Market Definition

The South-East Asia Epichlorohydrin Market encompasses the production, import, trade, and downstream consumption of epichlorohydrin monomer and its principal derivative chemical systems across the industrial economies of Thailand, Indonesia, Malaysia, Vietnam, Singapore, the Philippines, and neighboring ASEAN member states. Epichlorohydrin, also known as 1-chloro-2,3-epoxypropane with the chemical formula C3H5ClO, is a highly reactive bifunctional organic compound combining an epoxide ring and a chloromethyl group that impart exceptional cross-linking and chemical modification versatility, making ECH an indispensable reactive intermediate for synthesizing epoxy resins through its condensation reaction with bisphenol A or other polyhydric phenols, and for manufacturing synthetic glycerin, epichlorohydrin rubber, water treatment resins, ion exchange resins, and textile auxiliary chemicals across the chemical process industries of the region.

The market encompasses epichlorohydrin production through the conventional allyl chloride-based propylene chlorination route and through the bio-based glycerin-to-ECH route utilizing crude glycerin co-produced from the region’s substantial palm oil and biodiesel manufacturing industries as a renewable feedstock input; the downstream conversion of ECH into liquid and solid bisphenol A epoxy resins, novolac epoxy resins, and specialty epoxy systems serving the electronics, coatings, adhesives, wind energy, construction, and marine sectors; and the production of ECH-derived non-epoxy resin products including epichlorohydrin-dimethylamine water treatment polymers, epichlorohydrin rubber for sealing and hose applications, ECH-based cationic starch and paper wet-strength resins, and glycerin purification products. Key participants include integrated petrochemical producers operating ECH production units, bio-based ECH producers utilizing glycerin feedstock from oleochemical refining, epoxy resin manufacturers converting ECH into derivative resin products, specialty chemical companies formulating ECH-based water treatment and textile auxiliary products, and the diverse industrial end-user community spanning electronics manufacturing, construction, marine, automotive, and renewable energy sectors whose manufacturing activity defines the consumption volume and value structure of the South-East Asian ECH market. The market is significantly influenced by the region’s abundant palm oil-derived glycerin production capacity, the electronics manufacturing growth of Vietnam, Malaysia, and Thailand, and the wind energy composite manufacturing investments transforming the regional epoxy resin demand profile.

Market Insights

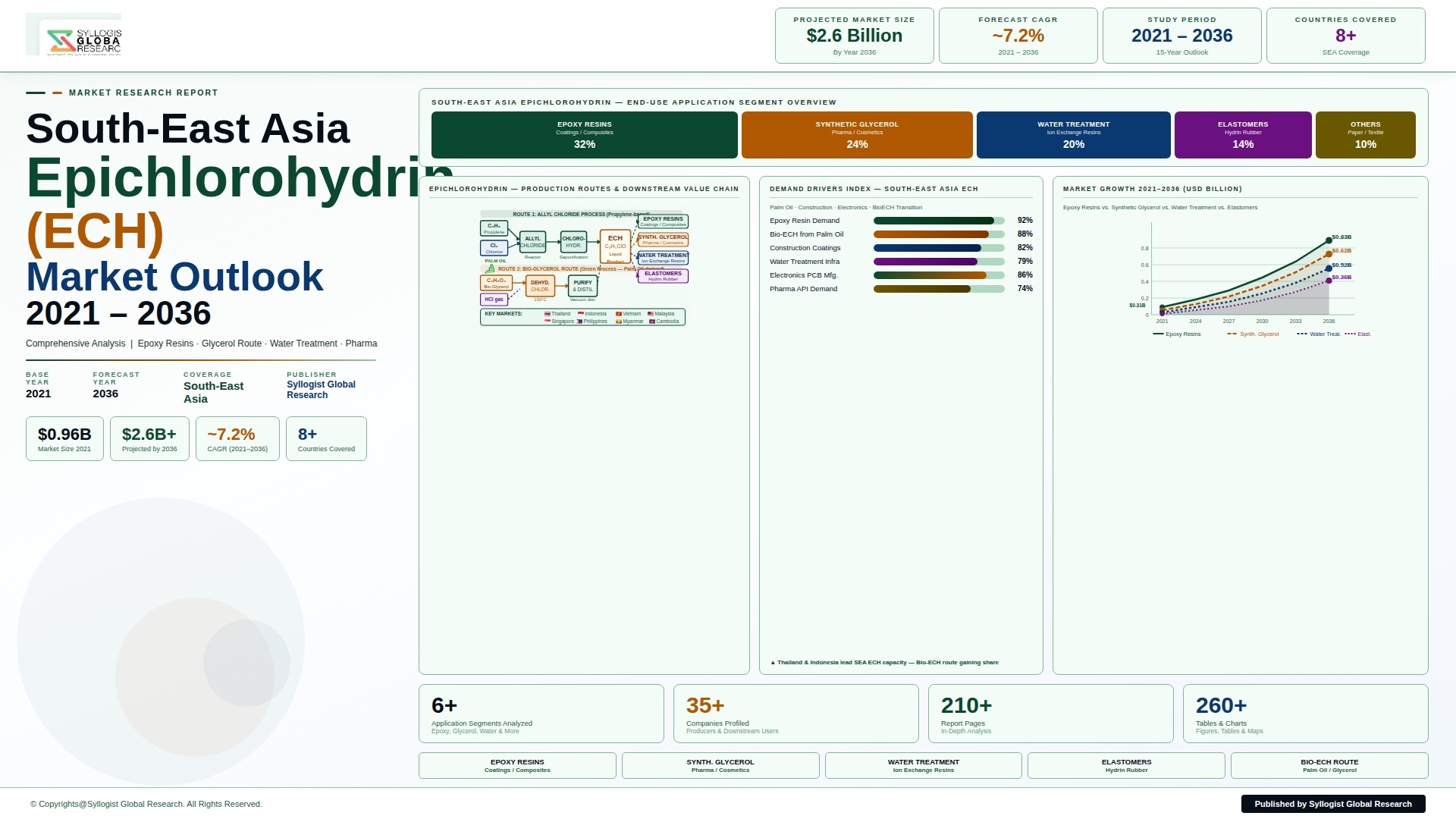

The South-East Asia epichlorohydrin market is positioned at the intersection of two structurally significant regional advantages: the world’s most abundant and cost-competitive supply of bio-based glycerin feedstock derived from the region’s dominant palm oil and coconut oil processing industries, and the rapidly industrializing manufacturing economies of Vietnam, Thailand, Malaysia, and Indonesia whose expanding electronics assembly, construction, automotive, and renewable energy sectors generate growing consumption of ECH-derived epoxy resins, water treatment chemicals, and specialty polymer systems. The South-East Asia epichlorohydrin market was valued at approximately USD 820 million in 2025 and is projected to reach USD 1.45 billion by 2034, advancing at a compound annual growth rate of 6.5% over the forecast period from 2027 to 2034, driven by the accelerating deployment of wind energy composite manufacturing capacity in Vietnam, Thailand, and the Philippines whose epoxy resin-intensive blade production generates growing ECH demand, the electronics manufacturing expansion of Vietnam and Malaysia attracting printed circuit board laminate producers requiring ECH-derived tetrabromobisphenol A and standard epoxy resin inputs, and the progressive commercial development of bio-based ECH production using the region’s low-cost glycerin surplus as a competitive feedstock advantage over conventional propylene-based ECH production routes whose costs are governed by global petrochemical feedstock price dynamics.

The epoxy resin segment constitutes the dominant downstream application for ECH in South-East Asia, consuming approximately 68% of total regional ECH output in 2025, and is itself experiencing a structural demand transformation driven by the region’s rapidly expanding wind energy manufacturing sector whose blade composite and nacelle component epoxy resin requirements are growing at rates substantially above the broader epoxy resin market. Vietnam has emerged as the most commercially dynamic ECH and epoxy resin market in South-East Asia, driven by its aggressive renewable energy expansion program that targets 70 gigawatts of wind and solar capacity by 2030 and has attracted substantial foreign direct investment in wind turbine manufacturing, blade production, and composite component fabrication facilities from European, Chinese, and South Korean manufacturers who require local epoxy resin supply chains of adequate quality and volume reliability to support their production operations. Thailand’s Rayong and Map Ta Phut industrial estate petrochemical clusters host the most developed ECH and epoxy resin production infrastructure in South-East Asia, with Dow Chemical’s epoxy resin facility, IRPC’s integrated petrochemical complex, and the downstream epoxy formulation operations of regional specialty chemical producers providing a commercially established regional supply base that serves export markets across the ASEAN region and supports Thailand’s domestic automotive, construction, and electronics manufacturing sectors. The electrical and electronic laminate segment, representing the largest single epoxy resin application category in value terms across the South-East Asian market, benefits from the concentration of printed circuit board manufacturing in Malaysia, Vietnam, and Thailand, where the epoxy resin-fiberglass laminate FR-4 material used in PCB substrate fabrication generates consistent and technically demanding ECH-derived epoxy resin consumption whose quality specifications and volume regularity provide stable commercial foundations for regional epoxy resin producers serving electronics sector customers.

The bio-based epichlorohydrin segment represents the most structurally distinctive and commercially strategic dimension of the South-East Asia ECH market, driven by the region’s unique position as the world’s largest producer of palm oil-derived crude glycerin whose abundance, low cost, and strategic availability as a bio-based ECH feedstock create a competitive manufacturing cost advantage for South-East Asian bio-based ECH producers that no other global region can replicate at equivalent scale. Palm oil refining in Indonesia and Malaysia generates approximately 8 to 10% of processed oil weight as crude glycerin co-product, and the combined palm oil processing industry of Indonesia and Malaysia produces in excess of 1.5 million metric tonnes of crude glycerin annually that is available at distressed prices relative to petrochemical propylene glycol alternatives when glycerin market oversupply conditions prevail, creating periods of exceptionally favorable raw material economics for bio-based ECH production that improve the competitiveness of the glycerin-to-ECH route versus conventional allyl chloride-based ECH synthesis. Solvay’s bio-based ECH production at its Taixing China facility demonstrated the commercial viability of the Epicerol process using glycerin feedstock, and the potential localization of bio-based ECH production within South-East Asia using Indonesian and Malaysian glycerin represents a commercially compelling investment opportunity that several regional chemical industry developers have evaluated, though actual commercial deployment within the region remains limited relative to the theoretical feedstock availability advantage. The quality and cost trajectory of palm-derived glycerin as an ECH feedstock is influenced by the biodiesel policy frameworks of Indonesia and Malaysia, whose mandatory biodiesel blending programs generating glycerin co-product volumes create a policy-linked feedstock supply dynamic that both supports bio-based ECH economics and introduces volumetric volatility tied to biodiesel production levels rather than ECH-specific market fundamentals.

From a competitive supply perspective, the South-East Asian ECH market is predominantly supplied through imports from China, Japan, South Korea, and European producers given the limited domestic ECH production capacity within the region outside Thailand’s integrated petrochemical complex infrastructure, creating a structural import dependency that exposes regional ECH consumers to international shipping logistics costs, supply chain disruption risks, and price dynamics governed by the production economics and capacity utilization of East Asian ECH producers rather than South-East Asian regional market conditions. China’s ECH production capacity, which reached approximately 850,000 metric tonnes per year in 2025 and accounts for approximately 45% of global ECH production, positions Chinese producers as the dominant ECH supply source for South-East Asian industrial consumers, with export pricing from Chinese ECH producers influenced by domestic demand cycles, environmental compliance cost escalation from China’s chemical industry regulatory tightening, and trade freight economics that create periodic supply cost volatility for regional ECH importers. The water treatment chemical segment, encompassing ECH-derived cationic polyamine flocculants and polyamidoamine-epichlorohydrin wet-strength resins used in municipal water treatment, industrial effluent treatment, and paper manufacturing applications across South-East Asia’s rapidly expanding industrial water management infrastructure, represents a growing secondary ECH consumption market whose demand is closely correlated with the industrial wastewater treatment capacity expansion being driven by environmental regulatory enforcement intensification in Thailand, Vietnam, Indonesia, and Malaysia. Singapore’s advanced specialty chemical industry, while not a primary ECH producer, serves as a regional commercial and technical hub for epoxy resin formulation, specialty coating development, and ECH-derivative specialty chemical distribution, whose sophisticated chemical industry infrastructure and free trade logistics position create a commercially important demand and distribution node within the broader South-East Asian ECH market ecosystem.

Key Drivers

South-East Asia Wind Energy Expansion and Electronics Manufacturing Growth Generating Structural Epoxy Resin and ECH Demand Across the Region

The structural transformation of South-East Asia’s energy mix toward renewable sources, driven by nationally binding renewable energy targets across Vietnam, Thailand, Indonesia, Malaysia, and the Philippines that collectively aim to install over 150 gigawatts of new wind and solar capacity by 2035, is generating a rapidly growing and commercially consequential epoxy resin demand stream from wind turbine blade manufacturing, composite nacelle component fabrication, and power infrastructure cable and transformer insulation applications that require ECH-derived epoxy resin systems whose performance in fatigue resistance, moisture barrier, and UV stability under tropical climate conditions is the critical material selection criterion for renewable energy infrastructure applications in the South-East Asian operating environment. Vietnam’s offshore wind energy program, whose 6 gigawatt offshore development target by 2030 has attracted Vestas, Siemens Gamesa, and MHI Vestas manufacturing investment in blade and composite component production facilities that require locally sourced epoxy resin inputs, represents a commercially catalytic demand development whose supply chain localization imperatives are driving ECH and epoxy resin capacity investment evaluation within Vietnam and neighboring Thailand. The continued growth of electronics manufacturing across Vietnam, Malaysia, and Thailand, where Samsung, Intel, Foxconn, and hundreds of semiconductor and electronic component suppliers operate production facilities generating consistent PCB laminate and electronics enclosure epoxy resin demand, provides a stable and technically demanding ECH consumption base that complements the more cyclically variable renewable energy and construction sector demand to create a commercially diversified ECH demand structure with multiple growth drivers operating across different industry cycles and investment timelines.

Abundant Bio-Based Glycerin Feedstock From Regional Palm Oil Industry Creating Structural Cost Competitive Advantage for ECH and Epoxy Resin Production

South-East Asia’s position as the producer of approximately 85% of the world’s palm oil, generating over 1.5 million metric tonnes of crude glycerin annually as an unavoidable co-product of palm oil refining and biodiesel production in Indonesia and Malaysia alone, creates a structural raw material cost advantage for bio-based ECH production within the region that is unique globally and that provides the feedstock economics foundation for a competitive domestic ECH manufacturing industry whose production costs can be structurally below those of conventional propylene-based ECH production at times of glycerin market oversupply that depress crude glycerin prices to levels well below their theoretical conversion value to ECH. The Indonesian and Malaysian government mandatory biodiesel blending programs, which require B35 and B20 blending ratios respectively as of 2025 and are subject to upward revision toward B40 and B30 targets in their respective national energy transition policies, generate glycerin co-product volumes that are structurally linked to national biodiesel policy implementation intensity and that can represent either abundant low-cost feedstock opportunity or market-depressing oversupply depending on the relative pace of glycerin demand growth from ECH production, food ingredient, personal care, and pharmaceutical applications in the regional market. The strategic alignment between South-East Asia’s palm oil industry sustainability certification requirements under RSPO and MSPO frameworks and the bio-based ECH production pathway’s renewable feedstock credentials creates a potential commercial premium positioning for certified bio-based ECH and its downstream epoxy resin derivatives in sustainability-conscious end markets including European offshore wind infrastructure procurement, premium marine coating applications, and multinational electronics company supply chain sustainability programs that are progressively requiring bio-based content documentation from their specialty chemical material suppliers.

Infrastructure Development Programs and Construction Sector Growth Across ASEAN Economies Driving Protective Coating and Adhesive Epoxy Demand

The ambitious infrastructure investment programs of major South-East Asian economies, encompassing Indonesia’s capital relocation and Nusantara development program targeting over USD 30 billion in infrastructure investment, Vietnam’s National Transport Development Strategy requiring USD 24 billion in road, rail, and port infrastructure, Thailand’s Eastern Economic Corridor infrastructure development, and the Philippines’ Build Better More infrastructure program, are generating substantial and growing demand for ECH-derived epoxy resin protective coatings, concrete repair and rehabilitation compounds, structural adhesives, and construction chemical systems whose application in steel structure corrosion protection, concrete surface treatment, bridge deck waterproofing, and infrastructure grouting and anchoring is directly proportional to the construction investment volumes being deployed across regional infrastructure programs. The tropical climate conditions of South-East Asia, characterized by high ambient temperature and humidity, marine salt spray exposure in coastal infrastructure environments, and intense UV radiation that accelerate the degradation of conventional organic protective coatings, create particularly demanding performance requirements for infrastructure protective coating systems that favor the superior chemical resistance, moisture barrier performance, and adhesion strength of ECH-derived epoxy coating formulations over alternative coating chemistries at technically justified premium price points. Marine infrastructure development including port expansion at Jakarta, Ho Chi Minh City, Klang, and Singapore, offshore oil and gas platform installation, and the growing South-East Asian shipbuilding industry in Vietnam, Indonesia, and the Philippines generate growing demand for marine-grade epoxy coating systems whose biocidal fouling control and corrosion protection performance in continuous seawater exposure environments represent technically demanding and commercially premium ECH-derived epoxy resin applications generating higher value per kilogram of ECH consumed than commodity industrial coating applications.

Key Challenges

Limited Regional ECH Production Capacity and Import Dependency Exposing South-East Asian Consumers to Supply Chain Disruption and Pricing Volatility

The South-East Asian ECH market’s structural dependence on imports from Chinese, Japanese, and Korean ECH producers to satisfy the majority of regional consumption requirements creates a commercially significant supply chain vulnerability whose manifestation in episodic supply disruptions, price spikes driven by East Asian production outages, and freight cost escalation during ocean shipping market tightening periods has repeatedly challenged the production planning, inventory management, and cost structure of South-East Asian epoxy resin manufacturers and ECH-derivative chemical producers whose manufacturing operations and customer commitments require consistent and cost-stable ECH availability. The geographic concentration of global ECH production at a limited number of large integrated chlorine-propylene manufacturing complexes in China, Germany, Thailand, and Japan creates a supply network whose resilience is vulnerable to simultaneous adverse events affecting multiple production sites, as demonstrated during the 2021 Texas freeze and the 2022 European energy cost crisis that each disrupted chlorine and ECH production at key supply sources and generated price spikes of 40% to 80% that propagated through the ECH-epoxy resin value chain into regional end-use markets within weeks of the initial supply constraint event. The investment required to establish integrated ECH production capacity within South-East Asia capable of displacing a meaningful proportion of current import volumes involves capital commitments of USD 150 million to USD 400 million for a world-scale ECH unit including chlorine and allyl chloride upstream integration, creating capital access and project development complexity barriers that have deterred domestic ECH capacity investment despite the commercial logic of import substitution at the current regional consumption scale.

Environmental Regulatory Tightening Governing ECH Handling, Storage, and Wastewater Treatment Increasing Compliance Costs Across the Value Chain

Epichlorohydrin is classified as a probable human carcinogen by the International Agency for Research on Cancer and as a hazardous substance under the chemical safety regulations of Thailand, Singapore, Malaysia, Vietnam, and Indonesia, imposing stringent occupational health and safety requirements, environmental discharge limits, hazardous substance handling and storage obligations, and manufacturing facility inspection and audit requirements on ECH producers, downstream epoxy resin manufacturers, and industrial consumers whose ECH handling operations generate compliance cost burdens that are increasing as regional environmental enforcement intensification progresses across South-East Asian regulatory jurisdictions. The ECH-containing wastewater streams generated by epoxy resin synthesis, ECH rubber vulcanization, and water treatment resin manufacturing operations require dedicated chemical treatment to destroy or remove ECH and its chlorinated degradation products before discharge to municipal sewer or receiving water bodies, and the capital and operating cost of compliant ECH wastewater treatment systems represents a meaningful addition to manufacturing operating cost for smaller epoxy resin and specialty chemical producers whose treatment system investment requirements are disproportionate relative to production scale. Thailand’s Hazardous Substance Act and its implementing Ministerial Notifications governing ECH import, use, and disposal, Singapore’s National Environment Agency requirements for toxic industrial waste management, and Vietnam’s Chemical Law implementing regulations have each tightened compliance requirements for ECH-handling operations over the past five years through more stringent emission reporting, worker exposure monitoring, and emergency response planning obligations that add regulatory administration cost and management attention requirements to ECH handling operations across the regional value chain.

Glycerin Feedstock Quality Inconsistency and Price Volatility Constraining Bio-Based ECH Production Economics and Commercial Reliability

The commercial viability of bio-based ECH production using palm oil-derived crude glycerin as a feedstock is highly sensitive to crude glycerin quality consistency and price stability, and both parameters are subject to significant variability arising from the diverse and fragmented structure of the South-East Asian palm oil refining and biodiesel production industry, where hundreds of small and medium-scale mills and refineries produce crude glycerin of highly variable purity, water content, salt content, and organic impurity profiles that require costly purification pre-treatment before the glycerin achieves the refined glycerin specification required for ECH synthesis reactor feed. Crude glycerin from biodiesel production typically contains 75% to 90% glycerol content alongside methanol, soap, water, and residual fatty acid methyl ester impurities whose removal through distillation and chemical treatment adds USD 80 to USD 150 per metric tonne of processing cost to the delivered cost of ECH-grade refined glycerin, substantially reducing the feedstock cost advantage of the bio-based route relative to petrochemical propylene-based ECH production particularly during periods when propylene prices are moderate and glycerin purification costs are elevated by feedstock quality degradation. The glycerin price cycle is driven by the interaction of palm oil production volumes, biodiesel policy implementation intensity, and the relatively limited industrial demand base for glycerin in South-East Asian markets, creating price volatility episodes in which crude glycerin prices collapse to below USD 100 per metric tonne during periods of biodiesel production surge and recover to USD 250 to USD 400 per metric tonne when biodiesel program intensity reduces, generating bio-based ECH production economics that oscillate between highly competitive and marginally viable on a cycle that is governed by agricultural and energy policy dynamics rather than ECH market fundamentals.

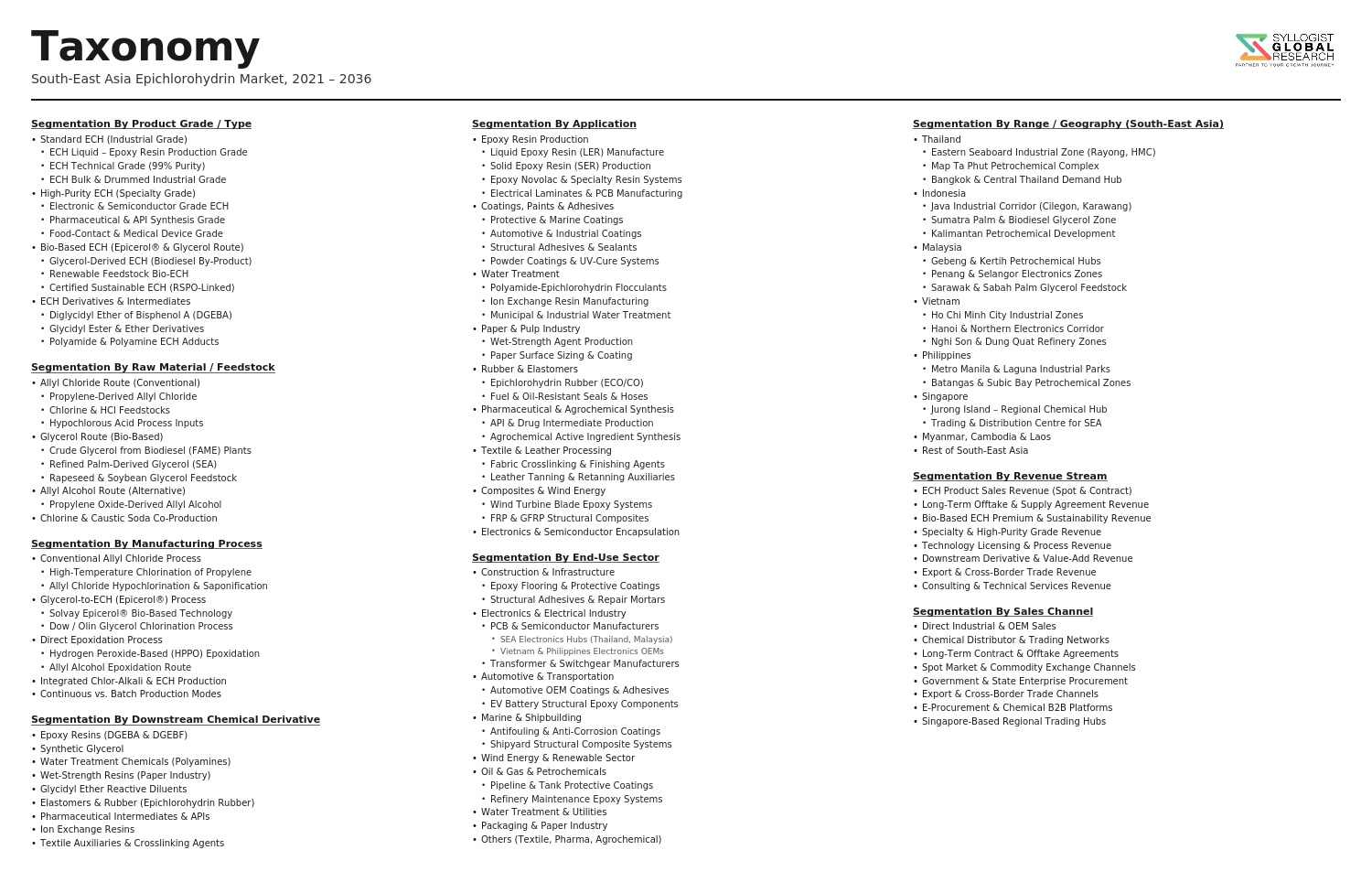

Market Segmentation

- Segmentation By Production Route

- Conventional Allyl Chloride-Based (Propylene Chlorination) ECH

- Bio-Based Glycerin-to-ECH (Epicerol and Similar Process Routes)

- Others

- Segmentation By Derivative Product

- Bisphenol A Liquid Epoxy Resin (Standard Grades)

- Bisphenol A Solid Epoxy Resin (Advanced Grades)

- Novolac and Specialty Epoxy Resins

- Epichlorohydrin Rubber (Hydrin Rubber)

- Water Treatment and Ion Exchange Polymers

- Paper Wet-Strength Resins (PAE Resins)

- Synthetic Glycerin and Pharmaceutical Glycerin

- Textile Auxiliary Chemicals

- Others

- Segmentation By End-Use Application

- Protective and Marine Coatings

- Electrical and Electronic PCB Laminates

- Wind Energy Blade and Composite Manufacturing

- Construction Adhesives, Grouts, and Flooring Systems

- Automotive Coatings and Adhesives

- Water and Wastewater Treatment Chemicals

- Paper and Pulp Processing Chemicals

- Aerospace and High-Performance Composite Structures

- Textile and Fiber Processing

- Others

- Segmentation By End-Use Industry

- Electronics and Electrical Manufacturing

- Construction and Infrastructure

- Renewable Energy (Wind and Solar)

- Marine and Shipbuilding

- Automotive and Transportation

- Oil and Gas and Industrial Processing

- Water Treatment and Environmental Services

- Pulp, Paper, and Packaging

- Textile and Apparel Manufacturing

- Others

- Segmentation By Supply Source

- Regional Domestic Production (Thailand, Indonesia)

- China Imports

- Japan and South Korea Imports

- European Imports (Solvay, Dow)

- Others

- Segmentation By Grade

- Technical Grade ECH

- Epoxy Resin Grade ECH

- Bio-Based Certified ECH

- High-Purity and Specialty Grade ECH

- Others

- Segmentation By Country

- Vietnam

- Thailand

- Indonesia

- Malaysia

- Singapore

- Philippines

- Rest of South-East Asia

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total market valuation of the South-East Asia Epichlorohydrin Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by production route, derivative product, end-use application, end-use industry, and country, to enable ECH producers, epoxy resin manufacturers, specialty chemical companies, and investment decision makers to identify which derivative segments and national markets will generate the highest absolute demand growth and the most commercially viable production and supply chain investment opportunities across the forecast period?

- What is the commercial and technical feasibility of establishing integrated bio-based ECH production capacity within South-East Asia using palm oil-derived glycerin feedstock from Indonesian and Malaysian refining industries, what capital investment, glycerin purification infrastructure, and process technology licensing requirements are associated with a viable commercial-scale bio-based ECH plant in the region, and at what crude glycerin price levels and ECH market prices does the bio-based production route achieve competitive parity with or advantage over conventional allyl chloride-based ECH production and imported ECH availability?

- How are the renewable energy manufacturing investment programs across Vietnam, Thailand, and the Philippines, specifically wind turbine blade fabrication, solar panel encapsulation, and power infrastructure composite component manufacturing, translating into incremental ECH and epoxy resin demand volumes by country and application segment through 2034, and which epoxy resin grades and performance specifications are required by offshore versus onshore wind blade manufacturers operating in South-East Asian tropical climate conditions?

- How is the competitive ECH supply landscape among Chinese exporters, Japanese and Korean producers, European specialty chemical companies, and the limited regional production base in Thailand evolving in terms of pricing dynamics, supply reliability, quality consistency, and strategic trade relationship development with South-East Asian epoxy resin manufacturers and industrial consumers, and what supply chain diversification strategies are regional ECH consumers implementing to manage import dependency risk and price volatility exposure through the forecast period?

- Who are the leading ECH producers supplying the South-East Asian market, the major epoxy resin manufacturers operating within the region including Dow Chemical Thailand, Aditya Birla Chemicals, Nan Ya Plastics, and regional epoxy formulators, the specialty chemical companies producing ECH-derived water treatment and paper chemical products, and the key industrial end users across electronics, construction, marine, and renewable energy sectors currently defining the commercial and competitive landscape of the South-East Asia ECH market, and what are their respective production capacities, technology sourcing arrangements, customer industry relationships, regional expansion plans, and strategic positioning in response to the structural growth opportunity and supply chain challenges characterizing the South-East Asian ECH value chain through the forecast period?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Propylene & Glycerol Feedstock Price Volatility & Supply Availability Risk for ECH Production in South-East Asia

- Import Competition from China & North-East Asia, Dumping Risk & Domestic Price Realisation Risk for Regional Producers

- Environmental Regulation, Chlorinated By-Product Waste Treatment & Effluent Compliance Risk in South-East Asia

- Epoxy Resin Demand Cyclicality, End-Use Industry Slowdown & ECH Demand Variability Risk

- Bio-Based ECH (Glycerol Route) Cost Competitiveness & Technology Adoption Risk vs. Conventional Propylene-Based ECH

- Regulatory Framework & Standards

- ASEAN Chemical Regulations, Industrial Chemical Notification & Registration Requirements Applicable to ECH Production & Use

- Thailand Chemical Hazard Labelling, Hazardous Substances Act & ECH Handling, Storage & Transportation Standards

- Indonesia Government Regulation on Hazardous Materials (B3), KLHK Environmental Permits & ECH Waste Disposal Requirements

- Vietnam Chemical Law, MONRE Environmental Regulations & ECH Classification & Control Framework

- Environmental, Health & Safety Standards: GHS Classification, REACH-Inspired National Frameworks & Worker Exposure Limits for ECH in South-East Asia

- South-East Asia Epichlorohydrin Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Metric Tonnes)

- Market Size & Forecast by Production Route

- Propylene-Based ECH (Chlorohydrin & Dichlorohydrin Process Route)

- Glycerol-Based Bio-ECH (Epicerol & Solvay HydrEcho Bio-Based Process Route)

- Allyl Chloride Intermediate Route

- Market Size & Forecast by Grade & Purity

- Industrial Grade ECH (Standard Purity for Epoxy Resin & General Applications)

- Electronic & High-Purity Grade ECH (For Advanced Epoxy Laminates & Semiconductor Applications)

- Bio-Based & Renewable Grade ECH

- Market Size & Forecast by Application

- Epoxy Resin Manufacturing (Liquid & Solid Epoxy, BPA-ECH & Non-BPA Epoxy Systems)

- Water Treatment Chemicals (Polyamine Coagulants & Ion Exchange Resin Synthesis)

- Synthetic Glycerol & Glycidol Production

- Pharmaceutical & Fine Chemical Intermediates

- Textile Finishing, Paper Wet-Strength Resin & Elastomer Applications

- Agrochemical Intermediate Production

- Flame Retardant & Specialty Chemical Manufacturing

- Market Size & Forecast by End-Use Industry

- Electrical & Electronics (PCB Laminates, Encapsulants & Semiconductor Packaging)

- Wind Energy & Composites (Blade Resin & Structural Adhesive)

- Automotive & Transportation

- Construction & Infrastructure (Flooring, Coatings & Civil Engineering Adhesives)

- Water Treatment & Environmental Management

- Marine & Offshore Coatings & Adhesives

- Packaging & Consumer Goods

- Pharmaceutical & Agrochemical Manufacturing

- Market Size & Forecast by End-User

- Epoxy Resin Manufacturers

- Water Treatment Chemical Producers

- Specialty Chemical & Fine Chemical Manufacturers

- Electrical Laminate & PCB Manufacturers

- Adhesive, Sealant & Coating Manufacturers

- Pharmaceutical & Agrochemical Producers

- Market Size & Forecast by Sales Channel

- Direct Producer-to-Downstream Manufacturer Supply

- Distributor, Stockist & Chemical Trading Company

- Long-Term Supply Contract & Toll Processing Arrangement

- Spot Market & Commodity Purchase

- Import via Authorised Agent & Trading House

- Thailand Epichlorohydrin Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Production Route

- By Application

- By End-Use Industry

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Indonesia Epichlorohydrin Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Production Route

- By Application

- By End-Use Industry

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Malaysia Epichlorohydrin Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Production Route

- By Application

- By End-Use Industry

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Vietnam Epichlorohydrin Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Production Route

- By Application

- By End-Use Industry

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Philippines, Singapore & Rest of South-East Asia Epichlorohydrin Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Production Route

- By Application

- By End-Use Industry

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Epichlorohydrin Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Production Route

- By Application

- By End-Use Industry

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- *Countries Analyzed in the Syllogist Global Research Portfolio: Thailand, Indonesia, Malaysia, Vietnam, Philippines, Singapore, Myanmar, Cambodia, Laos, Brunei, Timor-Leste

- Technology Landscape & Innovation Analysis

- Propylene Chlorohydrin Process Technology Deep-Dive: Chlorine Efficiency, By-Product Minimisation & ECH Yield Optimisation

- Bio-Based ECH (Glycerol Route) Technology: Solvay Epicerol, Dow HydrEcho & Emerging Catalytic Glycerol Chlorination Process

- Epoxy Resin Manufacturing Technology Using ECH: Liquid Epoxy (LER), Solid Epoxy (SER) & Advanced Formulation for South-East Asian Markets

- Water Treatment Polyamine & Polyamidoamine (PAMAM) Synthesis Technology Using ECH as Crosslinker

- Electronic-Grade ECH Purification Technology: Distillation, Ion Exchange & Ultra-High Purity Processing for PCB & Semiconductor Applications

- ECH Waste Stream Management Technology: Chlorinated Effluent Treatment, Calcium Chloride By-Product Valorisation & Zero Liquid Discharge

- Digital Process Control, Real-Time Analytics & AI-Driven Yield Optimisation Technology for ECH Production Plants

- Patent & IP Landscape in Epichlorohydrin & Bio-ECH Technologies Relevant to South-East Asia

- Value Chain & Supply Chain Analysis

- Propylene & Allyl Chloride Feedstock Production & Supply Chain in South-East Asia

- Glycerol Feedstock Supply Chain: Biodiesel Industry By-Product Availability in Thailand, Indonesia & Malaysia

- Chlorine & Caustic Soda (Chlor-Alkali) Supply Chain Supporting ECH Production in South-East Asia

- ECH Purification, Drumming, ISO Tank & Bulk Liquid Storage & Logistics Supply Chain

- Epoxy Resin Downstream Converter & Fabricator Procurement Channel

- Chemical Distributor, Stockist & Trading Company Channel in South-East Asia

- Waste Chlorinated By-Product Treatment, Calcium Chloride Recovery & Effluent Management Value Chain

- Pricing Analysis

- ECH Spot & Contract Price Benchmarking Across South-East Asian Markets: Thailand, Indonesia, Malaysia & Vietnam

- Propylene-Based vs. Glycerol-Based Bio-ECH Production Cost & Price Parity Analysis

- ECH Import Price vs. Regional Production Cost & Landed Cost Comparison in South-East Asia

- Electronic-Grade vs. Industrial-Grade ECH Price Premium & Specification Differential Analysis

- ECH-to-Epoxy Resin Price Spread & Downstream Margin Analysis for South-East Asian Producers

- Total ECH Cost-in-Use per Tonne of Epoxy Resin, Water Treatment Chemical & Specialty Chemical Produced

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of ECH Production Routes: Carbon Footprint, Energy Intensity, Chlorinated Waste Generation & Water Use Comparison

- Bio-Based ECH Sustainability Credentials: GHG Reduction, Renewable Feedstock & Circular Economy Benefits from Glycerol Valorisation

- Chlorinated By-Product & Effluent Management: Environmental Impact, Regulatory Compliance & Zero Liquid Discharge Solutions in South-East Asia

- ECH Contribution to Epoxy Resin Circular Economy: Recyclable Composite, Bio-Epoxy & Closed-Loop Resin Recycling Pathways

- Regulatory-Driven Sustainability, SDG 3 (Good Health), SDG 6 (Clean Water) & SDG 9 (Industry & Innovation) Alignment & ESG Disclosure Requirements

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Production Route & Country)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Production Route, Application & Country

- Player Classification

- Integrated Petrochemical & Chlor-Alkali Companies Producing ECH in South-East Asia

- Dedicated ECH Producers & Specialty Chemical Companies

- Bio-Based ECH Manufacturers Utilising Glycerol Feedstock

- Global ECH Majors with South-East Asia Supply & Distribution Operations

- Epoxy Resin Manufacturers with Backward Integration into ECH

- Chemical Distributors, Stockists & Trading Companies for ECH in South-East Asia

- Technology Licensors & Process Engineering Companies for ECH Production

- Water Treatment & Specialty Chemical Companies with ECH-Based Product Lines

- Competitive Analysis Frameworks

- Market Share Analysis by Production Route, Application & Country

- Company Profile

- Company Overview & Headquarters

- ECH Products, Grade Portfolio & Downstream Derivative Offerings

- Key Customer Relationships & Reference Accounts in South-East Asia

- Manufacturing Footprint & Production Capacity in South-East Asia

- Revenue (ECH & Derivatives Segment) & Order Book

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Capacity Expansion, Grade Launches, Bio-ECH Investment)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Production Scale vs. Product Portfolio Breadth)

- Key Company Profiles

- Market Structure & Concentration

- Strategic Opportunity Analysis

- Strategic Output

- Market Opportunity Matrix: By Production Route, Application, End-Use Industry, End-User & Country

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output