Market Definition

The Global Bio-Based Surfactants Market encompasses the research, development, manufacture, distribution, and commercial application of surface-active agents synthesized entirely or substantially from renewable biological feedstocks including vegetable oils, plant-derived fatty acids, sugars and polysaccharides, amino acids, starch, and microbially produced metabolites, as opposed to conventional surfactants derived from petrochemical intermediates obtained through fossil fuel processing. Bio-based surfactants retain the defining amphiphilic molecular architecture of conventional surfactants, comprising a hydrophilic head group and a hydrophobic tail structure that collectively reduce surface and interfacial tension and enable emulsification, foaming, wetting, dispersing, solubilizing, and detergency functions across a broad spectrum of end-use applications. The market encompasses both fermentation-derived microbial biosurfactants, including rhamnolipids, sophorolipids, mannosylerythritol lipids, and lipopeptides such as surfactin and iturin produced through controlled microbial fermentation of renewable carbon substrates, and chemically processed bio-based surfactants including alkyl polyglucosides, methyl ester sulfonates, sucrose esters, sorbitan esters, amino acid-derived surfactants, and fatty alcohol ethoxylates manufactured from oleochemical feedstocks sourced from coconut oil, palm kernel oil, castor oil, rapeseed oil, soybean oil, and sugarcane-derived intermediates. End-use markets served by bio-based surfactants span personal care and cosmetics, household and institutional cleaning, agricultural formulation, food processing, textile and leather processing, oilfield chemistry, pharmaceutical manufacturing, and industrial process applications globally. Key participants include oleochemical and fatty acid producers, bio-based surfactant manufacturers, fermentation biotechnology companies, specialty chemical formulators, consumer goods companies, and national and international regulatory bodies whose chemical safety, biodegradability, and sustainable sourcing standards define the technical and commercial environment for bio-based surfactant adoption across global markets.

Market Insights

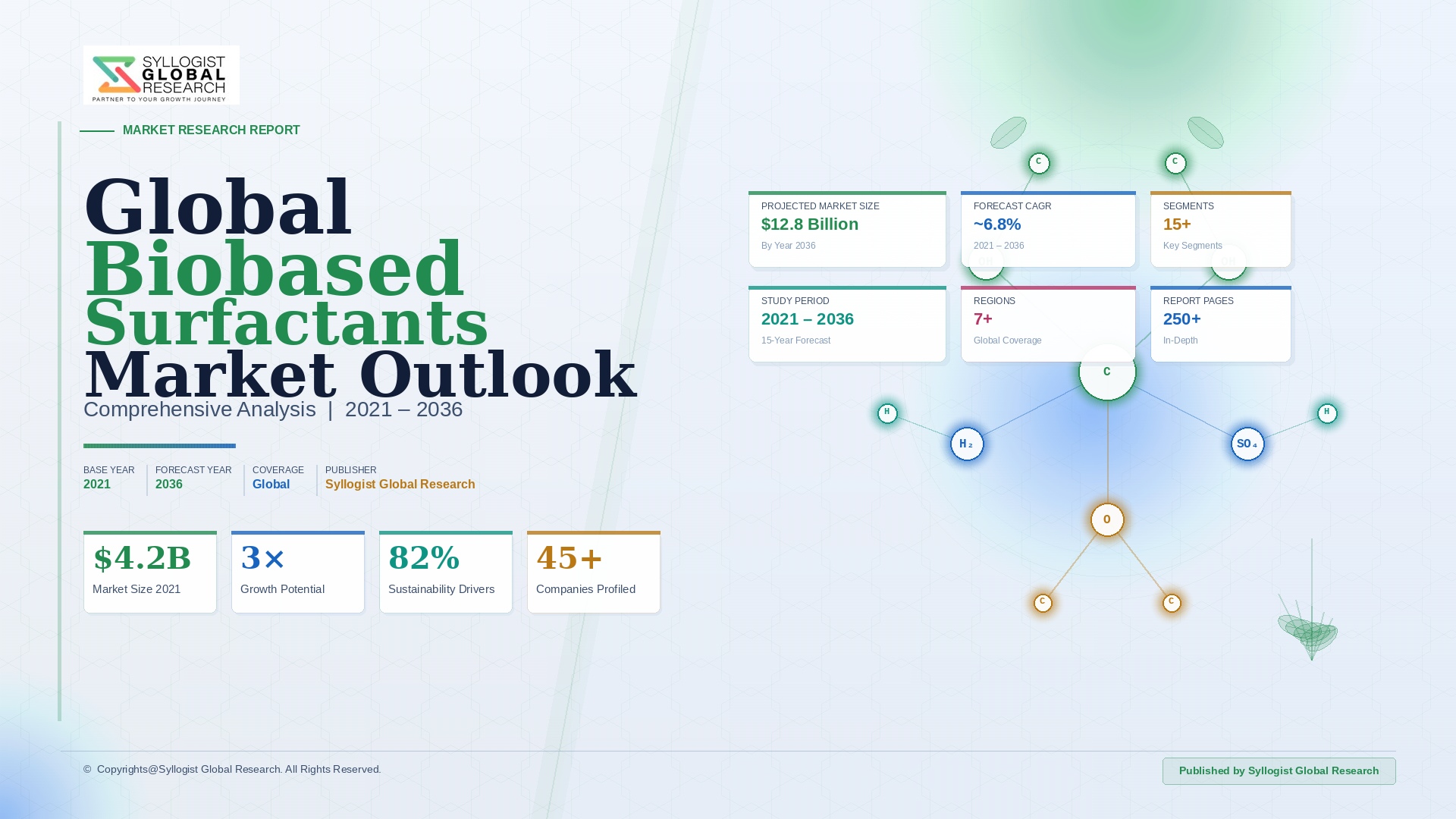

The global bio-based surfactants market was valued at approximately USD 6.8 billion in 2025 and is projected to reach USD 14.3 billion by 2034, advancing at a compound annual growth rate of 8.6% over the forecast period from 2027 to 2034, reflecting a broad-based and accelerating transition in surfactant procurement and formulation practices driven by tightening environmental regulations on conventional synthetic surfactants, rising consumer demand for naturally derived and biodegradable personal care and cleaning products, and the expanding commitment of global consumer goods manufacturers to science-based sustainability targets that prescribe minimum bio-based raw material content thresholds across their formulation portfolios. The market’s growth is structurally underpinned by the improving cost competitiveness of bio-based surfactant production relative to petrochemical alternatives, as advances in oleochemical processing efficiency, fermentation bioprocess engineering, and renewable feedstock supply chain development progressively narrow the historically wide production cost differential that constrained bio-based surfactant market penetration beyond premium application segments. Within the global surfactant market, bio-based grades accounted for approximately 19.4% of total surfactant consumption by volume in 2025, up from approximately 12.7% in 2020, indicating a meaningful and accelerating structural shift in the global surfactant production and consumption mix that is expected to continue throughout the forecast period as regulatory, commercial, and consumer-driven substitution pressures compound across all major geographic markets and end-use application categories.

The personal care and cosmetics segment constitutes the largest and most commercially mature application category within the global bio-based surfactants market, accounting for approximately 36% of total market revenue in 2025, driven by the worldwide proliferation of natural and organic beauty product lines, consumer-led clean beauty movements demanding sulfate-free and biodegradable formulation ingredients, and the reformulation activity of major global consumer goods companies replacing conventional sodium lauryl sulfate and sodium laureth sulfate with mild, skin-compatible bio-based alternatives including alkyl polyglucosides, sodium lauroyl glutamate, sodium cocoyl isethionate, and sucrose laurate across premium and mass-market personal care formulations. The household and institutional cleaning segment represents the second-largest application category, capturing approximately 28% of market revenue in 2025, with bio-based surfactant adoption in laundry detergents, automatic dishwashing formulations, and multi-surface cleaners gaining sustained commercial traction as green cleaning certification schemes including the EU Ecolabel, Nordic Swan, and UL Environment ECOLOGO progressively incorporate bio-based surfactant content requirements within their product standard criteria, compelling branded cleaning product manufacturers to advance bio-based surfactant integration across their core product portfolios. The industrial and institutional applications segment, encompassing oilfield chemistry, textile processing, agricultural adjuvants, and food-grade applications, represents a rapidly growing category where bio-based surfactants are displacing conventional synthetic alternatives driven by regulatory restrictions on persistent and bioaccumulative surfactant chemistries in industrial effluent discharge standards across North America, the European Union, and increasingly across Asia-Pacific markets.

Asia-Pacific constitutes the largest regional market for bio-based surfactants by both production output and consumption volume, accounting for approximately 41% of global market revenue in 2025, anchored by the region’s dominant oleochemical manufacturing base concentrated in Malaysia, Indonesia, the Philippines, and India that collectively supply the majority of the world’s palm kernel oil and coconut oil-derived feedstocks used in bio-based surfactant synthesis globally. China represents the fastest-growing major national market within Asia-Pacific, with domestic bio-based surfactant consumption growing at approximately 11.2% annually driven by the rapid expansion of China’s premium personal care and cosmetics market, the progressive tightening of China’s industrial effluent standards for anionic surfactant discharge, and the Chinese government’s 14th Five-Year Plan commitments to green chemistry manufacturing development and renewable raw material substitution across the specialty chemicals sector. Europe represents the second-largest regional market by revenue, characterized by the most mature and comprehensive regulatory framework governing surfactant biodegradability, aquatic toxicity, and environmental fate, with the European Union’s Detergents Regulation, REACH substance of very high concern designations for certain conventional surfactant chemistries, and the Green Deal’s chemicals strategy for sustainability collectively creating a robust and expanding regulatory pull for bio-based surfactant adoption across both consumer and industrial application segments that is expected to sustain above-average European market growth through 2034. North America, led by the United States, represents the third-largest regional market, characterized by strong demand in the premium personal care, institutional cleaning, and agricultural adjuvant segments.

The fermentation-derived biosurfactant segment, encompassing sophorolipids, rhamnolipids, mannosylerythritol lipids, and lipopeptide biosurfactants, represents the most technologically dynamic and highest-growth sub-segment within the global bio-based surfactants market, growing at approximately 14.3% annually in 2025 as advances in microbial strain engineering, fed-batch and continuous fermentation process optimization, and downstream recovery technology progressively reduce the production cost of biosurfactants toward price points that enable commercial competitiveness across broader application categories beyond current premium cosmetic and pharmaceutical niches. Sophorolipids, produced primarily through fermentation of Starmerella bombicola yeast on vegetable oil and glucose substrates, have achieved the most advanced commercial scale among glycolipid biosurfactants, with production volumes reaching approximately 3,800 metric tons globally in 2025 at production costs approaching USD 3.2 per kilogram at large-scale facilities, positioning sophorolipids as economically viable bio-based active ingredients for premium personal care, anti-microbial surface treatment, and specialty industrial cleaning formulations. The competitive landscape of the global bio-based surfactants market is characterized by a combination of large diversified oleochemical and specialty chemical companies including BASF, Evonik Industries, Nouryon, Croda International, and Kao Corporation that leverage integrated feedstock supply chains and global customer relationships to lead in volume-driven alkyl polyglucoside, methyl ester sulfonate, and fatty acid derivative segments, alongside emerging fermentation biosurfactant specialists and bio-based surfactant-focused companies that are advancing next-generation microbial biosurfactant production technologies with the objective of addressing larger-volume application markets as production cost reductions are achieved through continued bioprocess and strain engineering innovation.

Key Drivers

Accelerating Global Regulatory Restrictions on Petrochemical Surfactants and Expanding Biodegradability Mandates Compelling Bio-Based Surfactant Adoption Across Consumer and Industrial Markets

Regulatory frameworks governing surfactant biodegradability, aquatic toxicity, and environmental persistence across major global markets are progressively tightening in ways that structurally disadvantage conventional petrochemical surfactant chemistries and create compelling substitution incentives for bio-based alternatives with demonstrably superior environmental fate and biodegradability profiles. The European Union’s updated Detergents Regulation, advancing REACH restrictions on certain branched and poorly biodegradable alkylphenol ethoxylate surfactant chemistries, and the Chemicals Strategy for Sustainability’s commitment to progressively restricting substances of concern in consumer and professional cleaning products collectively represent a regulatory architecture whose implementation trajectory will eliminate significant categories of conventional synthetic surfactants from the European market over the forecast period, directly expanding the addressable commercial opportunity for compliant bio-based alternatives across laundry, dishwashing, personal care, and institutional cleaning formulation segments. The United States Environmental Protection Agency’s Safer Choice program, which requires bio-based and readily biodegradable surfactant ingredients as a condition of product certification, has certified over 2,800 consumer and institutional cleaning products to date, creating a substantial pull-through demand stream for approved bio-based surfactant grades across the North American market. China’s accelerating enforcement of GB standard biodegradability thresholds for detergent surfactants and the progressive incorporation of bio-based content requirements within China’s green product certification system are similarly expanding the regulatory case for bio-based surfactant substitution within the world’s largest single national surfactant consumption market.

Global Consumer Clean Beauty and Sustainable Cleaning Movements Generating Durable and Expanding Demand for Naturally Derived Bio-Based Surfactant Formulations

The structural convergence of the clean beauty movement in personal care, the green cleaning trend in household and institutional products, and the broader consumer sustainability consciousness across North American, European, and increasingly Asian consumer markets is generating a durable and commercially significant demand pull for bio-based surfactants as the preferred active ingredient system in naturally positioned, biodegradable, and environmentally responsible formulations that command measurable consumer price premiums and loyalty advantages over conventional synthetic formulations. The global natural and organic personal care market was valued at approximately USD 38.4 billion in 2025 and is growing at approximately 9.7% annually, with bio-based surfactants serving as the foundational cleansing and emulsifying ingredient architecture across sulfate-free shampoos, mild facial cleansers, biodegradable body washes, and natural liquid hand soaps that collectively constitute the fastest-growing segment within global personal care retail. Consumer ingredient awareness, amplified through social media platforms, clean beauty advocacy communities, and dermatologist-led digital content, is increasingly driving purchase decision-making based on surfactant chemistry transparency, natural origin certification, and skin compatibility data, compelling personal care brands at every price tier to reformulate existing products and develop new bio-based surfactant-formulated product lines to remain commercially competitive within the rapidly evolving global personal care marketplace. This consumer-driven demand momentum is reinforced by the procurement specifications of major global retailers who are progressively incorporating bio-based ingredient thresholds and biodegradability performance requirements within their private label and branded product sustainability sourcing standards.

Integrated Renewable Feedstock Availability, Oleochemical Manufacturing Expansion, and Fermentation Bioprocess Innovation Improving Bio-Based Surfactant Production Economics

The long-term structural improvement in bio-based surfactant production economics, driven by the combined effects of renewable feedstock supply chain expansion and cost reduction, oleochemical processing technology advancement, and fermentation bioprocess engineering innovation, is progressively closing the production cost gap between bio-based and petrochemical surfactant grades and expanding the range of application segments in which bio-based surfactants can compete on total formulation cost rather than solely on sustainability and regulatory compliance credentials. Global palm kernel oil and coconut oil production capacity, the primary renewable feedstocks for fatty alcohol and alkyl polyglucoside surfactant synthesis, has expanded substantially over the past decade with production volumes reaching approximately 8.4 million metric tons and 3.2 million metric tons respectively in 2025, providing a scale and geographic diversification of renewable feedstock supply that is supporting more competitive and stable bio-based surfactant raw material procurement economics for large-volume manufacturers. In the fermentation biosurfactant segment, advances in CRISPR-based microbial strain engineering, high-cell-density fed-batch fermentation process development, and integrated biorefinery approaches that co-produce multiple bio-based chemical products from shared fermentation infrastructure are collectively reducing the cost of biosurfactant production at commercial scale, with sophorolipid production costs declining from approximately USD 6.8 per kilogram in 2018 to approximately USD 3.2 per kilogram in 2025 at leading production facilities, a trajectory that is expected to continue reducing biosurfactant production costs toward mainstream commercial viability across additional application segments through the forecast period.

Key Challenges

Persistent Production Cost Premium of Bio-Based Surfactants Relative to Petrochemical Alternatives Constraining Volume Penetration in Price-Sensitive Commodity Segments

Despite meaningful progress in production cost reduction over the past decade, bio-based surfactants continue to carry a production cost premium relative to petrochemical-derived equivalents across the majority of surfactant chemistry categories and commercial application grades, with bio-based surfactant prices typically commanding a 20% to 65% premium over petrochemical equivalents depending on chemistry type, production route, bio-based content specification, and prevailing crude oil and vegetable oil price differentials, a cost disadvantage that structurally limits bio-based surfactant market penetration in the large-volume, price-competitive commodity segments of the global laundry detergent, textile processing, and industrial cleaning markets where total formulation cost optimization remains the dominant procurement criterion for the majority of industrial buyers and consumer goods formulators operating in highly competitive end markets. The production economics of fermentation-derived biosurfactants are particularly constrained by the capital intensity of sterile fermentation infrastructure, the energy cost of fermentation and downstream purification operations, and the inherently lower volumetric productivity of current microbial production strains relative to the continuous, high-throughput synthesis processes of world-scale petrochemical surfactant facilities, limiting the cost reduction achievable through scale-alone without accompanying advances in microbial strain performance, fermentation process intensification, and integrated downstream recovery efficiency. This cost barrier structurally restricts bio-based surfactant market penetration predominantly to premium-positioned consumer applications and compliance-driven industrial uses, leaving the substantially larger commodity surfactant volume segments of the global market insufficiently penetrated by bio-based alternatives and constraining the overall market growth trajectory relative to its underlying sustainability demand potential.

Feedstock Supply Chain Vulnerabilities, Agricultural Price Volatility, and Sustainability Controversies Around Primary Oleochemical Raw Materials Creating Input Cost and Reputational Risk

Bio-based surfactant manufacturers face material input cost volatility and supply security risk arising from the agricultural character of their primary renewable raw material supply chains, with palm kernel oil and coconut oil prices, the dominant feedstocks for large-volume bio-based surfactant production, subject to significant interannual price fluctuations driven by El Nino and La Nina precipitation pattern variability affecting Southeast Asian oil palm and Philippine coconut production yields, export policy interventions by major producing countries, and commodity market dynamics that can create rapid and substantial feedstock cost escalations that erode bio-based surfactant production margins and temporarily widen the cost competitiveness gap relative to crude oil-derived petrochemical alternatives. Beyond price volatility, palm oil-derived feedstocks face persistent sustainability credibility challenges arising from the association of palm oil cultivation with tropical deforestation, peatland destruction, and biodiversity loss in Southeast Asia, creating reputational risk for bio-based surfactant manufacturers and their formulator customers who source palm-derived oleochemical feedstocks without independently verified certification from schemes such as the Roundtable on Sustainable Palm Oil, and potentially undermining the sustainability marketing proposition of bio-based surfactant-formulated products whose green credentials depend on the genuine environmental integrity of their entire renewable feedstock supply chain from plantation to finished ingredient. The development of alternative non-palm renewable feedstock pathways including agricultural waste-derived fatty acids, microbial oil fermentation, and algae-based lipid production represents a strategic longer-term response to these supply chain vulnerabilities, but these alternative feedstock technologies remain at early commercial development stages and are not yet available at the scale or cost required to displace palm and coconut oleochemical feedstocks within mainstream bio-based surfactant production.

Complexity of Achieving Regulatory Approval, Biodegradability Certification, and Performance Validation Across Diverse Global Market Requirements Constraining Speed of Bio-Based Innovation Commercialization

The commercialization of novel bio-based surfactant chemistries and next-generation fermentation biosurfactant products faces a complex and costly multi-jurisdictional regulatory approval and certification pathway that substantially extends development timelines and increases the investment required to bring new bio-based surfactant ingredients to commercial market readiness across the global customer base, as regulatory frameworks for surfactant safety assessment, biodegradability test methodology, bio-based content certification, and environmental fate characterization vary materially across the European Union, United States, China, Japan, and emerging market regulatory jurisdictions in ways that preclude reliance on a single globally recognized approval pathway and require parallel regulatory submission and validation processes. The European Union’s REACH regulation requires comprehensive chemical safety documentation including biodegradation kinetic data, aquatic toxicity dose-response characterization across multiple trophic levels, and human health hazard assessment for new surfactant substances that can cost between USD 400,000 and USD 1.2 million per new substance registration at full Annex X data requirements, creating a financial barrier that disproportionately burdens smaller fermentation biosurfactant innovators and new market entrants relative to established large-scale surfactant manufacturers with existing registered substance portfolios. Performance validation requirements present an additional commercialization barrier, as bio-based surfactants must demonstrate cleaning performance, foaming characteristics, stability, and compatibility with co-formulants that meet or exceed the well-characterized performance benchmarks of established petrochemical surfactant systems across diverse application conditions, requiring extensive application testing, customer formulation development support, and demonstrated in-market performance data to overcome formulator conservatism and procurement inertia in established industrial and consumer goods supply chains.

Market Segmentation

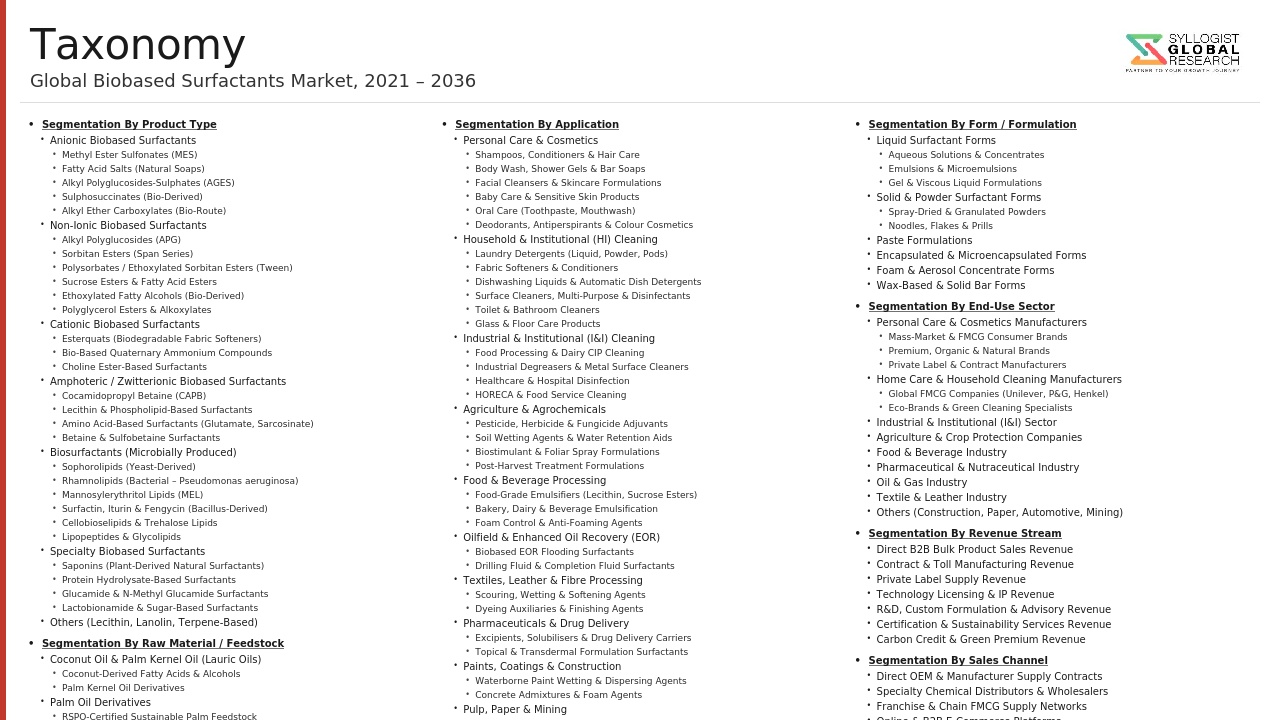

- Segmentation By Product Type

- Alkyl Polyglucosides (APG)

- Methyl Ester Sulfonates (MES)

- Sucrose Esters and Sucrose Fatty Acid Esters

- Amino Acid-Based Surfactants (Sodium Lauroyl Glutamate, Sodium Cocoyl Glycinate, and Others)

- Sorbitan Esters and Ethoxylated Sorbitan Esters (Polysorbates)

- Sophorolipids

- Rhamnolipids

- Mannosylerythritol Lipids (MEL)

- Lipopeptides (Surfactin, Iturin, and Others)

- Fatty Alcohol Ethoxylates (Bio-Based)

- Others

- Segmentation By Feedstock

- Palm Kernel Oil-Derived

- Coconut Oil-Derived

- Castor Oil-Derived

- Soybean Oil-Derived

- Rapeseed and Sunflower Oil-Derived

- Sugarcane and Glucose-Derived

- Agricultural Waste and By-Product-Derived

- Others

- Segmentation By Production Process

- Microbial Fermentation (Biosurfactants)

- Enzymatic Synthesis

- Chemical Synthesis from Bio-Based Feedstocks

- Oleochemical Processing and Derivatization

- Others

- Segmentation By Application

- Personal Care and Cosmetics

- Household and Institutional Cleaning

- Agricultural Formulations (Adjuvants, Emulsifiers, and Wetting Agents)

- Textile Processing and Finishing

- Food Processing and Food-Grade Applications

- Oilfield and Enhanced Oil Recovery

- Pharmaceutical and Healthcare

- Industrial Cleaning and Degreasing

- Pulp and Paper Processing

- Others

- Segmentation By End-Use Industry

- Personal Care and Beauty Industry

- Fast-Moving Consumer Goods (FMCG) Companies

- Agricultural Input and Crop Protection Companies

- Textile Mills and Processing Facilities

- Food and Beverage Manufacturers

- Oil and Gas Sector

- Healthcare and Pharmaceutical Companies

- Industrial and Institutional Cleaning Service Providers

- Pulp and Paper Manufacturers

- Others

- Segmentation By Distribution Channel

- Direct Sales (Business-to-Business)

- Specialty Chemical Distributors and Wholesalers

- Online Platforms and E-Commerce

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Bio-Based Surfactants Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by product type including alkyl polyglucosides, methyl ester sulfonates, amino acid-based surfactants, sophorolipids, rhamnolipids, and other biosurfactant chemistries, and by application including personal care, household cleaning, agriculture, textile processing, food processing, oilfield chemistry, and industrial cleaning, to enable bio-based surfactant manufacturers, oleochemical producers, fermentation biotechnology companies, consumer goods formulators, and investors to identify which product chemistries and application categories will deliver the highest absolute revenue growth and the most commercially durable demand trajectory across the forecast period?

- How are tightening global regulatory frameworks governing surfactant biodegradability, aquatic toxicity, and environmental persistence, including the European Union Detergents Regulation update, REACH substance of very high concern designations, the United States Environmental Protection Agency Safer Choice program certification requirements, and China’s green product certification biodegradability standards, expected to drive mandatory and voluntary substitution of conventional petrochemical surfactants by bio-based alternatives across consumer, institutional, and industrial application segments on a region-by-region and chemistry-by-chemistry basis through 2034, and what are the aggregate addressable market volumes and revenue opportunities arising from compliance-driven bio-based surfactant substitution in each major regulated market?

- What is the current production capacity, feedstock sourcing strategy, product portfolio breadth and specialization, key customer relationships, geographic market presence, and financial performance of the leading global bio-based surfactant producers including large diversified specialty chemical companies, oleochemical-integrated manufacturers, and emerging fermentation biosurfactant specialists, and how are these market participants differentiating their competitive positioning through bio-based content certification, biodegradability performance documentation, application technical support services, sustainable sourcing commitments, and new product innovation programs targeting the highest-growth personal care, green cleaning, and agricultural application segments?

- How is the production cost trajectory of bio-based surfactants, encompassing oleochemical-derived surfactant chemistries including alkyl polyglucosides and methyl ester sulfonates and fermentation-derived biosurfactants including sophorolipids and rhamnolipids, expected to evolve through 2034 as renewable feedstock supply chains mature, fermentation bioprocess engineering advances, microbial strain productivity improves through synthetic biology applications, and manufacturing scale increases, and at what production cost thresholds do specific bio-based surfactant chemistries achieve the price competitiveness required to penetrate the large-volume commodity application segments of the global laundry detergent, textile processing, and industrial cleaning markets that currently remain substantially underpenetrated by bio-based alternatives?

- What are the regional demand growth differentials within the global bio-based surfactants market across North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa, considering the distinct regulatory environments, consumer awareness and willingness-to-pay for bio-based products, oleochemical feedstock availability, manufacturing infrastructure maturity, and end-use industry composition of each region, and which regional markets are expected to generate the highest absolute revenue increments and the most compelling investment opportunities for bio-based surfactant capacity expansion, distribution network development, and application innovation over the forecast period to 2034?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Raw Material & Supply Chain Risk

- Regulatory & Compliance Risk

- Market & Demand Risk

- Technology & Product Risk

- Environmental & Circular Economy Risk

- Regulatory Framework & Standards

- Biodegradability & Environmental Regulations

- Chemical Safety & REACH Regulations

- Natural, Organic & Bio-Based Content Standards

- Agricultural & Pesticide Regulations for Biosurfactants

- Food, Pharmaceutical & Personal Care Grade Standards

- Global Bio-Based Surfactants Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Kilotonnes)

- Market Size & Forecast by Product Type

- Sugar-Based Surfactants

- Alkyl Polyglucosides (APG): C8-C10, C12-C14, C8-C16 Grades

- Sucrose Esters & Sucrose Fatty Acid Esters

- Methyl Glucoside Esters (MGE)

- Sorbitan Esters (Span Series)

- Polysorbates (Tween Series: Bio-Based Grade)

- Fatty Acid-Based Surfactants

- Sodium, Potassium & Ammonium Lauryl / Myristyl / Cocoyl Sulphate

- Sodium Lauroyl / Cocoyl Methyl Isethionate (SLMI / SLCI)

- Cocamidopropyl Betaine (CAPB: Bio-Based Grade)

- Sodium Cocoamphoacetate & Disodium Cocoamphodiacetate

- Amine Oxides (Lauramine Oxide: Bio-Based Grade)

- Amino Acid-Based Surfactants

- Sodium Lauroyl Glutamate & Sodium Cocoyl Glutamate

- Potassium Cocoyl Glycinate & Sodium Lauroyl Glycinate

- Sodium Cocoyl Alaninate & N-Acyl Sarcosinates

- Sodium Lauroyl Collagen Amino Acids & Silk Amino Acid Surfactants

- Acyl Taurate Surfactants (Sodium Lauroyl Methyl Taurate)

- Glycolipid Biosurfactants (Microbial / Fermentation-Derived)

- Sophorolipids (Acidic & Lactonic Forms: Candida bombicola Derived)

- Rhamnolipids (Mono-Rhamnolipid & Di-Rhamnolipid: Pseudomonas Derived)

- Mannosylerythritol Lipids (MEL): Moesziomyces Derived

- Cellobiose Lipids & Trehalose Lipids: Emerging Glycolipid Classes

- Lipopeptide Biosurfactants

- Surfactin: Bacillus subtilis Derived Cyclic Lipopeptide

- Iturin, Fengycin & Iturinic Acid Biosurfactant Complexes

- Lichenysin & Subtilisin Lipopeptides for Biocontrol Applications

- Lecithin & Phospholipid Surfactants

- Soy Lecithin: Standard & Modified (Lyso-, Hydrolysed, Enzymatic)

- Sunflower Lecithin (Non-GMO Premium Grade)

- Rapeseed Lecithin & Synthetic Phosphatidylcholine Analogues

- Saponin-Based Surfactants

- Quillaja (Soapbark) Saponin Extract: Food, Cosmetic & Agricultural Grade

- Yucca schidigera Saponin Extract

- Soapwort & Horse Chestnut (Aescin) Saponin Extracts

- Protein-Based & Polymeric Biosurfactants

- Hydrolysed Wheat Protein Surfactants for Hair & Skin Care

- Oat Beta-Glucan & Oat Protein Amphiphilic Extracts

- Casein & Whey Protein Emulsifiers for Food & Pharmaceutical Applications

- Market Size & Forecast by Raw Material / Feedstock

- Palm Kernel Oil (PKO) & Coconut Oil-Derived Surfactants (Lauric Acid Feedstock)

- Corn & Glucose (Dextrose) Derived Surfactants (APG, Sophorolipid Fermentation)

- Sugarcane-Derived Surfactants (Sucrose, Fructose & Ethanol Feedstock)

- Rapeseed & Sunflower Oil-Derived Surfactants (Erucic Acid, Oleic Acid Feedstock)

- Soybean Oil-Derived Surfactants (Lecithin, Linoleic Acid Feedstock)

- Castor Oil-Derived Surfactants (Ricinoleic Acid Feedstock: Ethoxylated Castor Oil)

- Waste & Second-Generation Feedstocks (Waste Cooking Oil, Whey, Molasses, Lignocellulosic Sugars)

- Algae-Derived Surfactant Feedstock (Microalgae Lipid, Carrageenan Derivatives)

- Market Size & Forecast by Application

- Home Care & Laundry

- Liquid Laundry Detergent: Bio-Based Surfactant Formulations

- Powder & Unit Dose (Pod) Laundry Detergent

- Fabric Softener & Conditioner

- Automatic Dishwash Detergent (ADD) & Hand Dishwash Liquid

- Hard Surface Cleaner, Bathroom & Toilet Cleaner

- Personal Care & Cosmetics

- Shampoo & Hair Conditioner (Baby, Sensitive, Premium Grade)

- Body Wash, Shower Gel & Bath Foam

- Facial Cleanser, Micellar Water & Cleansing Oil

- Skin Moisturiser, Sunscreen & Colour Cosmetics Emulsifiers

- Toothpaste & Oral Care Surfactants

- Industrial & Institutional (I&I) Cleaning

- Food Processing & CIP (Clean-in-Place) Cleaning Agents

- Institutional Laundry & Warewashing

- Healthcare Facility Cleaning & Surface Disinfection

- Industrial Degreasers & Workshop Cleaning Formulations

- Agriculture & Crop Protection

- Biosurfactant Pesticide Adjuvants & Spreader-Stickers

- Biostimulant Wetting Agent for Soil & Foliar Applications

- Biosurfactant-Based Biopesticide & Biofungicide Active Ingredients

- Oilfield & Mining

- Enhanced Oil Recovery (EOR) Bio-Based Surfactant Flooding

- Drilling Fluid & Stimulation Fluid Bio-Based Additives

- Froth Flotation Bio-Based Collector & Frother in Mineral Processing

- Food & Beverage Processing

- Food Emulsifiers (Lecithin, Sucrose Esters, Saponins) for Bakery, Dairy & Confectionery

- Beverage Clouding Agents & Foam Stabilisers

- Food Grade Wetting & Dispersing Agents for Powder Processing

- Pharmaceuticals & Healthcare

- Drug Solubilisation & Bioavailability Enhancement

- Vaccine Adjuvant (Saponin QS-21, Quillaja Extract)

- Topical Drug & Wound Care Formulation Emulsifiers

- Textile, Leather & Paper Processing

- Textile Scouring, Wetting & Softening Agents

- Leather Degreasing & Fatliquoring Agents

- Paper Sizing, Coating & Deinking Agents

- Market Size & Forecast by Function

- Emulsifiers & Solubilisers

- Detergents & Cleansers

- Foaming & Lathering Agents

- Wetting & Spreading Agents

- Dispersants & Suspending Agents

- Conditioning & Softening Agents

- Antimicrobial & Biocidal Agents

- Corrosion Inhibitors & Lubricity Agents

- Market Size & Forecast by Charge Type

- Anionic Bio-Based Surfactants

- Cationic Bio-Based Surfactants

- Non-Ionic Bio-Based Surfactants

- Amphoteric / Zwitterionic Bio-Based Surfactants

- Market Size & Forecast by Source

- Plant-Derived (Oleochemical-Based) Surfactants

- Microbially Fermented (Biosurfactant) Surfactants

- Enzymatically Synthesised Bio-Based Surfactants

- Animal-Derived Surfactants (Lecithin, Casein, Collagen Derivatives)

- Market Size & Forecast by Sales Channel

- Direct Sales (B2B: Bulk Formulator & Industrial Supply)

- Distributor & Specialty Chemical Trader Network

- Online & E-Commerce Platform (Specialty Chemical B2B Portals)

- Toll Manufacturing & Contract Processing Supply

- North America Bio-Based Surfactants Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotonnes)

- By Product Type

- By Raw Material / Feedstock

- By Application

- By Function

- By Charge Type

- By Source

- By Sales Channel

- Market Size & Forecast

- Europe Bio-Based Surfactants Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotonnes)

- By Product Type

- By Raw Material / Feedstock

- By Application

- By Function

- By Charge Type

- By Source

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Bio-Based Surfactants Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotonnes)

- By Product Type

- By Raw Material / Feedstock

- By Application

- By Function

- By Charge Type

- By Source

- By Sales Channel

- Market Size & Forecast

- Latin America Bio-Based Surfactants Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotonnes)

- By Product Type

- By Raw Material / Feedstock

- By Application

- By Function

- By Charge Type

- By Source

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Bio-Based Surfactants Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotonnes)

- By Product Type

- By Raw Material / Feedstock

- By Application

- By Function

- By Charge Type

- By Source

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Bio-Based Surfactants Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotonnes)

- By Product Type

- By Raw Material / Feedstock

- By Application

- By Function

- By Charge Type

- By Source

- By Sales Channel

- Market Size & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Italy, Spain, Netherlands, Sweden, Poland, China, Japan, South Korea, India, Indonesia, Thailand, Australia, Brazil, Argentina, Saudi Arabia, UAE, South Africa

- Technology Landscape & Innovation Analysis

- Oleochemical Bio-Based Surfactant Technology Deep-Dive

- Fermentation & Biosurfactant Technology Deep-Dive

- Enzymatic Synthesis Technology for Bio-Based Surfactants

- Formulation Technology & Application Science

- Analytical & Quality Technology for Bio-Based Surfactants

- Patent & IP Landscape in Bio-Based Surfactants

- Value Chain & Supply Chain Analysis

- Raw Material Supply Chain

- Bio-Based Surfactant Manufacturing Equipment Supply Chain

- Tier-1 Bio-Based Surfactant Manufacturer

- Formulator & Brand Owner Integration

- Distribution & Logistics

- End-of-Life & Circular Economy

- Pricing Analysis

- APG & Sugar-Based Surfactant Pricing Analysis

- Amino Acid-Based Surfactant Pricing Analysis

- Biosurfactant Pricing Analysis

- Lecithin & Natural Emulsifier Pricing Analysis

- Total System Pricing & Formulation Cost Analysis

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Bio-Based Surfactants

- Biodegradability & Aquatic Safety Profile

- Renewable Carbon & Climate Contribution

- Social & Ethical Sustainability

- Regulatory-Driven Sustainability Compliance

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Product Type & Application)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Product Type, Application & Geography

- Player Classification

- Global Integrated Oleochemical & Specialty Surfactant Conglomerates

- Specialist Bio-Based & Natural Surfactant Producers

- Biosurfactant Fermentation Technology Companies (Startups & Scale-Ups)

- Amino Acid Surfactant Specialists (Japan & Korea-Based)

- Regional Bio-Based Surfactant Producers (India, China, Europe)

- FMCG Brand Owner Internal Bio-Based Surfactant Development Programmes

- Competitive Analysis Frameworks

- Market Share Analysis by Product Type, Application & Region

- Company Profile

- Company Overview & Headquarters

- Bio-Based Surfactant Products & Technology Portfolio

- Key Customer Relationships & Application Focus

- Manufacturing Footprint & Production Capacity

- Revenue (Bio-Based Surfactant Segment) & Growth Trajectory

- Technology Differentiators & IP Portfolio

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Capacity Expansion, Product Launches, Certifications)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Leadership vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Strategic Opportunity Analysis

- Strategic Output

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Market Penetration Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-Term (2025–2028)

- Mid-Term (2029–2032)

- Long-Term (2033–2037)