Global Leather Chemicals Market By Chemical Type, By Process Stage, By Leather Type, By Application, By End Use Industry, By Distribution Channel, By Region, Competition, Forecast and Opportunities, 2021-2036F

Market Definition

The Global Leather Chemicals Market encompasses the formulation, manufacturing, and commercial supply of specialty chemicals used across all stages of raw hide and skin processing into finished leather, including beamhouse chemicals for soaking, liming, and deliming, tanning agents comprising chromium salts, vegetable tannins, and synthetic tannins, retanning agents, fatliquoring oils, dyestuffs, finishing chemicals, waterproofing agents, and effluent treatment auxiliaries. The market includes organic and inorganic chemical inputs procured by tanneries, leather finishing operations, footwear manufacturers, automotive upholstery producers, and luxury goods manufacturers to achieve specific performance, aesthetic, and regulatory compliance characteristics in finished leather products globally.

Market Insights

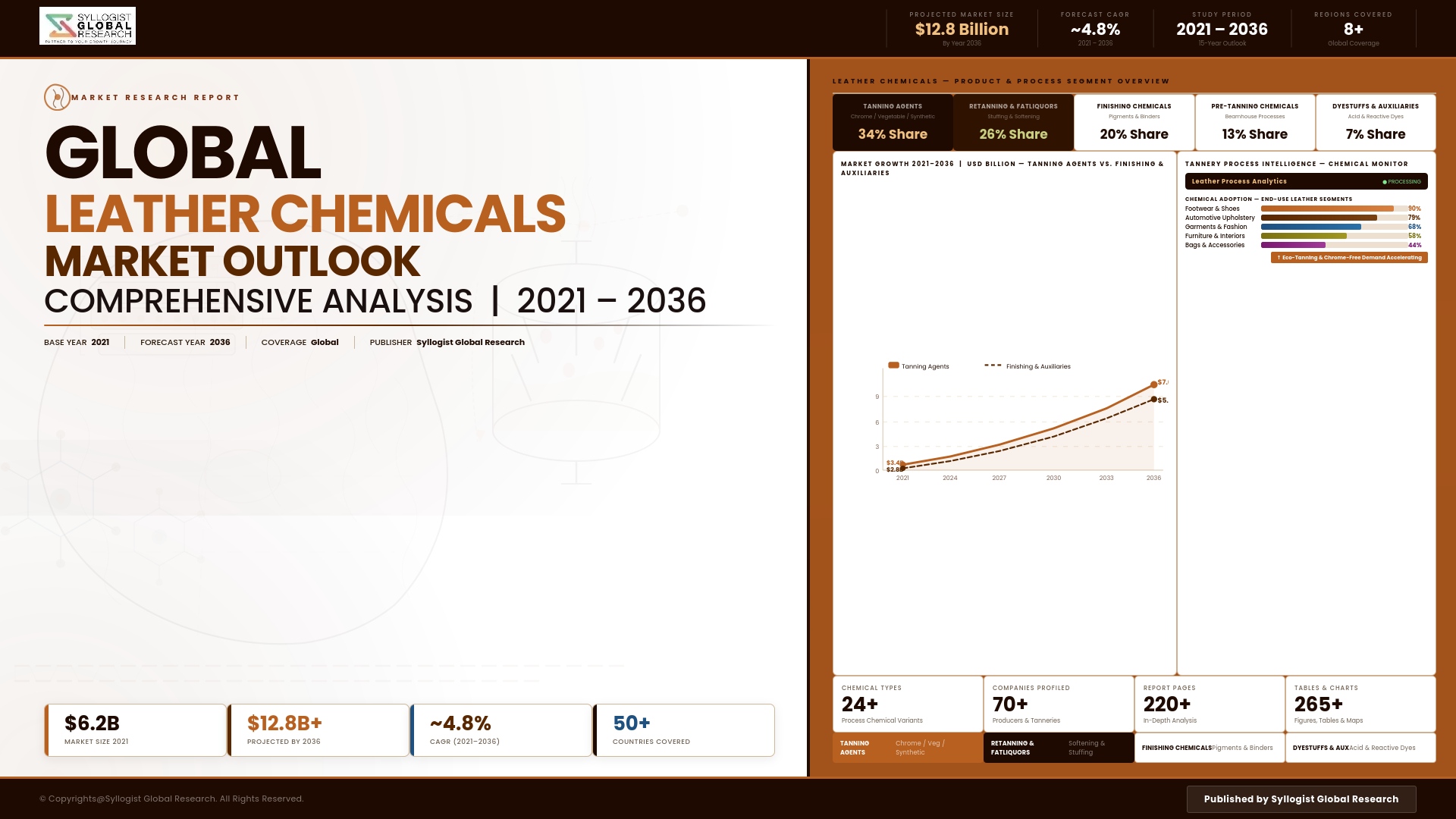

The global leather chemicals market is navigating a complex period of simultaneous demand growth and structural transformation, driven by recovering leather goods consumption across footwear, automotive upholstery, and luxury accessories categories on one hand, and mounting environmental regulatory pressure, chromium-free tanning mandate progression, and the expanding competitive challenge from high-performance synthetic leather alternatives on the other. The market was valued at approximately USD 9.1 billion in 2025 and is projected to reach USD 13.8 billion by 2034, advancing at a compound annual growth rate of 4.7% through the forecast period, as growth in leather consumption across Asia-Pacific emerging markets and premiumization trends in luxury leather goods sustain volume expansion while chemistry innovation in sustainable tanning systems, bio-based fatliquoring agents, and low-emission finishing chemicals drives per-unit value growth across the specialty chemical segments of the leather processing value chain.

The tanning chemicals segment remains the most strategically significant within the leather chemicals landscape, with the ongoing industry transition away from conventional chromium sulfate tanning systems toward chrome-free alternatives representing the most consequential chemistry shift in the tanning industry in several decades. Regulatory restrictions on hexavalent chromium in finished leather products, concerns regarding trivalent chromium conversion under heat and humidity conditions in automotive and footwear applications, and brand owner supply chain sustainability commitments are collectively accelerating the qualification and adoption of aldehyde-based, glutaraldehyde, oxazolidine, synthetic tannin, and metal-free organic tanning systems that can match the thermal stability, tensile strength, and finishing receptivity characteristics of chrome-tanned leather within acceptable processing cost differentials. The retanning and fatliquoring segment is experiencing parallel chemistry innovation as tanneries seek bio-based and biodegradable alternatives to petrochemical-derived sulfited oils and synthetic polymeric retanning agents that face increasing regulatory scrutiny under evolving chemical safety frameworks in European and North American markets where leather chemical suppliers must demonstrate environmental fate and worker exposure compliance across their product portfolios.

The automotive leather upholstery segment represents a particularly high-value demand driver for premium leather chemicals, as the stringent performance requirements of automotive interior leather encompassing UV and heat resistance, low volatile organic compound emissions, abrasion durability, and antimicrobial performance demand finishing chemical systems of substantially higher technical complexity and per-unit value than standard footwear or garment leather applications. The growing integration of leather in electric vehicle interiors, where the elimination of engine noise elevates the perceptibility of leather material off-gassing and tactile quality, is driving automakers and tier-one interior suppliers toward increasingly demanding VOC emission and odor specifications that are reshaping finishing chemical formulation requirements across the automotive leather supply chain. Asia-Pacific dominates global leather chemical consumption, anchored by the concentration of tanning capacity in China, India, Bangladesh, and Vietnam, which collectively process the majority of global raw hide supply. Europe maintains leadership in premium leather chemical innovation, chromium-free tanning system development, and high-value automotive and luxury goods leather finishing chemistry. North America represents a significant market through automotive leather upholstery chemical demand and premium footwear and accessories leather specification requirements that command the most technically advanced finishing system solutions.

Key Drivers

Expanding Footwear, Automotive Upholstery, and Luxury Leather Goods Consumption Across Emerging Markets Generating Sustained Volume Demand Growth for Leather Processing Chemicals

The continued expansion of middle-class consumer cohorts across China, India, Southeast Asia, and Latin America, combined with the premiumization of footwear and accessories consumption as disposable incomes rise toward discretionary luxury spending thresholds in high-growth markets, is generating sustained volume demand growth for leather processing chemicals across tanneries serving the global footwear, handbag, and small leather goods manufacturing supply chain. The recovery and growth of automotive leather upholstery in both conventional and electric vehicle interior programs, where leather remains the preferred premium surface material across mass-market premium and luxury vehicle segments globally, is creating additional durable demand for high-performance finishing and tanning chemical systems serving the technical requirements of automotive-qualified leather supply chains.

Chrome-Free and Sustainable Tanning Chemistry Regulatory Mandates and Brand Owner Supply Chain Requirements Driving Premium Innovation Investment Across Tanning and Retanning Chemical Segments

Progressive regulatory restrictions on chromium in leather products across the European Union, evolving automotive OEM low-emission and restricted substance list compliance requirements, and branded fashion and footwear company public commitments to eliminating heavy metal tanning from supply chains are collectively generating sustained investment in chrome-free tanning system development and commercialization that is creating a structurally growing premium market segment for aldehyde-based, synthetic organic, and metal-free tanning chemical systems whose per-unit value and technical service requirements substantially exceed those of conventional chromium sulfate tanning salt supply. Chemical suppliers capable of delivering validated chrome-free tanning systems with commercial-scale performance and cost acceptance are securing strategic long-term supply relationships with forward-positioned tanneries and brand owner supply chains.

Automotive Interior Leather Performance Requirement Escalation and Electric Vehicle VOC and Odor Specification Tightening Elevating Demand for High-Value Specialty Finishing Chemical Systems

The intensification of automotive OEM leather interior performance specifications across volatile organic compound emission limits, odor evaluation standards, antimicrobial performance requirements, and UV and thermal aging resistance criteria is compelling automotive leather supply chains to adopt finishing chemical systems of markedly higher technical sophistication and per-unit cost than those sufficient for footwear and general upholstery leather applications, creating a structurally high-value demand category for automotive-grade leather finishing chemicals. The transition to electric vehicle platforms, which eliminates powertrain noise masking of interior material emissions and elevates consumer and regulatory sensitivity to cabin air quality, is further tightening the emission and odor specifications applied to automotive leather finishing chemicals in ways that are driving continuous reformulation investment by specialty chemical suppliers serving the automotive leather segment.

Key Challenges

Stringent Effluent Treatment Regulations, Chromium Discharge Restrictions, and Tannery Wastewater Compliance Costs Constraining Leather Chemical Usage Flexibility and Tannery Operating Economics

The tanning industry is subject to progressively stringent wastewater discharge regulations governing chromium concentration, chemical oxygen demand, biological oxygen demand, sulfide content, and total dissolved solids across tannery effluent streams in most major leather-producing countries, imposing effluent treatment investment requirements and chemical usage constraints that increase the total cost of leather processing and create operational complexity for tanneries seeking to optimize chemical performance within tightening discharge limit frameworks. The regulatory trajectory toward further restriction of chromium discharges and the expansion of zero liquid discharge requirements in environmentally regulated tanning zones across India, China, and other major leather-producing countries is compelling chemical suppliers to reformulate existing products and develop new processing systems that reduce effluent burden without compromising leather quality outcomes, adding product development cost and complexity to the leather chemical supply chain.

Synthetic Leather and Vegan Material Competition Reducing Addressable Hide Processing Volume Across Footwear and Fashion Accessories Application Markets

The accelerating adoption of high-performance polyurethane synthetic leather, bio-based vegan leather alternatives derived from mushroom mycelium, apple waste, cactus, and other plant-based substrates, and recycled material composites across footwear, fashion accessories, and mid-range automotive upholstery applications is progressively reducing the hide processing volume addressed by leather chemical suppliers in application markets that have historically represented substantial demand. Major footwear and fashion brands publicly committing to vegan material transitions across portions of their product ranges, combined with consumer segment growth among ethically motivated purchasers actively seeking non-animal leather alternatives, are creating demand substitution dynamics that constrain the volume growth potential of leather chemical markets in developed economies where these consumer and brand commitment trends are most advanced.

Raw Hide Supply Concentration, Slaughter Cycle Dependency, and Traceability Requirement Complexity Introducing Supply Chain Vulnerability Into Leather Chemical Demand Planning

The global supply of raw bovine hides available for leather processing is structurally dependent on meat industry slaughter volumes that are determined by food consumption patterns, livestock herd cycles, and protein demand dynamics rather than leather demand signals, creating a supply inelasticity that periodically generates raw material availability constraints limiting tannery throughput and consequently leather chemical consumption volumes independently of downstream leather goods demand conditions. The expansion of hide supply chain traceability requirements by luxury brand owners and sustainability-committed retailers seeking to verify deforestation-free and ethical sourcing compliance is imposing documentation and chain-of-custody verification obligations on hide procurement and tannery operations that add supply chain management complexity and cost overhead to the leather processing value chain served by leather chemical suppliers.

Market Segmentation

- Segmentation By Chemical Type

- Beamhouse Chemicals (Soaking, Liming, Deliming, Bating Agents)

- Tanning Agents (Chromium Salts, Vegetable Tannins, Synthetic Tannins, Aldehyde-Based)

- Retanning and Filling Agents

- Fatliquoring and Softening Agents

- Dyestuffs and Pigment Systems

- Finishing Chemicals and Surface Coatings

- Waterproofing and Functional Performance Agents

- Effluent Treatment and Auxiliary Chemicals

- Others

- Segmentation By Process Stage

- Beamhouse and Pre-Tanning Operations

- Tanning and Pickling

- Post-Tanning (Retanning, Fatliquoring, Dyeing)

- Finishing and Surface Treatment

- Effluent and Wastewater Treatment

- Segmentation By Leather Type

- Full-Grain and Top-Grain Leather

- Corrected-Grain and Split Leather

- Nubuck and Suede Leather

- Patent and Coated Leather

- Chrome-Free and Vegetable-Tanned Leather

- Exotic and Specialty Animal Leather

- Others

- Segmentation By Application

- Footwear Upper and Lining Leather

- Automotive Upholstery and Interior Leather

- Luxury Handbags and Small Leather Goods

- Garments and Apparel Leather

- Furniture and Upholstery Leather

- Gloves and Sports Equipment Leather

- Industrial and Technical Leather Products

- Others

- Segmentation By End Use Industry

- Footwear Manufacturing

- Automotive and Mobility Interiors

- Luxury Fashion and Accessories

- Furniture and Home Furnishings

- Sports and Outdoor Equipment

- Garment and Apparel Manufacturing

- Others

- Segmentation By Distribution Channel

- Direct Supply to Tanneries and Leather Processors

- Specialty Chemical Distributor Networks

- Leather Chemical Trading Companies

- Online Chemical Procurement Platforms

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Leather Chemicals Market in 2025, projected through 2034, disaggregated by chemical type, process stage, and application, enabling chemical producers, tanneries, and investors to identify the highest-growth segments and most durable revenue opportunities across the global leather processing chemical value chain?

- How are chrome-free tanning regulatory mandates, automotive OEM restricted substance list requirements, and luxury brand owner sustainability commitments reshaping tanning chemical procurement priorities, and which aldehyde-based, synthetic organic, and metal-free tanning system technologies are achieving commercial-scale performance validation and securing strategic supply relationships with forward-positioned tanneries?

- What impact is the accelerating adoption of synthetic leather, bio-based vegan material alternatives, and recycled composites across footwear and fashion accessories markets having on leather chemical volume demand trajectories, and how are leather chemical producers adapting product portfolios and market positioning to address shifting application mix dynamics through 2034?

- Which leather chemical segments, including automotive finishing systems, chrome-free tanning agents, bio-based fatliquoring oils, and low-VOC topcoat formulations, are generating the highest per-unit value growth and technical development investment, and what performance specifications and regulatory compliance benchmarks are most critical to supplier qualification in premium application markets?

- How is the competitive landscape structured among global specialty chemical majors, regional leather chemical producers, and application-focused formulators, and what innovation investment, geographic expansion, chrome-free portfolio development, and technical service capability strategies are enabling leading suppliers to defend and grow market positions across tannery customer segments?

- What effluent treatment regulations, chromium discharge restrictions, zero liquid discharge mandates, and hide supply traceability requirements are constraining tannery operating economics and leather chemical usage flexibility, and how are chemical suppliers reformulating products and developing new processing systems to reduce effluent burden while maintaining leather quality and processing cost competitiveness?

- Which regional leather chemical markets, specifically Asia-Pacific, Europe, and Latin America, are expected to generate the most substantial demand growth through 2034, and what tannery capacity expansion, raw hide supply dynamics, environmental regulation implementation timelines, and downstream leather goods consumption trends are shaping chemical procurement volumes and supplier positioning in each region?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Raw Hide Supply, Slaughterhouse Availability & Seasonality Risk

- Chromium Regulation, Restricted Substance & Hexavalent Chrome Compliance Risk

- Effluent Discharge, Wastewater Treatment & Environmental Permitting Risk

- Technology Transition, Chrome-Free & Sustainable Leather Adoption Risk

- Capital Investment, Tannery Consolidation & Buyer Concentration Risk

- Regulatory Framework & Standards

- Chemical Management, REACH, ZDHC & Restricted Substance List Compliance Frameworks

- Leather Working Group (LWG), Audit & Sustainable Tanning Certification Standards

- Effluent Discharge, Chromium Wastewater & Industrial Pollution Control Regulations

- Worker Safety, Occupational Exposure & Tannery Labour Standards

- Green Finance, ESG Disclosure & Sustainable Leather Procurement Standards

- Global Leather Chemicals Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Kilotons)

- Market Size & Forecast by Chemical Type

- Beamhouse Chemicals (Soaking, Liming, Unhairing, Deliming, Bating & Pickling Agents)

- Chrome Tanning Agents (Basic Chromium Sulphate & Chrome Complexes)

- Vegetable Tanning Agents (Mimosa, Quebracho, Chestnut & Tara Extracts)

- Synthetic Tanning Agents (Syntans, Aldehyde & Phenolic Tanning Chemicals)

- Metal-Free & Chrome-Free Tanning Agents (Zirconium, Aluminium & Titanium-Based)

- Retanning Agents, Neutralising Agents & Post-Tanning Auxiliaries

- Fatliquors, Oils & Leather Lubricants

- Dyes, Pigments & Colour Solutions (Acid, Basic, Reactive & Metal-Complex Dyes)

- Finishing Agents, Binders, Polyurethane & Acrylic Coating Chemicals

- Market Size & Forecast by Technology

- Chrome Tanning Process Technology

- Vegetable Tanning Process Technology

- Wet-White, Chrome-Free & Metal-Free Tanning Technology

- Combination & Hybrid Tanning Technology

- Enzymatic Bio-Processing & Low-Impact Beamhouse Technology

- Waterless & Low-Water Tanning Technology

- Advanced Finishing, Spray, Roller Coating & Digital Printing Technology

- Chrome Recovery, Effluent Treatment & Closed-Loop Process Technology

- Market Size & Forecast by Form

- Liquid Leather Chemical & Concentrate

- Powder, Granular & Flake Form

- Emulsion, Dispersion & Colloidal Suspension

- Paste, Slurry & Viscous Formulation

- Pelletised, Encapsulated & Controlled-Release Form

- Market Size & Forecast by Leather Type

- Bovine Leather (Cow, Buffalo & Calf)

- Ovine & Caprine Leather (Sheep & Goat)

- Porcine Leather

- Exotic Leather (Reptile, Fish & Specialty Hides)

- Market Size & Forecast by Application

- Footwear Leather

- Automotive & Transportation Upholstery Leather

- Furniture & Home Furnishing Upholstery Leather

- Leather Goods, Bags, Wallets & Accessories

- Garment & Apparel Leather

- Industrial Leather (Gloves, Belts & Protective Wear)

- Sports, Luxury & Specialty Leather

- Market Size & Forecast by End-User

- Leather Tannery & Integrated Leather Processor

- Footwear Manufacturer & Brand

- Automotive, Aerospace & Transportation OEM

- Furniture & Home Furnishing Manufacturer

- Leather Goods, Apparel & Luxury Brand

- Market Size & Forecast by Sales Channel

- Direct Supply & Long-Term Tannery Contract

- Distributor, Specialty Chemical Trader & Spot Market Sales

- Joint Venture, Licensing & Technology Transfer

- Toll Manufacturing, Custom Blending & Contract Formulation Service

- North America Leather Chemicals Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotons)

- By Chemical Type

- By Technology

- By Form

- By Leather Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Leather Chemicals Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotons)

- By Chemical Type

- By Technology

- By Form

- By Leather Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Leather Chemicals Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotons)

- By Chemical Type

- By Technology

- By Form

- By Leather Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Leather Chemicals Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotons)

- By Chemical Type

- By Technology

- By Form

- By Leather Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Leather Chemicals Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotons)

- By Chemical Type

- By Technology

- By Form

- By Leather Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Leather Chemicals Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotons)

- By Chemical Type

- By Technology

- By Form

- By Leather Type

- By Application

- By End-User

- By Country

- By Sales Channel

- *Countries Analysed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Italy, Norway, Sweden, China, Japan, India, Australia, South Korea, Singapore, Brazil, Chile, Saudi Arabia, UAE, Egypt, South Africa, Israel

- Market Size & Forecast

- Technology Landscape & Innovation Analysis

- Chrome & Chrome Complex Tanning Chemistry Deep-Dive

- Vegetable Tannin Extract & Natural Tanning Technology

- Wet-White, Chrome-Free & Metal-Free Tanning Technology

- Fatliquor, Polymer-Based Retanning & Advanced Post-Tanning Technology

- Dye, Pigment & Colour Management Technology for Leather

- Finishing Binder, Polyurethane & Acrylic Coating Technology

- Enzymatic Bio-Processing & Low-Impact Beamhouse Technology

- Patent & IP Landscape in Leather Chemical Technologies

- Value Chain & Supply Chain Analysis

- Raw Hide, Slaughterhouse & Salted Hide Supply Chain

- Wet-Blue, Wet-White & Crust Leather Intermediate Supply Chain

- Specialty Chemical & Tanning Agent Raw Material Supply Chain

- Vegetable Tannin Extract & Natural Raw Material Supply Chain

- Tannery, Leather Processing & Finishing Manufacturing Supply Chain

- Footwear, Automotive, Furniture & Leather Goods OEM Procurement Landscape

- Distributor, Specialty Chemical Trader & Tannery Supply Channel

- Chrome Recovery, Effluent Sludge & Circular Material Loop

- Pricing Analysis

- Chrome & Chrome-Based Tanning Agent Pricing and Cost Structure Analysis

- Vegetable Tannin & Natural Tanning Extract Pricing Analysis

- Syntans, Chrome-Free & Metal-Free Tanning Chemical Pricing Analysis

- Fatliquor, Retanning & Post-Tanning Chemical Pricing Trend Analysis

- Dye, Pigment & Finishing Chemical Pricing Trend Analysis

- Leather Chemical Long-Term Supply Contract, Indexation & Pricing Structure Analysis

- Total Leather Processing Chemical Cost Economics: Cost per Square Foot & Learning Curve Analysis

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Leather Chemicals: Carbon Footprint, Energy Intensity & Water Footprint Across Tanning Routes

- Carbon Neutrality & Net Zero Contribution: Pathway to Low-Impact Tannery Operations and Sustainable Leather Chemistry

- Responsible Sourcing, Hide Traceability, Deforestation-Free & Animal Welfare Due Diligence

- Environmental Compliance, Chromium Management, Wastewater Discharge & Solid Waste Consideration

- Regulatory-Driven Sustainability, LWG, ZDHC, SDG 6 (Clean Water) & SDG 12 (Responsible Consumption) Alignment & Green Finance Eligibility

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Chemical Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Chemical Type, Tanning Process & Geography

- Player Classification

- Integrated Specialty Chemical & Leather Chemical Companies

- Specialist Tanning Agent & Chrome Chemistry Producers

- Vegetable Tannin, Natural Extract & Bio-Based Leather Chemical Suppliers

- Fatliquor, Retanning & Post-Tanning Chemical Manufacturers

- Dye, Pigment & Colour Solution Providers

- Finishing Agent, Binder & Polyurethane Coating Suppliers

- Enzyme, Bio-Processing & Low-Impact Leather Chemical Innovators

- Custom Blending, Toll Manufacturing & Tannery Service Specialists

- Competitive Analysis Frameworks

- Market Share Analysis by Chemical Type, Tanning Process & Region

- Company Profile

- Company Overview & Headquarters

- Leather Chemical Products & Technology Portfolio

- Key Customer Relationships & Reference Tannery Supply Contracts

- Manufacturing Footprint & Production Capacity

- Revenue (Leather Chemical Segment) & Order Book

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Capacity Expansion, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Chemical Type, Tanning Process, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output