, Industrial and Behind-the-Meter)

- Consumer Electronics (Smartphones, Laptops, Tablets and Wearables)

- Industrial and Other Applications (Material Handling, Marine, Aerospace and Defence)

- Market Size & Forecast by End-User

- Battery Cell Manufacturers and Gigafactory Operators

- Automotive OEMs and EV Manufacturers

- Energy Storage System Developers and Utilities

- Consumer Electronics Manufacturers

- Industrial and Defence End-Users

- Market Size & Forecast by Trade Flow Type

- Raw Ore and Concentrate Exports

- Intermediate Refined Metal and Alloy Exports

- Battery-Grade Chemical Product Exports (Lithium Hydroxide, Cobalt Sulphate, Nickel Sulphate and MnSO4)

- PCAM and CAM Trade Flows

- Domestic Value-Addition, In-Country Processing and Gigafactory Integration

- Market Size & Forecast by Sales and Offtake Channel

- Long-Term Offtake Agreements with Battery Manufacturers and Automakers

- Spot Market and Commodity Exchange Trading

- Government-to-Government Supply and Strategic Reserve Agreements

- Joint Venture and Equity Participation Offtake Structures

- North America Battery Metals Supply Chain Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tons of Metal Content)

- By Metal Type

- By Supply Chain Stage

- By Battery Chemistry

- By Application

- By End-User

- By Trade Flow Type

- By Country

- By Sales and Offtake Channel

- Market Size & Forecast

- Europe Battery Metals Supply Chain Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tons of Metal Content)

- By Metal Type

- By Supply Chain Stage

- By Battery Chemistry

- By Application

- By End-User

- By Trade Flow Type

- By Country

- By Sales and Offtake Channel

- Market Size & Forecast

- Asia-Pacific Battery Metals Supply Chain Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tons of Metal Content)

- By Metal Type

- By Supply Chain Stage

- By Battery Chemistry

- By Application

- By End-User

- By Trade Flow Type

- By Country

- By Sales and Offtake Channel

- Market Size & Forecast

- Latin America Battery Metals Supply Chain Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tons of Metal Content)

- By Metal Type

- By Supply Chain Stage

- By Battery Chemistry

- By Application

- By End-User

- By Trade Flow Type

- By Country

- By Sales and Offtake Channel

- Market Size & Forecast

- Middle East & Africa Battery Metals Supply Chain Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tons of Metal Content)

- By Metal Type

- By Supply Chain Stage

- By Battery Chemistry

- By Application

- By End-User

- By Trade Flow Type

- By Country

- By Sales and Offtake Channel

- Market Size & Forecast

- Country-Wise* Battery Metals Supply Chain Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tons of Metal Content)

- By Metal Type

- By Supply Chain Stage

- By Battery Chemistry

- By Application

- By End-User

- By Trade Flow Type

- By Country

- By Sales and Offtake Channel

- Market Size & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Poland, Norway, Sweden, China, Japan, South Korea, Australia, Indonesia, India, Chile, Argentina, Bolivia, Brazil, Democratic Republic of Congo (DRC), Zambia, South Africa, Mozambique, Tanzania, Saudi Arabia, UAE

- Technology Landscape & Innovation Analysis

- Direct Lithium Extraction (DLE) Technology Deep-Dive: Adsorption, Solvent Extraction and Membrane-Based Systems for Brine and Geothermal Lithium Recovery

- Nickel Laterite Processing Technology: High-Pressure Acid Leach (HPAL), Mixed Hydroxide Precipitate (MHP) and Ferronickel Routes

- Cobalt Refining and Battery-Grade Cobalt Sulphate Production Technology

- Graphite Purification, Spheronisation and Silicon-Carbon Composite Anode Material Technology

- Precursor Cathode Active Material (PCAM) Co-Precipitation and Cathode Active Material (CAM) Calcination Technology

- Battery Recycling Technology: Hydrometallurgical and Pyrometallurgical Black Mass Processing and Closed-Loop Metal Recovery

- Digital Supply Chain Traceability, Blockchain-Based Provenance and Responsible Sourcing Certification Platforms

- Patent & IP Landscape in Battery Metal Extraction, Refining and Processing Technologies

- Value Chain & Supply Chain Analysis

- Upstream Mining and Resource Development: Global Reserve Distribution, Exploration Pipeline and Mine Development Landscape

- Ore Processing, Beneficiation and Concentrate Logistics to Port and Smelter

- Refining and Hydrometallurgical Processing: Geographic Concentration of Refining Capacity and In-Country vs. Offshore Refining Trade-Offs

- Battery-Grade Chemical Production and Global Gigafactory Supply Chain Integration

- PCAM and CAM Manufacturing: Geographic Shift from China-Dominant to Multi-Regional Supply Chain Development

- Offtake, Trading and Procurement: Battery Manufacturer, Automaker and Commodity Trader Landscape

- Battery Recycling and Closed-Loop Secondary Supply Chain: Global Black Mass Collection, Processing and Metal Re-Entry

- Pricing Analysis

- Lithium Carbonate and Lithium Hydroxide Global Price Cycle Analysis: Historical Trends, 2024 Correction and Long-Term Forecast

- Cobalt, Nickel and Manganese LME, Fastmarkets and Benchmark Mineral Intelligence Price Benchmarking for Battery-Grade Products

- Graphite and Anode Material Pricing: Natural Flake, Spherical Graphite and Synthetic Graphite Global Price Comparison

- Production Cost Analysis: Cash Cost Per Tonne for Lithium, Cobalt, Nickel and Graphite Across Global Mining Operations

- Value-Addition Premium: Price Differential Across Ore, Concentrate, Refined Metal, Battery-Grade Chemical and PCAM Supply Chain Stages

- Offtake Agreement Pricing Structures: Fixed Price, Index-Linked, Floor-Price and Tolling Mechanisms in Global Battery Metal Contracts

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Global Battery Metal Supply Chains: Carbon Footprint, Water Intensity and Biodiversity Impact Across Mining Routes and Geographies

- Responsible Sourcing in the Cobalt Supply Chain: ASM Formalisation, Child Labour Elimination and OECD Due Diligence Implementation

- Water Stress in Lithium Brine Operations: Atacama and Global Salar Environmental Science, Regulatory Responses and Industry Practices

- EU Battery Regulation Carbon Footprint and Recycled Content Compliance: Implications for Global Battery Metal Supply Chain Participants

- Decarbonisation of Battery Metal Mining and Processing: Renewable Energy Integration, Green Hydrogen and Net-Zero Mining Pathway Initiatives

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Metal Type and Supply Chain Stage)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Metal Type, Supply Chain Stage and Geography

- Player Classification

- Integrated Global Mining Majors with Diversified Battery Metal Portfolios

- Dedicated Lithium Producers (Brine and Hard Rock)

- Cobalt and Copper Producers with Battery Metal By-Product Streams

- Nickel and Manganese Producers Targeting Battery-Grade Markets

- Graphite and Anode Material Producers and Processors

- PCAM and CAM Manufacturers and Battery Chemical Refiners

- Battery Recyclers and Secondary Supply Chain Operators

- Competitive Analysis Frameworks

- Market Share Analysis by Metal Type, Supply Chain Stage and Region

- Company Profile

- Company Overview & Headquarters

- Battery Metal Asset Portfolio: Mine, Processing and Chemical Plant Holdings

- Production Capacity, Annual Output and Reserve Base

- Key Offtake Agreements and Customer Relationships

- Revenue (Battery Metals Segment) and Capital Expenditure

- Technology Differentiators, Processing IP & Responsible Sourcing Certifications

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Mine Expansions, New Projects, Offtake Deals and Regulatory Milestones)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Resource Scale vs. Processing Integration and ESG Compliance)

- Key Company Profiles

- Market Structure & Concentration

- Strategic Outlook & Opportunity Analysis

- Strategic Output

- Market Opportunity Matrix: By Metal Type, Supply Chain Stage, Battery Chemistry, Application and Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Resource Development & Mining Asset Strategy

- In-Country Value-Addition & Processing Integration Strategy

- Offtake, Trading & Customer Diversification Strategy

- Regulatory Navigation, Government Relations & Critical Mineral Policy Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability, Responsible Sourcing & ESG Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output