Global Bio-Based Specialty Intermediates Market By Product Type, By Feedstock, By Technology, By Application, By End Use Industry, By Distribution Channel, By Region, Competition, Forecast and Opportunities, 2021-2036F

Market Definition

The Global Bio-Based Specialty Intermediates Market encompasses the production, processing, and commercial supply of high-value chemical intermediates derived from biological feedstocks including agricultural residues, lignocellulosic biomass, vegetable oils, sugars, starches, and microbial fermentation outputs. The market includes bio-based succinic acid, itaconic acid, levulinic acid, furandicarboxylic acid, bio-glycols, biosurfactants, bio-based polyols, amino acid-derived intermediates, and fermentation-derived platform chemicals used as building blocks in polymer synthesis, pharmaceutical manufacturing, agrochemical formulation, cosmetic ingredient production, and specialty coating applications procured by chemical manufacturers, formulation companies, and branded product developers globally.

Market Insights

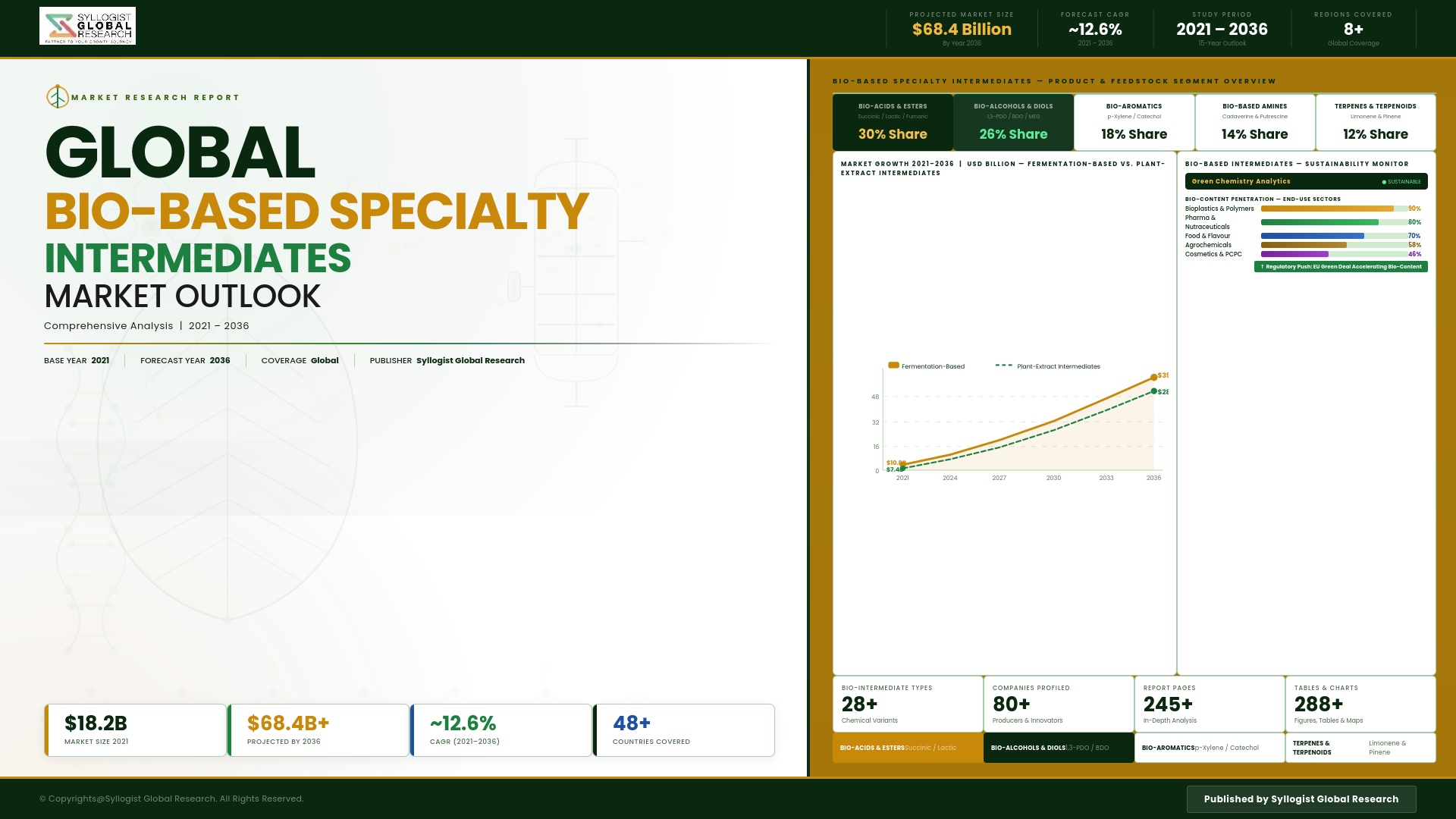

The global bio-based specialty intermediates market is at a decisive commercialization crossroads, propelled by the convergence of sustainability-driven regulatory pressure on petrochemical-derived intermediates, advancing biorefinery and synthetic biology technology platforms enabling economically competitive bio-based production routes, and an accelerating shift in downstream formulation and polymer industries toward bio-derived chemical inputs as brands respond to consumer demand and legislative mandates for lower carbon footprint supply chains. The market was valued at approximately USD 9.7 billion in 2025 and is projected to reach USD 28.4 billion by 2034, advancing at a compound annual growth rate of 12.7% through the forecast period, as bio-based specialty intermediates progressively displace petrochemical equivalents across polymer, pharmaceutical, personal care, and agrochemical supply chains where the functional performance of bio-derived alternatives has been validated at commercial scale and cost parity with fossil-based counterparts is increasingly achievable across a widening range of target molecules.

The bio-based polymer intermediate segment is generating the highest near-term commercial momentum, anchored by the rapid scaling of furandicarboxylic acid production as a bio-based alternative to terephthalic acid in polyethylene furanoate polyester synthesis, bio-based succinic acid displacement of adipic acid in polyurethane and polybutylene succinate applications, and the commercialization of bio-based 1,4-butanediol and 1,3-propanediol as diol monomers for biodegradable and bio-attributed polymer systems. These polymer intermediate applications benefit from the scale economics of downstream polymer manufacturing that create large-volume demand pull capable of justifying the substantial biorefinery capital investment required to bring new bio-based intermediate production routes to commercial scale. The synthetic biology and metabolic engineering revolution is simultaneously reshaping the competitive economics of bio-based specialty intermediate production by enabling the design of microorganism production strains with substantially higher titer, yield, and productivity performance than naturally occurring biosynthetic pathways, compressing fermentation production costs and expanding the range of target molecules whose bio-based production economics can compete with petrochemical alternatives at commercial scale without mandatory regulatory or policy support.

The pharmaceutical and cosmetic application segments represent the highest per-unit-value categories within the bio-based specialty intermediate landscape, with amino acid-derived pharmaceutical intermediates, bio-based chiral building blocks, and fermentation-derived cosmetic actives commanding significant price premiums over equivalent petrochemical-derived intermediates where the biological origin of the intermediate contributes directly to product positioning, regulatory compliance, or efficacy differentiation in end consumer formulations. Circular bioeconomy policy frameworks in the European Union, including the EU Bioeconomy Strategy and the Chemical Strategy for Sustainability, are creating regulatory tailwinds that impose increasing compliance burdens on fossil-derived chemical intermediates while facilitating accelerated approval pathways for bio-based replacements, generating a structural competitive shift in European formulation markets that is creating durable procurement incentives for bio-based intermediate substitution programs across personal care, coating, and polymer applications. Europe leads in regulatory-driven bio-based intermediate adoption, anchored by strong policy support and biorefinery investment. North America maintains significant commercial-scale bio-based intermediate production through corn and agricultural residue-based biorefinery infrastructure. Asia-Pacific is projected to record the highest compound annual growth rate through 2034, driven by rapidly expanding bioeconomy investment in China, India, and Southeast Asia where abundant agricultural feedstock availability and growing chemical industry sustainability commitments are accelerating bio-based intermediate capacity development.

Key Drivers

Accelerating Regulatory Pressure on Petrochemical-Derived Intermediates and Corporate Sustainability Commitments Generating Structural Demand Pull for Bio-Based Intermediate Substitution Across Formulation Industries

The progressive tightening of chemical substance regulations governing hazardous petrochemical intermediates, combined with expanding carbon pricing mechanisms, plastic and chemical waste directives, and scope three emissions reporting obligations that expose downstream chemical and consumer goods manufacturers to material carbon liability from fossil-derived intermediate procurement, is generating structural demand pull for bio-based alternatives whose lower carbon footprint and renewable origin provide measurable compliance and sustainability reporting advantages. Major consumer goods companies, polymer producers, and specialty chemical formulators are establishing internal bio-based content targets and supplier qualification programs for bio-derived intermediates that create durable long-term procurement commitments capable of underpinning the offtake economics required to justify commercial-scale biorefinery and fermentation facility investment by bio-based intermediate producers.

Synthetic Biology and Metabolic Engineering Advances Enabling Economically Competitive Bio-Based Production Routes Across an Expanding Range of High-Value Specialty Intermediate Target Molecules

The maturation of synthetic biology tools including CRISPR-based genome editing, computational pathway design, high-throughput strain screening, and adaptive laboratory evolution is enabling bio-based intermediate producers to develop microbial production strains with titer, yield, and productivity performance approaching or exceeding the economic viability thresholds of petrochemical synthesis routes for a rapidly expanding catalog of specialty chemical target molecules, fundamentally altering the competitive economics of bio-based intermediate production beyond the limited set of molecules where biological production had historically been cost-competitive. Continuous improvement in fermentation process engineering, downstream product recovery and purification efficiency, and biorefinery integrated process optimization is further compressing the production cost gap between bio-based and fossil-derived specialty intermediates, accelerating the timeline to cost parity across target molecule categories of commercial significance to polymer, pharmaceutical, and agrochemical applications.

Circular Bioeconomy Policy Frameworks and Renewable Chemical Investment Incentive Programs Mobilizing Capital into Bio-Based Intermediate Production Infrastructure Across Major Chemical Markets

Government circular bioeconomy investment programs, renewable chemical production tax credits, and agricultural residue valorization funding frameworks across the European Union, the United States, Brazil, and emerging Asian markets are providing the concessional capital and risk-sharing mechanisms that bio-based specialty intermediate projects require to bridge the financing gap between laboratory-validated production economics and commercially bankable investment structures capable of attracting institutional capital at competitive cost of capital. The United States Bipartisan Infrastructure Law and Inflation Reduction Act provisions supporting bio-based chemical manufacturing, combined with European Innovation Fund and national bioeconomy strategy funding mechanisms, are collectively mobilizing a multi-billion dollar bio-based chemical infrastructure investment cycle whose productive output will materially expand commercial bio-based intermediate supply through the forecast period.

Key Challenges

Feedstock Availability Variability, Agricultural Supply Chain Seasonality, and Land Use Competition Constraining Bio-Based Intermediate Production Cost Stability and Scale-Up Planning

Bio-based specialty intermediate production economics are fundamentally sensitive to feedstock cost and availability dynamics that introduce production cost variability substantially greater than that experienced by petrochemical intermediate producers operating on fossil-based raw material supply chains whose price dynamics, while volatile, are not subject to the seasonal availability cycles, weather-dependent yield variability, logistical concentration challenges, and land use competition from food, feed, and fuel applications that characterize agricultural and lignocellulosic biomass feedstock procurement. Achieving the feedstock supply security, quality consistency, and cost predictability required to underwrite long-term bio-based intermediate supply agreements with downstream chemical and polymer customers demands sophisticated procurement infrastructure, geographic sourcing diversification, and contractual risk-sharing mechanisms that add operational complexity and procurement overhead to bio-based intermediate production relative to petrochemical manufacturing.

Downstream Customer Product Qualification Requirements, Functional Performance Validation Timelines, and Supply Chain Certification Complexity Constraining Bio-Based Intermediate Market Penetration Rate

Bio-based specialty intermediates entering established petrochemical intermediate supply chains face demanding customer qualification programs that require demonstration of functional performance equivalence or superiority across all relevant application parameters, regulatory compliance across applicable chemical registration and consumer product safety frameworks, and supply continuity assurance at the volume and quality consistency levels required by downstream manufacturing operations whose production processes have been optimized around the specific physicochemical properties of incumbent fossil-derived intermediates. The qualification timeline for bio-based intermediates in pharmaceutical, polymer, and specialty coating applications can extend across multiple years of application testing, regulatory documentation, and production audit processes, creating a commercialization lag between production capacity availability and revenue-generating customer qualification that strains the cash flow economics of bio-based intermediate producers during early commercial scaling phases.

Capital Intensity of Commercial-Scale Biorefinery and Fermentation Infrastructure and the Financing Barriers Facing Bio-Based Intermediate Projects in Conventional Debt and Equity Markets

The commercial-scale production of bio-based specialty intermediates requires substantial capital investment in fermentation bioreactor infrastructure, downstream purification systems, feedstock handling and pretreatment facilities, and utility infrastructure whose combined capital expenditure typically exceeds comparable petrochemical intermediate production facility investment on a per-unit-output basis, creating financing requirements that are challenging to meet through conventional chemical industry debt markets where lenders apply conservative technology risk adjustments to first-of-kind and early-commercial-stage biorefinery assets. The combination of capital intensity, extended construction and commissioning timelines, feedstock risk, and customer qualification uncertainty creates a project finance risk profile that limits the pool of available capital providers and elevates the weighted average cost of capital for bio-based intermediate projects relative to petrochemical equivalents, constraining the pace of commercial capacity expansion.

Market Segmentation

- Segmentation By Product Type

- Bio-Based Dicarboxylic Acids (Succinic, Itaconic, Fumaric, Adipic)

- Bio-Based Furan Compounds (FDCA, HMF, Furfural)

- Bio-Based Glycols and Diols (1,3-PDO, 1,4-BDO, Bio-MEG)

- Amino Acid-Derived Intermediates

- Bio-Based Levulinic Acid and Derivatives

- Biosurfactants and Bio-Based Surface Active Agents

- Fermentation-Derived Specialty Platform Chemicals

- Others

- Segmentation By Feedstock

- Corn and Starch-Based Feedstocks

- Sugarcane and Sugar-Based Feedstocks

- Lignocellulosic Biomass and Agricultural Residues

- Vegetable Oils and Oleochemical Feedstocks

- Municipal Solid Waste and Organic Waste Streams

- Carbon Dioxide and Syngas-Based Feedstocks

- Others

- Segmentation By Technology

- Microbial Fermentation and Metabolic Engineering

- Enzymatic Biotransformation and Biocatalysis

- Thermochemical Conversion and Hydrothermal Processing

- Synthetic Biology and Genetically Engineered Production Organisms

- Integrated Biorefinery Platforms

- Chemocatalytic Conversion of Bio-Based Feedstocks

- Others

- Segmentation By Application

- Bio-Based Polymer and Monomer Synthesis

- Pharmaceutical Active Ingredient and Intermediate Manufacturing

- Personal Care and Cosmetic Ingredient Formulation

- Agrochemical and Crop Protection Formulation

- Specialty Coating and Adhesive Formulation

- Cleaning and Detergent Product Formulation

- Food and Feed Additive Applications

- Others

- Segmentation By End Use Industry

- Polymer and Plastics Manufacturing

- Pharmaceutical and Biotechnology

- Personal Care and Cosmetics

- Agrochemical and Agricultural Sciences

- Paints, Coatings, and Construction Chemicals

- Household and Industrial Cleaning Products

- Food Processing and Nutraceuticals

- Others

- Segmentation By Distribution Channel

- Direct Long-Term Offtake Agreements with Industrial Customers

- Specialty Chemical Distributor and Trading Networks

- Spot Market and Exchange-Based Procurement

- Online Chemical Trading Platforms

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Bio-Based Specialty Intermediates Market in 2025, projected through 2034, disaggregated by product type, feedstock, and end use industry, enabling chemical producers, biorefinery developers, investors, and downstream formulators to identify the highest-growth product categories and most durable revenue opportunities across the bio-based intermediates value chain?

- How are polymer manufacturers, pharmaceutical developers, personal care formulators, and agrochemical producers structuring bio-based intermediate qualification and procurement programs, and which product categories are achieving cost parity with petrochemical equivalents and generating the strongest downstream substitution momentum across regulated and consumer-facing application markets through 2034?

- What impact are the European Union Chemical Strategy for Sustainability, Bioeconomy Strategy investment frameworks, United States Inflation Reduction Act bio-based chemical provisions, and emerging Asian bioeconomy policy programs having on bio-based intermediate production capacity investment timelines, geographic supply chain development, and competitive positioning of regional producers through the forecast period?

- Which bio-based specialty intermediate product segments, including FDCA for polyethylene furanoate polymers, bio-succinic acid for polyurethane applications, and amino acid-derived pharmaceutical intermediates, are generating the highest commercial-scale production investment and downstream qualification activity, and what technology and cost performance thresholds are defining near-term commercial viability?

- How is the competitive landscape structured among dedicated bio-based chemical companies, integrated agricultural biorefinery operators, synthetic biology platform developers, and major petrochemical producers entering bio-based intermediates, and what feedstock, technology, customer partnership, and scale-up execution strategies are enabling leading producers to secure long-term downstream offtake commitments?

- What feedstock supply volatility, customer qualification timeline, capital intensity, and project financing barriers are constraining bio-based intermediate commercial scaling rates, and how are producers, investors, and policy programs addressing these challenges through concessional financing mechanisms, offtake risk-sharing structures, and integrated biorefinery co-product optimization strategies?

- Which regional bio-based specialty intermediate markets, specifically Europe, North America, and Asia-Pacific, are expected to generate the most substantial production capacity expansion and demand growth through 2034, and what feedstock availability, bioeconomy policy support, downstream industry proximity, and sustainability regulatory frameworks are shaping investment decisions and competitive positioning in each region?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Feedstock Supply, Agricultural Volatility & Land-Use Change Risk

- Fermentation Yield, Scale-Up & Process Economics Risk

- Regulatory, Food-vs-Fuel & Biobased Content Certification Risk

- Technology Maturity, Strain Performance & IP Infringement Risk

- Capital Investment, Offtake Agreement & Green Premium Acceptance Risk

- Regulatory Framework & Standards

- Biobased Content Certification, USDA BioPreferred & EU Ecolabel Frameworks

- Sustainable Feedstock Sourcing, ISCC, RSB & Chain-of-Custody Standards

- Food Contact, FDA, EFSA & Biomedical Bio-Intermediate Compliance Requirements

- End-of-Life, Biodegradability, Compostability & Circular Economy Regulations

- Green Finance, ESG Disclosure & Sustainable Chemistry Procurement Standards

- Global Bio-based Specialty Intermediates Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Kilotons)

- Market Size & Forecast by Intermediate Type

- Organic Acids (Succinic, Lactic, Itaconic, Adipic, Levulinic & 3-Hydroxypropionic Acid)

- Bio-Diols, Polyols & Glycols (1,3-Propanediol, 1,4-Butanediol, Bio-MEG, Bio-MPG & Isosorbide)

- Furans & Furanics (Furfural, Hydroxymethylfurfural & Furan Dicarboxylic Acid)

- Bio-Based Aromatics & Lignin-Derived Compounds (Bio-BTX, Bio-Phenol & Vanillin)

- Bio-Olefins & Drop-In Building Blocks (Bio-Ethylene, Bio-Propylene & Bio-Isobutylene)

- Bio-Alcohols & Intermediate Alcohols (Bio-Butanol, Bio-Isobutanol & Furfuryl Alcohol)

- Fatty Acid, Fatty Alcohol & Glycerol Derivatives

- Bio-Amines, Bio-Amino Acids & Specialty Nitrogen Intermediates

- Terpenes, Terpenoids & Natural Resin-Derived Intermediates

- Market Size & Forecast by Technology

- First-Generation Sugar & Starch-Based Fermentation Technology

- Second-Generation Lignocellulosic & Agricultural Residue Conversion Technology

- Vegetable Oil, Fatty Acid & Oleochemical Conversion Technology

- Glycerol, Biodiesel Co-Product & Waste-Based Valorisation Technology

- Algae, Seaweed & Third-Generation Biomass Conversion Technology

- Lignin Valorisation & Aromatic Depolymerisation Technology

- CO2-Based & Gas Fermentation Technology

- Biocatalysis, Enzymatic Conversion & Cell-Free Synthesis Technology

- Synthetic Biology, Metabolic Engineering & Precision Fermentation Technology

- Market Size & Forecast by Form

- Liquid Bio-Intermediate & Concentrate

- Crystalline Powder & Granular Solid

- Aqueous Solution & Emulsion

- Paste, Slurry & Viscous Formulation

- Pelletised, Flake & Masterbatch Form

- Market Size & Forecast by Production Process

- Aerobic & Anaerobic Fermentation

- Enzymatic & Biocatalytic Conversion

- Thermochemical (Pyrolysis & Gasification) Processing

- Hybrid Bio-Chemocatalytic & Downstream Purification

- Market Size & Forecast by Application

- Bioplastics, Biopolymers & Sustainable Packaging

- Paints, Coatings, Adhesives & Sealants

- Surfactants, Detergents, Home & Personal Care

- Pharmaceutical, Nutraceutical & Biomedical Ingredients

- Food, Beverage, Flavour & Fragrance Ingredients

- Lubricants, Plasticisers & Specialty Industrial Chemicals

- Market Size & Forecast by End-User

- Bioplastic, Biopolymer & Sustainable Packaging Producer

- Coating, Paint, Adhesive & Sealant Formulator

- Personal Care, Home Care & Cosmetic Brand

- Pharmaceutical, Nutraceutical & Food Ingredient Company

- Industrial, Agrochemical & Specialty Chemical Manufacturer

- Market Size & Forecast by Sales Channel

- Direct Long-Term Offtake & Strategic Supply Contract

- Distributor, Specialty Chemical Trader & Spot Market Sales

- Joint Venture, Licensing & Strain Technology Transfer

- Toll Fermentation, Custom Synthesis & Contract Manufacturing Service

- North America Bio-based Specialty Intermediates Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotons)

- By Intermediate Type

- By Technology

- By Form

- By Production Process

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Bio-based Specialty Intermediates Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotons)

- By Intermediate Type

- By Technology

- By Form

- By Production Process

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Bio-based Specialty Intermediates Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotons)

- By Intermediate Type

- By Technology

- By Form

- By Production Process

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Bio-based Specialty Intermediates Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotons)

- By Intermediate Type

- By Technology

- By Form

- By Production Process

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Bio-based Specialty Intermediates Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotons)

- By Intermediate Type

- By Technology

- By Form

- By Production Process

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Bio-based Specialty Intermediates Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotons)

- By Intermediate Type

- By Technology

- By Form

- By Production Process

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- *Countries Analysed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Italy, Norway, Sweden, China, Japan, India, Australia, South Korea, Singapore, Brazil, Chile, Saudi Arabia, UAE, Egypt, South Africa, Israel

- Technology Landscape & Innovation Analysis

- Organic Acid Fermentation Technology Deep-Dive (Succinic, Lactic, Itaconic & Adipic Acid Routes)

- Bio-Diol, Glycol & Polyol Production Technology (1,3-PDO, 1,4-BDO & Bio-MEG)

- Furan, Furanic & Bio-Aromatic Production Technology (HMF, FDCA & Lignin-Derived)

- Bio-Olefin, Bio-Ethylene & Drop-In Building Block Technology

- Fatty Acid, Oleochemical & Glycerol Derivative Conversion Technology

- Synthetic Biology, Strain Engineering & Precision Fermentation Technology

- Enzymatic, Biocatalytic & Cell-Free Bio-Intermediate Technology

- Patent & IP Landscape in Bio-based Specialty Intermediate Technologies

- Value Chain & Supply Chain Analysis

- Agricultural Feedstock, Sugar & Biomass Residue Supply Chain

- Vegetable Oil, Oleochemical & Fatty Acid Feedstock Supply Chain

- Lignin, Forestry Residue & Woody Biomass Supply Chain

- Fermentation, Biocatalysis & Downstream Purification Manufacturing Supply Chain

- Bioplastic, Biopolymer & Coating Formulator Procurement Landscape

- Distributor, Specialty Chemical Trader & Sustainability-Certified Channel

- Waste Valorisation, CO2 Capture & Circular Feedstock Loop

- Pricing Analysis

- Organic Acid (Succinic, Lactic & Itaconic) Pricing and Cost Structure Analysis

- Bio-Diol & Glycol (1,3-PDO, 1,4-BDO & Bio-MEG) Pricing and Margin Analysis

- Furan, FDCA & Bio-Aromatic Pricing Trend and Green Premium Analysis

- Bio-Olefin & Drop-In Intermediate Pricing versus Petrochemical Parity Analysis

- Bio-Intermediate Long-Term Offtake Contract, Indexation & Green Premium Analysis

- Total Bio-Based Value Chain Cost Economics: Cost per Ton & Learning Curve Analysis

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Bio-based Specialty Intermediates: Carbon Footprint, Energy Intensity & Water Footprint Across Feedstock Routes

- Carbon Neutrality, Biogenic Carbon Accounting & Net Zero Contribution of Bio-Intermediate Manufacturing

- Responsible Feedstock Sourcing, Land-Use Change & Food-vs-Fuel Due Diligence

- Environmental Compliance, Biodegradability, Compostability & End-of-Life Consideration

- Regulatory-Driven Sustainability, Biobased Content Certification, SDG 12 (Responsible Consumption) & SDG 13 (Climate Action) Alignment & Green Finance Eligibility

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Intermediate Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Intermediate Type, Technology & Geography

- Player Classification

- Integrated Biorefinery & Bio-based Chemical Companies

- Specialist Organic Acid & Fermentation-Based Intermediate Producers

- Bio-Diol, Glycol & Drop-In Bio-Olefin Manufacturers

- Furan, FDCA & Bio-Aromatic Technology Developers

- Oleochemical, Fatty Acid & Glycerol Derivative Producers

- Synthetic Biology, Precision Fermentation & Strain Technology Innovators

- Lignin Valorisation & Second-Generation Biomass Conversion Companies

- Custom Fermentation, Toll Manufacturing & Contract Bio-Synthesis Specialists

- Competitive Analysis Frameworks

- Market Share Analysis by Intermediate Type, Technology & Region

- Company Profile

- Company Overview & Headquarters

- Bio-based Specialty Intermediate Products & Technology Portfolio

- Key Customer Relationships & Reference Commercial Offtake Contracts

- Manufacturing Footprint & Production Capacity

- Revenue (Bio-based Intermediate Segment) & Order Book

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Capacity Expansion, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Intermediate Type, Technology, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output