Market Definition

The Asia-Pacific Lithium Hexafluorophosphate (LiPF6) Market encompasses the research, development, manufacturing, purification, packaging, and commercial distribution of lithium hexafluorophosphate, the dominant lithium-salt electrolyte solute deployed in lithium-ion battery systems across the full spectrum of energy storage applications in the region. LiPF6 is an inorganic fluorinated lithium salt produced through the controlled reaction of lithium fluoride with phosphorus pentafluoride under precisely regulated anhydrous conditions, yielding a white crystalline powder or solution-phase product of exceptional ionic conductivity that, when dissolved at molar concentrations of approximately 1.0 mol/L in mixed organic carbonate solvent systems comprising ethylene carbonate, dimethyl carbonate, diethyl carbonate, and ethyl methyl carbonate, constitutes the electrolyte formulation used in the overwhelming majority of commercial lithium-ion battery cells manufactured across the Asia-Pacific region. The market encompasses the complete LiPF6 value chain, including anhydrous hydrogen fluoride procurement and refining, lithium carbonate and lithium hydroxide feedstock sourcing and conversion to lithium fluoride, phosphorus pentafluoride synthesis and purification, LiPF6 crystallization and drying operations, electrolyte solution blending incorporating functional additives such as vinylene carbonate, fluoroethylene carbonate, and lithium bis(oxalato)borate, and the final packaging and cold-chain logistics infrastructure required to deliver moisture-sensitive LiPF6 products to battery cell manufacturers under rigorously controlled humidity and temperature conditions. Key market participants include diversified chemical manufacturers with fluorine chemistry capabilities, specialty battery material producers, electrolyte solution formulators, battery cell manufacturers integrating electrolyte procurement within vertically structured supply chains, electric vehicle original equipment manufacturers with battery cell production operations, consumer electronics battery module producers, and stationary energy storage system integrators whose collective demand for high-purity LiPF6 defines the structural growth trajectory of the Asia-Pacific market across the forecast period.

Market Insights

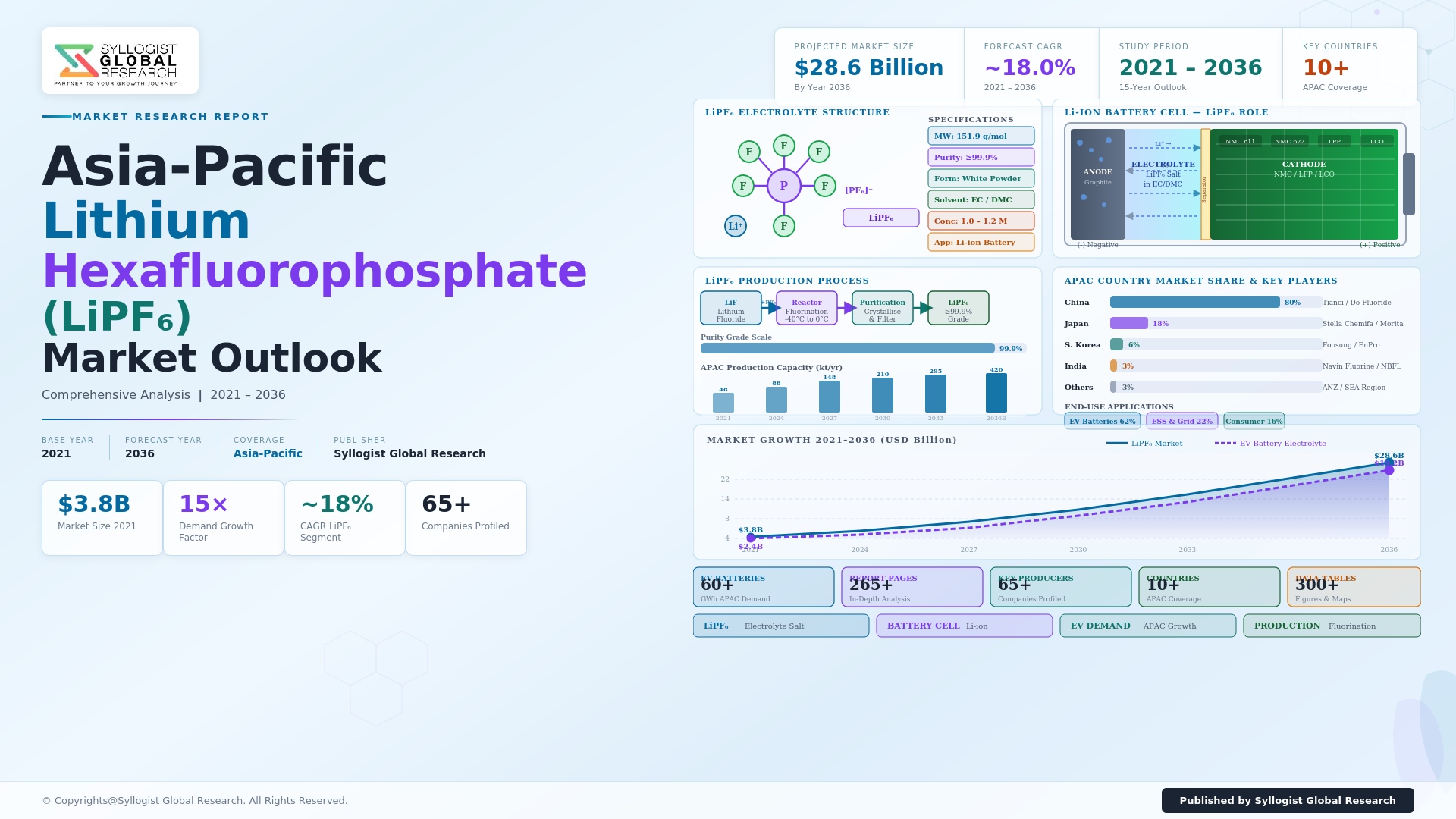

The Asia-Pacific LiPF6 market occupies a structurally pivotal position within the global lithium-ion battery materials value chain, functioning as the single most critical electrolyte input whose purity specification, supply security, and unit pricing directly govern the electrochemical performance, cycle life, and thermal stability parameters of the battery cells manufactured across the region. The Asia-Pacific LiPF6 market was valued at approximately USD 3.6 billion in 2025 and is projected to reach USD 8.7 billion by 2034, advancing at a compound annual growth rate of 10.3% over the forecast period from 2027 to 2034, driven by the accelerating deployment of lithium-ion battery capacity across electric vehicle, energy storage, and consumer electronics end-use segments in China, South Korea, Japan, India, and Southeast Asia. China alone accounts for approximately 76% of Asia-Pacific LiPF6 production capacity in 2025, with major production facilities concentrated in Shandong, Jiangsu, Zhejiang, and Fujian provinces, where integrated fluorochemical industrial parks provide the anhydrous hydrogen fluoride feedstock infrastructure essential for economically viable LiPF6 synthesis at commercial scale. The structural dominance of Asia-Pacific in global LiPF6 supply is reinforced by the co-location of the world’s largest battery cell manufacturing base within the region, with the top five global battery cell manufacturers by installed capacity all operating primary production facilities in China, South Korea, or Japan, creating a proximity-driven supply chain architecture that reduces electrolyte logistics complexity and cold-chain cost while enabling just-in-time delivery models aligned with the inventory management requirements of high-throughput battery cell production lines.

The technology landscape of LiPF6-based electrolyte formulations in Asia-Pacific is undergoing continuous refinement as battery cell manufacturers pursue higher energy density, faster charge capability, and broader operating temperature performance to satisfy the increasingly demanding specifications of next-generation electric vehicle battery packs and grid-scale energy storage systems. Battery electrolyte formulators across China, South Korea, and Japan have invested substantially in the development of functional additive packages that address the intrinsic limitations of standard LiPF6-carbonate electrolyte systems, including the relatively modest thermal decomposition onset temperature of approximately 60 degrees Celsius for dissolved LiPF6 that generates lithium fluoride and phosphorus pentafluoride decomposition products detrimental to solid electrolyte interphase stability under elevated temperature cycling conditions. The integration of fluoroethylene carbonate as a film-forming additive at concentrations of 1% to 10% by weight in commercial electrolyte formulations has substantially improved the cycling stability and capacity retention of silicon-graphite anode battery cells at elevated temperatures, enabling the deployment of higher silicon content anodes that increase gravimetric energy density toward the 300 Wh/kg targets established by leading Asian electric vehicle battery manufacturers for their next-generation cell platforms. High-concentration LiPF6 electrolyte formulations operating at molar concentrations of 2.0 to 5.0 mol/L, sometimes designated as high-concentration or localized high-concentration electrolytes through the dilution of fluorinated ether co-solvents, represent an active area of electrolyte innovation among Asian battery research institutes and cell manufacturers pursuing breakthrough improvements in lithium metal anode compatibility and fast-charging performance that could unlock the next step-change in energy storage technology beyond conventional graphite-anode lithium-ion chemistry.

From a supply chain and raw material perspective, the Asia-Pacific LiPF6 industry is navigating a period of significant structural adjustment following the extreme price volatility experienced between 2021 and 2023, when LiPF6 spot prices in China surged from approximately USD 13,500 per metric ton in early 2021 to a peak exceeding USD 58,000 per metric ton in late 2021 before collapsing back toward USD 8,500 per metric ton by mid-2023 as substantial new production capacity commissioned during the price spike entered operation simultaneously with a temporary moderation in downstream battery demand growth. This price cycle has fundamentally reshaped the competitive dynamics of the Asia-Pacific LiPF6 industry, accelerating consolidation among Chinese producers toward larger, more cost-efficient operations with fully integrated fluorine feedstock supply, while simultaneously incentivizing South Korean and Japanese LiPF6 producers to differentiate on product quality, high-purity specification consistency, and technical service capability for premium battery cell customer segments rather than competing on price with Chinese volume producers. Battery cell manufacturers across Asia-Pacific are additionally responding to LiPF6 supply chain concentration risks by qualifying alternative lithium salt electrolytes including lithium bis(fluorosulfonyl)imide as partial or full replacements in specific cell chemistry applications, though LiPF6 retains compelling cost and ionic conductivity advantages over LiFSI that will sustain its dominance across the majority of commercial lithium-ion battery production in the region through the forecast period.

The competitive landscape of LiPF6 manufacturing in Asia-Pacific is characterized by a pronounced concentration of production capacity among a relatively small number of vertically integrated Chinese producers, supplemented by technologically differentiated Japanese and South Korean manufacturers serving premium battery cell customer segments where ultra-high purity LiPF6 specifications of 99.99% or greater and stringent control of metallic impurity levels below sub-parts-per-billion thresholds command price premiums that insulate non-Chinese producers from direct cost-based competition with Chinese volume suppliers. India represents the most significant emerging production geography within Asia-Pacific for LiPF6 and lithium-ion battery electrolyte materials, with government production-linked incentive schemes targeting battery chemical manufacturing capacity as a strategic national priority, multiple announced investments in fluorochemical and battery electrolyte production facilities, and a rapidly expanding domestic electric vehicle market that generated approximately 1.8 million electric two-wheeler and three-wheeler sales and approximately 90,000 electric four-wheeler sales in fiscal year 2025, collectively establishing a domestic battery demand base that justifies incremental domestic LiPF6 production investment as India’s battery manufacturing ecosystem matures toward commercial scale. Southeast Asian markets including Vietnam, Indonesia, Thailand, and Malaysia are emerging as secondary LiPF6 demand growth centers as electric vehicle assembly investments by Chinese and South Korean automotive manufacturers establish new battery pack and, increasingly, battery cell production operations within the ASEAN region, creating geographically distributed demand nodes that are progressively supplementing the historically China-centric LiPF6 demand concentration pattern across Asia-Pacific.

Key Drivers

Accelerating Electric Vehicle Adoption Across China, India, and Southeast Asia Generating Structural and Sustained Growth in Lithium-Ion Battery Electrolyte Demand The Asia-Pacific region is the epicenter of global electric vehicle adoption, with China sustaining its position as the world’s largest electric vehicle market with approximately 11.3 million new energy vehicle sales recorded in 2025, representing a penetration rate of approximately 38% of total passenger vehicle sales, while India’s electric two-wheeler and three-wheeler market reached 2.1 million units in fiscal year 2025 and is growing at approximately 28% annually as government production-linked incentive programs and state-level subsidy schemes reduce consumer acquisition cost differentials between electric and internal combustion engine alternatives. Electric vehicle battery cell production in Asia-Pacific consumed approximately 196,000 metric tons of LiPF6 in 2025, accounting for the dominant share of total regional LiPF6 demand, and this consumption volume is projected to grow at a compound annual growth rate of 13.6% through 2034 as electric vehicle production volumes scale across China, South Korea, Japan, India, and increasingly Southeast Asian manufacturing hubs in Vietnam, Indonesia, and Thailand. The hybridization of national industrial policies across Asia-Pacific governments, combining electric vehicle purchase subsidies, internal combustion engine phase-out timelines, domestic battery manufacturing incentives, and public charging infrastructure investment programs, creates a durable and policy-reinforced demand foundation for LiPF6 that is structurally decoupled from short-term consumer sentiment fluctuations and insulated from near-term macroeconomic headwinds that might otherwise moderate electric vehicle adoption velocity across individual regional markets.

Grid-Scale Energy Storage System Deployment Creating a Rapidly Expanding Non-Automotive Demand Pool for High-Purity LiPF6 Grid-scale stationary energy storage systems using lithium-iron-phosphate and nickel-manganese-cobalt battery cell chemistries are being deployed at accelerating pace across Asia-Pacific to support renewable energy integration, peak demand shaving, and grid frequency stabilization objectives embedded within the national energy transition policy frameworks of China, Australia, Japan, South Korea, and India, generating a large and structurally growing non-automotive LiPF6 demand stream that now represents approximately 22% of total regional LiPF6 consumption in 2025 and is growing faster than automotive demand on a percentage basis as utility-scale storage project pipelines across the region reach commercial operation. China’s National Development and Reform Commission and National Energy Administration jointly issued targets requiring 30 gigawatt-hours of new electrochemical energy storage installation by 2025, a figure that was exceeded with approximately 38 gigawatt-hours of new capacity commissioned, with cumulative installed electrochemical energy storage capacity in China reaching approximately 79 gigawatt-hours at year-end 2025 and generating LiPF6 demand of approximately 31,000 metric tons annually from the energy storage sector alone. Australia’s rapidly expanding utility-scale battery storage market, driven by the Capacity Investment Scheme and state-level renewable energy zone development programs, South Korea’s Energy Storage System Safety and Promotion Act providing fiscal incentives for grid storage deployment, and India’s National Electricity Plan mandating 51.5 gigawatts of battery energy storage by 2032 collectively constitute a multi-country policy architecture that structurally guarantees sustained and growing LiPF6 demand from the energy storage segment through the forecast period, partially insulating regional LiPF6 producers from dependence on automotive demand cycle dynamics.

Vertical Integration Investments by Asian Battery Cell Manufacturers Driving Upstream LiPF6 Capacity Expansion and Long-Term Supply Agreement Structures Leading Asian battery cell manufacturers including those domiciled in China, South Korea, and Japan are pursuing aggressive vertical integration strategies that extend upstream from cell manufacturing into electrolyte production and, in some cases, LiPF6 synthesis, driven by the strategic imperative to secure cost-competitive, specification-consistent electrolyte supply as battery production volumes scale toward multi-hundred gigawatt-hour annual capacities that expose cell manufacturers to material supply concentration risks if sourced exclusively from independent third-party LiPF6 producers. The strategic logic of vertical integration in electrolyte supply is reinforced by the proprietary nature of electrolyte additive formulations that constitute a core competency for battery manufacturers seeking to differentiate their cell performance characteristics from competitors, with electrolyte formulation know-how becoming increasingly difficult to protect when electrolyte procurement is managed through arm’s length commercial relationships with independent formulators. Long-term supply agreements with durations of five to ten years, incorporating committed volume offtake obligations, co-investment in dedicated production capacity, and joint specification development protocols, have become the dominant commercial structure governing LiPF6 supply relationships between major producers and battery cell manufacturer customers across Asia-Pacific, providing LiPF6 manufacturers with revenue visibility and capital investment justification for capacity expansion programs while simultaneously securing battery cell manufacturers against the supply disruptions and price volatility that characterized spot market LiPF6 procurement during the 2021 to 2022 price spike cycle.

Key Challenges

Fluorine Supply Chain Concentration, Anhydrous Hydrogen Fluoride Handling Hazards, and Environmental Regulatory Pressure on Fluorochemical Manufacturing Operations The synthesis of LiPF6 is fundamentally dependent on anhydrous hydrogen fluoride as a primary fluorine-source reagent, and the geographic concentration of commercial anhydrous hydrogen fluoride production capacity within a small number of fluorite-mining and fluorochemical processing clusters in China, Mexico, South Africa, and Mongolia creates a structural supply security vulnerability for LiPF6 manufacturers that is amplified by the extreme toxicity, corrosivity, and regulatory sensitivity of anhydrous hydrogen fluoride as an industrial chemical whose transport, storage, and handling are subject to increasingly stringent safety and environmental regulations across Asia-Pacific jurisdictions. Chinese regulators have progressively tightened environmental discharge standards and safety management requirements applicable to fluorochemical production facilities in response to a series of industrial accidents involving hydrogen fluoride releases, resulting in periodic capacity curtailments at fluorite processing and hydrofluoric acid production facilities that propagate upstream supply disruptions into the LiPF6 supply chain with limited warning time and significant price impact. The disposal of fluorine-containing process waste streams generated during LiPF6 synthesis, including phosphorus trifluoride and phosphorus oxyfluoride byproducts and fluoride-contaminated process water, is subject to increasingly prescriptive environmental control requirements across China, South Korea, Japan, and India that increase the capital and operating cost of regulatory compliance for LiPF6 manufacturers and create permitting barriers that slow the pace of new production capacity approvals in established manufacturing geographies.

Competitive Pressure from Alternative Lithium Salt Electrolytes and the Structural Risk of LiPF6 Substitution in Next-Generation Battery Chemistries Lithium bis(fluorosulfonyl)imide has emerged as the most commercially significant alternative lithium salt to LiPF6 in Asia-Pacific battery electrolyte markets, offering superior thermal stability with a decomposition onset temperature exceeding 200 degrees Celsius compared to approximately 60 degrees Celsius for LiPF6, better ionic conductivity at low temperatures relevant to cold-climate electric vehicle applications, and reduced sensitivity to trace moisture contamination that simplifies electrolyte manufacturing process control requirements. LiFSI adoption in commercial battery electrolyte formulations has accelerated as Chinese LiFSI producers have reduced production costs through process optimization and scale expansion, narrowing the cost premium of LiFSI relative to LiPF6 from approximately USD 60,000 to USD 70,000 per metric ton in 2020 toward USD 18,000 to USD 22,000 per metric ton in 2025, reaching a cost threshold at which LiFSI is economically viable as a partial co-salt with LiPF6 or as a primary salt in performance-optimized electrolyte formulations for premium electric vehicle battery applications. The development of solid-state electrolyte systems using lithium-phosphorus-oxynitride, lithium-lanthanum-zirconium-oxide sulfide-based inorganic conductors, and polymer-ceramic composite electrolytes by leading Asian battery manufacturers represents a longer-term structural substitution risk for LiPF6 that, while unlikely to generate material LiPF6 demand displacement within the forecast period to 2034, introduces strategic uncertainty into capacity investment decisions for LiPF6 manufacturers planning capital commitments with 15-to-20-year asset life horizons.

Lithium Carbonate and Lithium Hydroxide Feedstock Price Volatility Transmitting Upstream Commodity Cycle Risk into LiPF6 Manufacturing Cost Structures LiPF6 manufacturing cost is materially exposed to lithium carbonate and lithium hydroxide spot price dynamics through the lithium fluoride intermediate production step, with lithium raw material costs representing approximately 18% to 25% of total LiPF6 production cost at prevailing lithium prices in 2025, creating a feedstock cost pass-through mechanism that complicates long-term fixed-price supply contracting between LiPF6 producers and battery cell manufacturer customers and generates earnings volatility for LiPF6 manufacturers operating under commercial contracts that lag spot lithium market movements by six to twelve months. The lithium carbonate spot price in China experienced extraordinary volatility between 2021 and 2024, rising from approximately USD 8,500 per metric ton in January 2021 to a peak of approximately USD 81,000 per metric ton in November 2022 before declining sharply to approximately USD 11,000 per metric ton by December 2024 as expanded hard rock and brine lithium production from Australia, Chile, Argentina, and China simultaneously reached the market. LiPF6 manufacturers across Asia-Pacific have responded to lithium feedstock cost volatility by implementing lithium price indexation mechanisms in customer supply agreements, establishing lithium raw material procurement hedging programs through forward purchase contracts with Australian and South American lithium producers, and in certain cases investing in upstream lithium resource equity stakes or offtake agreements that provide partial insulation from spot market exposure, though the inherent lag between lithium market movements and contracted LiPF6 price adjustment mechanisms continues to create timing mismatches that generate margin compression during periods of rapidly rising lithium feedstock costs.

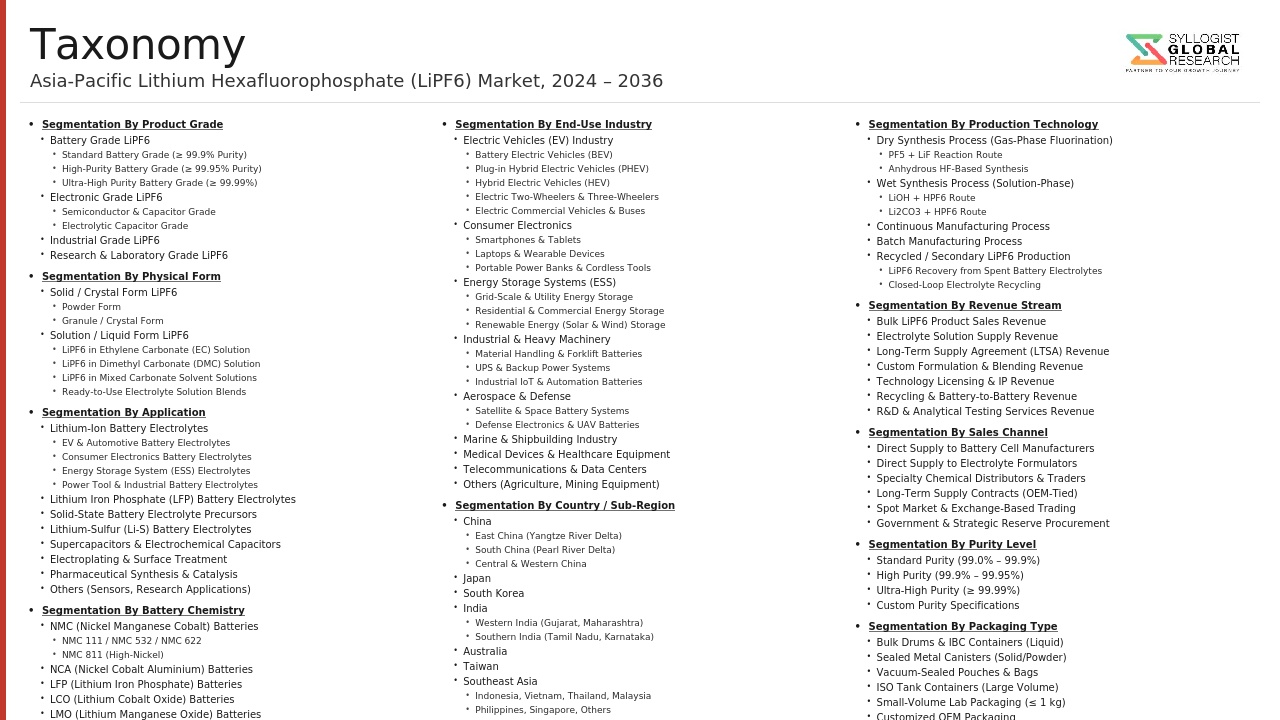

Market Segmentation

- Segmentation By Product Form

- Anhydrous LiPF6 Crystal and Powder

- LiPF6 Electrolyte Solution (Standard Concentration)

- LiPF6 Electrolyte Solution (High Concentration)

- LiPF6 Electrolyte Solution with Functional Additive Packages

- Others

- Segmentation By Purity Grade

- Battery Grade (99.9% Purity)

- Ultra-High Purity Battery Grade (99.99% Purity and Above)

- Industrial Grade

- Others

- Segmentation By Electrolyte Additive Composition

- Standard LiPF6-Carbonate Electrolyte (No Additives)

- LiPF6 Electrolyte with Vinylene Carbonate Additive

- LiPF6 Electrolyte with Fluoroethylene Carbonate Additive

- LiPF6 Electrolyte with LiFSI Co-Salt

- LiPF6 Electrolyte with Multi-Functional Additive Blends

- Others

- Segmentation By Application

- Electric Vehicle Battery Cells (BEV and PHEV)

- Hybrid Electric Vehicle Battery Cells

- Consumer Electronics Batteries (Smartphones, Laptops, Tablets)

- Grid-Scale Stationary Energy Storage Systems

- Industrial and Commercial Energy Storage

- Power Tools and Portable Equipment Batteries

- Others

- Segmentation By Battery Cell Chemistry

- Lithium Iron Phosphate (LFP) Cells

- Nickel Manganese Cobalt (NMC) Cells

- Nickel Cobalt Aluminum (NCA) Cells

- Lithium Manganese Oxide (LMO) Cells

- Others

- Segmentation By End User

- Battery Cell Manufacturers

- Battery Module and Pack Assemblers

- Electric Vehicle Original Equipment Manufacturers (OEMs)

- Consumer Electronics Manufacturers

- Energy Storage System Integrators

- Others

- Segmentation By Sales Channel

- Direct Supply Under Long-Term Offtake Agreements

- Spot Market and Short-Term Contract Sales

- Electrolyte Formulator Intermediary Channel

- Distributor and Trading Company Channel

- Others

- Segmentation By Country

- China

- Japan

- South Korea

- India

- Australia

- Southeast Asia (Vietnam, Indonesia, Thailand, Malaysia, and Others)

- Rest of Asia-Pacific

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total Asia-Pacific market valuation of the Lithium Hexafluorophosphate (LiPF6) Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by product form, purity grade, application, battery cell chemistry, end user, and country, to enable LiPF6 producers, electrolyte formulators, battery cell manufacturers, electric vehicle OEMs, and investors to identify which product segments and geographic markets will generate the highest absolute revenue and the most durable growth trajectory across the forecast period?

- How is the competitive landscape of LiPF6 manufacturing in Asia-Pacific structured across Chinese volume producers, Japanese and South Korean premium-grade manufacturers, and emerging Indian producers, and what are the respective cost structures, purity specification capabilities, vertical integration degrees, customer relationship profiles, capacity expansion programs, and strategic differentiation approaches of leading regional producers as they navigate the transition from a supply-constrained high-price environment toward a more balanced market characterized by competitive pricing pressure and increasing customer quality requirements?

- What is the projected consumption volume of LiPF6 attributable to grid-scale stationary energy storage systems across Asia-Pacific through 2034, disaggregated by country, battery chemistry, and project type, and how will the relative growth rates of energy storage versus electric vehicle LiPF6 demand evolve across the forecast period as renewable energy integration requirements accelerate utility-scale battery storage deployment in China, Australia, India, South Korea, and Southeast Asian markets?

- How are the competitive economics of LiPF6 versus lithium bis(fluorosulfonyl)imide evolving in Asia-Pacific electrolyte formulations for electric vehicle battery applications, at what cost crossover points and performance threshold conditions does LiFSI substitution for LiPF6 become commercially rational for specific battery cell chemistry and application combinations, and what is the projected market share trajectory for LiFSI co-salt and full-substitution electrolyte formulations relative to conventional LiPF6-carbonate electrolyte systems across the forecast period?

- What are the fluorine feedstock supply chain risks, anhydrous hydrogen fluoride procurement strategies, environmental regulatory compliance cost trajectories, and lithium carbonate price hedging mechanisms employed by leading Asia-Pacific LiPF6 manufacturers, and how are these raw material and regulatory risk management approaches influencing capacity location decisions, production cost structures, and customer contract pricing architectures as producers seek to insulate operating margins from the commodity cycle volatility that characterized the LiPF6 and upstream material price environment between 2021 and 2024?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Sub-Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Hydrofluoric Acid (HF) & Phosphorus Pentafluoride (PF5) Feedstock Supply Concentration & Price Volatility Risk

- LiPF6 Market Oversupply, Capacity Overbuild & Price Collapse Risk Following China Gigafactory Expansion Wave

- Technology Substitution Risk: LiFSI, LiDFOB & Solid-State Electrolyte Displacement of LiPF6 in Next-Generation Battery Chemistries

- Geopolitical, Export Control & Critical Mineral Supply Chain Disruption Risk in Asia-Pacific Fluorine & Lithium Chemical Value Chain

- Environmental, Safety & Regulatory Compliance Risk for HF Handling, Fluorine Waste & LiPF6 Manufacturing Plant Operation

- Regulatory Framework & Standards

- China LiPF6 Industry Policy: MIIT Battery Material Standard (GB/T Series), Fluorine Chemical Industry Regulation, Environmental Supervision of HF Production & National New Energy Vehicle (NEV) Battery Supply Chain Policy

- Japan & South Korea Battery Material Regulation: METI Battery Material Quality Standard, JIS Chemical Safety Regulation, K-Battery Strategy & Critical Mineral Supply Chain Security Framework for LiPF6 & Electrolyte Salt

- Hazardous Chemical Safety & Environmental Standards: GHS SDS for LiPF6, HF & PF5, China Hazardous Chemical Catalogue, Japan PRTR Chemical Release Reporting & Korea Chemical Control Act Compliance

- Battery Regulation & Recycled Content Standards Impacting LiPF6 Demand: EU Battery Regulation (2023/1542) Asia Export Compliance, China GB Battery Recycling Standard & South Korea Battery Resource Circulation Act

- Critical Mineral & Fluorine Supply Chain Policy: China Fluorite Export Quota & Mining Regulation, Japan Critical Mineral Strategy, India Critical Mineral Mission & ASEAN Battery Material Localisation Policy

- Asia-Pacific Lithium Hexafluorophosphate (LiPF6) Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Metric Tonnes)

- Market Size & Forecast by Product Grade

- Battery Grade LiPF6 (Purity Above 99.99%: Ultra-High Purity for EV & BESS)

- High-Purity Battery Grade LiPF6 (99.95% to 99.99%: Standard EV & Consumer Electronics)

- Standard Battery Grade LiPF6 (99.9% to 99.95%)

- Anhydrous LiPF6 Solution & Pre-Formulated Electrolyte Base

- Market Size & Forecast by Application

- EV & xEV Battery Electrolyte (BEV, PHEV & HEV Traction Battery)

- Stationary Energy Storage System (BESS, Grid-Scale & Behind-the-Meter)

- Consumer Electronics Battery (Smartphone, Laptop, Tablet & Wearable)

- E-Bike, E-Scooter, E-Motorcycle & Light Electric Vehicle Battery

- Power Tool, Industrial Equipment & Commercial Battery

- Research, Specialty & Emerging Application

- Market Size & Forecast by Battery Chemistry

- NMC (Nickel Manganese Cobalt Oxide) Battery: LiPF6-Based Electrolyte for High-Energy EV Application

- LFP (Lithium Iron Phosphate) Battery: LiPF6-Based Electrolyte for Standard EV, BESS & LFP Gigafactory

- NCA (Nickel Cobalt Aluminium) Battery: LiPF6 Electrolyte for High-Performance EV

- LCO (Lithium Cobalt Oxide) Battery: LiPF6 Electrolyte for Consumer Electronics

- Next-Generation Cell Chemistry: LiPF6 Role in LMFP, High-Nickel & Silicon Anode Electrolyte

- Market Size & Forecast by Packaging Form

- Drum (25 kg & 50 kg Standard Industrial Drum)

- Small Pack (1 kg & 5 kg Bag for R&D & Specialty Use)

- IBC & Bulk Container (500 kg to 1,000 kg for Large Volume Customers)

- Pre-Formulated Liquid Electrolyte Solution (LiPF6 Dissolved in Carbonate Solvent Mix)

- Market Size & Forecast by End-User

- Li-Ion Battery Cell Manufacturer & Gigafactory Operator (CATL, BYD, CALB, Panasonic, Samsung SDI, LG Energy Solution, SK On)

- Electrolyte Formulator & Electrolyte Manufacturer (Capchem, Guotai Huarong, Tinci Materials, Shanshan)

- EV OEM with Integrated Battery Manufacturing (BYD, SAIC, Geely, Toyota, Hyundai)

- Consumer Electronics & Power Tool Battery Manufacturer

- Energy Storage System (ESS) Integrator & BESS Developer

- Market Size & Forecast by Sales Channel

- Direct Long-Term Supply Agreement (LTA) to Battery Cell Manufacturer & Electrolyte Formulator

- Chemical Distributor, Trading Company & Spot Market Channel

- Toll Manufacturing, Custom Grade Processing & Technical Service

- Online B2B Chemical Platform & E-Commerce Channel

- China Lithium Hexafluorophosphate (LiPF6) Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Product Grade

- By Application

- By Battery Chemistry

- By Packaging Form

- By End-User

- By Production vs. Consumption Balance

- By Country

- By Sales Channel

- Market Size & Forecast

- Japan & South Korea Lithium Hexafluorophosphate (LiPF6) Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Product Grade

- By Application

- By Battery Chemistry

- By Packaging Form

- By End-User

- By Production vs. Consumption Balance

- By Country

- By Sales Channel

- Market Size & Forecast

- Southeast Asia Lithium Hexafluorophosphate (LiPF6) Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Product Grade

- By Application

- By Battery Chemistry

- By Packaging Form

- By End-User

- By Production vs. Consumption Balance

- By Country

- By Sales Channel

- Market Size & Forecast

- India & South Asia Lithium Hexafluorophosphate (LiPF6) Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Product Grade

- By Application

- By Battery Chemistry

- By Packaging Form

- By End-User

- By Production vs. Consumption Balance

- By Country

- By Sales Channel

- Market Size & Forecast

- Oceania & Rest of Asia-Pacific Lithium Hexafluorophosphate (LiPF6) Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Product Grade

- By Application

- By Battery Chemistry

- By Packaging Form

- By End-User

- By Production vs. Consumption Balance

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Asia-Pacific Lithium Hexafluorophosphate (LiPF6) Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Product Grade

- By Application

- By Battery Chemistry

- By Packaging Form

- By End-User

- By Production vs. Consumption Balance

- By Country

- By Sales Channel

- Market Size & Forecast

*Countries Analyzed in the Syllogist Asia-Pacific Research Portfolio: China, Japan, South Korea, Taiwan, India, Indonesia, Vietnam, Thailand, Malaysia, Philippines, Singapore, Australia, New Zealand, Bangladesh, Pakistan, Sri Lanka

- Technology Landscape & Innovation Analysis

- LiPF6 Synthesis Technology Deep-Dive: LiF plus PF5 Gas-Phase Route, Li2CO3 plus HF plus PCl5 Wet Process & Continuous Reactor Design for Battery Grade Yield Optimisation

- High-Purity LiPF6 Purification, Recrystallisation & Solvent Removal Technology for Ultra-High Purity Battery Grade Quality

- Hydrofluoric Acid (HF), Phosphorus Pentafluoride (PF5) & Fluorite (CaF2) Raw Material Production, Handling & Integration Technology

- Next-Generation Electrolyte Salt Technology: LiFSI, LiDFOB, LiFTFSI & Multi-Salt Electrolyte Formulation as LiPF6 Performance Enhancer or Substitute

- Solid-State Electrolyte & Next-Generation Battery Technology Impact on LiPF6 Demand: All-Solid-State, Semi-Solid & Lithium Metal Battery Transition Timeline Analysis

- LiPF6 Recycling, Spent Electrolyte Recovery & Circular Fluorine and Lithium Value Chain Technology

- Quality Control, Analytical Metrology, ICP-MS Trace Metal Analysis & In-Process LiPF6 Purity Monitoring Technology

- Patent & IP Landscape in LiPF6 Production & Advanced Electrolyte Salt Technologies Across Asia-Pacific

- Value Chain & Supply Chain Analysis

- Upstream Raw Material Supply Chain: Lithium Carbonate & LiOH (Australia, Chile & China Upstream), Fluorspar/Fluorite (China, Mexico), HF Production & PF5 Manufacturing

- LiPF6 Manufacturing & Production Capacity Landscape: China Domestic Producers, Japan & South Korea Specialty Producers & Emerging India/Southeast Asia Investment

- Electrolyte Formulation & Blending: Electrolyte Manufacturer Integration of LiPF6 with Carbonate Solvent (EC, DMC, EMC, DEC) & Additive Mix

- Battery Cell Manufacturer Integration: LiPF6 Procurement, Electrolyte Qualification, Cell Formation & Battery Pack Integration

- EV OEM, ESS Integrator & Consumer Electronics Brand Downstream Demand Channel

- Chemical Distributor, Trader & Spot Market Channel Across Asia-Pacific

- End-of-Life Battery Recycling, Black Mass Processing & Electrolyte Salt Recovery Circular Economy

- Pricing Analysis

- LiPF6 Spot & Contract Price Analysis (USD/kg & CNY/tonne): China Domestic Market, Japan Specialty & Export Price Historical Trend 2019-2024 & Forecast 2025-2034

- LiPF6 Price Cycle Analysis: 2021-2022 Supercycle Peak, 2023-2024 Price Collapse & Recovery Scenario from China Capacity Overbuild

- Battery Grade vs. Standard Grade LiPF6 Price Premium Analysis by Purity Level & Application

- LiPF6 Production Cost Analysis: Raw Material (LiOH, HF, PF5) Cost Structure, Energy Cost & Manufacturing Cost per kg by Producer Location

- LiFSI & Next-Generation Salt Price Premium vs. LiPF6 Benchmark: Cost Parity Roadmap & Blending Economics

- LiPF6 Import-Export Price Differential Across Asia-Pacific: China Export Price, Japan & South Korea Specialty Premium & India Import Cost Build-Up

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of LiPF6 Production: Carbon Footprint, Energy Intensity, HF Emission & Fluorine Waste Generation per Kilogram LiPF6 Manufactured

- Hydrofluoric Acid (HF) Hazard Management, Fluorine Waste Treatment, Scrubber Technology & Environmental Compliance at LiPF6 Production Facility

- Circular Economy & Battery Electrolyte Recycling: LiPF6 Recovery from Spent Battery Black Mass, Electrolyte Solvent Regeneration & Closed-Loop Fluorine Value Chain

- Critical Mineral Supply Chain Sustainability: Responsible Fluorite Sourcing, Lithium Supply Traceability & OECD Due Diligence for LiPF6 Feedstock in Asia-Pacific

- Regulatory-Driven Sustainability: EU Battery Regulation Carbon Footprint Declaration for Electrolyte Materials, China Green Battery Supply Chain Standard & South Korea Battery ESG Disclosure for LiPF6 Producers

- Competitive Landscape

- Market Structure & Concentration

- Asia-Pacific LiPF6 Market Consolidation Level: China Domestic Dominance vs. Japan & South Korea Specialty Segment

- Top 10 Players Market Share by Production Volume & Revenue

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Product Grade, Application & Sub-Region

- Player Classification

- China Large-Scale LiPF6 Producer (Jiangsu Jiujiujiu Technology, Tianjin Jinniu, Stella Chemifa Suzhou, Foolung & Do-Fluoride New Materials)

- China Vertically Integrated LiPF6 & Electrolyte Company (Shenzhen Capchem, Guotai Huarong, Shanshan, Tinci Materials)

- Japan High-Purity LiPF6 Specialty Producer (Stella Chemifa, Morita Chemical Industries, Kanto Denka Kogyo)

- South Korea LiPF6 & Electrolyte Supplier (Foosung, ENF Technology, Dongwha Electrolyte)

- Battery Cell Manufacturer with Electrolyte & LiPF6 Vertical Integration

- Emerging LiPF6 Producer in India & Southeast Asia (Pilot & Investment Stage)

- Chemical Distributor & Trading Company Serving Asia-Pacific LiPF6 Market

- Next-Generation Electrolyte Salt Company (LiFSI, LiDFOB Specialist)

- Competitive Analysis Frameworks

- Market Share Analysis by Product Grade, Application & Sub-Region

- Company Profile

- Company Overview & Headquarters

- LiPF6 Product Grade Portfolio & Purity Capability

- Key Customer Relationships & Long-Term Supply Agreements

- Production Facility Location & Annual LiPF6 Nameplate Capacity (Metric Tonnes)

- Revenue (LiPF6 Segment) & Financial Performance

- Technology Differentiators & IP Portfolio

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Capacity Expansion, New Customer Wins, Quality Certifications)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Purity Capability vs. Production Scale)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Product Grade, Application, Battery Chemistry, End-User & Sub-Region

- White Space Opportunity Analysis

- Strategic Output

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing Capacity, Purity Upgrade & Operational Excellence Strategy

- Geographic Expansion & Asia-Pacific Sub-Region Localisation Strategy

- Customer & Battery Manufacturer Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability, Circular Fluorine & ESG Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)