Market Definition

The South America Battery Metals Supply Chain Market encompasses the exploration, mining, processing, refining, and downstream value-added transformation of critical mineral resources required for the manufacture of rechargeable battery cells, modules, and packs deployed across electric vehicles, stationary energy storage systems, portable consumer electronics, and grid-scale power applications, spanning the complete upstream-to-midstream supply chain from geological resource characterisation and mine development through ore extraction, primary processing, chemical conversion, and the production of battery-grade refined materials and precursor compounds. The market covers the regional supply chains of lithium, cobalt, nickel, manganese, graphite, copper, and emerging battery metal candidates including vanadium and titanium across South America’s resource-rich geological provinces, with particular emphasis on the Lithium Triangle jurisdictions of Chile, Argentina, and Bolivia, which collectively host approximately 58% of the world’s identified lithium resources, the significant nickel and cobalt mineral endowment of Brazil, and the copper-dominant mining economies of Chile and Peru whose byproduct and associated metal streams contribute to battery metal supply chains. The market value chain encompasses brine extraction and direct lithium extraction operations, hard rock spodumene and petalite mining, lateritic and sulphide nickel ore processing, cobalt recovery from polymetallic systems, lithium carbonate and lithium hydroxide chemical conversion plants, nickel sulphate and mixed hydroxide precipitate refining operations, and the nascent battery material precursor manufacturing facilities that represent the downstream value addition frontier within South America’s battery metals industrial development. Key participants include national mining majors, international mining companies, junior exploration entities, national government enterprises, chemical processing operators, battery material offtakers, and the multilateral development finance institutions and private capital providers whose investment decisions are shaping the pace and configuration of South America’s battery metals supply chain development.

Market Insights

The South America battery metals supply chain market was valued at approximately USD 14.7 billion in 2025 and is projected to reach USD 38.2 billion by 2034, advancing at a compound annual growth rate of 11.2% over the forecast period from 2027 to 2034, driven by the accelerating global demand for battery-grade lithium compounds, nickel intermediates, and copper from the electric vehicle and stationary energy storage industries whose collective battery metal consumption is expanding at a rate that existing global supply pipelines are structurally challenged to match. Chile remains the world’s largest lithium producer by volume, with lithium carbonate equivalent production reaching approximately 210,000 metric tons in 2025, while Argentina’s lithium production has scaled rapidly to approximately 47,000 metric tons of lithium carbonate equivalent in the same year as new brine and hard rock projects commissioned in the Puna region and Atacama puna geological provinces contribute incremental supply. The trajectory of South America’s battery metals market is shaped by the intersection of extraordinary geological endowment, evolving national resource governance frameworks, global battery supply chain decarbonisation and localisation imperatives, and the strategic competition among the United States, European Union, China, Japan, and South Korea to secure long-term battery metal supply commitments from South American resource nations.

Lithium is the defining commodity of South America’s battery metals landscape, with the region’s brine-hosted lithium deposits in the Atacama, Hombre Muerto, Cauchari-Olaroz, Pastos Grandes, and Salar de Uyuni salt flat systems representing the world’s largest and lowest-cost primary lithium resource base, characterised by high lithium concentrations, favourable brine chemistry, and solar evaporation processing economics that deliver production costs substantially below those achievable from hard rock spodumene operations in Australia or Africa. The technology transition from conventional solar evaporation pond lithium extraction toward direct lithium extraction processes, which recover lithium selectively from brine using ion exchange, solvent extraction, or membrane separation mechanisms with recovery efficiencies of 70% to 90% compared to approximately 40% to 50% for evaporation pond systems, is progressing from pilot scale toward commercial deployment across multiple projects in Argentina and Chile, with successful commercial-scale direct lithium extraction operations projected to materially expand recoverable lithium resource volumes and reduce the environmental footprint and water consumption of brine lithium production. Argentina’s lithium sector is experiencing a particularly dynamic expansion phase following the implementation of the Regime of Incentives for Large Investments introduced in 2024, which provides fiscal stability guarantees, import duty exemptions, and profit remittance liberalisation provisions that have stimulated a significant acceleration in foreign direct investment commitments to Argentine lithium projects from international mining companies and battery supply chain participants.

Brazil occupies a distinct and strategically significant position within South America’s battery metals supply chain as the region’s primary source of nickel, cobalt, graphite, manganese, and niobium, complementing the lithium dominance of the Andean nations with a diversified battery metal resource portfolio whose development is supported by Brazil’s more mature mining regulatory framework, established metallurgical processing infrastructure, and proximity to Atlantic shipping routes serving European and North American battery manufacturing destinations. Brazil’s nickel laterite endowment, particularly in the Para and Goias states, supports integrated nickel mining and hydrometallurgical processing operations producing mixed hydroxide precipitate and nickel sulphate, with production capacity expanding in response to battery sector demand growth for high-purity nickel intermediates suitable for nickel-manganese-cobalt and nickel-cobalt-aluminium cathode active material manufacturing. Chile’s copper mining industry, which produces approximately 5.7 million metric tons of refined copper annually and accounts for approximately 27% of global copper supply, is generating increasing attention as a battery metal supplier given copper’s critical role as a current collector material in lithium-ion battery cell construction, with each electric vehicle requiring approximately 83 kilograms of copper across the battery, motor, wiring, and charging system, creating a structural demand uplift for Chilean copper production as global electric vehicle penetration advances.

The geopolitical dimension of South America’s battery metals supply chain has intensified substantially since 2022, as the United States Inflation Reduction Act’s requirements for qualifying battery mineral content sourced from free trade agreement partner nations or domestic production, the European Union Critical Raw Materials Act’s strategic stockpile and supply diversification mandates, and equivalent policy frameworks in Japan, South Korea, and the United Kingdom have elevated the strategic value of South American battery metal resources and prompted a wave of government-to-government mineral security agreements, critical minerals partnership frameworks, and bilateral investment treaties between South American resource nations and battery metal consuming economies. The emerging tension between national resource sovereignty aspirations and foreign investment attraction imperatives is a defining market dynamic, with Bolivia pursuing full state ownership of lithium development through Yacimientos de Litio Bolivianos, Chile debating the appropriate role of state enterprise Codelco and a proposed national lithium company in future lithium development, and Argentina maintaining a more investment-liberal approach that has attracted a broader range of international capital commitments. The downstream value addition imperative, expressed in the policy objectives of multiple South American governments seeking to capture a greater share of battery value chain economics through domestic lithium carbonate-to-hydroxide conversion, cathode precursor manufacturing, and ultimately battery cell assembly, is creating both commercial development opportunities and policy-driven investment requirements that are reshaping the configuration of South America’s battery metals industrial landscape over the forecast period.

Key Drivers

Accelerating Global Electric Vehicle Adoption and Battery Manufacturing Capacity Expansion Creating Structural Long-Term Demand for South American Battery Metals

The global electric vehicle market is generating a demand trajectory for battery-grade lithium, nickel, cobalt, manganese, and copper that is structurally transforming the scale and strategic importance of South America’s battery metals supply chains, with global electric vehicle sales reaching approximately 17.1 million units in 2025 and projected to exceed 45 million units annually by 2034, each battery electric vehicle requiring approximately 8 to 10 kilograms of lithium carbonate equivalent, 25 to 40 kilograms of nickel, and significant quantities of manganese, cobalt, and copper depending on cathode chemistry architecture. Battery gigafactory construction programs in the United States, European Union, South Korea, Japan, and India are creating committed long-term demand for battery material supply that global mining and processing capacity pipelines are challenged to satisfy at the pace required, elevating the strategic priority of South American resource development in the supply security calculus of battery manufacturers, automotive OEMs, and the governments of battery consuming nations. The International Energy Agency projects that lithium demand will increase by approximately 42 times between 2020 and 2040 under accelerated clean energy transition scenarios, with nickel demand increasing approximately 19 times and cobalt demand approximately 21 times over the same period, establishing a demand growth trajectory for South American battery metals whose magnitude is without precedent in the history of global mining and materials markets and whose fulfilment will require sustained capital investment in South American resource development throughout the forecast period and beyond.

Government Policy Frameworks, Free Trade Agreements, and Bilateral Critical Minerals Partnerships Attracting Foreign Investment into South American Battery Metal Projects

The combination of favourable national resource policy reforms in Argentina, Chile, and Brazil, expanding bilateral critical minerals partnership frameworks between South American resource nations and battery metal consuming economies, and the multilateral development finance institution investment mobilisation programs targeting clean energy transition supply chains is generating a structurally supportive investment environment for South American battery metal project development that is accelerating mine construction, processing plant commissioning, and downstream value addition facility investment across the region. Argentina’s Regime of Incentives for Large Investments, operational since 2024, provides 30-year fiscal stability guarantees, customs duty exemptions on capital goods imports, and a three-stage foreign currency retention framework that allows qualifying mining projects to retain 100% of export revenues in foreign currency for the first four years, addressing the macroeconomic risk concerns that had historically constrained foreign direct investment in Argentine mining. Chile’s revised National Lithium Strategy, announced in 2023, while introducing requirements for state participation in new lithium development through Codelco, simultaneously confirmed the continuation of existing concessionaire operations and opened new lithium development areas including chloride-rich brines previously outside the concession framework, providing a more predictable policy foundation for international investment planning. The United States-Chile Critical Minerals Agreement, the EU-Chile Strategic Partnership Agreement covering critical raw materials, and equivalent frameworks being negotiated with Argentina and Brazil are providing preferential market access commitments and investment protection assurances that are material factors in the capital allocation decisions of mining companies and battery supply chain investors evaluating South American project portfolios.

Direct Lithium Extraction Technology Commercialisation and Processing Innovation Expanding Recoverable Resource Base and Improving Supply Chain Economics

The commercialisation of direct lithium extraction technologies represents the most consequential near-term technical development for South America’s lithium supply chain, with the successful deployment of selective lithium recovery processes capable of extracting lithium from brines at recovery efficiencies of 70% to 90% compared to the 40% to 50% achievable by conventional solar evaporation systems offering the prospect of materially expanding the volume of economically recoverable lithium from existing brine resources, reducing the multi-year production timeline from brine resource to saleable lithium product characteristic of evaporation pond operations, and enabling the development of lower-grade or more complex brine resources that are uneconomic under conventional processing approaches. Multiple direct lithium extraction technology platforms including sorbent-based ion exchange, solvent extraction, and membrane filtration systems are advancing through pilot and demonstration scale programs in Argentina and Chile, with the first commercial-scale direct lithium extraction operations expected to contribute meaningful production volumes by 2027 to 2028, providing an important supply growth vector beyond the conventional evaporation pond expansion programs that have driven the majority of South American lithium production growth to date. The parallel development of integrated brine-to-battery-grade lithium hydroxide processing facilities, which convert lithium chloride eluate from direct lithium extraction systems directly to battery-grade lithium hydroxide monohydrate without the intermediate lithium carbonate conversion step, is creating the technical pathway for South American producers to manufacture the lithium hydroxide product form preferred by the nickel-rich cathode active material production segment without the energy-intensive conversion step that adds cost and complexity to the conventional carbonate-to-hydroxide processing route.

Key Challenges

Political and Regulatory Uncertainty, Resource Nationalism, and Inconsistent Policy Frameworks Constraining Long-Term Investment Commitment in Key Jurisdictions

South America’s battery metals investment environment is materially complicated by the political and regulatory instability affecting multiple key jurisdictions, with Bolivia’s state-controlled lithium development model having failed to attract the scale of international technical and capital partnership required to advance development of the Salar de Uyuni at the pace demanded by global battery metal market growth, Chile’s ongoing policy evolution regarding the appropriate balance between state enterprise participation and private investment in lithium development creating investment planning uncertainty for international mining companies evaluating Chilean lithium project opportunities, and Argentina’s historically volatile macroeconomic environment including recurring sovereign debt restructuring events, foreign exchange controls, and inflation rates that have historically elevated the risk premium applied to Argentine mining investment despite the country’s exceptional lithium resource endowment. The fiscal and regulatory terms governing mining investment, including royalty rates, windfall profit taxation proposals, environmental permitting requirements, indigenous community consultation obligations, and water use authorisation processes, are subject to legislative and regulatory change across South American mining jurisdictions in ways that can materially alter project economics after significant capital has been committed, creating a structural investment risk that institutional mining capital and battery supply chain investors must price into their return requirements. Community opposition to mining development, particularly in water-stressed high-altitude Andean environments where brine lithium production operations share water resources with indigenous communities, agricultural users, and fragile high-altitude wetland ecosystems, has generated permitting delays, injunctive legal challenges, and operational disruptions at multiple South American lithium and mining projects and represents a persistent constraint on development timelines across the region.

Infrastructure Deficits in Remote Mining Regions and the High Capital Cost of Enabling Logistics, Power, and Water Supply for Battery Metal Projects

South America’s most significant battery metal resources are predominantly located in remote, high-altitude, and climatically challenging environments including the Atacama and Puna plateaus of Chile, Argentina, and Bolivia at elevations of 3,500 to 5,000 metres above sea level, the Amazon basin laterite nickel deposits of Brazil’s Para state, and the Andean hard rock lithium and copper deposits of Peru and Argentina, where the absence of adequate road, rail, port, power, and water supply infrastructure imposes capital and operating cost burdens on mining and processing operations that are substantially higher than those encountered in more accessible mining regions globally. The power supply challenge is particularly acute for electrochemical lithium processing and hydrometallurgical nickel refining operations whose specific energy consumption requirements exceed what renewable energy installations alone can reliably provide in remote locations, necessitating costly hybrid power supply infrastructure, grid extension investments, or diesel generation backup systems that increase project capital requirements and carbon footprints relative to operations located in grid-connected industrial zones. Water availability and allocation in the hydrologically sensitive high-altitude salt flat environments of the Lithium Triangle represents both an operational constraint and a social licence risk, as freshwater consumption by brine processing, dust suppression, and camp operations in regions where water resources are shared with indigenous communities and agricultural users generates regulatory scrutiny, community opposition, and permitting complexity that can delay project timelines by years and impose water management system capital investments that are significant relative to total project development costs.

Competition from Non-South American Supply Sources, Chinese Midstream Processing Dominance, and Battery Chemistry Evolution Introducing Demand Uncertainty

South American battery metal producers face competitive supply dynamics from alternative global resource development programs, the established dominance of Chinese midstream battery material processing operations, and the evolving trajectory of battery cell chemistry whose future composition will determine the relative demand intensities for individual battery metals in ways that introduce strategic uncertainty into long-term resource development investment decisions. Australia’s hard rock spodumene lithium mining industry, which produced approximately 340,000 metric tons of lithium carbonate equivalent in 2025 and benefits from a stable investment environment, established export logistics infrastructure, and existing long-term offtake relationships with Chinese and South Korean battery material processors, represents a significant competitive supply source for the global lithium market whose output growth trajectory constrains the pricing environment available to South American brine lithium producers. China’s dominance of battery material midstream processing, including lithium hydroxide refining, nickel sulphate production, cobalt chemical processing, and cathode active material manufacturing, means that a substantial proportion of South American battery metal output is currently exported as relatively low-value mineral concentrates or intermediate products to Chinese processors rather than being converted to higher-value battery material products within South America, limiting the regional economic value capture from battery metal production and creating supply chain geopolitical vulnerability for battery manufacturers in the United States, European Union, and other regions seeking to diversify away from China-dependent battery material supply chains.

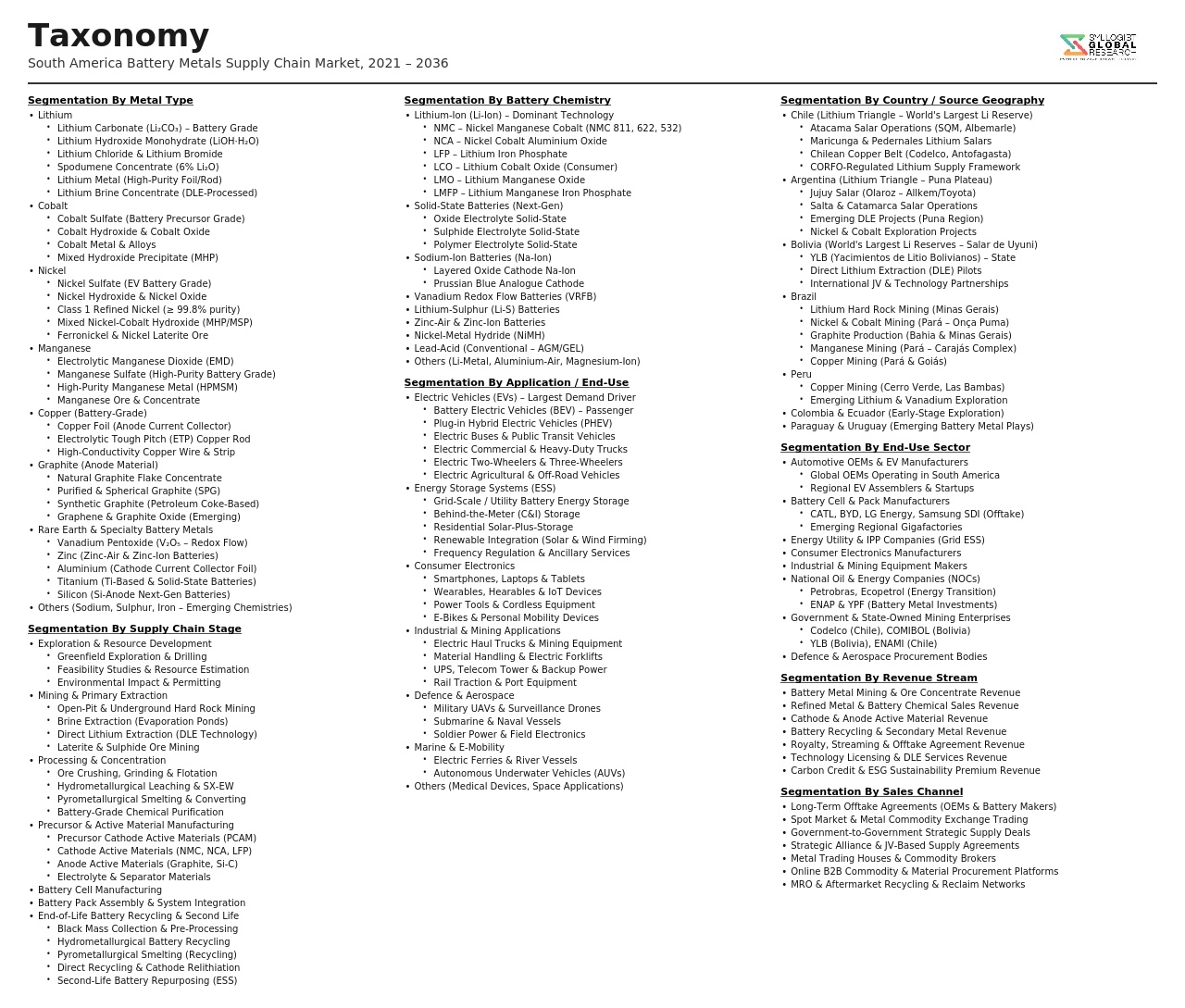

Market Segmentation

- Segmentation By Metal Type

- Lithium (Lithium Carbonate and Lithium Hydroxide)

- Nickel (Nickel Sulphate and Mixed Hydroxide Precipitate)

- Cobalt (Cobalt Sulphate and Cobalt Hydroxide)

- Manganese (Battery-Grade Manganese Sulphate and EMD)

- Copper (Refined Copper and Copper Sulphate)

- Graphite (Natural and Synthetic Anode Material)

- Vanadium (Vanadium Pentoxide and Electrolyte)

- Others

- Segmentation By Value Chain Stage

- Exploration and Resource Delineation

- Mining and Extraction (Open Pit, Underground, and Brine Extraction)

- Primary Processing and Concentration

- Hydrometallurgical and Chemical Refining

- Battery-Grade Material and Precursor Production

- Cathode Active Material and Anode Material Manufacturing

- Battery Cell Component Supply

- Segmentation By Extraction Technology

- Solar Evaporation Pond Brine Extraction

- Direct Lithium Extraction (Sorbent-Based Ion Exchange)

- Direct Lithium Extraction (Solvent Extraction and Membrane Filtration)

- Open Pit Hard Rock Mining

- Underground Hard Rock Mining

- Laterite Nickel Hydrometallurgical Processing (HPAL)

- Sulphide Nickel Pyrometallurgical Processing

- Others

- Segmentation By End-Use Application

- Electric Vehicle Battery Packs

- Stationary and Grid-Scale Energy Storage Systems

- Consumer Electronics Batteries

- Industrial and Commercial Energy Storage

- E-Mobility (Two-Wheelers, Three-Wheelers, and Buses)

- Others

- Segmentation By Battery Chemistry

- Lithium Nickel Manganese Cobalt Oxide (NMC) Batteries

- Lithium Nickel Cobalt Aluminium Oxide (NCA) Batteries

- Lithium Iron Phosphate (LFP) Batteries

- Lithium Manganese Oxide (LMO) Batteries

- Solid-State and Next-Generation Battery Chemistries

- Others

- Segmentation By Country

- Chile

- Argentina

- Brazil

- Bolivia

- Peru

- Colombia

- Other South American Nations

- Segmentation By Ownership Structure

- National Government Enterprises and State-Owned Mining Companies

- Large Diversified International Mining Companies

- Mid-Tier and Junior Mining and Exploration Companies

- Battery Manufacturer and Automotive OEM Direct Investment

- Joint Ventures and Public-Private Partnership Structures

- Segmentation By Off-Take Destination

- China (Battery Material Processors and Cell Manufacturers)

- United States and Canada

- European Union

- Japan and South Korea

- Domestic South American Battery Value Chain

- Others

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total valuation of the South America Battery Metals Supply Chain Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by metal type, lithium, nickel, cobalt, manganese, copper, and graphite, by country, Chile, Argentina, Brazil, Bolivia, Peru, and others, and by value chain stage, mining, primary processing, and refined battery material production, to enable mining investors, battery manufacturers, automotive OEMs, and government policymakers to identify which metal categories, jurisdictions, and supply chain stages will generate the highest absolute revenue and most strategically significant supply contributions across the forecast period?

- How is the competitive landscape between conventional solar evaporation brine lithium production and emerging direct lithium extraction technology platforms expected to evolve through 2034 in Chile and Argentina, what are the projected production cost trajectories, recovery efficiency improvements, and capital expenditure requirements of commercial-scale direct lithium extraction deployments relative to conventional evaporation systems, and which direct lithium extraction technology platforms and project developers are best positioned to achieve commercial-scale production volumes that can displace or supplement evaporation pond output within the forecast period?

- How are the national resource policy frameworks governing lithium and battery metal development in Chile, Argentina, Bolivia, and Brazil, including state enterprise participation requirements, fiscal stability provisions, royalty and taxation regimes, environmental permitting standards, and indigenous community consultation obligations, expected to evolve through 2034, and what are the implications of divergent national policy trajectories for the relative attractiveness and pace of battery metal project investment across South American jurisdictions in the context of intensifying global competition for battery metal supply commitments from resource consuming nations?

- What is the trajectory of South American downstream value addition in battery metals through 2034, encompassing lithium carbonate-to-hydroxide conversion, nickel mixed hydroxide precipitate-to-sulphate refining, cathode precursor active material manufacturing, and battery cell assembly, which jurisdictions and investment programs are most likely to successfully advance from raw material export toward integrated battery material production, and what are the enabling infrastructure, technology transfer, workforce development, and policy incentive requirements for South American nations to capture a materially larger share of battery value chain economics than they currently retain from mineral resource export alone?

- Who are the leading mining companies, lithium chemical producers, nickel and cobalt processors, national government enterprises, and battery supply chain investors currently shaping the competitive and strategic landscape of the South America battery metals supply chain market, and what are their respective resource portfolios and production capacity positions across lithium, nickel, cobalt, and copper, project development and expansion timelines through 2034, offtake agreements and strategic partnerships with battery manufacturers and automotive OEMs, technology investment commitments in direct lithium extraction and downstream processing, and strategic responses to the geopolitical, regulatory, and competitive dynamics reshaping the global battery metals supply chain?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Mining, Processing & Refining Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Resource Nationalism, Royalty Regime Changes & Government Intervention Risk in Mining and Processing Operations

- Geopolitical Risk: US-China Technology Competition, Critical Mineral Export Controls & South American Supply Chain Leverage

- Environmental, Social & Governance (ESG) Risk: Indigenous Land Rights, Water Usage in Arid Regions & Community Opposition to Mining

- Price Volatility Risk: Lithium, Cobalt, Nickel and Manganese Commodity Cycle Exposure for Supply Chain Participants

- Infrastructure Deficit Risk: Port Capacity, Road and Rail Connectivity Constraints Affecting Ore and Concentrate Export Logistics

- Regulatory Framework & Standards

- National Mining Codes, Concession Frameworks & Royalty Structures: Chile, Argentina, Bolivia, Brazil and Peru Comparative Analysis

- Lithium Nationalisation and State Participation Policies: Bolivia YPFB-Lithium, Chile CODELCO-Lithium and Argentina Provincial Regime Variations

- Environmental Impact Assessment (EIA), Water Rights Regulation & Brine Extraction Permits for Lithium Operations in the Lithium Triangle

- Critical Minerals Strategies and Bilateral Supply Agreements: US IRA, EU Critical Raw Materials Act & South American Offtake and Investment Treaties

- Export Tax, Local Value-Addition Incentives & Free Trade Zone Frameworks Applicable to Battery Metal Concentrate and Refined Product Exports

- South America Battery Metals Supply Chain Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Metric Tons of Metal Content)

- Market Size & Forecast by Metal Type

- Lithium (Brine-Derived and Hard Rock Spodumene)

- Cobalt

- Nickel (Sulphide and Laterite)

- Manganese

- Copper (as Battery and EV Wiring Enabler Metal)

- Graphite (Natural and Synthetic Anode Material)

- Rare Earth Elements (REEs) for Battery and EV Motor Applications

- Other Battery Metals (Vanadium, Titanium and Aluminium)

- Market Size & Forecast by Supply Chain Stage

- Mining and Ore Extraction

- Ore Processing and Beneficiation

- Smelting, Refining and Hydrometallurgical Processing

- Battery-Grade Chemical Production (Lithium Carbonate, Lithium Hydroxide, Nickel Sulphate, Cobalt Sulphate and MnSO4)

- Precursor Cathode Active Material (PCAM) Manufacturing

- Cathode Active Material (CAM) Manufacturing

- Battery Cell and Pack Assembly

- Battery Recycling and Secondary Supply

- Market Size & Forecast by Battery Chemistry

- Lithium Iron Phosphate (LFP)

- Nickel Manganese Cobalt (NMC: 111, 532, 622 and 811)

- Nickel Cobalt Aluminium (NCA)

- Solid-State and Next-Generation Battery Chemistries

- Other Battery Chemistries (LMO, NiMH and Vanadium Redox Flow)

- Market Size & Forecast by Application

- Electric Vehicles (Passenger EVs, Commercial EVs and Two and Three Wheelers)

- Energy Storage Systems (Grid-Scale, Industrial and Behind-the-Meter)

- Consumer Electronics (Smartphones, Laptops and Portable Devices)

- Industrial and Other Applications (Material Handling, Marine and Defence)

- Market Size & Forecast by End-User

- Global Battery Cell and Gigafactory Manufacturers (Asia, Europe and North America)

- Automotive OEMs and EV Manufacturers

- Energy Storage System Developers and Utilities

- South American Domestic Industrial and Emerging EV End-Users

- Market Size & Forecast by Trade Flow Type

- Raw Ore and Concentrate Exports

- Intermediate Refined Metal and Chemical Exports

- Battery-Grade Refined Product Exports (Lithium Carbonate, Lithium Hydroxide and Nickel Sulphate)

- Domestic Value-Addition and In-Country Processing

- Market Size & Forecast by Sales and Offtake Channel

- Long-Term Offtake Agreements with Global Battery Manufacturers and Automakers

- Spot Market and Commodity Exchange Trading

- Government-to-Government Supply and Strategic Reserve Agreements

- Joint Venture and Equity Participation Offtake Structures

- Lithium Triangle (Chile, Argentina and Bolivia) Battery Metals Supply Chain Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tons of Metal Content)

- By Metal Type

- By Supply Chain Stage

- By Battery Chemistry

- By Application

- By End-User

- By Trade Flow Type

- By Country

- By Sales and Offtake Channel

- Market Size & Forecast

- Brazil Battery Metals Supply Chain Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tons of Metal Content)

- By Metal Type

- By Supply Chain Stage

- By Battery Chemistry

- By Application

- By End-User

- By Trade Flow Type

- By Country

- By Sales and Offtake Channel

- Market Size & Forecast

- Peru and Ecuador Battery Metals Supply Chain Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tons of Metal Content)

- By Metal Type

- By Supply Chain Stage

- By Battery Chemistry

- By Application

- By End-User

- By Trade Flow Type

- By Country

- By Sales and Offtake Channel

- Market Size & Forecast

- Colombia and Venezuela Battery Metals Supply Chain Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tons of Metal Content)

- By Metal Type

- By Supply Chain Stage

- By Battery Chemistry

- By Application

- By End-User

- By Trade Flow Type

- By Country

- By Sales and Offtake Channel

- Market Size & Forecast

- Rest of South America (Paraguay, Uruguay and Guyana) Battery Metals Supply Chain Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tons of Metal Content)

- By Metal Type

- By Supply Chain Stage

- By Battery Chemistry

- By Application

- By End-User

- By Trade Flow Type

- By Country

- By Sales and Offtake Channel

- Market Size & Forecast

- Country-Wise* Battery Metals Supply Chain Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tons of Metal Content)

- By Metal Type

- By Supply Chain Stage

- By Battery Chemistry

- By Application

- By End-User

- By Trade Flow Type

- By Country

- By Sales and Offtake Channel

- Market Size & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: Chile, Argentina, Bolivia, Brazil, Peru, Ecuador, Colombia, Venezuela, Paraguay, Uruguay, Guyana, Suriname

- Technology Landscape & Innovation Analysis

- Lithium Brine Direct Lithium Extraction (DLE) Technology Deep-Dive: Adsorption, Solvent Extraction and Membrane-Based DLE Systems

- Hard Rock Lithium Processing: Spodumene Roasting, Acid Leaching and Lithium Hydroxide Conversion Technology

- Nickel Laterite Processing: High-Pressure Acid Leach (HPAL), Ferronickel and Mixed Hydroxide Precipitate (MHP) Technology

- Battery-Grade Lithium Carbonate and Lithium Hydroxide Purification and Specification Compliance Technology

- Precursor Cathode Active Material (PCAM) Co-Precipitation Technology and In-Region Manufacturing Feasibility

- Battery Recycling Technology: Hydrometallurgical and Pyrometallurgical Black Mass Processing for Secondary Battery Metal Recovery

- Digital Supply Chain Traceability, Blockchain-Based Provenance and Responsible Sourcing Certification Platforms

- Patent & IP Landscape in Battery Metal Extraction and Processing Technologies

- Value Chain & Supply Chain Analysis

- Upstream Mining and Resource Development: Exploration, Reserve Estimation and Mine Development in South America

- Ore Processing, Beneficiation and Concentrate Logistics to Port and Smelter

- Refining and Hydrometallurgical Processing: In-Country vs. Export of Intermediate for Offshore Refining

- Battery-Grade Chemical Production and Quality Specification Compliance for Global Gigafactory Supply

- Export Logistics: Port Infrastructure, Shipping Routes and Freight Cost Analysis for South American Battery Metal Exports

- Offtake and Trading: Global Battery Manufacturer, Automaker and Commodity Trader Procurement Landscape

- Battery Recycling and Closed-Loop Secondary Supply Chain Development in South America

- Pricing Analysis

- Lithium Carbonate and Lithium Hydroxide Price Cycle Analysis: 2018 to 2030 Spot and Contract Price Trends

- Nickel, Cobalt and Manganese LME and Fastmarkets Price Benchmarking for Battery-Grade Products

- South American Production Cost Analysis: Cash Cost Per Tonne for Lithium, Nickel and Copper vs. Global Peers

- Value-Addition Premium: Price Differential Between Raw Ore, Concentrate, Refined Metal and Battery-Grade Chemical Products

- Offtake Agreement Pricing Structures: Fixed Price, Index-Linked and Floor-Price Mechanisms in South American Battery Metal Contracts

- Export Tax and Royalty Impact on Netback Pricing and Project Economics for South American Battery Metal Producers

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of South American Battery Metal Supply Chains: Carbon Footprint, Water Intensity and Biodiversity Impact Across Mining and Processing Routes

- Water Stress and Brine Extraction Impact in the Atacama and Puna Salars: Scientific Evidence, Regulatory Responses and Industry Practices

- Indigenous Community Rights, Free Prior and Informed Consent (FPIC) & Social Licence to Operate in South American Mining Jurisdictions

- Responsible Sourcing Certification: IRMA, Initiative for Responsible Mining Assurance, RMI and EU Battery Regulation Due Diligence Requirements

- Decarbonisation of South American Battery Metal Mining and Processing: Renewable Energy Integration, Green Hydrogen and Net-Zero Mining Pathways

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Metal Type and Supply Chain Stage)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Metal Type, Supply Chain Stage and Country

- Player Classification

- Integrated Global Mining Majors with South American Battery Metal Operations

- South American State-Owned Enterprises and National Mining Companies

- Junior and Mid-Tier Lithium, Nickel and Cobalt Exploration and Development Companies

- Battery Chemical Refiners and Converters with South American Feedstock Sourcing

- Chinese Battery Manufacturers and Automakers with South American Upstream Equity Investments

- Battery Recyclers and Secondary Supply Chain Operators

- Competitive Analysis Frameworks

- Market Share Analysis by Metal Type, Supply Chain Stage and Country

- Company Profile

- Company Overview & Headquarters

- Battery Metal Asset Portfolio: Mine, Processing and Chemical Plant Holdings in South America

- Production Capacity, Annual Output and Reserve Base

- Key Offtake Agreements and Customer Relationships

- Revenue (Battery Metals Segment) and Capital Expenditure

- Technology Differentiators, DLE or Processing IP & Certifications

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Mine Expansions, New Projects, Offtake Deals and Regulatory Milestones)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Resource Scale vs. Processing Integration)

- Key Company Profiles

- Market Structure & Concentration

- Strategic Outlook & Opportunity Analysis

- Strategic Output

- Market Opportunity Matrix: By Metal Type, Supply Chain Stage, Battery Chemistry, Application and Country

- White Space Opportunity Analysis

- Strategic Recommendations

- Resource Development & Mining Asset Strategy

- In-Country Value-Addition & Processing Integration Strategy

- Offtake, Trading & Customer Diversification Strategy

- Regulatory Navigation & Government Relations Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability, Responsible Sourcing & ESG Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output