Market Definition

The Global Deep Sea Mining Market encompasses the exploration, resource assessment, technology development, equipment manufacturing, regulatory licensing, extraction operations, and mineral processing activities associated with the recovery of commercially valuable mineral deposits located on and beneath the seafloor at water depths typically exceeding 200 meters and extending to abyssal plain depths of 4,000 to 6,000 meters across international seabed areas and the exclusive economic zones of coastal states. Deep sea mining targets three primary deposit categories distinguished by their geological origin, mineral composition, water depth, and extraction method requirements: polymetallic nodules, which are potato-sized concretions of manganese, nickel, copper, cobalt, and rare earth elements resting on the sediment surface of abyssal plains at depths of 4,000 to 6,000 meters, with the Clarion-Clipperton Zone in the eastern Pacific Ocean representing the most extensively explored and commercially prospective nodule province globally; seafloor massive sulfide deposits, which are hydrothermal vent-associated mineral accumulations rich in copper, zinc, gold, silver, and lead formed at mid-ocean ridge and back-arc basin settings at depths of 1,500 to 3,500 meters; and cobalt-rich ferromanganese crusts, which are mineral coatings encrusting the flanks and summits of seamounts and underwater ridges at depths of 800 to 2,500 meters containing high concentrations of cobalt, nickel, platinum, tellurium, and rare earth elements. The market encompasses the complete value chain from seabed mapping, geophysical survey, and resource estimation through robotic collector vehicle design and deployment, riser and lift system engineering, support vessel operations, seafloor-to-surface mineral transport, onshore dewatering and processing, and the environmental monitoring, impact assessment, and regulatory compliance activities mandated by the International Seabed Authority and coastal state maritime authorities. Key participants include deep sea mining contractors, remotely operated vehicle developers, naval engineering companies, metallurgical processing firms, technology licensors, battery and critical mineral consumers, and environmental science organizations.

Market Insights

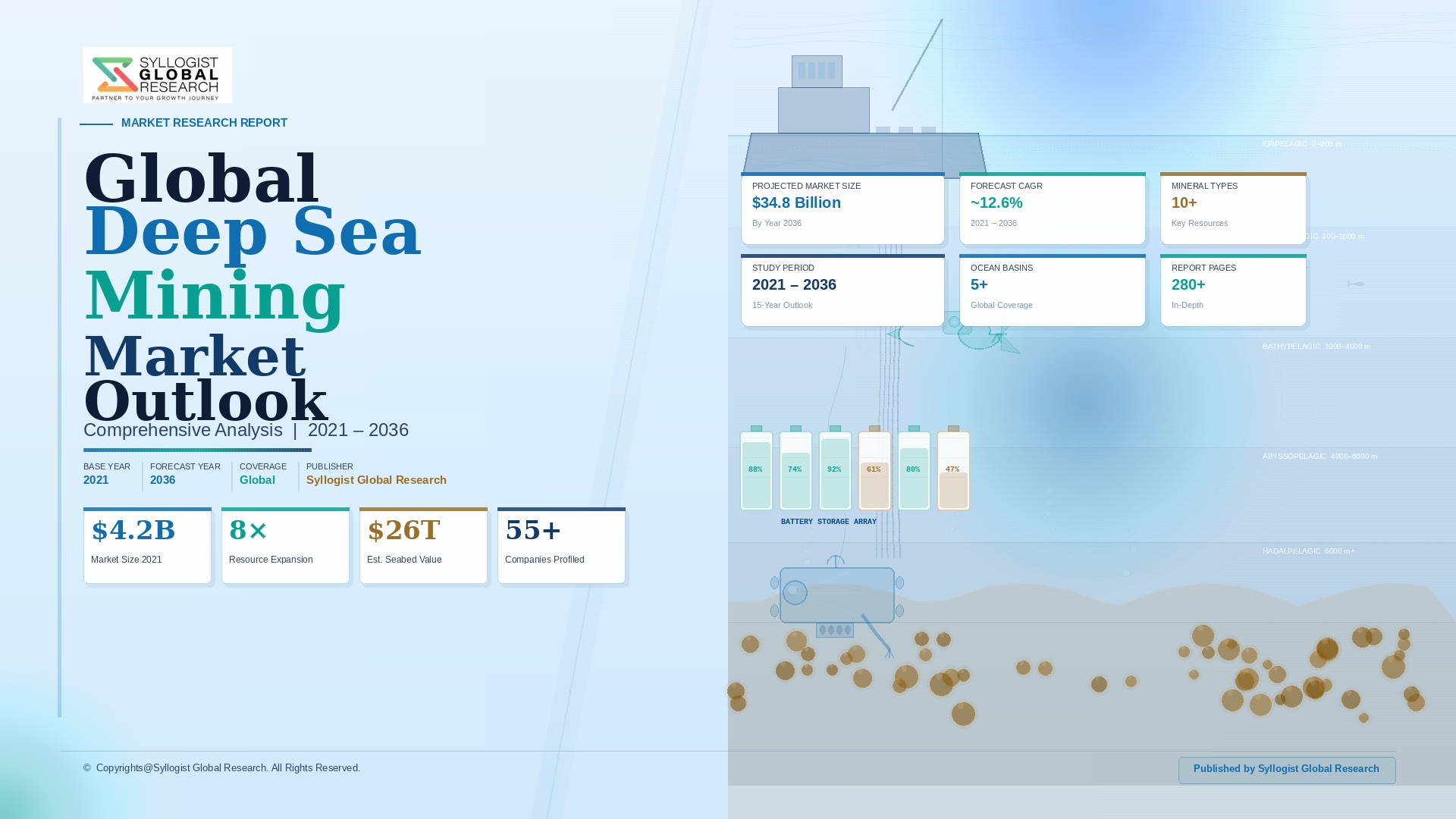

The global deep sea mining market was valued at approximately USD 1.2 billion in 2025, encompassing exploration, technology development, regulatory licensing, and pre-commercial pilot operations, and is projected to reach USD 11.6 billion by 2034, advancing at a compound annual growth rate of 28.7% over the forecast period from 2027 to 2034 as the first commercial-scale polymetallic nodule extraction operations transition from pilot to production phase and seafloor massive sulfide projects in national exclusive economic zones advance through environmental permitting and development investment decision processes. The market’s exceptional growth trajectory reflects the convergence of a structurally significant demand imperative for the critical minerals concentrated in deep sea deposits, particularly nickel, cobalt, manganese, copper, and rare earth elements that are indispensable to lithium-ion battery cathode chemistry, permanent magnet production, and clean energy technology manufacturing, with the progressive maturation of remotely operated extraction technology platforms, nodule collector vehicle systems, and riser and lift engineering that are advancing from prototype validation toward commercial deployment readiness. The Clarion-Clipperton Zone in the Pacific Ocean, where the International Seabed Authority has issued 17 exploration contracts covering approximately 1.4 million square kilometers of polymetallic nodule-bearing abyssal plain, is estimated to contain nodule resources with an aggregate contained metal value exceeding USD 8 trillion at 2025 metal prices, representing a mineral endowment of extraordinary scale relative to any comparable terrestrial mineral province, with individual exploration contract areas of 75,000 square kilometers each estimated to contain 200 to 400 million metric tons of wet nodule resource at surface densities of 10 to 20 kilograms per square meter, collectively positioning the Clarion-Clipperton Zone as the globally dominant commercial development target for the first generation of deep sea mining operations.

The critical minerals supply imperative driving deep sea mining development is grounded in specific and quantifiable supply deficit projections for the battery and clean energy technology metals concentrated in polymetallic nodules and seafloor massive sulfide deposits, with nickel demand for battery applications projected to reach approximately 1.8 million metric tons per year by 2034 against a current global mined supply of approximately 3.3 million metric tons per year from predominantly laterite and sulfide terrestrial sources whose reserve base and geographic concentration in Indonesia, the Philippines, Russia, and New Caledonia create supply security concerns for battery manufacturers and electric vehicle producers in North America, Europe, and Japan seeking to diversify critical mineral procurement away from politically sensitive supply chains. Polymetallic nodules recovered from the Clarion-Clipperton Zone contain average grades of approximately 1.3% nickel, 1.1% copper, 0.2% cobalt, and 29% manganese per dry metric ton, a multi-metal co-product profile that generates revenue from four simultaneous commodity streams and creates a fundamentally different economic model relative to single-commodity terrestrial mining, with the co-product economics providing a natural hedge against individual metal price volatility and improving project returns across a range of metal price scenarios. The cobalt content of Clarion-Clipperton Zone nodules is particularly commercially significant, as a single nodule production operation of 3 million wet metric tons per year annual throughput would yield approximately 5,500 to 6,000 metric tons of contained cobalt annually, equivalent to approximately 6% of current global cobalt mine production dominated by the Democratic Republic of Congo, providing a meaningful supply diversification contribution to a cobalt market where geographic concentration and artisanal mining conditions create persistent supply security and ethical sourcing concerns for battery supply chain managers.

The technology development and engineering maturation landscape of the deep sea mining market is being shaped by the parallel advancement of three interdependent system platforms whose combined readiness determines the commercial viability of nodule extraction at depth: remotely operated collector vehicle systems that traverse the abyssal seabed hydraulically harvesting nodules from the sediment surface without excavating the underlying substrate; vertical riser and lift systems encompassing hydraulic or airlift pump arrays, flexible riser pipe strings of 4,000 to 5,000 meter length, and seafloor buffer storage stations that transport slurried nodules from collection depth to the production support vessel; and surface production support vessels of specialized design incorporating nodule dewatering, sizing, and temporary storage facilities alongside the riser top tensioning, dynamic positioning, and marine operations infrastructure required for continuous seabed production. The Metals Company, operating through its NORI and TOML subsidiary contract areas in the Clarion-Clipperton Zone in partnership with Allseas engineering, completed a pilot nodule collection campaign in 2022 that recovered approximately 3,000 metric tons of polymetallic nodules from 4,500 meter depth using a prototype collector vehicle and riser system, demonstrating the technical feasibility of nodule recovery at commercial water depth and providing critical engineering data on sediment plume generation, collector vehicle performance, and riser system operability that informs the design of first-generation commercial production systems. Nautilus Minerals, despite its insolvency in 2019 following cost overruns and permitting delays at the Solwara 1 seafloor massive sulfide project in Papua New Guinea’s Bismarck Sea, generated substantial engineering knowledge in seafloor massive sulfide extraction equipment design including the auxiliary cutter, bulk cutter, and collecting machine system architecture that continues to inform seafloor massive sulfide project engineering by successor developers in Japan, the Republic of Korea, and Canada.

The regulatory and geopolitical landscape governing deep sea mining in international waters is at a pivotal juncture following the International Seabed Authority’s failure to finalize the Mining Code governing commercial exploitation regulations by the July 2023 deadline triggered by Nauru’s invocation of the two-year rule on behalf of The Metals Company’s NORI subsidiary, a regulatory impasse that has created a legal ambiguity in which sponsoring states can submit exploitation applications under existing Part XI provisions of the United Nations Convention on the Law of the Sea but the International Seabed Authority lacks a formally adopted regulatory framework against which to evaluate and approve such applications, effectively delaying the commencement of commercial nodule extraction in international waters beyond the timelines originally anticipated by the leading commercial developers and extending the pre-revenue exploration and technology development phase of the market. The International Seabed Authority had issued 31 exploration contracts covering polymetallic nodules, seafloor massive sulfides, and cobalt-rich ferromanganese crusts as of 2025, with sponsoring states including China, South Korea, Japan, India, France, Germany, Russia, and multiple small island developing states, reflecting the strategic importance attributed to deep sea mineral rights by major economies seeking to establish resource access positions for battery and clean energy metal supply chains ahead of commercial extraction framework finalization. Within national exclusive economic zones, several coastal states are advancing deep sea mineral development under domestic regulatory frameworks, with Japan progressing cobalt-rich crust exploration and seafloor massive sulfide development in its western Pacific exclusive economic zone, Papua New Guinea re-evaluating the Solwara 1 area, and Cook Islands advancing polymetallic nodule licensing within its exclusive economic zone under national mining legislation that provides a clearer and more expedient regulatory pathway than international seabed area governance frameworks.

Key Drivers

Structural Critical Mineral Supply Deficits for Battery and Clean Energy Technologies Creating Strategic Commercial and National Security Imperatives for Deep Sea Resource Development

The clean energy transition’s insatiable demand for battery metals including nickel, cobalt, manganese, and copper is generating projected supply deficits that terrestrial mining investment pipelines are widely assessed as insufficient to close within the timeframes required by electric vehicle production scaling and grid-scale energy storage deployment, creating both a commercial investment case and a national supply security imperative for deep sea mining development that is mobilizing capital from battery manufacturers, electric vehicle producers, critical mineral funds, and sovereign wealth vehicles seeking to secure long-term access to the exceptional mineral endowment of deep sea polymetallic nodule and seafloor massive sulfide deposits. Global cobalt demand for battery applications is projected to reach approximately 320,000 metric tons per year by 2034, compared to current global mine supply of approximately 210,000 metric tons per year dominated at approximately 72% by the Democratic Republic of Congo, a geographic concentration that creates acute supply security concerns for battery supply chain managers in the United States, European Union, Japan, and South Korea who are subject to government critical mineral supply chain resilience mandates including the United States Inflation Reduction Act’s domestic content and free trade agreement sourcing requirements, the European Union’s Critical Raw Materials Act minimum domestic processing thresholds, and Japan’s strategic mineral stockpile and supply diversification programs, collectively making deep sea cobalt and nickel supply an element of industrial policy rather than merely a commercial mining investment decision for multiple major economies simultaneously. The multi-metal co-product economics of polymetallic nodules, which simultaneously supply nickel, cobalt, copper, and manganese from a single extraction operation, offer battery supply chain investors a uniquely diversified critical mineral supply position that reduces concentration risk relative to any single-commodity terrestrial supply investment of equivalent capital scale.

Rapid Advancement of Deep Sea Robotic Collection Technology, Riser Engineering, and Remotely Operated Vehicle Systems Progressively De-Risking Commercial Extraction Feasibility

The engineering maturation of the three principal technology systems required for commercial polymetallic nodule extraction, namely seabed collector vehicles, deep water riser and hydraulic lift systems, and purpose-designed production support vessels, has accelerated substantially over the 2018 to 2025 period driven by increasing private capital investment, technology partnership programs between deep sea mining contractors and established offshore oil and gas engineering companies with relevant deep water systems expertise, and the completion of multiple pilot collection and system integration trials at commercial water depths that have generated the performance data and engineering confidence required to advance project bankability assessments toward investment decision readiness. Allseas, the global offshore pipeline and marine engineering specialist, has invested significantly in developing a purpose-designed nodule production vessel and riser system for deployment in partnership with The Metals Company, leveraging its extensive experience in deepwater offshore pipeline installation to engineer the riser tensioning, vessel interface, and seafloor-to-surface transport system architecture for nodule slurry transport from 4,500 meter collection depth. Remotely operated collector vehicle technology has advanced through multiple design generations incorporating improved hydraulic nodule pickup efficiency, reduced sediment disturbance and plume generation, autonomous navigation across uneven abyssal terrain, and real-time monitoring systems that enable surface-controlled collection optimization, with collector vehicle prototypes tested by The Metals Company, Global Sea Mineral Resources in Belgium, and Japan’s Nippon Steel and Sumitomo Metal Corporation-backed programs each contributing incremental engineering knowledge to the commercial collector vehicle design space. The progressive transfer of offshore oil and gas industry expertise in dynamic positioning, deep water riser systems, subsea robotics, and remote sensing to the deep sea mining sector is substantially accelerating technology readiness timelines.

Growing State Strategic Interest, Sovereign Critical Mineral Policies, and National Exclusive Economic Zone Development Initiatives Expanding the Investable Deep Sea Mining Opportunity

National governments across the Indo-Pacific, Atlantic, and Caribbean regions are increasingly treating deep sea mineral resources within their exclusive economic zones as strategic national assets requiring active development investment and regulatory framework establishment, driven by the recognition that polymetallic nodule, seafloor massive sulfide, and cobalt-rich crust deposits within sovereign maritime jurisdiction represent a potentially transformative source of battery and technology metal supply that can contribute to domestic industrial development, export revenue diversification, and critical mineral supply chain sovereignty. Japan has invested over USD 700 million in seafloor mineral exploration and technology development programs across its Pacific and Indian Ocean exclusive economic zone areas since 2000, advancing cobalt-rich ferromanganese crust resource characterization at seamount sites in the Minami-Torishima exclusive economic zone where cobalt grades exceeding 0.8% have been documented, and conducting seafloor massive sulfide production tests in the Okinawa Trough at water depths of approximately 1,600 meters, positioning Japan as the most technically advanced national program for exclusive economic zone deep sea mineral development globally. The Republic of Korea’s Deep Sea Resources Development Organization has maintained a sustained national deep sea mineral exploration program spanning Clarion-Clipperton Zone nodule areas, Indian Ocean sulfide fields, and Korean exclusive economic zone seamount crust sites, with government-funded annual exploration expenditure of approximately USD 45 million in 2025, reflecting Korea’s strategic calculation that battery metal supply security requires a diversified mineral access portfolio including deep sea resource positions that complement its terrestrial mining investment and recycling programs. Cook Islands, Kiribati, the Federated States of Micronesia, and other Pacific small island developing states are progressing national exclusive economic zone nodule licensing frameworks that represent commercially significant development opportunities in potentially more expedient regulatory environments than international seabed governance.

Key Challenges

Profound Scientific Uncertainty Around Deep Sea Ecosystem Impacts and the Absence of a Finalized International Seabed Authority Mining Code Creating Regulatory and Environmental License Risk

The most fundamental and commercially consequential challenge confronting the global deep sea mining market is the combination of unresolved scientific uncertainty regarding the nature, scale, and permanence of ecological impacts from commercial nodule extraction operations on abyssal plain ecosystems, and the failure of the International Seabed Authority to finalize and adopt the Mining Code regulatory framework that governs commercial exploitation applications in international seabed areas, creating a compounded risk of environmental license erosion and indefinite regulatory delay that threatens to postpone commercial operations significantly beyond the timelines embedded in deep sea mining project development plans and investor return projections. Deep sea abyssal plain ecosystems, while not photosynthetically productive, harbor extraordinary and largely undescribed biodiversity concentrated in the nodule fields themselves, with scientific expeditions to the Clarion-Clipperton Zone documenting thousands of benthic species including sponges, polychaete worms, holothurians, foraminifera, and microbial communities for which the nodule substrate constitutes the primary habitat, and whose population recovery timelines following physical disturbance by collector vehicle passes are measured in decades to centuries based on available natural and experimental disturbance study evidence, generating scientific opinion that commercial nodule extraction causes effectively permanent habitat loss at the scale of the extraction footprint. A growing coalition of nations including France, Chile, Germany, New Zealand, Palau, Fiji, and Samoa have called for a moratorium or precautionary pause on commercial deep sea mining pending completion of environmental impact assessment frameworks and mining code finalization, while major corporate consumers of battery metals including BMW, Volkswagen, Google, Samsung SDI, and Volvo Group have issued statements declining to source materials from deep sea mining operations until environmental standards are established, creating demand-side reputational risk that complicates the offtake agreement fundraising essential to deep sea mining project financing.

Exceptional Capital Investment Requirements, Absence of Commercial Precedent, and Project Financing Complexity for First-of-Kind Ultra-Deep Commercial Extraction Operations

The capital investment required to develop a first-generation commercial polymetallic nodule extraction operation in the Clarion-Clipperton Zone is estimated at approximately USD 4.5 to USD 6.8 billion encompassing production support vessel construction and conversion, collector vehicle fleet development and manufacturing, riser and lift system fabrication and installation, onshore processing facility construction, environmental monitoring infrastructure deployment, and the working capital required to sustain multi-year production ramp-up operations before steady-state revenue generation, representing a project financing challenge of exceptional complexity for an industry sector with no operational commercial precedent, no established insurance frameworks for seabed extraction equipment, no track record of production performance at commercial scale, and no commodity price certainty over the decade-long development and ramp-up period during which project economics must be sustained. Commercial lenders and institutional investors evaluating deep sea mining project financing face a risk profile that combines the technical uncertainties of first-of-kind marine engineering systems operating continuously at 4,000 to 5,000 meter depth with no established maintenance and repair experience base, the regulatory uncertainties of International Seabed Authority mining code finalization and exploitation license approval processes whose timeline and outcome cannot be reliably predicted, the market risk of metal price movements over multi-decade project lives, and the reputational risk of association with an industry sector facing active environmental opposition and corporate customer commitment avoidance, collectively creating a financing environment that requires substantial equity risk tolerance from project sponsors and strategic investors willing to accept first-mover commercial risk in the absence of traditional project finance debt availability on commercially acceptable terms. The insolvency of Nautilus Minerals in 2019 following its inability to raise construction financing for the Solwara 1 seafloor massive sulfide project despite extensive development expenditure exceeding USD 500 million continues to weigh on investor confidence in deep sea mining project execution and financing risk.

Sediment Plume Generation, Benthic Disturbance, and Deep Ocean Noise and Light Pollution Creating Operational Environmental Compliance Obligations of Unprecedented Complexity

Commercial-scale polymetallic nodule extraction operations generate multiple categories of environmental impact whose characterization, prediction, monitoring, and mitigation impose operational constraints, technology design requirements, and ongoing scientific compliance obligations of unprecedented complexity for any extractive industry project, encompassing the generation of seafloor sediment plumes from collector vehicle disturbance that can travel tens to hundreds of kilometers from the extraction site before settling, the discharge of deep cold water and fine sediment particulate from the production support vessel back into the mid-water column during onboard dewatering operations, continuous acoustic and light disturbance of the deepwater environment from collector vehicle and riser system operations, and the complete physical removal of nodule substrate habitat from within the extraction footprint that eliminates the primary hard substrate resource for benthic community colonization across the mined area for the duration of the operational lifetime. Environmental monitoring requirements mandated by the International Seabed Authority’s environmental management and monitoring plan framework require commercial operators to deploy extensive arrays of benthic landers, water column sensors, acoustic monitoring systems, and biological sampling programs across impact zones extending far beyond the direct extraction footprint, representing an ongoing operational cost estimated at USD 20 to USD 50 million per year per commercial operation that adds substantially to operating cost structure and requires dedicated scientific and environmental management capability as a permanent component of commercial operations. The absence of established environmental baseline data for many Clarion-Clipperton Zone contract areas, combined with the limited understanding of naturally occurring variability in abyssal plain ecosystem parameters, makes it difficult to define unambiguous environmental impact thresholds and adaptive management trigger points that would give commercial operators and regulators the decision framework needed to manage extraction operations within clearly defined environmental compliance boundaries.

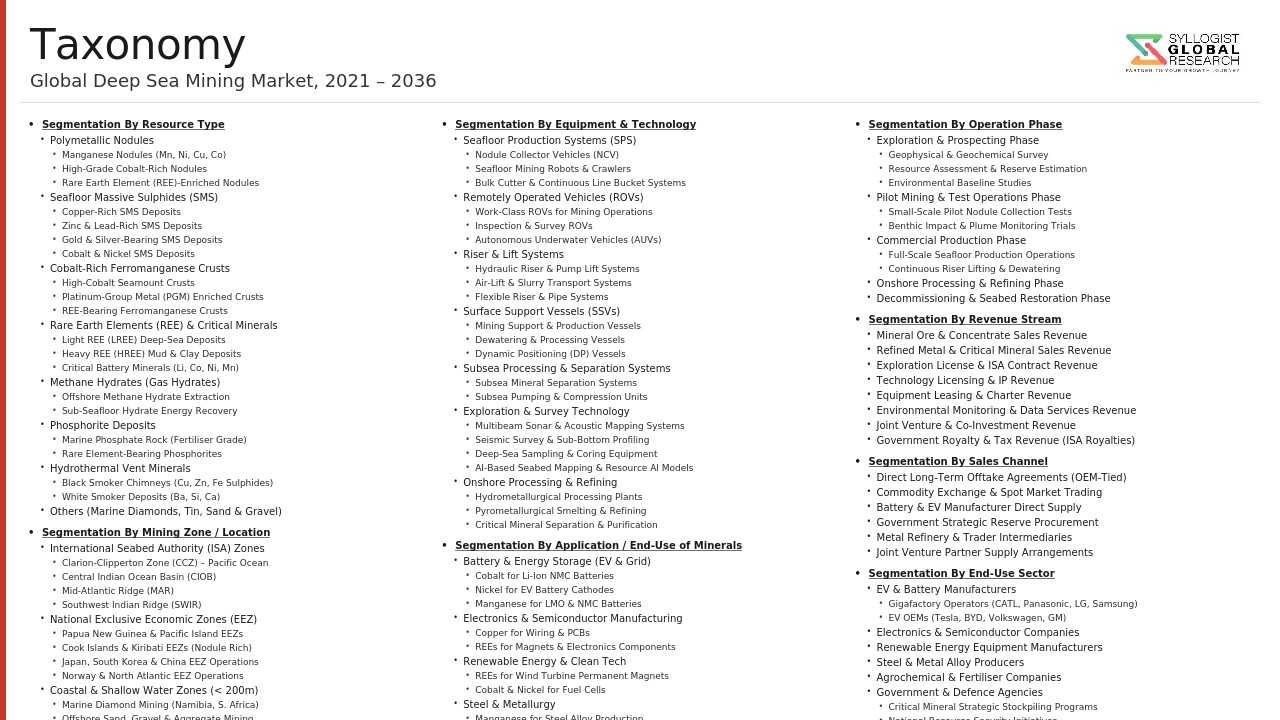

Market Segmentation

- Segmentation By Deposit Type

- Polymetallic Nodules (Manganese Nodules)

- Seafloor Massive Sulfide Deposits

- Cobalt-Rich Ferromanganese Crusts

- Phosphorite Deposits

- Others

- Segmentation By Water Depth

- Shallow Deep Sea (200 to 1,000 Meters)

- Intermediate Deep Sea (1,000 to 2,500 Meters)

- Deep Abyssal (2,500 to 4,000 Meters)

- Ultra-Abyssal (4,000 to 6,000 Meters)

- Segmentation By Target Mineral

- Manganese

- Nickel

- Copper

- Cobalt

- Zinc

- Gold and Silver

- Rare Earth Elements and Critical Minerals (Tellurium, Platinum, and Others)

- Others

- Segmentation By Technology and Equipment

- Seabed Collector Vehicles and Robotic Harvesting Systems

- Riser and Hydraulic Lift Systems

- Production Support Vessels and Offshore Processing Platforms

- Remotely Operated Vehicles (ROVs) and Autonomous Underwater Vehicles (AUVs)

- Seabed Survey and Geophysical Mapping Systems

- Mineral Processing and Metallurgical Recovery Systems

- Environmental Monitoring and Sensing Infrastructure

- Others

- Segmentation By Activity Type

- Seabed Exploration and Resource Assessment

- Environmental Impact Assessment and Baseline Studies

- Technology Development and Pilot Testing

- Commercial Extraction Operations

- Onshore Mineral Processing and Refining

- Others

- Segmentation By Jurisdiction

- International Seabed Area (International Seabed Authority Regulated)

- National Exclusive Economic Zones (Coastal State Regulated)

- Continental Shelf Extended Jurisdiction Areas

- Others

- Segmentation By End-Use Industry

- Battery Manufacturing and Electric Vehicle Supply Chains

- Clean Energy Technology and Renewable Energy Equipment

- Electronics and Semiconductor Manufacturing

- Steel and Specialty Alloy Production

- Defense and Aerospace

- Others

- Segmentation By Region

- Pacific Ocean (Clarion-Clipperton Zone, Central Pacific, and Western Pacific)

- Indian Ocean

- Atlantic Ocean (Mid-Atlantic Ridge and Adjacent Areas)

- Arctic and Antarctic Regions

- National Exclusive Economic Zones by Region (Asia-Pacific, Latin America, Caribbean, and Pacific Island States)

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Deep Sea Mining Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by deposit type including polymetallic nodules, seafloor massive sulfides, and cobalt-rich ferromanganese crusts, by activity type including exploration, environmental assessment, technology development, and commercial extraction, and by target mineral including nickel, cobalt, copper, manganese, zinc, gold, and rare earth elements, to enable deep sea mining contractors, technology developers, critical mineral investors, battery manufacturers, national government resource agencies, and environmental finance institutions to assess the size, growth trajectory, and commercial maturation timeline of each market segment across the forecast period to 2034?

- What is the current status of the International Seabed Authority Mining Code development and adoption process, what are the most likely timeline scenarios for finalization of exploitation regulations governing commercial nodule extraction in international seabed areas, how does the July 2023 two-year rule invocation by Nauru on behalf of NORI affect the legal standing of exploitation applications submitted in advance of Mining Code adoption, and what are the implications of alternative regulatory outcomes including Mining Code adoption, exploitation license approval under existing Part XI provisions, or a prolonged moratorium for the commercial development timelines and financing structures of the leading Clarion-Clipperton Zone nodule extraction projects advanced by The Metals Company, Global Sea Mineral Resources, UK Seabed Resources, and the state-sponsored programs of China, Japan, South Korea, and India?

- What is the current technology readiness level, engineering performance validation status, remaining development investment requirement, and projected commercial deployment timeline of the three critical system platforms required for commercial polymetallic nodule extraction including seabed collector vehicles, deep water riser and hydraulic lift systems, and production support vessel designs, and how are the leading technology developers including The Metals Company in partnership with Allseas, Global Sea Mineral Resources with its Patania II collector vehicle program, and state-sponsored programs in Japan and South Korea differentiating their technical approaches to collector vehicle efficiency, sediment plume minimization, riser system reliability, and production vessel design to address the engineering performance and environmental compliance requirements of commercial-scale operations at 4,000 to 5,000 meter depth?

- How are the critical mineral supply security imperatives and domestic content requirements embedded in the United States Inflation Reduction Act, the European Union Critical Raw Materials Act, and Japan and South Korea’s strategic mineral supply diversification programs expected to shape government policy support, strategic investment, and offtake agreement structures for deep sea mining projects that would supply battery-grade nickel, cobalt, copper, and manganese to domestic processing and battery manufacturing supply chains, and what investment incentive mechanisms, strategic mineral stockpile commitments, development finance institution support programs, and diplomatic engagement with International Seabed Authority processes are major economies deploying to accelerate deep sea mineral resource development aligned with their critical mineral supply chain resilience objectives?

- What are the quantified environmental impact assessments, sediment plume dispersion modeling results, benthic biodiversity impact studies, and long-term ecosystem recovery projections available from existing disturbance experiments and pilot extraction operations in the Clarion-Clipperton Zone and other deep sea mining prospect areas, how do these scientific findings inform the environmental threshold and adaptive management frameworks being developed by the International Seabed Authority and national regulatory bodies for commercial exploitation licensing, and what environmental monitoring technology platforms, mitigation engineering design requirements, and ongoing scientific compliance obligations are likely to be mandated as conditions of commercial exploitation authorization in ways that affect the operating cost structure, technology design specifications, and commercial viability assessments of first-generation deep sea mining operations?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Geological & Resource Uncertainty Risk

- Regulatory, Permitting & Geopolitical Risk

- Technology & Operational Risk

- Market, Commodity Price & Demand Risk

- Environmental, Reputational & Social Licence Risk

- Regulatory Framework & Standards

- International Seabed Authority (ISA) Mining Code, Exploitation Regulations & Area Governance

- National EEZ Deep Sea Mining Legislation, Licensing & Permitting Frameworks

- Environmental Impact Assessment (EIA), Marine Protected Area & Biodiversity Offset Regulations

- UNCLOS, International Maritime Law & High Seas Treaty (BBNJ Agreement) Implications

- Vessel Classification, Equipment Safety, Operational Standards & Worker Health Regulations

- Global Deep Sea Mining Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Metric Tonnes of Wet & Dry Ore)

- Market Size & Forecast by Resource Type

- Polymetallic / Manganese Nodules (Abyssal Plain Deposits, 4,000–6,000m)

- Seafloor Massive Sulphides (SMS) / Polymetallic Sulphides (Hydrothermal Vent Deposits)

- Cobalt-Rich Ferromanganese Crusts (CRCs) (Seamount Flank Deposits, 800–2,500m)

- Marine Phosphorite Deposits (Continental Shelf & Slope, 200–500m)

- Rare Earth Element (REE) Rich Deep-Sea Sediments

- Marine Placer Deposits (Gold, Diamonds & Heavy Mineral Sands, Shallow Water)

- Market Size & Forecast by Technology / Equipment

- Seafloor Mining Robots & Crawler Collection Systems

- Remotely Operated Vehicles (ROVs) for Mining Operations

- Autonomous Underwater Vehicles (AUVs) for Exploration & Survey

- Hydraulic Pump & Air-Lift Riser Systems

- Production Support Vessels (PSVs) & Offshore Surface Processing Ships

- Subsea Processing & Beneficiation Systems

- Cutting, Fragmentation & Collection Head Tools

- Subsea Communication, Power Transmission & Control Systems

- Market Size & Forecast by Operation Phase

- Exploration & Prospecting Phase

- Resource Assessment & Pilot / Test Mining Phase

- Commercial Production Phase

- Decommissioning & Site Remediation Phase

- Market Size & Forecast by Water Depth

- Shallow Water (Up to 200m): Marine Placer & Phosphorite Deposits

- Mid-Water (200–1,500m): Phosphorite, SMS & Shallow CRC Deposits

- Deep Water (1,500–3,500m): SMS, CRC & Seamount Deposits

- Ultra-Deep Water (Above 3,500m): Polymetallic Nodules, CRC & REE Sediments

- Market Size & Forecast by Target Mineral

- Manganese

- Nickel

- Copper

- Cobalt

- Zinc

- Rare Earth Elements (REEs): Light & Heavy REEs

- Gold, Silver & Platinum Group Metals (PGMs)

- Lithium & Other Battery Minerals

- Phosphate

- Market Size & Forecast by End-Use Application of Extracted Minerals

- Battery & Energy Storage: EV & Stationary Battery Supply Chain (Ni, Co, Mn, Li)

- Electronics, Semiconductors & Clean Technology (Cu, REEs, Co)

- Steel & Specialty Alloys (Mn, Ni, Co, Cr)

- Renewable Energy Technologies (REEs for Magnets, Cu for Cables, Co for Turbines)

- Fertilisers & Agriculture (Phosphate, Mn)

- Aerospace, Defence & Advanced Manufacturing (REEs, Co, Ni, Ti)

- Market Size & Forecast by Project Location

- Clarion-Clipperton Zone (CCZ): Pacific Ocean International Waters (ISA Area)

- Mid-Atlantic Ridge & Atlantic Ocean Deposits

- Indian Ocean Deposits (Central Indian Ridge, Carlsberg Ridge)

- Pacific Ocean: National EEZ Projects (Cook Islands, Kiribati, Tonga, PNG, Fiji)

- Arctic Ocean & Norwegian EEZ Deposits

- Other National EEZ Deposits (Japan, China, South Korea, New Zealand, Mexico)

- Market Size & Forecast by End-User

- Integrated Mining & Metals Majors with Deep Sea Mining Subsidiaries

- Independent Deep Sea Mining Operators & Development Companies

- State-Owned Enterprises (SOEs) with National Deep Sea Mining Programmes

- Technology, Equipment & Marine Service Providers

- Market Size & Forecast by Sales Channel

- Direct Resource Development & Mine Operation Contracts

- Joint Ventures, Sponsoring State Partnerships & ISA Contract Holders

- Technology Licensing, Equipment Supply & Marine Service Contracts

- State-Sponsored Research & National Programme Funding

- North America Deep Sea Mining Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Resource Type

- By Technology / Equipment

- By Operation Phase

- By Water Depth

- By Target Mineral

- By End-Use Application

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Deep Sea Mining Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Resource Type

- By Technology / Equipment

- By Operation Phase

- By Water Depth

- By Target Mineral

- By End-Use Application

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Deep Sea Mining Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Resource Type

- By Technology / Equipment

- By Operation Phase

- By Water Depth

- By Target Mineral

- By End-Use Application

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Deep Sea Mining Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Resource Type

- By Technology / Equipment

- By Operation Phase

- By Water Depth

- By Target Mineral

- By End-Use Application

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Deep Sea Mining Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Resource Type

- By Technology / Equipment

- By Operation Phase

- By Water Depth

- By Target Mineral

- By End-Use Application

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Deep Sea Mining Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Resource Type

- By Technology / Equipment

- By Operation Phase

- By Water Depth

- By Target Mineral

- By End-Use Application

- By Country

- By Sales Channel

- Market Size & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, United Kingdom, Norway, Germany, France, Japan, South Korea, China, India, Australia, New Zealand, Cook Islands, Papua New Guinea, Kiribati, Tonga, Fiji, Nauru, Jamaica, Mexico, Brazil, Chile, South Africa

- Technology Landscape & Innovation Analysis

- Seafloor Mining Robot & Crawler System Technology Deep-Dive

- Seafloor Crawler Design for Abyssal & Seamount Operations: Track System, Buoyancy Control, Sediment Plume Minimisation & Payload Capacity for 6,000m+ Depth Rating

- Nodule Collection Head Technology: Hydraulic Suction, Mechanical Pick-Up & Pre-Screening System Design for Polymetallic Nodule Size Fraction Optimisation

- SMS Cutting & Fragmentation Tool Technology: Drum Cutter, Disc Cutter & Water Jet Cutting Head Design for Massive Sulphide Ore Breakage at Hydrothermal Vent Sites

- CRC Scraper & Crust Harvesting Tool Technology: Bucket Wheel, Chain Cutter & Selective Thickness Control Design for Cobalt-Rich Crust Recovery from Seamount Flanks

- Hydraulic Pump & Air-Lift Riser System Technology: Centrifugal & Positive Displacement Pump Selection, Slurry Transport Modelling & Buffer Station Design for Ultra-Deep Lifting

- Remotely Operated Vehicle (ROV) & Autonomous Underwater Vehicle (AUV) Technology

- Production Support Vessel (PSV), Offshore Processing Ship & Marine Logistics Technology

- Subsea Processing, Beneficiation & Pre-Concentration Technology

- Subsea Power Transmission, Communication & Control System Technology

- Environmental Monitoring, Sediment Plume Tracking & Benthic Impact Assessment Technology

- Digital Twin, Simulation, AI-Based Navigation & Autonomous Seafloor Operations Technology

- Patent & IP Landscape in Deep Sea Mining Technologies

- Seafloor Mining Robot & Crawler System Technology Deep-Dive

- Value Chain & Supply Chain Analysis

- Exploration, Prospecting, Geophysical Survey & Resource Assessment Supply Chain

- Deep Sea Mining Equipment, ROV, AUV & Crawler Manufacturer Supply Chain

- Production Support Vessel, Marine Contractor & Offshore Service Supply Chain

- Riser System, Subsea Processing & Beneficiation Technology Supply Chain

- Onshore Processing, Hydrometallurgical Refining & Metals Marketing Supply Chain

- ISA Licensing, Sponsoring State Governance & Regulatory Compliance Channel

- Environmental Monitoring, Marine Science, Remediation & Circular Economy

- Pricing Analysis

- Polymetallic Nodule Extraction, Lifting & Onshore Processing Cost Analysis

- Seafloor Massive Sulphide (SMS) Mining & Metallurgical Processing Cost Analysis

- Cobalt-Rich Ferromanganese Crust (CRC) Mining Cost Analysis

- Deep Sea Mining Equipment & Technology Capital Cost Analysis

- Marine Phosphorite & REE Sediment Extraction Cost Analysis

- Total Project Economics, Internal Rate of Return (IRR) & Breakeven Commodity Price vs. Terrestrial Mining Benchmark

- Sustainability & Environmental Analysis

- Environmental Impact Assessment (EIA) of Deep Sea Mining: Benthic Disturbance, Habitat Destruction & Species Loss Risk

- Sediment Plume Dispersion, Water Column Impact & Benthic Recovery Rate Analysis

- Carbon Footprint & Energy Intensity of Deep Sea Mining vs. Terrestrial Mining Alternatives

- International Environmental Governance, Precautionary Principle & Moratorium Advocacy Impact

- Social Licence, Stakeholder Opposition Management & Pacific Island Community Engagement

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Concentrated by Resource Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Resource Type, Operation Phase & Geography

- Player Classification

- Integrated Mining & Metals Majors with Deep Sea Mining Subsidiaries or Strategic Interests

- Independent Deep Sea Mining Operators & Resource Development Companies

- State-Owned Enterprises (SOEs) with National Deep Sea Mining Exploration Programmes

- ISA Contract Holders & Sponsoring State Programme Operators

- Deep Sea Mining Equipment, ROV & Crawler Technology Manufacturers

- Marine Survey, Geophysical & Seafloor Mapping Service Providers

- Offshore Marine Contractors, PSV Operators & Subsea Engineering Companies

- Environmental Monitoring, Marine Science & Deep Sea Research Institutions

- Competitive Analysis Frameworks

- Market Share Analysis by Resource Type, Operation Phase & Region

- Company Profile

- Company Overview & Headquarters

- Deep Sea Mining Resource Portfolio, ISA Contracts & EEZ Licence Holdings

- Key Customer & Offtake Partner Relationships

- Operational Footprint, Vessel Fleet & Technology Assets

- Revenue (Deep Sea Mining Segment) & Project Investment Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Exploration Results, Pilot Tests, Regulatory Milestones)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Resource Quality vs. Technology Readiness Level)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Resource Type, Technology, Target Mineral, End-Use Application & Geography

- White Space Opportunity Analysis

- Strategic Output

- Strategic Recommendations

- Resource Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Licence Acquisition Strategy

- Customer, Offtake Partner & End-Use Industry Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability, Environmental Stewardship & Social Licence Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025–2028)

- Mid-term (2029–2032)

- Long-term (2033–2037)