Market Definition

The Global Mining Electrification Technologies Market encompasses the design, engineering, manufacturing, integration, and commercial deployment of electrical power systems, battery and fuel cell propulsion platforms, electrified mining equipment, and supporting energy infrastructure used to replace diesel-powered and fossil fuel-dependent machinery, processes, and utilities across surface and underground mining operations in the extraction of metallic ores, industrial minerals, coal, and construction aggregates. Mining electrification technologies span a broad and technically diverse product and system portfolio including battery electric vehicles encompassing electric haul trucks, electric load-haul-dump machines, electric drill rigs, electric bolters, electric utility vehicles, and electric conveyors, fuel cell electric vehicles utilizing hydrogen as an energy carrier for high-duty-cycle heavy mining equipment, fixed and mobile battery energy storage systems for mine site energy management and peak shaving, renewable energy generation systems including solar photovoltaic, wind, and hybrid microgrids designed specifically for remote mine site power supply, high-voltage direct current and medium-voltage alternating current underground mine electrification systems, trolley assist systems for open-pit haul roads, electrified material handling and conveying systems, and the associated digital energy management, charging infrastructure, fleet management, and grid integration platforms required to operate electrified mine sites at commercial scale. The market encompasses the complete electrification value chain from technology development and equipment manufacturing through system integration, mine infrastructure electrification, equipment commissioning, fleet conversion support, operator training, predictive maintenance services, and lifecycle energy optimization that define the total commercial relationship between mining electrification technology providers and mining operators across all major commodity and geographic markets globally. Key participants include original equipment manufacturers of electrified mining machinery, battery system developers, fuel cell technology providers, renewable energy developers, electrical infrastructure contractors, mining companies driving adoption, and regulatory bodies setting emissions and ventilation standards.

Market Insights

The global mining electrification technologies market was valued at approximately USD 7.3 billion in 2025 and is projected to reach USD 24.8 billion by 2034, advancing at a compound annual growth rate of 14.6% over the forecast period from 2027 to 2034, driven by the convergence of tightening mine site emissions regulations, the rapidly declining total cost of ownership of battery electric mining equipment relative to diesel alternatives as battery energy density improves and pack costs decline, escalating corporate decarbonization commitments by major global mining companies, and the growing recognition among mine operators that electrification delivers operational advantages beyond emissions reduction including improved underground air quality, reduced ventilation requirements, lower heat generation, and superior torque and speed control characteristics that improve equipment productivity and operator working conditions simultaneously. Global diesel fuel consumption within the mining sector was estimated at approximately 82 billion liters in 2025, representing approximately 7% of total global diesel consumption and generating approximately 215 million metric tons of carbon dioxide equivalent annually, with diesel propulsion and power generation collectively accounting for 30% to 50% of total mine site operating costs depending on mine type, geographic remoteness, and commodity produced, creating a compelling total cost of ownership case for electrification investment that is increasingly commercially decisive independent of regulatory or sustainability pressures. Battery electric vehicle penetration within the total global mining equipment fleet reached approximately 4.8% by unit count in 2025, concentrated predominantly in underground hard rock mining applications where diesel elimination delivers the highest operational value through ventilation cost reduction and improved air quality, with penetration projected to expand to approximately 22.4% by 2034 as product range maturity, battery performance confidence, and charging infrastructure availability progressively extend battery electric vehicle viability into surface mining and broader underground soft rock mining applications.

The underground hard rock mining segment represents the most commercially advanced and fastest-growing application category within the global mining electrification technologies market, accounting for approximately 54% of total market revenue in 2025, driven by the operational economics of diesel elimination underground where ventilation systems required to dilute and extract diesel exhaust gases represent 30% to 50% of total underground mine energy consumption, meaning that converting underground fleets from diesel to battery electric propulsion generates ventilation energy savings of approximately USD 1.2 to USD 2.8 million per year for a mid-scale underground mine of 3,000 to 5,000 tonnes per day production capacity, creating a direct and quantifiable financial return on battery electric vehicle investment that accelerates payback periods toward three to five years for many underground fleet conversion programs. Epiroc and Sandvik, the two leading underground mining equipment manufacturers globally, have each committed to offering fully electrified versions of their complete underground product portfolios by 2030 and have already commercialized battery electric versions of their flagship load-haul-dump machines, underground drill rigs, and utility vehicles that are operating in production deployments across mines in Canada, Sweden, Australia, Chile, and South Africa, providing the commercial reference installations and operational performance data that are accelerating adoption decisions by mine operators who require demonstrated productivity and reliability evidence before committing to large-scale fleet electrification programs. The battery electric load-haul-dump machine segment is the most commercially mature product category, with Epiroc’s Scooptram ST14 Battery, Sandvik’s LH518B, and Normet’s Charmec electric bolter accumulating substantial operating hours across multiple continents, collectively validating battery electric performance in the demanding duty cycles, variable grades, and confined space operating conditions that characterize underground hard rock mining environments.

The surface mining electrification segment, encompassing battery electric and trolley-assist systems for large open-pit haul trucks, electric rope and hydraulic shovels, electric blast hole drills, and electrified crushing and conveying systems, represents the highest-volume and longest-term growth opportunity within the global mining electrification technologies market, as surface haul trucks operating in large open-pit copper, iron ore, gold, and coal mines constitute the single largest category of diesel consumption within the global mining sector and their electrification offers the largest absolute emissions reduction and fuel cost saving opportunity per machine, with a fleet of 50 large diesel haul trucks of 220 to 300 tonne payload capacity consuming approximately 180 to 220 million liters of diesel fuel annually at a fuel cost of approximately USD 180 to USD 220 million at prevailing diesel prices. Komatsu’s 930E-5 electric drive haul truck, Caterpillar’s 794 AC electric drive series, and Liebherr’s T 284 represent the dominant conventional electric drive platform architecture in surface mining, where diesel engines power AC generators that drive electric wheel motors, a hybrid architecture that positions these machines for battery or trolley-assist augmentation as the next electrification step without requiring complete drivetrain replacement. The trolley assist system market for large open-pit mines, in which overhead wire electrical infrastructure provides mains power to electric drive haul trucks on uphill loaded travel segments, is experiencing renewed commercial interest with installations advancing at major copper mines in Chile, Zambia, and the Democratic Republic of Congo, at iron ore mines in Sweden and Brazil, and at coal mines in Germany, where trolley assist has demonstrated fuel consumption reductions of 30% to 50% on equipped haul road segments and provides a commercially viable near-term electrification step for large surface mining fleets ahead of full battery electric haul truck commercialization at ultra-class payload capacities.

The mine site renewable energy and energy storage infrastructure segment is emerging as the fastest-growing component of the broader mining electrification market, with mining companies increasingly deploying integrated solar, wind, and battery energy storage microgrids at remote mine sites to reduce diesel generator dependency for site power generation, lower electricity procurement costs, improve energy security, and provide the renewable electricity supply required to genuinely decarbonize electrified mining equipment operations rather than merely substituting diesel engine emissions with grid electricity emissions from fossil fuel-powered grids. The average grid electricity cost for connected mine sites in Chile’s Atacama region declined to approximately USD 0.062 per kilowatt-hour in 2025 following large-scale solar capacity deployment in the region, compared to diesel generation costs of approximately USD 0.18 to USD 0.28 per kilowatt-hour at remote mines without grid access, creating a powerful economic incentive for renewable energy investment at off-grid mining operations globally. BHP, Rio Tinto, Anglo American, Freeport-McMoRan, and Glencore have each announced multi-hundred-million-dollar renewable energy and electrification investment programs targeting net-zero or significant emissions reduction commitments between 2030 and 2050, with BHP’s USD 400 million investment in renewable energy and electrification at its Escondida copper mine in Chile, Rio Tinto’s partnership with Caterpillar for autonomous battery electric haul truck development at Pilbara iron ore operations, and Anglo American’s FutureSmart Mining program incorporating full surface mine electrification demonstrations at its Mogalakwena platinum group metals mine in South Africa collectively illustrating the scale and ambition of mining company electrification investment commitments that are driving sustained and accelerating demand for mining electrification technologies across all major commodity sectors through the forecast period.

Key Drivers

Compelling Total Cost of Ownership Advantage of Battery Electric Mining Equipment Over Diesel Alternatives Driven by Ventilation Savings, Fuel Cost Elimination, and Maintenance Cost Reduction

The total cost of ownership economics of battery electric mining equipment relative to equivalent diesel-powered machines have undergone a fundamental and commercially decisive improvement over the past five years, driven by the convergence of declining battery pack costs, improving energy density and cycle life specifications, rising diesel fuel prices, and the growing quantification of indirect operational savings from ventilation energy reduction, heat load management, and maintenance interval extension that collectively shift the financial case for electrification from a regulatory compliance or sustainability investment to a core operational cost optimization decision for mining operators. Battery pack costs for mining applications declined from approximately USD 420 per kilowatt-hour in 2020 to approximately USD 195 per kilowatt-hour in 2025 and are projected to reach approximately USD 110 per kilowatt-hour by 2030, directly reducing the capital cost premium of battery electric mining equipment relative to diesel equivalents and shortening fleet conversion payback periods to commercially acceptable thresholds across an expanding range of mine types and operating conditions. Underground mines transitioning complete diesel fleets to battery electric propulsion are achieving total annual operating cost reductions of USD 3 to USD 8 million per 1,000 tonnes per day of production capacity through the combined effect of diesel fuel cost elimination, ventilation energy savings arising from the removal of diesel exhaust dilution requirements, reduced engine and drivetrain maintenance costs attributable to the simpler mechanical architecture of electric drive systems, and lower heat generation underground that reduces cooling and air conditioning energy requirements, creating a multi-lever cost reduction case that is increasingly capable of justifying battery electric fleet investment on financial returns alone without requiring any carbon price or regulatory emissions compliance consideration.

Tightening Underground Mine Ventilation and Emissions Regulations Across Major Mining Jurisdictions Accelerating Mandatory Diesel Equipment Phase-Out Timelines

Regulatory frameworks governing diesel particulate matter exposure, nitrogen oxide concentrations, and carbon monoxide levels in underground mine environments across Canada, Australia, the United States, Chile, South Africa, and the European Union are progressively tightening permissible exposure limits and introducing mandatory diesel equipment phase-out timelines that create compliance-driven adoption requirements for battery electric and fuel cell alternatives regardless of cost premium or operational readiness considerations at individual mine sites. Canada’s province of Ontario, which hosts a significant concentration of the world’s underground hard rock nickel, gold, and copper mines, introduced binding regulations under the Occupational Health and Safety Act requiring all diesel-powered underground mining equipment to comply with new diesel particulate matter exposure limits that in many cases cannot be achieved without either complete engine replacement or fleet electrification, effectively mandating battery electric vehicle adoption for Ontario mine operators seeking to maintain production without disproportionate ventilation infrastructure capital expenditure. Australia’s mining safety regulators in New South Wales, Queensland, and Western Australia have similarly updated diesel engine exhaust standards for underground mines, with the New South Wales Resources Regulator publishing a diesel particulate matter action plan that establishes a clear regulatory pathway toward zero-emission underground equipment requirements. The European Union’s revised directive on the protection of workers from risks related to carcinogen exposure, which classifies diesel engine exhaust as a Group 1 carcinogen and establishes new permissible exposure limits at substantially lower concentrations than previously applicable standards, is extending the regulatory pressure for underground mine electrification to European mining operations in Finland, Sweden, Portugal, and Poland that collectively represent important underground mining markets for electrification technology adoption.

Major Mining Company Net-Zero Commitments, Investor ESG Requirements, and Green Finance Incentives Mobilizing Sustained Capital Investment in Mine Electrification Infrastructure

The net-zero greenhouse gas emission commitments adopted by the world’s largest mining companies, combined with the rapidly intensifying environmental, social, and governance performance requirements of institutional investors, sustainability-linked lending facilities, and green bond frameworks that finance mining capital expenditure, are mobilizing unprecedented levels of sustained investment in mine electrification infrastructure that extends well beyond the financial returns justifiable on a standalone total cost of ownership basis and reflects a broader strategic imperative to maintain investor access, social license, and capital market competitiveness in an era of mandatory climate-related financial disclosure. The Science Based Targets initiative’s mining sector guidance requires committed mining companies to reduce Scope 1 and Scope 2 emissions in alignment with 1.5-degree Celsius pathways, with diesel combustion in mining equipment constituting the largest single source of Scope 1 emissions for most mining operations, making equipment electrification the primary operational lever available to mining companies for meeting science-based emissions reduction commitments. Sustainability-linked loan facilities, which tie lending interest rates to the achievement of predefined electrification and emissions reduction milestones, have been executed by major mining companies including Vale, Freeport-McMoRan, and Newmont, creating direct financial incentives for advancing electrification investment timelines and providing lower-cost capital for mining electrification programs that demonstrably advance borrower sustainability key performance indicators, while green bond issuance by mining companies specifically for electrification and renewable energy capital projects has grown to approximately USD 4.8 billion in cumulative proceeds globally by the end of 2025, providing dedicated low-cost capital pools for electrification infrastructure investment.

Key Challenges

High Capital Cost of Battery Electric Mining Equipment and Charging Infrastructure Relative to Diesel Alternatives Creating Upfront Investment Barriers for Mine Operators

The capital cost of battery electric mining equipment continues to carry a substantial premium relative to equivalent diesel-powered machines across the majority of product categories and payload classes, with battery electric underground load-haul-dump machines of 14 to 18 tonne payload capacity priced at approximately USD 1.2 to USD 1.6 million compared to USD 700,000 to USD 900,000 for equivalent diesel machines, and battery electric haul trucks at surface mine scale remaining in prototype or early commercial stage at price points that are expected to carry premiums of 40% to 80% above diesel equivalents even at initial commercial launch volumes, creating capital allocation challenges for mine operators that must simultaneously fund ore body development, processing plant maintenance, and technology transition investment within capital budgets constrained by commodity price cycles and shareholder return expectations. The charging and electrical infrastructure investment required to support electrified underground mine fleets represents a significant additional capital commitment beyond equipment procurement costs, with a fully electrified underground mine of moderate scale requiring electrical substation upgrades, high-voltage cable installation throughout underground workings, fast-charging station installation at productive ore development and production areas, surface battery swap or overnight charging facilities, and energy management system integration, collectively representing an additional infrastructure investment of USD 8 to USD 25 million per mine depending on size, depth, and existing electrical infrastructure capacity. Mine operators also face battery replacement cost risk across the equipment ownership lifecycle, as battery pack degradation over charge cycles and in the demanding thermal and vibration conditions of underground mining environments can require partial or complete battery replacement within seven to ten years of initial equipment commissioning, representing an unbudgeted lifecycle cost that is difficult to predict precisely and creates financial planning uncertainty for fleet electrification business cases that extend over standard mining equipment amortization periods of ten to fifteen years.

Battery Performance Limitations at High Payload Capacities and in Extreme Temperature and High-Altitude Mine Operating Environments Constraining Product Range Completeness

The energy density, cycle life, charging speed, and thermal performance characteristics of current lithium-ion battery technology impose meaningful operational constraints on battery electric mining equipment at the largest payload capacities and in the most demanding mine site environmental conditions, limiting the market-ready product range for battery electric equipment to underground and smaller surface applications while leaving the largest and most fuel-intensive surface mining equipment categories, including ultra-class haul trucks of 300 to 400 tonne payload capacity, large rope shovels, and high-capacity blast hole drills, without commercially available battery electric alternatives during the near-term period through approximately 2028 to 2030. Large surface haul trucks of 220 to 360 tonne payload capacity require energy storage systems of 1,000 to 2,500 kilowatt-hours to achieve the 45 to 60 minute operating cycles between charges needed for continuous production operation, battery pack weights that impose significant payload capacity penalties and axle load increases that can exceed road infrastructure design limits at operating mines, while fast-charging power requirements of 2,000 to 6,000 kilowatts per vehicle create electrical grid capacity and infrastructure investment demands that are technically and financially challenging at high-altitude Andean copper mines, remote Western Australian iron ore operations, and Arctic region base metal mines that lack grid connectivity and existing high-voltage electrical infrastructure. High-altitude mine sites above 3,500 meters elevation in Chile, Peru, and Bolivia present additional battery thermal management challenges as reduced atmospheric pressure and extreme diurnal temperature variation affect battery cooling efficiency and state-of-charge management, requiring specialized thermal management systems and conservative energy management strategies that reduce effective operating range and productivity relative to sea-level reference performance specifications, complicating technology transfer from European and North American mine reference installations to Latin American high-altitude mining applications.

Remote Mine Site Energy Infrastructure Limitations, Grid Connectivity Constraints, and Renewable Energy Intermittency Creating Reliable Clean Power Supply Challenges for Electrified Operations

The majority of globally significant mining operations are located in remote geographic environments distant from existing high-voltage grid infrastructure, creating a fundamental energy supply challenge for mining electrification programs that require reliable, high-capacity, and cost-competitive clean electricity to achieve their full emissions reduction and operational cost savings potential, as electrified mining equipment powered by diesel generator electricity delivers only partial emissions reduction while maintaining diesel fuel dependency and the associated fuel logistics, storage, and cost exposure that electrification programs are fundamentally intended to eliminate. Constructing grid connection infrastructure to remote mine sites typically requires transmission line investments of USD 50,000 to USD 200,000 per kilometer depending on terrain, permitting complexity, and required capacity, with many major mining operations located 100 to 500 kilometers from the nearest high-voltage transmission network, generating grid connection capital requirements of USD 10 to USD 100 million per mine that must be justified against mine remaining life and grid electricity cost savings relative to on-site diesel generation economics. Remote mine site renewable energy microgrid solutions, while commercially advancing rapidly, face the intermittency challenge that solar and wind generation cannot be dispatched to match the variable and high-intensity power demand profiles of electrified mining operations without battery energy storage or diesel backup generation of sufficient capacity to maintain continuous operations through extended periods of low renewable generation, requiring battery energy storage system investment that scales with the required backup duration and peak power demand and can represent a capital commitment comparable to the renewable generation asset itself, increasing the total energy infrastructure investment required to achieve fully renewable-powered electrified mine site operations to levels that are commercially viable at long-life, large-scale mining operations but remain challenging to justify at shorter-life or smaller-scale mining projects.

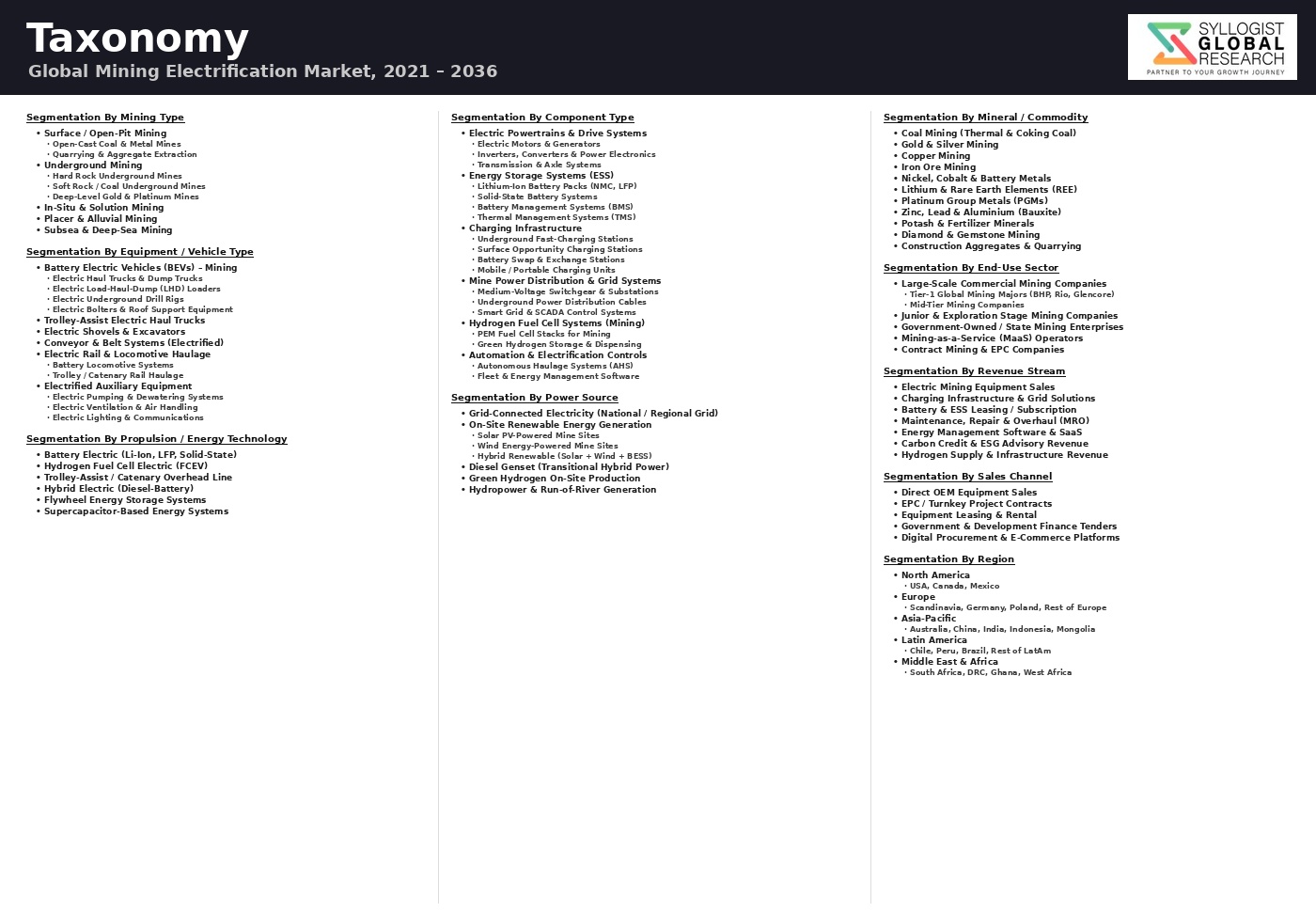

Market Segmentation

- Segmentation By Technology Type

- Battery Electric Vehicles and Mobile Mining Equipment

- Fuel Cell Electric Vehicles (Hydrogen-Powered Mining Equipment)

- Trolley Assist Systems for Surface Haul Trucks

- Fixed and Mobile Battery Energy Storage Systems

- Renewable Energy Generation Systems (Solar PV, Wind, and Hybrid Microgrids)

- High-Voltage Underground Electrification Infrastructure

- Electrified Conveying and Material Handling Systems

- Mine Energy Management and Grid Integration Platforms

- Charging Infrastructure (Fast Charging, Battery Swap, and Overhead Catenary Systems)

- Others

- Segmentation By Equipment Category

- Electric Load-Haul-Dump (LHD) Machines and Underground Loaders

- Electric Underground Haul Trucks and Articulated Dump Trucks

- Electric Surface Haul Trucks (Battery Electric and Trolley Assisted)

- Electric Drill Rigs (Underground and Surface Blast Hole Drills)

- Electric Underground Bolters, Scalers, and Ground Support Equipment

- Electric Utility Vehicles, Personnel Carriers, and Light Duty Equipment

- Electric Shovels, Excavators, and Loading Equipment

- Electric Crushing, Grinding, and Processing Equipment

- Others

- Segmentation By Mine Type

- Underground Hard Rock Mining (Gold, Copper, Nickel, Zinc, and PGMs)

- Underground Soft Rock Mining (Coal, Potash, and Trona)

- Open-Pit and Surface Hard Rock Mining

- Open-Cut Surface Coal Mining

- Quarrying and Industrial Mineral Extraction

- Others

- Segmentation By Commodity

- Copper

- Gold

- Nickel and Cobalt

- Iron Ore

- Platinum Group Metals

- Zinc and Lead

- Coal

- Potash and Fertilizer Minerals

- Industrial Minerals and Aggregates

- Others

- Segmentation By Power Source

- Battery Electric (Lithium-Ion)

- Hydrogen Fuel Cell

- Grid-Connected Renewable Electricity

- Captive Renewable Energy Microgrid

- Hybrid Battery and Diesel

- Trolley Overhead Line Power

- Others

- Segmentation By End User

- Major Diversified Mining Companies

- Mid-Tier and Junior Mining Producers

- State-Owned Mining Enterprises

- Contract Mining Companies

- Mining Equipment Rental and Leasing Operators

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Mining Electrification Technologies Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by technology type including battery electric vehicles, fuel cell electric vehicles, trolley assist systems, battery energy storage, renewable energy microgrids, underground electrical infrastructure, and charging platforms, and by mine type including underground hard rock, underground soft rock, open-pit surface, and surface coal mining, to enable mining equipment manufacturers, battery technology developers, renewable energy companies, mining operators, electrification infrastructure contractors, and capital market investors to identify which technology categories, mine types, and commodity sectors will generate the largest absolute revenue growth and the most commercially resilient electrification technology demand across the forecast period to 2034?

- How is the total cost of ownership economics of battery electric mining equipment expected to evolve through 2034 as battery pack costs continue to decline from approximately USD 195 per kilowatt-hour in 2025 toward projected levels below USD 110 per kilowatt-hour by 2030, and what are the mine type, operating condition, fleet utilization, and diesel price scenarios under which battery electric mining equipment achieves lifecycle cost parity with equivalent diesel machines across underground load-haul-dump, underground haul truck, surface utility vehicle, and large surface haul truck product categories, and what proportion of the global diesel-powered mining equipment fleet transitions to electrified alternatives under base case, accelerated, and delayed electrification adoption scenarios through 2034?

- What is the current product portfolio, commercial deployment reference base, battery technology platform, charging infrastructure approach, service and support network, key mining company customer relationships, and electrification roadmap commitments of the leading mining equipment manufacturers including Epiroc, Sandvik, Komatsu, Caterpillar, Liebherr, Normet, MacLean Engineering, and emerging pure-play electric mining equipment developers, and how are these market participants differentiating their electrification value propositions through battery performance specifications, integrated energy management systems, fleet conversion service programs, financing structures, and partnership arrangements with battery developers, renewable energy providers, and mining company customers driving large-scale electrification deployment?

- What are the mine site renewable energy and battery energy storage infrastructure requirements, capital investment profiles, grid connection economics versus off-grid microgrid economics, and renewable energy procurement approaches being adopted by major mining companies at their most significant operational sites across Chile, Australia, Canada, South Africa, the Democratic Republic of Congo, and other major mining geographies, and how are mining companies structuring energy service agreements, power purchase agreements, and integrated electrification and renewable energy contracts with technology providers to manage the capital commitment and operational risk of transitioning from diesel-dependent to fully renewable-powered electrified mine operations within their announced net-zero and emissions reduction commitment timelines?

- Which regulatory frameworks governing underground mine ventilation standards, diesel particulate matter exposure limits, greenhouse gas emissions reporting obligations, and mine operator social license requirements in Canada, Australia, the United States, Chile, South Africa, and the European Union are creating mandatory or effectively compulsory electrification adoption timelines for underground mining operations, and how do these jurisdiction-specific regulatory drivers interact with voluntary corporate sustainability commitments and total cost of ownership financial incentives to determine the pace and geographic distribution of mining electrification technology adoption investment, and which mining jurisdictions are projected to achieve the highest electrification technology deployment rates and generate the largest absolute electrification market revenue by 2034?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Technology & Commercialisation Risk

- Raw Material & Battery Supply Chain Risk

- Regulatory & Compliance Risk

- Market & Demand Risk

- Operational & Safety Risk

- Regulatory Framework & Standards

- Mine Safety, Occupational Health & Equipment Certification Standards

- Carbon Pricing, Emission Reduction & Decarbonisation Policy Frameworks for Mining

- Electrical Equipment, Hazardous Area & Intrinsic Safety Standards for Mines

- Battery, Hydrogen & Alternative Energy Storage Safety Regulations

- Environmental, Permitting & Energy Efficiency Standards for Mine Sites

- Global Mining Electrification Technologies Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Units & Installed Capacity)

- Market Size & Forecast by Technology

- Battery Electric Vehicles (BEV) for Mining: Surface & Underground

- Trolley-Assist Systems for Surface Haul Trucks (Overhead Catenary)

- Fuel Cell Electric Vehicles (FCEV) for Mining: Green Hydrogen-Powered

- Electric Fixed Plant & Infrastructure (Conveyors, Hoists, Mills, Pumps & Fans)

- In-Pit Crushing & Conveying (IPCC) Electrified Systems

- Mine Power Systems & Microgrids (Renewable Integration & Battery Energy Storage)

- Electrified Rail & Underground Haulage Systems

- Charging Infrastructure & Battery Swap Systems for Mining

- Mine Electrification Monitoring, Control & Digital Management Systems

- Market Size & Forecast by Equipment Type

- Surface Mining Equipment

- Electric Haul Trucks: Battery Electric & Trolley-Assist (100t to 400t+ Class)

- Electric Rope Shovels, Hydraulic Excavators & Face Shovels

- Electric Surface Drill Rigs & Blasthole Drills

- Electric Dozers, Graders & Auxiliary Surface Equipment

- Underground Mining Equipment

- Underground Battery Electric Haul Trucks (40t to 65t Class)

- Battery-Electric Load Haul Dump (LHD) Scooptrams (2t to 25t Class)

- Underground Battery-Electric Drill Rigs (Face, Long-Hole & Bolting)

- Underground Battery-Electric Personnel Carriers, Shotcrete & Utility Vehicles

- Fixed Plant & Infrastructure Equipment

- Variable Speed Drive (VSD) Electric Mill Drives (SAG, Ball & AG Mills)

- Electric Gearless Mill Drives (GMD) & High-Voltage Conveyor Systems

- Electric Hoisting, Winding & Skip Systems

- Electric Pumps, High-Pressure Fans & Mine Ventilation-on-Demand (VoD) Systems

- Market Size & Forecast by Power Source

- Battery Electric: Lithium-Ion (LFP, NMC, NCA Cell Chemistry)

- Battery Electric: Solid-State Battery (Next-Generation, Post-2028)

- Fuel Cell Electric: Green Hydrogen (FCEV)

- Trolley-Assist: Overhead Catenary Grid Power

- Grid-Connected Electric (Mine Site Power Supply: Utility & Captive)

- Hybrid: Diesel-Electric & Battery-Diesel (Transition-Phase Systems)

- Renewable Energy + Storage (Solar-Wind-BESS Mine Microgrid)

- Market Size & Forecast by Mining Method

- Open-Pit & Surface Mining

- Underground Hard Rock Mining

- Underground Soft Rock & Coal Mining

- In-Situ Leaching & Solution Mining

- Placer Mining & Dredging

- Market Size & Forecast by Mineral / Commodity

- Copper Mining

- Gold Mining

- Iron Ore Mining

- Coal Mining

- Battery Minerals: Lithium, Cobalt, Nickel & Manganese Mining

- Potash, Phosphate & Fertiliser Mineral Mining

- Other Base & Precious Metals (Zinc, Lead, Silver, PGMs)

- Market Size & Forecast by End-User

- Tier-1 Major Mining Companies (Global Diversified & Single-Commodity Majors)

- Mid-Tier Mining Companies

- Junior Mining Companies & Explorers (Greenfield Electrification-First Projects)

- Contract Mining Operators

- Market Size & Forecast by Sales Channel

- Direct OEM Supply to Mining Operators (Long-Term Capital Equipment Contracts)

- Mining EPC & EPCM Contractor Supply & Procurement

- Equipment Leasing, Rental & Electrification-as-a-Service (EaaS) Models

- Aftermarket, Parts, Service & Retrofit Upgrade Channel

- North America Mining Electrification Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units & Installed Capacity)

- By Technology

- By Equipment Type

- By Power Source

- By Mining Method

- By Mineral / Commodity

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Mining Electrification Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units & Installed Capacity)

- By Technology

- By Equipment Type

- By Power Source

- By Mining Method

- By Mineral / Commodity

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Mining Electrification Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units & Installed Capacity)

- By Technology

- By Equipment Type

- By Power Source

- By Mining Method

- By Mineral / Commodity

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Mining Electrification Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units & Installed Capacity)

- By Technology

- By Equipment Type

- By Power Source

- By Mining Method

- By Mineral / Commodity

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Mining Electrification Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units & Installed Capacity)

- By Technology

- By Equipment Type

- By Power Source

- By Mining Method

- By Mineral / Commodity

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Mining Electrification Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units & Installed Capacity)

- By Technology

- By Equipment Type

- By Power Source

- By Mining Method

- By Mineral / Commodity

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Sweden, Finland, Norway, Australia, China, Japan, South Korea, India, Chile, Brazil, Peru, South Africa, Democratic Republic of Congo, Zambia, Russia, Kazakhstan, Indonesia

- Technology Landscape & Innovation Analysis

- Battery Electric Vehicle (BEV) Technology Deep-Dive

- Large-Format Lithium-Ion Battery System Design for Heavy Mining Equipment: Cell Chemistry (LFP, NMC, NCA), Pack Architecture & Thermal Management in Harsh Environments

- Battery Swapping Technology for Continuous Mining Cycle Operation: Automated Swap Station Design, Cycle Time Optimisation & Fleet Utilisation Rate Impact

- Fast Charging & Opportunity Charging Technology for Mining BEV: Stationary High-Power Charger Design, Underground Cable Management & Grid Impact Management

- Battery Management System (BMS) for Mining Duty Cycles: State-of-Charge, State-of-Health, Predictive Maintenance Integration & Underground Communication Protocol

- Solid-State Battery Technology Outlook for Mining Applications: Energy Density, Intrinsic Safety, Temperature Range Performance & Commercialisation Timeline (Post-2028)

- Trolley-Assist & Overhead Catenary System Technology for Surface Mining

- Fuel Cell Electric Vehicle (FCEV) & Green Hydrogen Technology for Heavy Mining Equipment

- Mine Power System, Microgrid & Renewable Energy Integration Technology

- Electric Fixed Plant Technology (Mill Drives, Conveyor Systems, Hoisting & Ventilation)

- Charging Infrastructure, Energy Management & Battery Swap Station Technology

- Digital Electrification, Fleet Management, Telemetry & Predictive Maintenance Technology

- Patent & IP Landscape in Mining Electrification Technologies

- Battery Electric Vehicle (BEV) Technology Deep-Dive

- Value Chain & Supply Chain Analysis

- Battery Cell, Module & Pack Supply Chain (Critical Mineral, Cell Manufacturer & Pack Integrator)

- Electric Drivetrain, Motor, Inverter & Power Electronics Supply Chain

- Mining OEM Electrification Equipment Manufacturer & Assembly Landscape

- Mine Power & Renewable Energy Infrastructure Supply Chain

- Charging Equipment, Battery Swap System & Mine Electrical Infrastructure Suppliers

- Mining Operator, EPC Contractor & Systems Integrator Procurement Process

- End-of-Life Battery Recycling, Second-Life Application & Circular Economy

- Pricing Analysis

- Battery Electric Surface Haul Truck Pricing Analysis

- Underground Battery Electric Equipment (LHD, Trucks & Drills) Pricing Analysis

- Trolley-Assist System Infrastructure Capital & Operating Cost Analysis

- Mine Power System, Microgrid & Renewable Integration Pricing Analysis

- Charging Infrastructure & Battery Swap System Pricing Analysis

- Total Cost of Ownership (TCO) Electrification vs. Diesel Benchmark Analysis

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Mining Electrification Technologies vs. Diesel Baseline

- Carbon Footprint & GHG Emission Reduction Accounting for Electrified Mine Operations

- Underground Air Quality, Heat Load Reduction & Diesel Elimination Co-Benefits

- Mine Site Renewable Energy Integration, Energy Transition & Net Zero Target Contribution

- Regulatory-Driven Sustainability, Social Licence & Just Transition in Mining Communities

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Technology & Equipment Segment)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Technology, Equipment Type & Geography

- Player Classification

- Global Mining OEM Electrification Leaders (Full-Range Surface & Underground Equipment)

- Specialist Battery Electric Underground Mining Equipment Manufacturers

- Trolley-Assist & Overhead Catenary Infrastructure System Providers

- Fuel Cell & Green Hydrogen Mining Equipment Developers

- Mine Power System, Microgrid & Renewable Energy Integration Providers

- Battery Technology, Cell & Pack Suppliers to Mining OEMs

- Charging Infrastructure & Battery Swap System Specialists

- Mining Technology Integrators, Digital Electrification & Fleet Management Platforms

- Competitive Analysis Frameworks

- Market Share Analysis by Technology, Equipment Type & Region

- Company Profile

- Company Overview & Headquarters

- Mining Electrification Products & Technology Portfolio

- Key Mining Customer Relationships & Reference Site Installations

- Manufacturing Footprint & Production Capacity

- Revenue (Mining Electrification Segment) & Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Capacity Expansion, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Technology, Equipment Type, Mining Method, Mineral & Geography

- White Space Opportunity Analysis

- Strategic Output

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & Mining Operator Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025–2028)

- Mid-term (2029–2032)

- Long-term (2033–2037)