Market Definition

The Global Hydrogen-Based Iron Reduction Market encompasses the development, engineering, construction, operation, and commercial scaling of industrial process technologies that utilise hydrogen as the primary reductant in the conversion of iron ore to metallic iron, substituting the carbon-intensive coking coal and coke reductants used in conventional blast furnace ironmaking with hydrogen molecules that react with iron oxide at elevated temperatures to produce direct reduced iron and water vapour rather than the carbon dioxide emissions generated by incumbent carbon-based reduction pathways. The market covers the complete value chain from hydrogen production via water electrolysis using renewable electricity, steam methane reforming with carbon capture, or alternative low-carbon hydrogen generation routes, through hydrogen compression, storage, and pipeline or on-site supply infrastructure, to the direct reduction shaft furnace, fluidised bed reactor, or plasma-based reduction systems in which hydrogen reacts with iron ore pellets, lump ore, or iron ore fines to produce sponge iron or hot briquetted iron suitable for melting in electric arc furnaces for steel production. Product forms encompass cold direct reduced iron, hot direct reduced iron, hot briquetted iron, and the emerging category of hot direct reduced iron fed directly to electric arc furnaces or smelting reduction vessels as part of integrated green steelmaking process routes. Key participants include steel producers investing in decarbonisation technology programs, engineering contractors and process technology licensors developing hydrogen direct reduction reactor systems, electrolyser manufacturers and hydrogen production plant developers, iron ore mining companies investing in high-grade pellet feed production tailored to hydrogen reduction requirements, renewable energy developers supplying dedicated power to electrolysis operations, and the governments and multilateral institutions whose climate policy frameworks, carbon pricing mechanisms, and green hydrogen support programs are defining the commercial development timeline of this strategically critical industrial decarbonisation market.

Market Insights

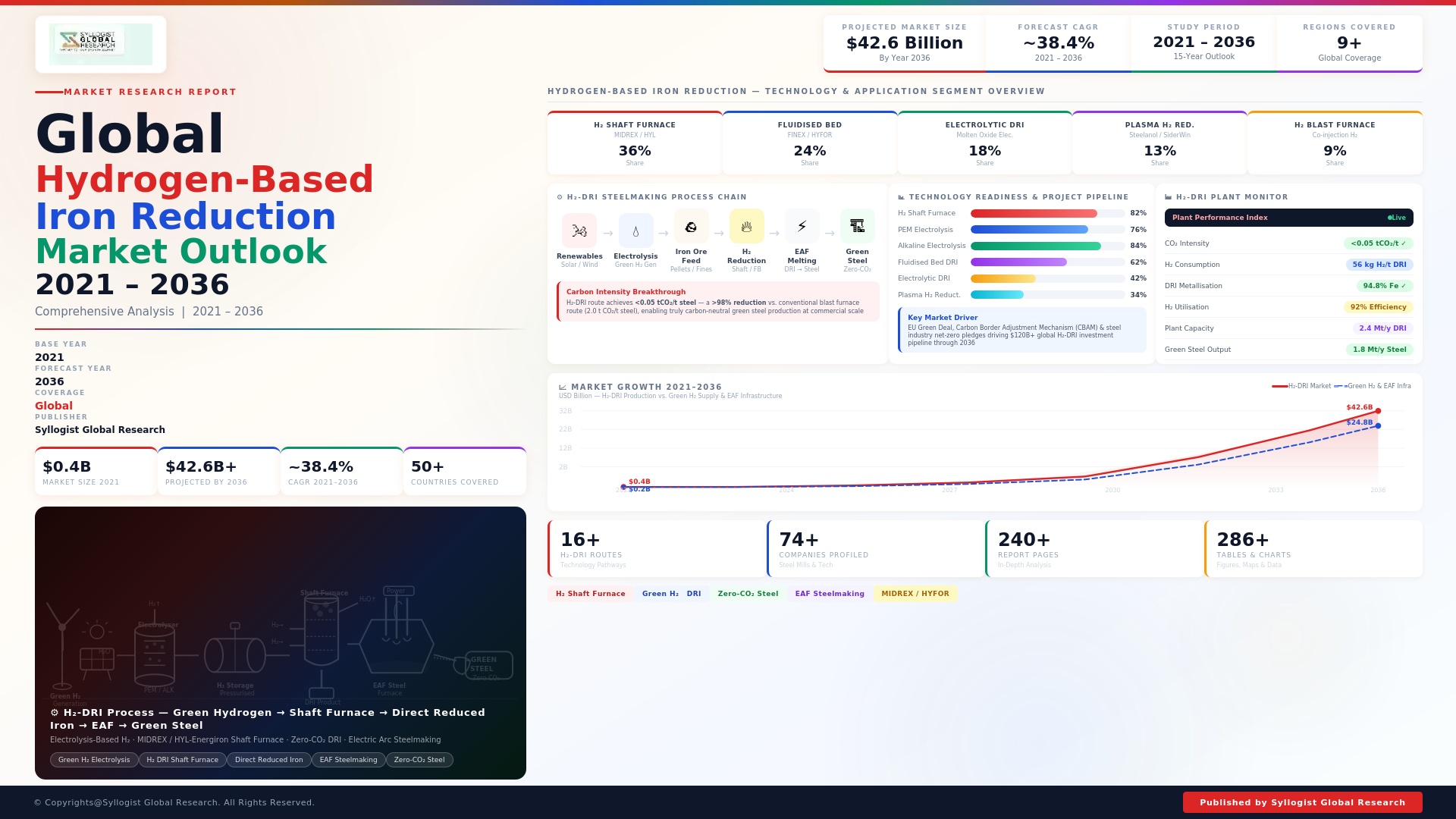

The global hydrogen-based iron reduction market was valued at approximately USD 2.1 billion in 2025 and is projected to reach USD 24.6 billion by 2034, advancing at a compound annual growth rate of 31.4% over the forecast period from 2027 to 2034, representing one of the highest growth rate trajectories among all heavy industrial decarbonisation market segments as the global steel industry accelerates investment in near-zero-emission production pathways to meet carbon reduction commitments, comply with emerging carbon border adjustment mechanisms, and respond to procurement requirements from automotive, construction, and consumer goods customers with Scope 3 emission reduction obligations. The steel industry is responsible for approximately 7% to 8% of global anthropogenic carbon dioxide emissions, producing approximately 1.85 metric tons of carbon dioxide per metric ton of crude steel via the dominant blast furnace-basic oxygen furnace route, and hydrogen-based direct reduction integrated with electric arc furnace steelmaking represents the most commercially credible large-scale decarbonisation pathway currently available, capable of reducing carbon dioxide emissions per metric ton of steel to below 0.1 metric tons when powered by renewable hydrogen, compared to the 0.4 to 0.6 metric tons achievable through optimised natural gas-based direct reduced iron and electric arc furnace routes and the 1.7 to 2.1 metric tons characteristic of blast furnace-based production.

The technology landscape of hydrogen-based iron reduction is evolving rapidly across three principal process architecture categories whose commercial development timelines, capital requirements, and operational performance envelopes differ materially and whose simultaneous progression is creating a competitive and complementary technology ecosystem rather than a single dominant pathway. Shaft furnace direct reduction technology, adapted from the commercially mature Midrex and Energiron natural gas direct reduced iron process platforms that collectively processed approximately 133 million metric tons of iron ore in 2025, is the nearest-term hydrogen reduction pathway, with multiple commercial-scale demonstration and early production projects having validated the operability of shaft furnaces on hydrogen-natural gas blend feedstocks containing up to 70% to 100% hydrogen by volume, providing a technologically de-risked migration path from existing natural gas direct reduced iron assets toward full hydrogen operation as green hydrogen supply costs decline. Fluidised bed reduction technology for iron ore fines, which eliminates the pelletisation step required for shaft furnace feed preparation and reduces the iron ore quality premium demanded by direct reduction processes, is advancing through pilot and demonstration scale programs with projected commercial-scale deployments from 2028 to 2030 offering the potential to broaden the iron ore feed specifications compatible with hydrogen reduction and reduce the raw material cost premium relative to blast furnace ironmaking. Plasma-based hydrogen iron reduction, which uses hydrogen plasma at temperatures exceeding 3,000 degrees Celsius to reduce iron ore without requiring pelletisation or the thermal efficiency constraints of conventional shaft furnace operation, is advancing through pilot scale development and represents a longer-term but potentially transformative pathway for processing lower-grade iron ore feeds and generating liquid iron product directly rather than solid direct reduced iron requiring subsequent electric arc furnace remelting.

Europe is the most advanced regional market for hydrogen-based iron reduction investment and policy development, driven by the European Union Emissions Trading System carbon price that reached approximately USD 68 per metric ton of carbon dioxide in 2025, the Carbon Border Adjustment Mechanism applying to steel imports from 2026, national green hydrogen support programs in Sweden, Germany, the Netherlands, Spain, and France, and the strategic decarbonisation investment programs of European integrated steel producers who collectively committed over USD 38 billion to green steel transition projects between 2021 and 2025. Sweden’s Hybrit project, a joint venture involving a major steel producer, an iron ore mining company, and a state-owned energy company, achieved commercial-scale demonstration of full hydrogen shaft furnace direct reduced iron production and electric arc furnace steelmaking by 2024, establishing the world’s first industrial proof-of-concept for green hydrogen-based steelmaking and providing the technical validation basis for the commercial-scale plant investment decisions being made by steel producers across Europe, the Middle East, and Asia-Pacific. The Middle East is emerging as a strategically significant hub for green and blue hydrogen-based iron reduction investment, with Saudi Arabia, the United Arab Emirates, Oman, and Bahrain pursuing integrated green hydrogen production and hydrogen direct reduced iron export strategies that leverage the region’s exceptional solar and wind energy resources, low-cost electricity generation economics, existing iron ore import infrastructure, and geographic positioning between European and Asian steel markets to develop export-oriented hydrogen-reduced iron production that supplies decarbonised iron feedstock to electric arc furnace steelmakers lacking access to low-cost domestic renewable energy.

Green hydrogen cost reduction is the single most consequential variable governing the commercial scaling timeline of the global hydrogen-based iron reduction market, with the delivered cost of green hydrogen to direct reduction plant gate representing the largest operating cost component of hydrogen-based steelmaking and the critical economic threshold that determines the price premium of green steel relative to blast furnace-produced steel at prevailing carbon prices. Green hydrogen production costs at the electrolysis plant gate declined from approximately USD 5.5 to USD 7.0 per kilogram in 2021 to approximately USD 3.2 to USD 5.0 per kilogram in 2025 as electrolyser capital costs fell by approximately 35% and utility-scale renewable energy costs continued their long-term decline trajectory, with further reduction to USD 1.5 to USD 2.5 per kilogram projected by 2030 in regions with the most favourable renewable energy resources including the Middle East, North Africa, Australia, Chile, and parts of the United States. The iron ore pellet quality requirement for hydrogen shaft furnace reduction, which demands iron content above 67% and very low levels of gangue minerals including silica, alumina, and phosphorous, is creating a structural demand premium for high-grade iron ore pellet feed that is reshaping iron ore market segmentation and incentivising mining capital investment in high-grade magnetite and itabirite concentrate production in Australia, Brazil, Canada, and the Nordic nations whose ore characteristics and beneficiation capabilities are best suited to producing the pellet feed specifications demanded by hydrogen reduction plant operators at the commercial scale required to support the green steel transition.

Key Drivers

Carbon Pricing, Carbon Border Adjustment Mechanisms, and Green Steel Procurement Requirements Creating Commercial Pull for Hydrogen-Based Iron Reduction Investment

The progressive tightening of carbon pricing and carbon trade regulation across major steel-consuming economies is transforming the economics of hydrogen-based iron reduction from a green premium technology into an increasingly commercially competitive production pathway whose total cost of production, including carbon cost obligations, is converging toward parity with blast furnace steelmaking in high carbon-price jurisdictions and is projected to achieve full cost parity in multiple markets by 2030 to 2032 as green hydrogen costs decline and carbon prices increase. The European Union Carbon Border Adjustment Mechanism, which became fully operational for steel in 2026, imposes carbon cost obligations on steel imports based on embedded carbon dioxide emissions calculated against EU Emissions Trading System benchmark prices, creating a direct financial incentive for non-European steel producers exporting to the EU market to decarbonise their production processes through hydrogen-based iron reduction or face mounting competitiveness penalties relative to domestically produced low-carbon steel. Automotive original equipment manufacturers, construction material suppliers, consumer electronics assemblers, and consumer goods manufacturers with validated Scope 3 emission reduction commitments under the Science Based Targets initiative are generating direct procurement demand for certified low-carbon and green steel whose embedded carbon content documentation requirements can only be met by steel produced through hydrogen-based iron reduction or equivalent near-zero-emission production pathways, creating a forward market demand signal that supports the commercial case for green steel plant investment decisions being made today for production facilities with 2027 to 2032 commissioning timelines.

Renewable Energy Cost Deflation and Green Hydrogen Electrolyser Scale-Up Accelerating the Economic Viability of Hydrogen-Based Ironmaking

The sustained and accelerating cost reduction trajectory of utility-scale solar photovoltaic and wind power generation, combined with the rapid scaling of electrolyser manufacturing capacity and the consequent decline in electrolyser capital costs, is fundamentally improving the economics of green hydrogen production for direct iron reduction applications at a pace that is consistently exceeding the projections of energy transition scenarios published as recently as three years ago, pulling forward the timeline for green hydrogen to achieve the USD 2.0 per kilogram or below delivered cost threshold at which hydrogen-based iron reduction becomes cost-competitive with natural gas-based direct reduced iron in most markets. Utility-scale solar power purchase agreement prices in the most favourable locations including Saudi Arabia, the UAE, Chile, Australia, and the southwestern United States fell below USD 0.02 per kilowatt hour in competitive procurement rounds conducted in 2024 and 2025, providing the electricity cost foundation for green hydrogen production at below USD 2.0 per kilogram at the electrolyser gate in these locations by 2027 to 2028 based on current electrolyser efficiency and capital cost trajectories. Electrolyser manufacturing capacity is scaling rapidly across alkaline, proton exchange membrane, and solid oxide platforms, with global installed electrolyser manufacturing capacity reaching approximately 25 gigawatts per year in 2025 and projected to exceed 100 gigawatts per year by 2030, driving electrolyser capital cost reduction from approximately USD 1,100 per kilowatt in 2023 toward projected USD 350 to USD 500 per kilowatt by 2030, materially improving the capital efficiency of green hydrogen production plants sized for direct iron reduction applications.

Steel Industry Net-Zero Commitments and National Industrial Decarbonisation Policy Programs Mobilising Capital for Green Steelmaking Transition Investment

The global steel industry’s collective commitment to net-zero carbon emission production by 2050, expressed through corporate decarbonisation strategies, national industrial policy programs, and multilateral climate frameworks including the First Movers Coalition and the Industrial Deep Decarbonisation Initiative, is mobilising investment capital into hydrogen-based iron reduction at a scale and pace that is creating a self-reinforcing technology development and commercial scaling dynamic whose momentum is becoming increasingly difficult for individual steel producers or governments to opt out of without risking competitiveness and market access consequences. Major global steel producers including those headquartered in Europe, Japan, South Korea, India, and the United States have collectively announced hydrogen-based iron reduction project investments exceeding USD 72 billion as of 2025, spanning greenfield hydrogen direct reduced iron and electric arc furnace plant construction, conversion of existing blast furnace assets to hydrogen shaft furnace and electric arc furnace routes, and pilot and demonstration scale projects validating emerging hydrogen reduction technologies. National green steel programs in Sweden, Germany, Spain, Australia, Japan, South Korea, India, and Canada are providing grants, concessional loans, production tax credits, and carbon contract-for-difference support mechanisms whose combined value is estimated at approximately USD 18 billion across committed and announced programs globally as of 2025, providing the commercial risk mitigation framework required to attract private capital into first-of-kind commercial-scale hydrogen-based iron reduction projects whose technology risk profiles and long payback periods would otherwise challenge financing under purely commercial criteria.

Key Challenges

Green Hydrogen Cost and Supply Infrastructure Immaturity Constraining the Commercial Viability and Scaling Pace of Hydrogen-Based Iron Reduction Plants

The single most binding constraint on the commercial scaling of hydrogen-based iron reduction is the current cost and supply infrastructure immaturity of green hydrogen, whose delivered cost to direct reduction plant gate of approximately USD 4.0 to USD 6.5 per kilogram in most markets in 2025 makes hydrogen-based steelmaking between USD 150 and USD 280 per metric ton of steel more expensive than blast furnace production at current carbon prices, requiring either carbon price increases, green premium revenue from customers, or government subsidy mechanisms to bridge the commercial gap during the current decade when green hydrogen costs are expected to decline but have not yet reached the competitive threshold required for unsubsidised commercial operation. The hydrogen supply infrastructure challenge is compounded by the very large volumes of hydrogen required for commercial-scale iron reduction operations, with a single 2-million-metric-ton-per-year direct reduced iron plant requiring approximately 110,000 metric tons of hydrogen annually, equivalent to approximately 550 megawatts of continuous electrolyser capacity operating at full utilisation, whose capital cost at current electrolyser pricing exceeds USD 600 million for the electrolysis system alone, independent of the renewable electricity generation assets, water treatment systems, hydrogen compression and storage infrastructure, and grid or off-grid power supply arrangements required to operate a fully integrated green hydrogen iron reduction complex. Pipeline hydrogen transport infrastructure for delivering green hydrogen from production locations with the most favourable renewable energy resources to existing steel plant locations is largely absent and requires decades-scale development investment, constraining near-term hydrogen direct reduction deployment to locations where renewable electricity generation can be co-located with or situated in close proximity to the iron reduction plant.

High-Grade Iron Ore Pellet Feed Scarcity and the Capital Investment Required to Develop Pelletisation Capacity Compatible with Hydrogen Reduction Requirements

Hydrogen shaft furnace direct reduction technology requires iron ore pellets with iron content typically exceeding 67% and very low concentrations of silica, alumina, phosphorous, and other gangue minerals whose presence in the reduction feed increases energy consumption, reduces productivity, and generates slag volumes in subsequent electric arc furnace melting operations that compromise the economics of green steelmaking relative to blast furnace production using standard iron ore sinter and pellet feeds. The available global supply of high-grade iron ore pellet feed meeting the specifications demanded by hydrogen reduction operations is significantly smaller than the total iron ore pellet market, with the premium pellet feed production capacity of the world’s major iron ore suppliers estimated at approximately 180 million metric tons per year in 2025 against projected hydrogen direct reduced iron demand for pellet feed of 350 to 500 million metric tons per year by 2034 if announced project pipelines are realised, implying a structural pellet feed supply deficit that will require substantial investment in new magnetite concentrate beneficiation plants, pelletisation facilities, and exploration and development of new high-grade iron ore deposits. The capital cost of developing integrated pellet feed mining, beneficiation, and pelletisation capacity for hydrogen direct reduction specifications is substantial, with a 10-million-metric-ton-per-year pellet production facility requiring capital investment of approximately USD 1.5 billion to USD 2.5 billion depending on ore body characteristics and location, representing a parallel capital mobilisation requirement alongside hydrogen production and direct reduction plant investment that increases the total green steelmaking transition investment per unit of decarbonised steel production capacity.

Regulatory Uncertainty, Carbon Price Volatility, and the Commercial Risk of Long-Duration First-of-Kind Industrial Decarbonisation Investments

Hydrogen-based iron reduction investments involve capital commitments of USD 1 billion to USD 5 billion per project, asset lives of 25 to 40 years, and payback periods under current market conditions that extend beyond the near-term policy and carbon price visibility horizon, creating a structural commercial risk profile that requires long-term contractual certainty from carbon pricing frameworks, green hydrogen offtake agreements, green steel supply contracts, and government support mechanisms whose combined stability cannot be fully assured over the investment horizon relevant to project financing decisions being made today. Carbon price trajectory uncertainty is particularly significant, as the commercial viability of hydrogen-based iron reduction relative to blast furnace steelmaking is sensitive to carbon price levels whose future evolution in the European Union Emissions Trading System, emerging carbon markets in the United Kingdom, Canada, Australia, South Korea, and China, and the potential development of a global carbon price floor is governed by political dynamics that introduce material scenario uncertainty into the long-term financial modelling of green steel investment cases. The financing of first-of-kind commercial-scale hydrogen direct reduced iron plants at the multi-billion-dollar scale required for competitive green steel production is challenged by lender risk aversion toward novel industrial technology operating at unprecedented scale, the absence of a deep project finance market with experience in hydrogen-based iron reduction project structures, the limited availability of investment-grade offtake counterparties capable of committing to green steel supply agreements of the duration and volume required to support project debt financing on commercial terms, and the residual technology performance uncertainty associated with operating hydrogen shaft furnaces at full hydrogen concentration at commercial production scale over extended periods.

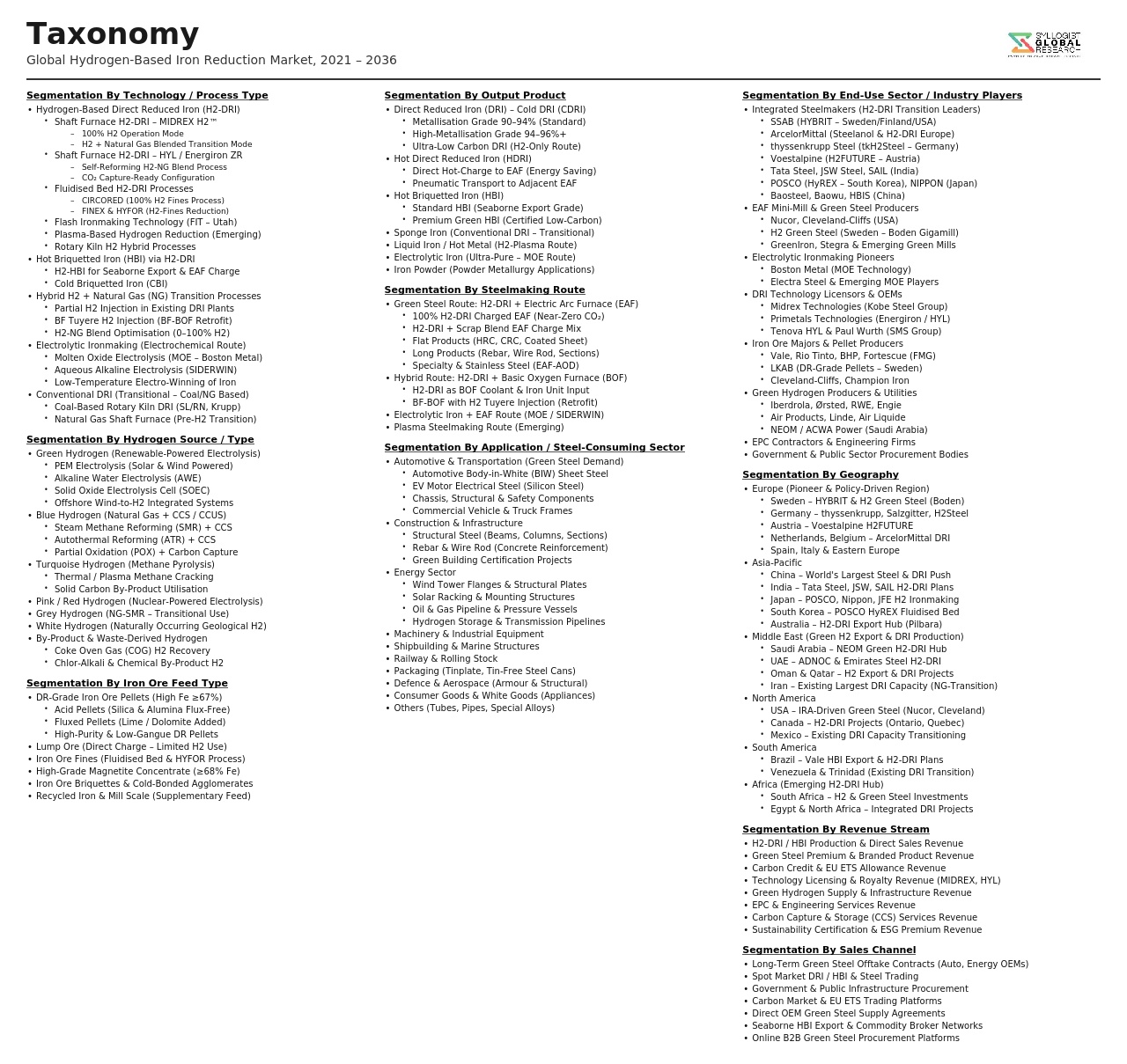

Market Segmentation

- Segmentation By Process Technology

- Shaft Furnace Direct Reduction (Hydrogen-Natural Gas Blend and Full Hydrogen)

- Fluidised Bed Reduction for Iron Ore Fines

- Plasma-Based Hydrogen Iron Reduction

- Smelting Reduction with Hydrogen Injection

- Electrochemical Iron Ore Reduction (Molten Oxide Electrolysis)

- Others

- Segmentation By Hydrogen Feedstock Type

- Green Hydrogen (Water Electrolysis via Renewable Energy)

- Blue Hydrogen (Steam Methane Reforming with Carbon Capture)

- Turquoise Hydrogen (Methane Pyrolysis)

- Natural Gas and Hydrogen Blend (Transitional)

- Low-Carbon Hydrogen from Nuclear Energy

- Others

- Segmentation By Product Form

- Cold Direct Reduced Iron (Cold DRI)

- Hot Direct Reduced Iron (Hot DRI)

- Hot Briquetted Iron (HBI)

- Liquid Iron (Plasma and Smelting Reduction Routes)

- Hot Direct Reduced Iron for Direct Electric Arc Furnace Charging

- Segmentation By Downstream Steelmaking Route

- Electric Arc Furnace (EAF) Steelmaking

- Submerged Arc Furnace Processing

- Induction Furnace Melting

- Integrated Hydrogen Direct Reduced Iron and Electric Arc Furnace Green Steel Plants

- Hybrid Blast Furnace and Hydrogen Injection Transitional Routes

- Segmentation By Iron Ore Feed Type

- High-Grade Iron Ore Pellets (Greater than 67% Fe Content)

- Lump Iron Ore

- Iron Ore Fines (for Fluidised Bed Reduction)

- Magnetite Concentrate Pellets

- Itabirite and Haematite High-Grade Concentrate Pellets

- Segmentation By End-Use Steel Application

- Flat Steel Products (Automotive, Appliances, and Packaging)

- Long Steel Products (Construction and Infrastructure)

- Specialty and Stainless Steel

- Tube and Pipe Products (Oil, Gas, and Industrial)

- Wire Rod and Merchant Bar

- Others

- Segmentation By Plant Configuration

- Greenfield Integrated Hydrogen Direct Reduced Iron and Electric Arc Furnace Plants

- Brownfield Conversion of Existing Direct Reduced Iron Shaft Furnaces

- Greenfield Export-Oriented Hydrogen Direct Reduced Iron Production

- Captive Steel Producer Integrated Plants

- Merchant Hot Briquetted Iron Production for Third-Party Steel Producers

- Segmentation By Region

- Europe (Sweden, Germany, Spain, Netherlands, and Austria)

- Middle East (Saudi Arabia, UAE, Oman, and Bahrain)

- Asia-Pacific (Japan, South Korea, India, Australia, and China)

- North America (United States and Canada)

- South America (Brazil and Others)

- Africa and Other Regions

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Hydrogen-Based Iron Reduction Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by process technology platform, shaft furnace, fluidised bed, and plasma reduction, by hydrogen type, green, blue, and turquoise hydrogen, by product form, cold direct reduced iron, hot direct reduced iron, and hot briquetted iron, and by region, to enable steel producers, engineering contractors, hydrogen developers, iron ore miners, and investors to quantify the commercial scale and investment opportunity of hydrogen-based iron reduction across the forecast period?

- What is the projected green hydrogen cost reduction trajectory through 2034 across the major regions pursuing hydrogen-based iron reduction investment, including the Middle East, North Africa, Australia, Northern Europe, and North America, how will declining electrolyser capital costs, improving renewable energy economics, and scaling electrolyser manufacturing capacity collectively translate into delivered green hydrogen costs at direct reduction plant gate, and at what carbon price and green steel premium levels does hydrogen-based iron reduction achieve unsubsidised cost parity with blast furnace steelmaking in each major regional steel market?

- How are the European Union Carbon Border Adjustment Mechanism, national carbon contracts for difference programs, green steel production tax credits, and multilateral green hydrogen support frameworks expected to evolve through 2034, which policy instruments are proving most effective at mobilising private capital into first-of-kind commercial-scale hydrogen direct reduced iron projects, and what are the residual policy gaps and regulatory uncertainties that are most significantly constraining investment commitment pace for projects currently in the feasibility and front-end engineering design stages across Europe, the Middle East, Australia, and Asia?

- What is the current and projected supply-demand balance for high-grade iron ore pellet feed meeting hydrogen direct reduction specifications through 2034, which iron ore mining jurisdictions and companies are best positioned to develop the incremental pellet feed mining, beneficiation, and pelletisation capacity required to support the announced hydrogen direct reduced iron project pipeline, and how are iron ore quality premiums and pellet feed pricing expected to evolve as hydrogen reduction demand competes with conventional direct reduced iron and blast furnace pellet consumption for limited high-grade iron ore supply?

- Who are the leading steel producers, engineering technology licensors, electrolyser manufacturers, hydrogen project developers, and iron ore suppliers currently defining the competitive and investment landscape of the global hydrogen-based iron reduction market, and what are their respective technology development and project commissioning timelines, capital investment commitments and project pipeline positions, green hydrogen supply agreements and renewable energy partnerships, iron ore pellet feed supply arrangements, green steel offtake agreement structures with automotive and industrial customers, and strategic responses to the cost, supply chain, and policy challenges governing the pace of commercial scale deployment through 2034?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Project Development & Investment Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Green Hydrogen Cost and Availability Risk: Electrolyser Scaling, Renewable Energy Supply and Hydrogen Logistics Constraints Limiting H-DRI Viability

- Iron Ore Pellet Quality and Supply Risk: High-Grade DR-Grade Pellet Scarcity, Pellet Premium Volatility and Supplier Concentration

- Technology and Process Performance Risk: Reactor Scaling, Hydrogen Embrittlement, Metallisation Rate Variability and EAF Integration Challenges

- Carbon Border Adjustment Mechanism (CBAM) and Regulatory Transition Risk: Policy Reversal, Timeline Uncertainty and Competitiveness Impact on Green Steel Adoption

- Capital Expenditure, Project Financing and Offtake Risk for First-of-Kind and Pioneer-Scale H-DRI and Green Steel Projects

- Regulatory Framework & Standards

- EU Carbon Border Adjustment Mechanism (CBAM), EU Emissions Trading System (EU ETS) Phase IV and Their Competitive Implications for H-DRI and Green Steel Producers

- EU Hydrogen Strategy, Delegated Acts on Renewable Fuels of Non-Biological Origin (RFNBO) and Green Hydrogen Certification Standards Applicable to H-DRI

- US Inflation Reduction Act (IRA) Section 45V Clean Hydrogen Production Tax Credit and Section 48C Advanced Manufacturing Credit: Implications for H-DRI Investment in North America

- National Green Steel Procurement Policies, Public Sector Low-Carbon Steel Standards and Government Offtake Commitments Across Key Markets

- ISO and CEN Standards for Hydrogen-Based Direct Reduced Iron Quality, Green Steel Certification, Embodied Carbon Accounting and Product-Level Environmental Declarations

- Global Hydrogen-Based Iron Reduction Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Million Metric Tons of H-DRI and HBI Produced)

- Market Size & Forecast by Technology Route

- Pure Hydrogen Direct Reduced Iron (H-DRI) via Shaft Furnace (MIDREX H2, Energiron and Other Shaft-Based Systems)

- Hybrid Hydrogen-Natural Gas DRI Transitional Route (Partial H2 Injection into Existing NG-DRI Plants)

- Fluidised Bed Hydrogen Reduction Technology (HYFOR, Circored and Other Fluidised Bed Systems)

- Hydrogen Plasma Smelting Reduction (HPSR) and Molten Oxide Electrolysis (MOE) Novel Routes

- Hydrogen-Based Hot Briquetted Iron (HBI) Production for Sea-Borne Trade and EAF Charge

- Market Size & Forecast by Hydrogen Source

- Green Hydrogen (PEM and Alkaline Electrolysis Powered by Renewable Energy)

- Blue Hydrogen (Steam Methane Reforming with Carbon Capture and Storage)

- Turquoise Hydrogen (Methane Pyrolysis)

- Mixed and Transitional Hydrogen Supply (Grid Electricity and Partially Renewable Sources)

- Market Size & Forecast by Iron Ore Feed Type

- High-Grade DR-Grade Iron Ore Pellets (67 Percent Fe and Above)

- Iron Ore Lump (Direct Charge without Pelletisation)

- Iron Ore Fines (for Fluidised Bed and HYFOR-Type Processes)

- Beneficiated Magnetite Concentrate (for Pellet Feed)

- Market Size & Forecast by Output Product

- Hot Direct Reduced Iron (HDRI) for Direct EAF Charging

- Cold Direct Reduced Iron (CDRI) for Storage and Short-Distance Transport

- Hot Briquetted Iron (HBI) for Sea-Borne Trade and Merchant EAF Supply

- Market Size & Forecast by Downstream Steelmaking Route

- Electric Arc Furnace (EAF) Steelmaking (H-DRI as Primary Charge)

- EAF with Scrap and H-DRI Blend (Hybrid Charge Optimisation)

- Submerged Arc Furnace and Other Smelting Routes with H-DRI Feed

- Market Size & Forecast by Steel Product End-Use

- Flat Products (Hot-Rolled Coil, Cold-Rolled Coil, Coated Sheet for Automotive and Appliances)

- Long Products (Rebar, Wire Rod, Sections and Structural Steel for Construction)

- Tubes, Pipes and Special Bar Quality (SBQ) for Energy and Industrial Applications

- Specialty and High-Value Steels (Stainless, Electrical, Tool and Alloy Steels)

- Market Size & Forecast by End-Use Industry

- Automotive and Transportation (Green Steel for EV Platforms and Lightweighting)

- Construction and Infrastructure (Low-Carbon Structural Steel and Rebar)

- Energy (Offshore Wind Foundations, Pipelines and Power Generation Equipment)

- Machinery, Industrial Equipment and Consumer Goods

- Defence and Aerospace

- Market Size & Forecast by Project Scale

- Pioneer and Demonstration Scale (Below 0.5 Million Tons Per Annum H-DRI)

- Commercial Scale (0.5 to 2 Million Tons Per Annum H-DRI)

- Full Industrial Scale (Above 2 Million Tons Per Annum H-DRI)

- Market Size & Forecast by Sales and Offtake Channel

- Integrated Steelmaker Captive H-DRI Supply (On-Site Reduction and EAF)

- Merchant HBI Supply via Long-Term Offtake Agreements with EAF Steelmakers

- Spot and Exchange-Traded HBI and CDRI

- Green Steel Supply Contracts with Automotive OEMs and Industrial Off-Takers

- North America Hydrogen-Based Iron Reduction Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Metric Tons of H-DRI and HBI Produced)

- By Technology Route

- By Hydrogen Source

- By Iron Ore Feed Type

- By Output Product

- By Downstream Steelmaking Route

- By Steel Product End-Use

- By End-Use Industry

- By Project Scale

- By Country

- By Sales and Offtake Channel

- Market Size & Forecast

- Europe Hydrogen-Based Iron Reduction Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Metric Tons of H-DRI and HBI Produced)

- By Technology Route

- By Hydrogen Source

- By Iron Ore Feed Type

- By Output Product

- By Downstream Steelmaking Route

- By Steel Product End-Use

- By End-Use Industry

- By Project Scale

- By Country

- By Sales and Offtake Channel

- Market Size & Forecast

- Asia-Pacific Hydrogen-Based Iron Reduction Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Metric Tons of H-DRI and HBI Produced)

- By Technology Route

- By Hydrogen Source

- By Iron Ore Feed Type

- By Output Product

- By Downstream Steelmaking Route

- By Steel Product End-Use

- By End-Use Industry

- By Project Scale

- By Country

- By Sales and Offtake Channel

- Market Size & Forecast

- Latin America Hydrogen-Based Iron Reduction Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Metric Tons of H-DRI and HBI Produced)

- By Technology Route

- By Hydrogen Source

- By Iron Ore Feed Type

- By Output Product

- By Downstream Steelmaking Route

- By Steel Product End-Use

- By End-Use Industry

- By Project Scale

- By Country

- By Sales and Offtake Channel

- Market Size & Forecast

- Middle East & Africa Hydrogen-Based Iron Reduction Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Metric Tons of H-DRI and HBI Produced)

- By Technology Route

- By Hydrogen Source

- By Iron Ore Feed Type

- By Output Product

- By Downstream Steelmaking Route

- By Steel Product End-Use

- By End-Use Industry

- By Project Scale

- By Country

- By Sales and Offtake Channel

- Market Size & Forecast

- Country-Wise* Hydrogen-Based Iron Reduction Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Metric Tons of H-DRI and HBI Produced)

- By Technology Route

- By Hydrogen Source

- By Iron Ore Feed Type

- By Output Product

- By Downstream Steelmaking Route

- By Steel Product End-Use

- By End-Use Industry

- By Project Scale

- By Country

- By Sales and Offtake Channel

- Market Size & Forecast

- *Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, Sweden, France, United Kingdom, Netherlands, Spain, Italy, Norway, Austria, China, Japan, South Korea, India, Australia, Brazil, Chile, Argentina, Saudi Arabia, UAE, Oman, South Africa, Egypt, Israel

- Technology Landscape & Innovation Analysis

- Shaft Furnace H-DRI Technology Deep-Dive: MIDREX H2, Energiron ZR Hydrogen Mode, Voestalpine greentec steel and Tenova HYL H2 Process Configurations

- Fluidised Bed Hydrogen Reduction Technology: HYFOR (Primetals), Circored (Outotec) and Iron Ore Fines Direct Reduction Process Comparison

- Hydrogen Plasma Smelting Reduction (HPSR) and Molten Oxide Electrolysis (MOE): Next-Generation Ironmaking Technology Readiness and Commercialisation Pathway

- Green Hydrogen Production Integration: PEM and Alkaline Electrolyser Sizing, Renewable Energy Coupling and Hydrogen Storage for Continuous DRI Operation

- Hot Direct Rolling and HDRI-to-EAF Integration: Thermal Energy Recovery, Process Efficiency and Hot Charging Technology

- Carbon Capture, Utilisation and Storage (CCUS) Integration with Blue Hydrogen DRI Routes as Transitional Decarbonisation Pathway

- Digital Twin, Process Simulation and AI-Based Optimisation Platforms for H-DRI Plant Operation

- Patent & IP Landscape in Hydrogen-Based Iron Reduction Technologies

- Value Chain & Supply Chain Analysis

- DR-Grade Iron Ore Pellet Supply Chain: Mining, Beneficiation, Pelletisation and Logistics to H-DRI Plant

- Green and Blue Hydrogen Production, Compression, Storage and Pipeline or Tube-Trailer Delivery to H-DRI Facility

- H-DRI and HBI Production, Handling, Cooling and Briquetting Operations

- HBI Sea-Borne Logistics: Port Infrastructure, Bulk Carrier Shipping and Import Terminal Requirements

- EAF Steelmaking Integration: Scrap Sourcing, Charge Mix Optimisation and Ladle Metallurgy with H-DRI

- Green Steel Rolling, Finishing and Certification: Product Carbon Footprint Declaration and Green Premium Realisation

- End-Market Offtake: Automotive OEM, Construction and Industrial Green Steel Procurement Landscape

- Pricing Analysis

- Green Hydrogen Levelised Cost of Hydrogen (LCOH) Trajectory: 2024 to 2040 Cost Reduction Pathway and Sensitivity to Electrolyser CAPEX and Renewable Energy Price

- DR-Grade Iron Ore Pellet Price Trends, Premium Structure and Long-Term Supply Contract Pricing

- H-DRI and HBI Production Cost Benchmarking: Green H-DRI vs. Natural Gas DRI vs. Blast Furnace Hot Metal Cost Comparison

- Green Steel Price Premium: Current Green Steel Spot and Contract Price vs. Conventional BF-BOF and Scrap EAF Steel

- Carbon Price Impact: EU ETS Carbon Cost Pass-Through and CBAM Levy Effect on H-DRI Project Economics and Green Steel Competitiveness

- Offtake Agreement and Green Premium Contract Structures: Fixed Premium, Index-Linked and Carbon-Credit-Based Pricing Mechanisms

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Hydrogen-Based Iron Reduction: Scope 1, 2 and 3 Carbon Footprint Comparison Across Green H-DRI, Blue H-DRI and Conventional BF-BOF and NG-DRI Routes

- Water Consumption in Green H-DRI: Electrolyser Water Demand, Process Water Use and Water Stress Implications for Plant Siting in Arid Renewable Energy Regions

- Renewable Energy Land Use, Grid Impact and 24/7 Carbon-Free Energy Requirements for Truly Green Hydrogen-Based Iron Reduction

- Embodied Carbon Accounting, Environmental Product Declarations (EPDs) and Green Steel Certification Standards for H-DRI-Based Steel Products

- Contribution to Steel Industry Net-Zero Pathways: H-DRI Role in SBTi, Science-Based Targets, ResponsibleSteel and GSCC Decarbonisation Scenarios

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Pioneer Phase Fragmentation vs. Emerging Commercial Concentration by Technology Route and Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Technology Route, Project Scale and Geography

- Player Classification

- Integrated Steel Companies Developing Proprietary H-DRI and Green Steel Programmes

- DRI Technology Licensors and Engineering Companies (MIDREX, Tenova, Primetals and Others)

- Green Hydrogen Producers and Electrolyser Manufacturers with H-DRI Partnerships

- Iron Ore Miners and Pellet Producers Investing in DR-Grade Supply and Downstream H-DRI

- EPC Contractors and Project Developers Specialising in H-DRI and Green Steel Projects

- Equipment Suppliers: EAF Manufacturers, Gas Treatment and Heat Recovery System Providers

- Competitive Analysis Frameworks

- Market Share Analysis by Technology Route, Output Product and Region

- Company Profile

- Company Overview & Headquarters

- H-DRI Technology Portfolio, Process Licence and Project Pipeline

- Installed and Planned H-DRI Capacity (Million Tons Per Annum)

- Key Customer Relationships, Offtake Agreements and Green Steel Partners

- Revenue (H-DRI and Green Steel Segment) and Capital Expenditure

- Technology Differentiators, Process IP & Green Certifications

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Plant Commissioning, FID Decisions, Offtake Deals and Policy Milestones)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Readiness vs. Production Scale and Green Credential)

- Key Company Profiles

- Market Structure & Concentration

- Strategic Outlook & Opportunity Analysis

- Strategic Output

- Market Opportunity Matrix: By Technology Route, Hydrogen Source, Output Product, End-Use Industry and Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Technology Selection & Process Route Investment Strategy

- Green Hydrogen Sourcing, Electrolyser Partnership & Energy Integration Strategy

- DR-Grade Iron Ore Pellet Sourcing & Supply Security Strategy

- Green Steel Offtake, Customer Engagement & Premium Realisation Strategy

- Geographic Expansion, Plant Siting & Renewable Energy Co-Location Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability, Net-Zero & Green Certification Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output