Market Definition

The Asia-Pacific Bisphenol A Market encompasses the production, trade, processing, and end-use consumption of bisphenol A monomer and its derivative products across the full petrochemical and polymer value chain operating within the Asia-Pacific region, including BPA synthesis from phenol and acetone at integrated petrochemical production facilities, the downstream conversion of BPA into polycarbonate resin and epoxy resin that together account for over 95% of global BPA consumption, and the further processing of polycarbonate and epoxy resin into engineering plastic components, protective coatings, electrical laminates, adhesives, composite matrices, and specialty chemical intermediates serving a diverse range of industrial, construction, electronics, automotive, packaging, and consumer goods end-use markets across China, Japan, South Korea, India, Taiwan, Southeast Asia, and Australia. Bisphenol A is an organic synthetic compound produced through the condensation reaction of phenol and acetone in the presence of an acid catalyst, yielding a white crystalline solid with the chemical formula C15H16O2 whose dual phenolic hydroxyl groups and central isopropylidene bridge impart the reactive difunctionality that makes BPA an indispensable monomer building block for the synthesis of polycarbonate and epoxy resin polymer systems with uniquely valuable combinations of optical clarity, mechanical toughness, thermal stability, chemical resistance, and electrical insulation properties.

The market encompasses BPA monomer production at world-scale petrochemical facilities operated by Sinopec, CNPC, Kumho P and B Chemical, Nan Ya Plastics, LG Chem, Mitsui Chemicals, Mitsubishi Chemical, and independent Asian BPA producers; polycarbonate resin manufacturing through interfacial or melt transesterification polymerization; epoxy resin synthesis via BPA reaction with epichlorohydrin to produce liquid and solid bisphenol A diglycidyl ether epoxy resins across a spectrum of molecular weight grades; and the application of BPA-derived polycarbonate and epoxy resins across electrical and electronic laminates, automotive lighting and glazing components, optical media, safety glazing, food contact packaging, construction composites, marine and aerospace coatings, adhesives, and thermal paper coating applications. Key participants include integrated petrochemical producers with BPA and derivative resin manufacturing capacity, specialty chemical formulators converting BPA-derived resins into downstream application products, regulatory bodies monitoring BPA safety and imposing use restrictions across specific application categories, and the diverse industrial end-user community whose manufacturing activity and product development programs define the consumption volume and value structure of the Asia-Pacific BPA market across its principal downstream derivative segments.

Market Insights

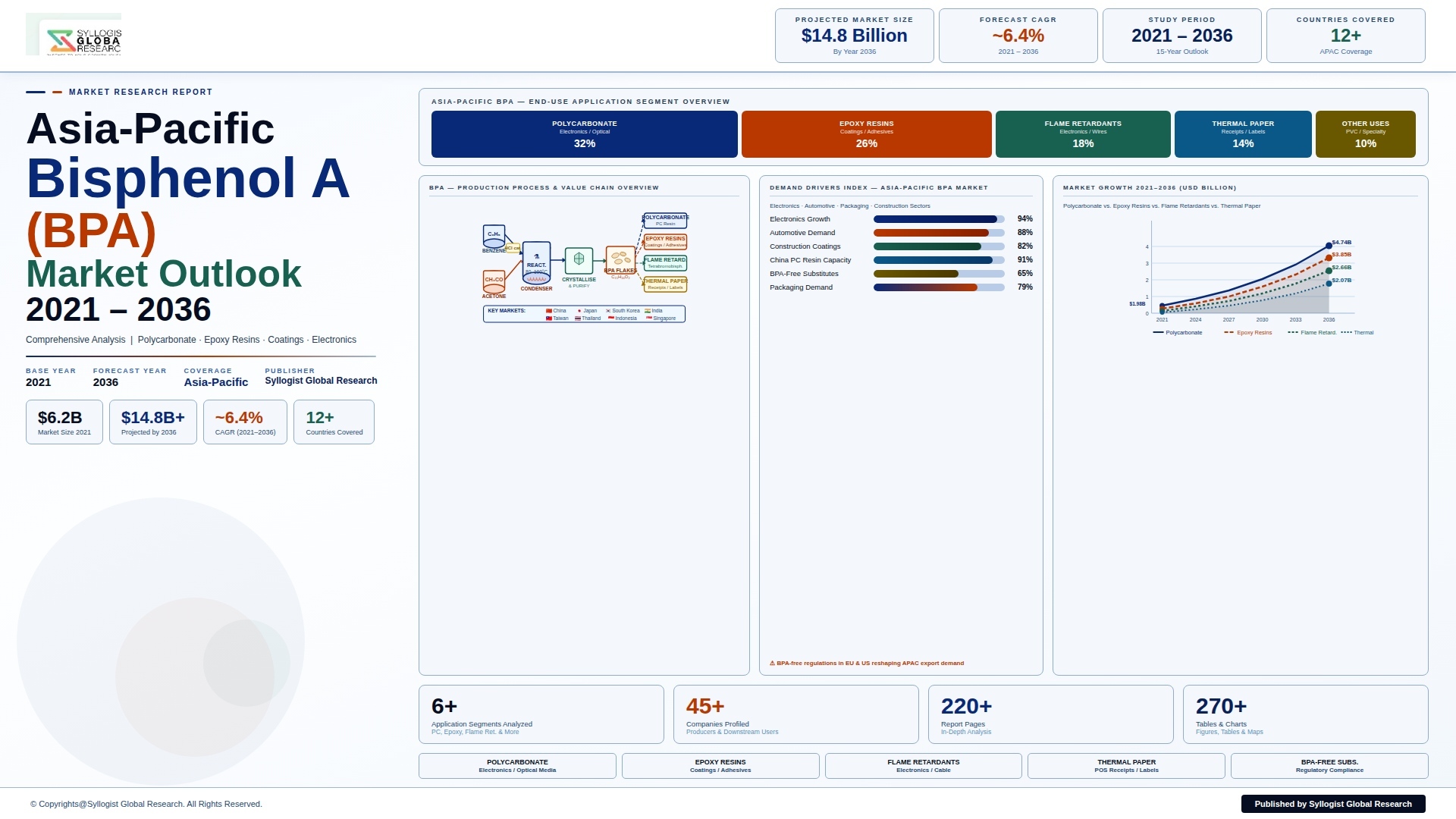

The Asia-Pacific bisphenol A market occupies a structurally dominant position in the global BPA value chain, accounting for approximately 73% of total global BPA production capacity and approximately 68% of total global BPA consumption in 2025, reflecting the concentration of the world’s polycarbonate and epoxy resin manufacturing base, the electronics and electrical component production ecosystem, and the automotive and construction industry growth momentum within the Asia-Pacific region whose demand fundamentals are structurally more favorable than the mature and regulatory-constrained BPA end-use markets of Europe and North America. The Asia-Pacific BPA market was valued at approximately USD 9.6 billion in 2025 and is projected to reach USD 14.3 billion by 2034, advancing at a compound annual growth rate of 4.5% over the forecast period from 2027 to 2034, driven by the continued expansion of polycarbonate demand across electronics, automotive, and construction applications in China and India, the growing epoxy resin consumption generated by wind energy composite manufacturing, printed circuit board production, and infrastructure protective coating applications across the region, and the sustained growth of BPA production capacity investment by Chinese and Korean petrochemical producers whose integrated feedstock and derivative manufacturing complexes are progressively displacing Japanese BPA producers from market share positions they previously held through technological leadership and established customer relationships.

Polycarbonate resin constitutes the largest single downstream application for BPA in the Asia-Pacific market, consuming approximately 57% of total regional BPA output in 2025, and is produced at world-scale manufacturing facilities operated by SABIC Innovative Plastics in its licensed Asian plants, Covestro at its Shanghai and Map Ta Phut facilities, LG Chem’s polycarbonate complex in South Korea, and Mitsubishi Chemical’s Japanese operations, whose combined production serves the electronics, automotive, optical media, construction glazing, and medical device markets across the region and generates global polycarbonate export volumes that influence world market pricing and supply dynamics. The electronics and electrical segment is the dominant polycarbonate consumption category in Asia-Pacific, driven by the concentration of the world’s consumer electronics manufacturing in China, South Korea, Taiwan, and Vietnam, where polycarbonate’s optical clarity, impact resistance, and flame retardancy performance in notebook computer housings, smartphone bodies, display components, and electrical enclosure applications generates large and relatively stable polycarbonate demand volumes that are closely correlated with regional consumer electronics production output rather than raw material price cycles. China’s polycarbonate demand reached approximately 2.8 million metric tonnes in 2025, making it the world’s largest single polycarbonate consuming market by a substantial margin, and China’s continued domestic polycarbonate capacity buildout under the Five-Year Plan for petrochemical industry development has materially reduced the country’s historical polycarbonate import dependency while simultaneously pressuring the export economics of Japanese and Korean polycarbonate producers who previously relied on Chinese offtake for a significant proportion of their production volumes. The optical polycarbonate segment, serving high-performance application in optical lenses, LED lighting diffusers, automotive headlamp lenses, and precision optical components, commands significant price premiums over commodity polycarbonate grades and represents a technically differentiated market segment where the proprietary polymerization process technologies and optical grade quality management systems of Covestro, Mitsubishi Chemical, and Teijin create durable competitive advantages that smaller Asian BPA and polycarbonate producers cannot easily replicate without equivalent technology investment and quality certification infrastructure.

The epoxy resin segment represents the second-largest BPA consumption category in Asia-Pacific, accounting for approximately 36% of total regional BPA consumption in 2025, and is experiencing diversified demand growth across traditional coating, adhesive, and electrical laminate applications alongside the rapidly expanding wind energy composite and high-performance structural composite manufacturing sectors whose BPA-based epoxy resin consumption is growing at rates substantially above the broader epoxy resin market average driven by the aggressive renewable energy capacity installation programs of China, India, Australia, Japan, and South Korea. China has installed over 440 gigawatts of cumulative wind power capacity as of the end of 2024 and is adding approximately 70 to 80 gigawatts of new wind capacity annually, with each megawatt of wind turbine capacity requiring approximately 10 to 14 tonnes of epoxy resin in blade manufacturing, nacelle component encapsulation, and tower base foundation grouting applications, translating China’s wind energy installation trajectory directly into growing epoxy resin and BPA demand at a scale whose impact on Asian BPA market balance is commercially significant. The printed circuit board and electrical laminate segment, where BPA-based tetrabromobisphenol A and standard BPA diglycidyl ether epoxy resins are the dominant matrix resins for FR-4 glass-reinforced epoxy laminate production serving the global electronics manufacturing industry concentrated in China, Taiwan, South Korea, and Vietnam, represents a structurally stable and technically demanding BPA consumption category whose demand growth is correlated with global PCB production volume expansion driven by automotive electrification, data center infrastructure investment, and 5G telecommunications equipment manufacturing. The marine and industrial protective coating segment, while a smaller absolute BPA consumption category than polycarbonate or electrical laminate applications, is experiencing above-average demand growth in Asia-Pacific driven by the expansion of shipbuilding output in South Korean, Chinese, and Japanese yards and the infrastructure maintenance coating requirements generated by the large and aging industrial asset base of China’s manufacturing economy.

The competitive and regulatory landscape of the Asia-Pacific BPA market is being shaped by two powerful and structurally opposing forces: the continued capacity expansion and market share gain of Chinese BPA and polycarbonate producers whose government-supported capital investment programs, integrated feedstock advantages, and lower manufacturing cost structures are progressively concentrating BPA production within China at the expense of Japanese and Korean incumbent producers, and the escalating regulatory scrutiny of BPA as an endocrine-disrupting substance under food contact material safety frameworks that is progressively restricting BPA’s application in consumer-facing packaging, infant feeding products, and food storage applications across Japan, South Korea, Australia, and increasingly through voluntary brand owner restriction programs that affect consumer product applications even in markets without formal regulatory prohibition. Japan’s Food Sanitation Act restrictions on BPA migration from food contact resins, South Korea’s Ministry of Food and Drug Safety limits on BPA in thermal paper and food packaging, Australia’s Therapeutic Goods Administration restrictions on BPA in medical devices, and China’s GB 9685 food contact material standard limiting BPA migration from polycarbonate and epoxy resin food contact applications are creating a fragmented national regulatory landscape that requires BPA-based product manufacturers serving consumer and food-adjacent markets to maintain jurisdiction-specific compliance programs and to develop BPA-free alternative formulations for regulated application categories. The growth of BPA-free polycarbonate alternatives based on non-BPA bisphenol monomers including bisphenol TMC, bisphenol AP, and bio-based isosorbide polycarbonate, while currently constrained to a small proportion of total polycarbonate market volume, is creating competitive pressure on BPA-derived polycarbonate in premium optical and medical device applications where brand owner preferences for regulatory risk mitigation are driving material substitution investment independent of formal regulatory mandates.

Key Drivers

Asia-Pacific Electronics Manufacturing Expansion and EV Automotive Growth Sustaining Structural Polycarbonate Demand Across BPA Value Chain

The continued dominance of Asia-Pacific as the world’s consumer electronics and semiconductor manufacturing hub, accounting for approximately 88% of global smartphone production, over 90% of notebook computer and tablet manufacturing, and the majority of global display panel, printed circuit board, and LED component production, generates a structurally resilient and gradually growing demand base for polycarbonate resin in electronics enclosures, optical components, and electrical insulation applications that directly sustains BPA consumption across the region’s integrated polycarbonate production capacity. The accelerating electrification of the automotive sector across China, South Korea, and Japan, where combined battery electric vehicle production exceeded 9.8 million units in 2024, is creating growing BPA-derived polycarbonate demand for EV-specific applications including high-voltage battery pack housings requiring the combination of impact resistance, flame retardancy, and dimensional stability that polycarbonate uniquely provides, automotive lighting systems with LED and laser light source designs demanding the optical polycarbonate precision quality that BPA-based resin enables, and the expanding use of polycarbonate glazing in EV roof panels, panoramic windshields, and camera and sensor cover applications where weight reduction relative to glass improves vehicle energy efficiency. The rapid expansion of data center construction across Singapore, Malaysia, India, Japan, Australia, and China to support cloud computing, artificial intelligence workload processing, and hyperscale platform deployment is generating growing demand for the epoxy resin-based printed circuit board laminates, polycarbonate cable management and server enclosure components, and BPA-based electrical insulation materials that constitute material content within data center electrical and electronic infrastructure, creating a durable BPA demand growth vector that is structurally linked to the digitalization investment acceleration of the Asia-Pacific economy.

Renewable Energy Infrastructure Buildout Driving Epoxy Resin Consumption Growth Across Wind Blade, Solar Panel Encapsulation, and Power Infrastructure Applications

The Asia-Pacific region’s aggressive renewable energy capacity installation programs, led by China’s commitment to achieving 1,200 gigawatts of combined wind and solar capacity by 2030, India’s 500 gigawatts of non-fossil fuel power capacity target, and Australia, Japan, South Korea, and Vietnam’s national renewable energy expansion programs, are generating a rapidly growing and commercially consequential demand stream for epoxy resin in wind turbine blade manufacturing, solar photovoltaic module encapsulation, high-voltage power transmission cable systems, and utility-scale energy storage system structural components that is driving above-average BPA consumption growth in the epoxy resin derivative value chain independent of the cyclical demand patterns of conventional industrial application segments. Wind turbine blade manufacturing, which consumes epoxy resin as the primary matrix material in glass-fiber and carbon-fiber reinforced composite blade structures, has become one of the largest single epoxy resin application categories in Asia-Pacific, with China’s domestic wind turbine manufacturing industry producing blades for both domestic installation and export markets that collectively consume several hundred thousand tonnes of epoxy resin annually and require the consistent supply of BPA-derived liquid epoxy resin grades meeting blade manufacturer quality specifications for viscosity, reactivity, and cured mechanical performance. The development of offshore wind energy in China, Taiwan, South Korea, Japan, and Vietnam, whose more demanding marine environment exposure requires enhanced epoxy resin formulations with superior corrosion resistance and UV stability relative to onshore wind blade applications, is creating a premium-specification BPA-based epoxy resin demand segment that commands higher product value and provides incremental commercial opportunity for technically advanced epoxy resin producers with the formulation expertise and quality assurance infrastructure to serve offshore wind blade manufacturing specifications.

India and Southeast Asia Industrial Expansion Creating New BPA Demand Growth Frontiers Beyond the Established China, Japan, and Korea Markets

The structural industrialization momentum of India and the ASEAN economies, encompassing the rapid expansion of electronics manufacturing in Vietnam, Indonesia, Thailand, and Malaysia, the acceleration of India’s manufacturing GDP growth under PLI scheme incentives attracting electronics, automotive, pharmaceutical, and consumer goods investment, and the infrastructure construction boom across Indonesia’s capital relocation program, Vietnam’s industrial zone development, and India’s National Infrastructure Pipeline, is creating a geographically expanding BPA demand base that supplements the mature market demand of Japan and Korea and the dominant but slowing growth trajectory of China with new high-growth consumption nodes whose polycarbonate and epoxy resin demand intensity is at earlier stages of per-capita industrial output development with substantial headroom for continued growth. India’s polycarbonate consumption reached approximately 420,000 metric tonnes in 2025 and is growing at approximately 8.2% annually, driven by the rapid expansion of the domestic automotive component, consumer electronics assembly, construction glazing, and electrical equipment manufacturing sectors whose polycarbonate material requirements are partially met through domestic production from SABIC’s Shriram compound facility and partially through imports from Korean, Japanese, and increasingly Chinese producers, creating a market structure whose growing import volumes are attracting domestic polycarbonate capacity investment proposals that would progressively localize India’s BPA derivative value chain. Vietnam’s emergence as a major global electronics manufacturing destination, hosting manufacturing operations for Samsung, LG, Intel, Apple supplier Foxconn, and dozens of electronic component producers, is generating growing local PCB laminate, polycarbonate component, and epoxy coating consumption that is establishing Vietnam as a meaningful regional BPA derivative demand market whose growth rate substantially exceeds the average for the established Asia-Pacific economies.

Key Challenges

Escalating Regulatory Restrictions on BPA in Consumer and Food Contact Applications Creating Demand Displacement Risk Across Specific End-Use Segments

The progressive tightening of BPA regulatory restrictions across Asia-Pacific national frameworks governing food contact materials, consumer product safety, thermal paper coating, and medical device applications is creating a structural demand displacement risk in consumer-facing BPA application segments that individually represent small proportions of total BPA consumption but whose combined regulatory pressure is generating sustained commercial uncertainty about the long-term addressable market for BPA in applications requiring food or human contact. Japan’s Ministry of Health, Labour and Welfare has maintained BPA migration limits for food contact polycarbonate and epoxy resin linings under the Food Sanitation Act since the early 2000s, with periodic reassessment of permissible migration levels generating compliance uncertainty for Japanese food packaging manufacturers whose customers include multinational food brands with global BPA reduction commitments. The voluntary elimination of BPA from thermal paper coating formulations, driven by retailer and food service operator customer requirements rather than formal regulatory mandate across most Asian markets, has effectively removed thermal paper as a commercially viable BPA application in customer-facing point-of-sale receipt and label applications, with BPA-free phenol-free and BPA-free developer alternatives from Nippon Soda, Sanko, and specialty chemical suppliers now dominating the thermal paper coating market. The cumulative effect of these application-specific restrictions, while not threatening the structural industrial BPA demand generated by electronics, automotive, wind energy, and construction applications, is creating reputational sensitivity around BPA in consumer product contexts that is influencing voluntary material substitution decisions by multinational brand owners whose global sustainability frameworks drive BPA elimination programs that affect Asian manufacturing operations regardless of local regulatory requirement status.

Chinese Polycarbonate Capacity Oversupply and Price Compression Threatening Profitability of Regional BPA and Derivative Producers

China’s aggressive domestic polycarbonate capacity expansion over the past decade, which has added over 2.2 million metric tonnes of new polycarbonate production capacity since 2018 from projects including Wanhua Chemical, Luxi Chemical, Covestro Caojing, and multiple state-owned enterprise polycarbonate investments, has generated a structural oversupply situation in the Asian polycarbonate market that has compressed polycarbonate prices, reduced polycarbonate producer operating margins, and created cascading pricing pressure throughout the BPA value chain as polycarbonate producers seek to reduce their BPA raw material costs to partially offset the margin compression from lower polycarbonate selling prices. The polycarbonate price in Asian spot markets declined from approximately USD 2,400 per metric tonne in early 2022 to approximately USD 1,450 to USD 1,600 per metric tonne in 2024, representing a price erosion of nearly 40% over two years that has simultaneously reduced the revenue realization of BPA producers supplying polycarbonate manufacturers and pressured the margins of polycarbonate producers across the value chain. The competitive displacement of Japanese and Korean polycarbonate and BPA producers by Chinese domestic production, whose lower manufacturing cost structures arising from integrated feedstock supply, lower labor costs, and government capital support create structural pricing advantages that established producers in Japan and Korea cannot match through efficiency improvement alone, is creating strategic existential pressure on regional producers including Mitsubishi Chemical, Teijin, and Kumho P and B Chemical to differentiate toward specialty and optical grade polycarbonate markets or to rationalize their BPA and polycarbonate production capacity in response to the structurally altered competitive landscape created by Chinese overcapacity.

Feedstock Price Volatility for Phenol and Acetone Compressing BPA Production Economics and Introducing Raw Material Supply Uncertainty

BPA production economics are fundamentally determined by the cost and availability of phenol and acetone feedstocks, which are co-produced through the cumene peroxidation process and whose market prices are therefore structurally linked through a fixed stoichiometric co-production ratio that creates feedstock supply and pricing dynamics unique to the BPA value chain, where the simultaneous demand satisfaction requirements for both phenol and acetone in their respective derivative markets generate pricing volatility that affects BPA production cost in ways that are partially decoupled from the broader petrochemical feedstock cycle. The phenol market in Asia-Pacific is subject to supply disruption risk arising from the geographic concentration of phenol production at a limited number of large cumene-to-phenol production units in Japan, South Korea, Taiwan, China, and Thailand whose scheduled maintenance turnarounds, unplanned outages, and trade flow adjustments during periods of feedstock economics unfavorability create periodic phenol availability tightness that limits BPA production rates and elevates spot market BPA prices in ways that are difficult for downstream polycarbonate and epoxy resin producers to manage through short-term procurement adjustments. The acetone market dynamics present a structurally different challenge, where acetone is produced as a mandatory co-product of cumene peroxidation regardless of acetone demand, creating periodic acetone surplus situations particularly in markets where downstream acetone consumption in methyl methacrylate, solvent, and pharmaceutical applications does not grow commensurately with phenol demand, depressing acetone co-product credit realizations and affecting the integrated production economics of phenol and BPA producers whose cost optimization frameworks depend on adequate acetone revenue to offset phenol production costs.

Market Segmentation

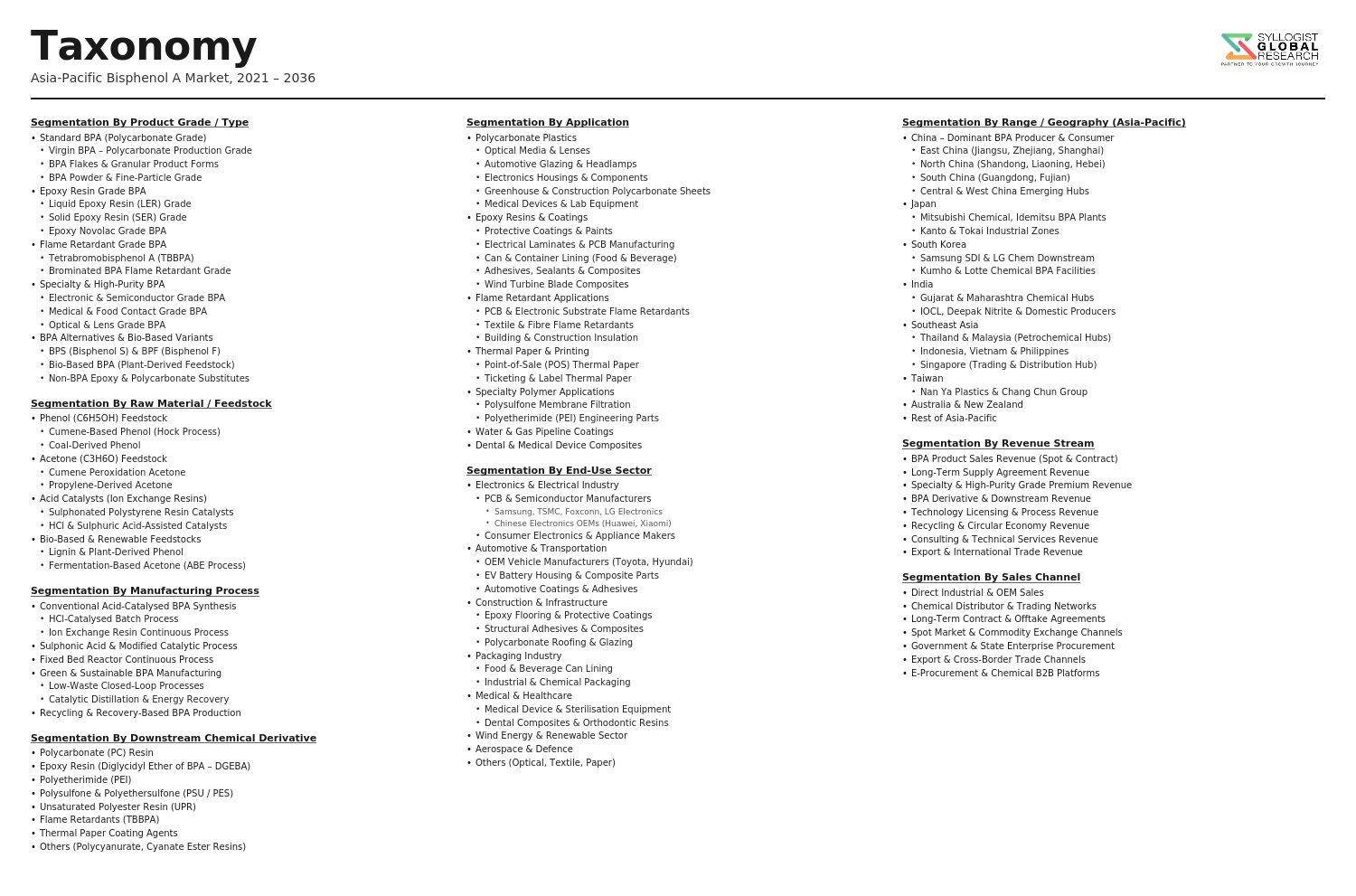

- Segmentation By Derivative Product

- Polycarbonate Resin

- Epoxy Resin (Liquid and Solid Bisphenol A Diglycidyl Ether)

- Tetrabromobisphenol A (TBBPA) Flame Retardant

- Unsaturated Polyester Resin (BPA-Based)

- Polysulfone and Polyethersulfone Specialty Polymers

- Thermal Paper Coating Developers (BPA-Based)

- Others

- Segmentation By End-Use Application

- Electrical and Electronic Laminates and PCB Manufacturing

- Automotive Components (Lighting, Glazing, Interior Trims)

- Construction and Safety Glazing

- Wind Energy Blade and Composite Manufacturing

- Protective and Industrial Coatings

- Optical Media and Precision Optical Components

- Food and Beverage Packaging Linings

- Medical Devices and Healthcare Equipment

- Adhesives and Sealants

- Consumer Electronics Enclosures and Components

- Thermal Paper and Specialty Paper Coating

- Others

- Segmentation By Grade

- Technical Grade BPA

- Polycarbonate Grade BPA

- Epoxy Grade BPA

- Optical Grade BPA and Polycarbonate

- Food Contact Grade BPA Derivatives

- Others

- Segmentation By Production Process

- Ion Exchange Resin Catalyzed BPA Synthesis

- Homogeneous Acid Catalyzed BPA Synthesis

- Interfacial Polycarbonate Polymerization

- Melt Transesterification Polycarbonate Polymerization

- BPA-Epichlorohydrin Epoxy Resin Synthesis

- Others

- Segmentation By End User

- Consumer Electronics Manufacturers

- Automotive OEMs and Tier-1 Suppliers

- Wind Turbine and Renewable Energy Equipment Manufacturers

- PCB and Electronic Component Manufacturers

- Construction and Building Materials Producers

- Paints, Coatings, and Adhesives Manufacturers

- Packaging and Container Manufacturers

- Medical Device and Healthcare Equipment Manufacturers

- Others

- Segmentation By Country

- China

- Japan

- South Korea

- India

- Taiwan

- Southeast Asia (Vietnam, Thailand, Malaysia, Indonesia)

- Australia and New Zealand

- Rest of Asia-Pacific

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total market valuation of the Asia-Pacific Bisphenol A Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by derivative product, end-use application, grade, and country, to enable BPA producers, polycarbonate and epoxy resin manufacturers, downstream industrial processors, and petrochemical investors to identify which derivative segments and national markets will generate the highest absolute demand growth and the most commercially favorable supply-demand balance through the forecast period?

- How is China’s aggressive polycarbonate capacity expansion, which has added over 2.2 million metric tonnes of new production since 2018, reshaping the Asia-Pacific polycarbonate and BPA supply-demand balance, price trajectory, and competitive dynamics among Chinese, Japanese, Korean, and international producers, and what is the projected polycarbonate price floor, capacity utilization stabilization timeline, and market share redistribution across producer nationalities as the oversupply cycle progresses through 2034?

- What is the projected BPA and epoxy resin demand trajectory from Asia-Pacific’s wind energy capacity buildout, specifically China’s 70 to 80 gigawatt annual wind installation program, India’s renewable energy expansion targets, and offshore wind development across Taiwan, South Korea, Japan, and Vietnam through 2034, and how does wind energy-driven epoxy resin demand growth compare in absolute volume and growth rate terms to traditional industrial coating, PCB laminate, and adhesive epoxy resin demand across the region?

- How are national BPA regulatory frameworks across Japan, South Korea, Australia, China, and India governing food contact migration limits, thermal paper developer restrictions, and medical device BPA content evolving through 2034, which application categories face the highest probability of formal BPA use restriction or prohibition within the forecast period, and how are BPA producers and derivative manufacturers developing BPA-free alternative product lines and substitution strategies to manage the commercial risk of regulatory-driven demand displacement in affected application segments?

- Who are the leading Asia-Pacific BPA producers including Sinopec, CNPC, Kumho P and B Chemical, Nan Ya Plastics, LG Chem, Mitsui Chemicals, and Mitsubishi Chemical, the major polycarbonate and epoxy resin manufacturers including Covestro, SABIC, Wanhua Chemical, and Luxi Chemical, and the key downstream application processors currently defining the competitive and commercial landscape of the Asia-Pacific BPA market, and what are their respective production capacities, plant locations, feedstock integration strategies, derivative product portfolios, customer industry relationships, regulatory compliance frameworks, capital expansion plans, and strategic positioning in response to the dual opportunities of Asia-Pacific industrial demand growth and the challenges of Chinese overcapacity and BPA regulatory evolution through the forecast period?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- BPA Regulatory Restriction, Phase-Out Mandate & Substitution Pressure Risk Across Asia-Pacific Jurisdictions

- Feedstock Price Volatility: Phenol, Acetone & Benzene Supply Chain & Price Risk in Asia-Pacific

- Capacity Oversupply, Chinese Export Pressure & Regional Price Realisation Risk for BPA Producers

- BPA-Free Transition, Epoxy Resin Reformulation & Polycarbonate Substitution Risk from Alternative Materials

- Environmental Liability, Endocrine Disruptor Classification & Extended Producer Responsibility Risk for BPA Downstream Users

- Regulatory Framework & Standards

- China GB Standards, MEE Chemical Registration & BPA Restriction Regulations for Food Contact & Consumer Applications

- Japan MHLW Food Sanitation Act, CSCL Chemical Substance Control & BPA Usage Restrictions in Food Contact Materials

- South Korea K-REACH, NIER Chemical Safety Assessment & BPA Regulation in Consumer & Industrial Applications

- Australia NICNAS / AICIS Assessment, FSANZ Food Contact Standards & BPA Regulatory Framework

- ASEAN National Chemical Regulations, Food Contact Material Standards & BPA Restriction Developments Across Southeast Asian Markets

- Asia-Pacific Bisphenol A (BPA) Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Metric Tonnes)

- Market Size & Forecast by Product Type

- Bisphenol A (BPA) Monomer

- Epoxy Resin (BPA-Based)

- Polycarbonate (PC) Resin

- BPA-Based Unsaturated Polyester & Vinyl Ester Resins

- BPA Flame Retardants (Tetrabromobisphenol A, TBBPA)

- BPA-Based Thermal Paper Coating & Developer

- BPA-Based Dental Sealants & Composites

- BPA Alternatives & BPA-Free Substitute Compounds (BPS, BPF & Next-Generation Alternatives)

- Market Size & Forecast by Downstream Derivative

- Epoxy Resin Derivatives (Liquid, Solid & Solution Epoxy)

- Polycarbonate Resin & Compounds

- Flame Retardant Derivatives (TBBPA & Brominated Epoxy)

- Specialty Resins & Coatings Derivatives

- Market Size & Forecast by Application

- Epoxy Resin Coatings (Can Linings, Metal Coatings & Industrial Protective Coatings)

- Electrical Laminates & Printed Circuit Boards (PCB)

- Composites, Wind Blade & Structural Adhesives

- Polycarbonate Optical Media, Lenses & Glazing

- Polycarbonate Automotive Components & Lightweighting

- Polycarbonate Consumer Electronics Housings & Components

- Food & Beverage Can Internal Coatings & Drum Linings

- Thermal Paper & Point-of-Sale Receipt Coatings

- Dental Composites, Sealants & Medical Device Applications

- Market Size & Forecast by End-Use Industry

- Electrical & Electronics

- Automotive & Transportation

- Packaging (Food & Beverage, Industrial & Chemical Packaging)

- Construction & Infrastructure

- Wind Energy & Composites

- Consumer Goods & Appliances

- Healthcare & Medical Devices

- Aerospace & Defence

- Market Size & Forecast by Purity Grade

- Technical Grade BPA

- Electronic & High-Purity Grade BPA

- Food Contact Grade BPA

- Market Size & Forecast by End-User

- Epoxy Resin Manufacturers

- Polycarbonate Resin Manufacturers

- Flame Retardant Manufacturers

- Coating, Paint & Varnish Manufacturers

- Electrical & Electronic Component Manufacturers

- Automotive Component Manufacturers

- Packaging & Container Manufacturers

- Market Size & Forecast by Sales Channel

- Direct Producer-to-Downstream Manufacturer Supply

- Distributor, Stockist & Chemical Trading Company

- Long-Term Contract & Toll Processing Arrangement

- Spot Market & Commodity Exchange Purchase

- Import via Authorised Agent & Trading House

- East Asia Bisphenol A (BPA) Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Product Type

- By Application

- By End-Use Industry

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- South Asia Bisphenol A (BPA) Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Product Type

- By Application

- By End-Use Industry

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Southeast Asia Bisphenol A (BPA) Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Product Type

- By Application

- By End-Use Industry

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Oceania Bisphenol A (BPA) Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Product Type

- By Application

- By End-Use Industry

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Central Asia Bisphenol A (BPA) Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Product Type

- By Application

- By End-Use Industry

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Bisphenol A (BPA) Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Product Type

- By Application

- By End-Use Industry

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- *Countries Analyzed in the Syllogist Global Research Portfolio: China, Japan, India, South Korea, Australia, Singapore, Indonesia, Thailand, Malaysia, Vietnam, Philippines, Pakistan, Bangladesh, New Zealand, Taiwan, Hong Kong SAR, Sri Lanka, Myanmar, Cambodia, Laos

- Technology Landscape & Innovation Analysis

- BPA Production Technology Deep-Dive: Ion Exchange Resin Catalyst, Fixed-Bed & Sulphonic Acid Catalyst Process Efficiency & Selectivity

- Epoxy Resin Manufacturing Technology: Liquid Epoxy Resin (LER), Solid Epoxy Resin (SER) & Advanced Formulation for Electrical Laminates

- Polycarbonate Resin Manufacturing Technology: Phosgene-Based & Non-Phosgene (Melt Transesterification) Polycarbonate Process

- BPA-Free Epoxy & Polycarbonate Alternative Technology: BPS, BPF, Novolac Epoxy, Bio-Based & Cycloaliphatic Epoxy Routes

- Recycled & Circular Polycarbonate Technology: Chemical Depolymerisation, Methanol Recovery & Virgin-Quality Recycled PC Production

- High-Purity & Electronic-Grade BPA Manufacturing Technology for Advanced PCB & Semiconductor Packaging Applications

- Waste Treatment, Effluent Management & BPA Contamination Remediation Technology in Asia-Pacific Production Facilities

- Patent & IP Landscape in BPA, Epoxy Resin & Polycarbonate Technologies Relevant to Asia-Pacific

- Value Chain & Supply Chain Analysis

- Phenol, Acetone & Cumene Feedstock Production & Supply Chain in Asia-Pacific

- BPA Monomer Synthesis, Purification, Prilling & Packaging Supply Chain

- Epoxy Resin Formulation, Hardener & Additive Supply Chain in Asia-Pacific

- Polycarbonate Compounding, Colouring & Specialty Grade Manufacturing Supply Chain

- Downstream Converter, Laminator & Component Manufacturer Procurement Channel

- Chemical Distributor, Stockist & Trading Company Channel in Asia-Pacific

- Waste BPA, Off-Spec Material, Effluent Treatment & Circular Economy Value Chain

- Pricing Analysis

- BPA Monomer Spot & Contract Price Benchmarking Across Key Asia-Pacific Markets: China, Japan, South Korea & India

- BPA-to-Epoxy Resin & BPA-to-Polycarbonate Price Spread & Margin Analysis

- Import vs. Domestic Production Cost Comparison & Landed Cost Analysis for BPA in Asia-Pacific

- Electronic-Grade vs. Technical-Grade BPA Price Premium & Purity Specification Analysis

- BPA-Free Alternative Pricing: BPS, BPF & Bio-Based Substitute Price Premium vs. BPA Analysis

- Total BPA Cost-in-Use per Downstream Application Across Epoxy Resin, Polycarbonate & Flame Retardant End-Uses

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of BPA & Downstream Derivatives: Carbon Footprint, Energy Intensity & Water Use Across Production Routes

- BPA Endocrine Disruption, Human Health Impact & Environmental Persistence: Scientific Evidence & Regulatory Response in Asia-Pacific

- BPA-Free Transition in Asia-Pacific: Substitution Progress, Alternative Material Performance & Circular Economy Implications

- Wastewater Treatment, BPA Contamination in Aquatic Ecosystems & Industrial Effluent Management in Asia-Pacific

- Regulatory-Driven Sustainability, SDG 3 (Good Health), SDG 6 (Clean Water) & SDG 12 (Responsible Consumption) Alignment & ESG Disclosure Requirements

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Product Type & Country)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Product Type, Application & Country

- Player Classification

- Integrated Petrochemical & BPA Monomer Producers in Asia-Pacific

- Dedicated Epoxy Resin Manufacturers Using BPA Feedstock

- Polycarbonate Resin Producers in Asia-Pacific

- Flame Retardant (TBBPA) Manufacturers

- BPA-Free Alternative & Specialty Resin Manufacturers

- Chemical Distributors & Trading Companies for BPA in Asia-Pacific

- Downstream Converters & Fabricators with Significant BPA Consumption

- Technology Licensors & Process Engineering Companies for BPA & Derivatives

- Competitive Analysis Frameworks

- Market Share Analysis by Product Type, Application & Country

- Company Profile

- Company Overview & Headquarters

- BPA & Downstream Derivative Products & Grade Portfolio

- Key Customer Relationships & Reference Accounts in Asia-Pacific

- Manufacturing Footprint & Production Capacity in Asia-Pacific

- Revenue (BPA & Derivatives Segment) & Order Book

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Capacity Expansion, Grade Launches, Regulatory Response Initiatives)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Production Scale vs. Product Portfolio Breadth)

- Key Company Profiles

- Market Structure & Concentration

- Strategic Opportunity Analysis

- Strategic Output

- Market Opportunity Matrix: By Product Type, Application, End-Use Industry, End-User & Country

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output