Global Mining Robotics Market By Robot Type, By Mining Method, By Technology, By Application, By Autonomy Level, By End User, By Region, Competition, Forecast and Opportunities, 2021-2036F

Market Definition

The Global Mining Robotics Market encompasses the design, manufacturing, integration, and deployment of autonomous and semi-autonomous robotic systems, unmanned ground vehicles, remotely operated drilling and blasting equipment, autonomous haulage systems, robotic inspection drones, and AI-enabled mine automation platforms used across surface, underground, and subsea mineral extraction operations. The market includes associated perception sensor suites, real-time positioning systems, fleet management software, collision avoidance hardware, remote operation control infrastructure, and predictive maintenance platforms procured by coal, metal, and non-metal mining companies, contract mining operators, and mineral processing facility operators globally.

Market Insights

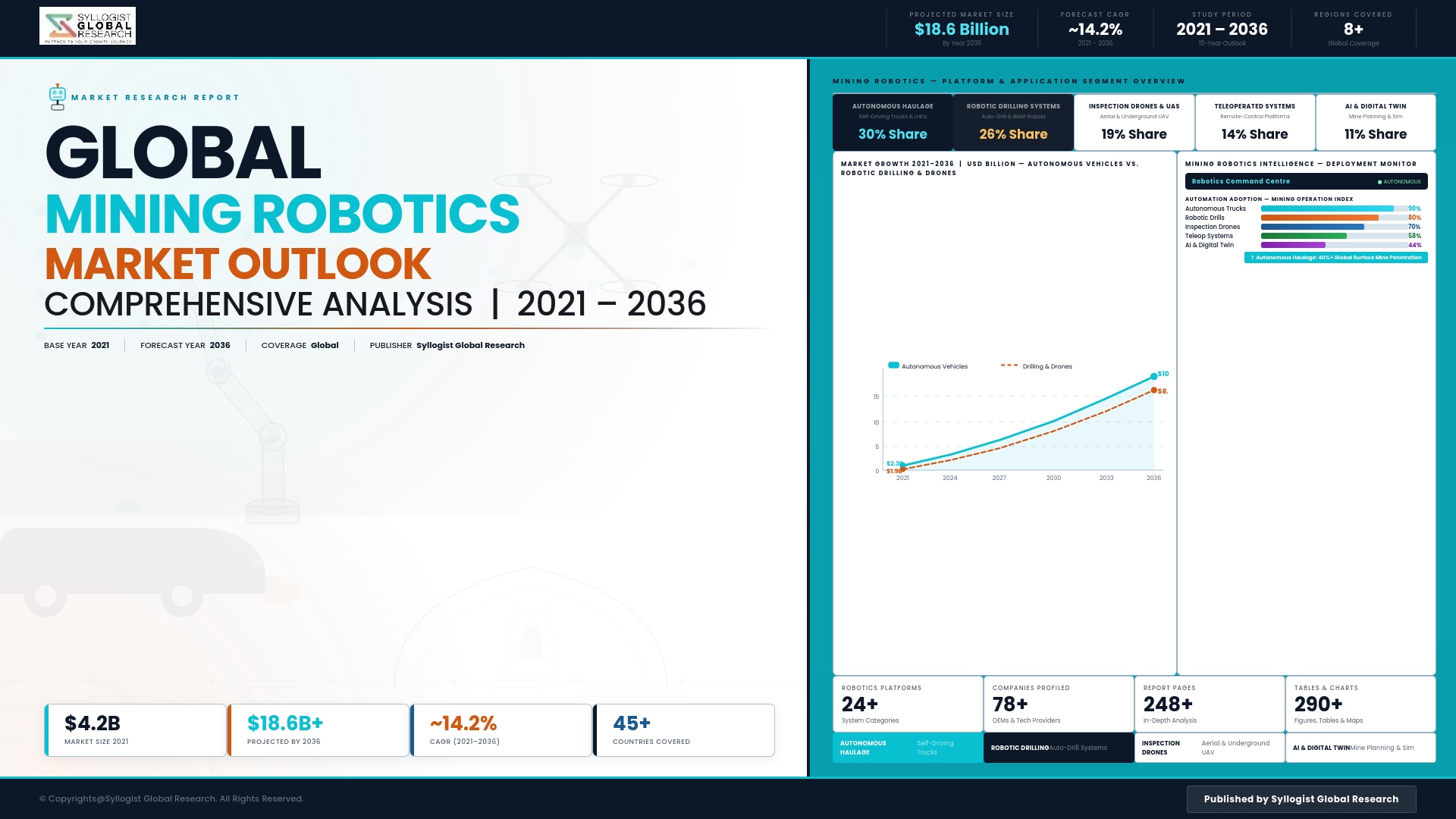

The global mining robotics market is undergoing a structural acceleration, driven by the convergence of worsening skilled labor shortages across global mining labor markets, intensifying mine safety regulatory pressure compelling the removal of personnel from hazardous extraction environments, and a critical minerals demand surge that is compelling mining operators to maximize ore extraction productivity from existing and new mine assets through automation investment that delivers productivity and utilization gains beyond what human-operated equipment can sustain across continuous multi-shift operation cycles. The market was valued at approximately USD 5.6 billion in 2025 and is projected to reach USD 16.8 billion by 2034, advancing at a compound annual growth rate of 13.0% through the forecast period, as autonomous haulage systems, robotic drilling platforms, AI-powered ore sorting systems, and underground autonomous navigation technologies transition from pioneering deployments at a small number of technologically advanced mining operations into standard procurement considerations across large-scale surface and underground mines globally.

The autonomous haulage system segment represents the most commercially mature and highest-revenue category within mining robotics, with large-format autonomous haul trucks operating across open-cut iron ore, copper, and coal operations in Australia, Chile, Canada, and North America demonstrating measurable improvements in haul cycle productivity, fuel efficiency, tyre life, and equipment availability relative to human-operated equivalents, creating a commercially validated business case that is accelerating autonomous haulage adoption across a widening range of mining commodities and geographies beyond the early-adopter operations where the technology was initially proven. The economic compulsion driving autonomous haulage adoption is reinforced by the structural driver shortage affecting commercial vehicle operators globally, which is creating recruitment and retention challenges for mining companies whose remote site locations and rotating roster working conditions make competitive labor market positioning particularly difficult relative to urban employment alternatives for experienced equipment operators. Underground mining automation is advancing at a particularly rapid pace, driven by the safety imperative of removing personnel from ground failure, rockfall, blast fume, and equipment collision hazard environments that characterize underground stoping, development, and ore haulage operations, with robotic bolting systems, autonomous load-haul-dump vehicles, and remote blast initiation platforms enabling a progressive transition toward less-manned and ultimately non-entry underground mine operations.

The critical minerals imperative is reshaping mining robotics investment priorities, as the accelerating global demand for lithium, cobalt, nickel, copper, and rare earth elements required by electric vehicle battery, renewable energy infrastructure, and advanced electronics supply chains is compelling mining companies and national resource development programs to accelerate the development of deposits in remote, geologically complex, and environmentally sensitive locations where robotic and autonomous systems offer distinct advantages over human-operated approaches in terms of operational continuity, environmental footprint minimization, and workforce risk management. Robotic exploration drilling systems capable of operating in extreme environment conditions without continuous human supervision, AI-powered geological modeling platforms integrating drill core data with geophysical survey intelligence, and precision robotic ore sorting systems that improve ore grade selectivity at the mine face are each generating investment from mining companies seeking to improve the economic viability of marginal deposits and extend the productive lives of mature operations. Asia-Pacific is projected to record the highest regional compound annual growth rate through 2034, driven by large-scale mine automation programs in Australia, accelerating robotics adoption in Chinese and Indian mining sectors, and critical minerals development investment across Southeast Asia and the Pacific. North America and Latin America maintain significant market shares through large autonomous haulage deployments in Canadian oil sands and Chilean copper operations.

Key Drivers

Chronic Skilled Mining Labor Shortages, Remote Site Workforce Recruitment Challenges, and Rising Labor Cost Pressures Compelling Autonomous Equipment Deployment as a Strategic Capacity Solution

The global mining industry is confronting a structural and worsening deficit of experienced equipment operators, maintenance technicians, and underground mine workers whose combination of technical skill requirements, willingness to work in remote and physically demanding mine environments, and availability at compensation levels consistent with mine operating cost budgets is declining across all major mining labor markets simultaneously, creating a workforce capacity constraint that autonomous and robotic systems directly address by enabling continuous multi-shift equipment operation without the recruitment, retention, fatigue management, and accommodation cost obligations associated with equivalent human-operated equipment fleets. Mining companies in Australia, Canada, Chile, and South Africa are reporting critical labor availability limitations that are constraining production volume below installed equipment capacity, creating an operational imperative for autonomous system deployment that is driving investment decisions independent of purely financial return on investment calculations.

Intensifying Mine Safety Regulations and Zero Harm Corporate Commitments Driving Systematic Removal of Personnel from High-Hazard Extraction and Haulage Environments Through Robotic Substitution

The mining industry globally is subject to progressive tightening of occupational health and safety regulations governing worker exposure to ground movement hazards, blast proximity, equipment interaction risks, and atmospheric contaminants in underground and open-cut mine environments, with regulatory agencies in Australia, Canada, the United States, Chile, and South Africa implementing enforcement frameworks that impose increasing liability on mining operators for worker fatalities and serious injuries that create powerful financial and reputational incentives to remove personnel from hazardous operational zones through robotic and autonomous system deployment. Corporate zero harm commitments adopted by major mining companies as board-level strategic objectives are further reinforcing this regulatory driver by creating internal investment justification frameworks that evaluate mine automation capital expenditure against the cost of workplace incidents, regulatory penalties, and community and investor scrutiny of safety performance.

Critical Minerals Demand Surge and the Productivity Imperative of Maximizing Extraction from Complex Deposits Driving Advanced Robotics and AI Integration Across Exploration, Extraction, and Processing

The structural surge in demand for critical minerals required by electric vehicle battery manufacturing, renewable energy infrastructure, and advanced semiconductor production is generating investment pressure on mining companies to maximize ore extraction productivity, improve ore grade selectivity, and accelerate the development of geologically complex and remotely located deposits that represent the next generation of critical mineral supply, creating a commercially compelling case for robotic exploration drilling, autonomous ore sorting, AI-powered geological modeling, and precision robotic extraction systems that collectively improve the economic viability and environmental performance of critical mineral mine development programs. Mining companies and national critical mineral programs are treating mine automation investment as a strategic enabler of supply security rather than a purely operational efficiency measure, driving higher investment intensity in robotics deployment than conventional mining productivity economics alone would justify.

Key Challenges

Underground Mine Connectivity Infrastructure Limitations, GPS-Denied Navigation Challenges, and Ruggedization Requirements Constraining Autonomous System Performance and Deployment Pace in Subsurface Operations

Underground mine environments present fundamental technical challenges for autonomous robotic system deployment that are substantially more demanding than surface operations, including the absence of GPS satellite positioning signals requiring alternative real-time localization solutions, limited and unreliable wireless communications infrastructure in narrow, curved, and geometrically complex underground tunnel networks, extreme dust, moisture, vibration, and temperature conditions that impose severe ruggedization requirements on sensors and electronics, and the dynamic geometry of active underground mine workings where excavated void shapes and obstacle profiles change continuously as mining progresses. Achieving the navigation precision, communication reliability, and environmental durability required for commercially viable autonomous underground equipment operation demands significant infrastructure investment in underground positioning beacons, mesh communication networks, and equipment hardening programs that add capital cost and deployment complexity beyond the equipment procurement cost itself.

High Capital Expenditure Requirements, Long Payback Periods, and Technology Integration Complexity Constraining Mining Robotics Adoption Among Mid-Tier and Junior Mining Operators

The capital expenditure required for autonomous haulage system deployment, robotic drilling platform installation, and mine-wide automation infrastructure encompasses not only the robotic equipment acquisition cost but also substantial investment in mine site communications infrastructure upgrades, control room facility construction, fleet management system integration, and workforce retraining programs whose aggregate cost creates investment thresholds that are accessible primarily to large-scale Tier 1 mining operators with the financial capacity and asset longevity to justify multi-year payback period automation investments. Mid-tier and junior mining operators, which collectively represent a significant portion of global mineral production across precious metals, specialty minerals, and smaller commodity operations, face financing constraints, mine life uncertainty, and technology integration capability limitations that substantially restrict their near-term participation in advanced mining robotics adoption beyond entry-level remote monitoring and inspection applications.

Workforce Transition Resistance, Union Opposition to Automation-Driven Job Displacement, and Social License Requirements in Mining Community Contexts Complicating Autonomous System Deployment Programs

The deployment of autonomous mining equipment that directly displaces human equipment operators generates significant workforce resistance, union opposition, and community relations challenges in mining regions where equipment operation employment represents a major source of regional economic activity and where the transition from human-operated to autonomous equipment is perceived by workers and their representatives as a direct threat to employment security and community economic viability that requires negotiated transition programs, redeployment commitments, and community investment obligations that add cost, delay, and political complexity to autonomous system deployment timelines. Mining companies operating in jurisdictions with strong trade union representation, mandatory works council consultation requirements, or social license frameworks linked to local employment commitments must navigate workforce transition obligations that extend automation deployment timelines and impose negotiated operational constraints on the pace and scale of autonomous system rollout.

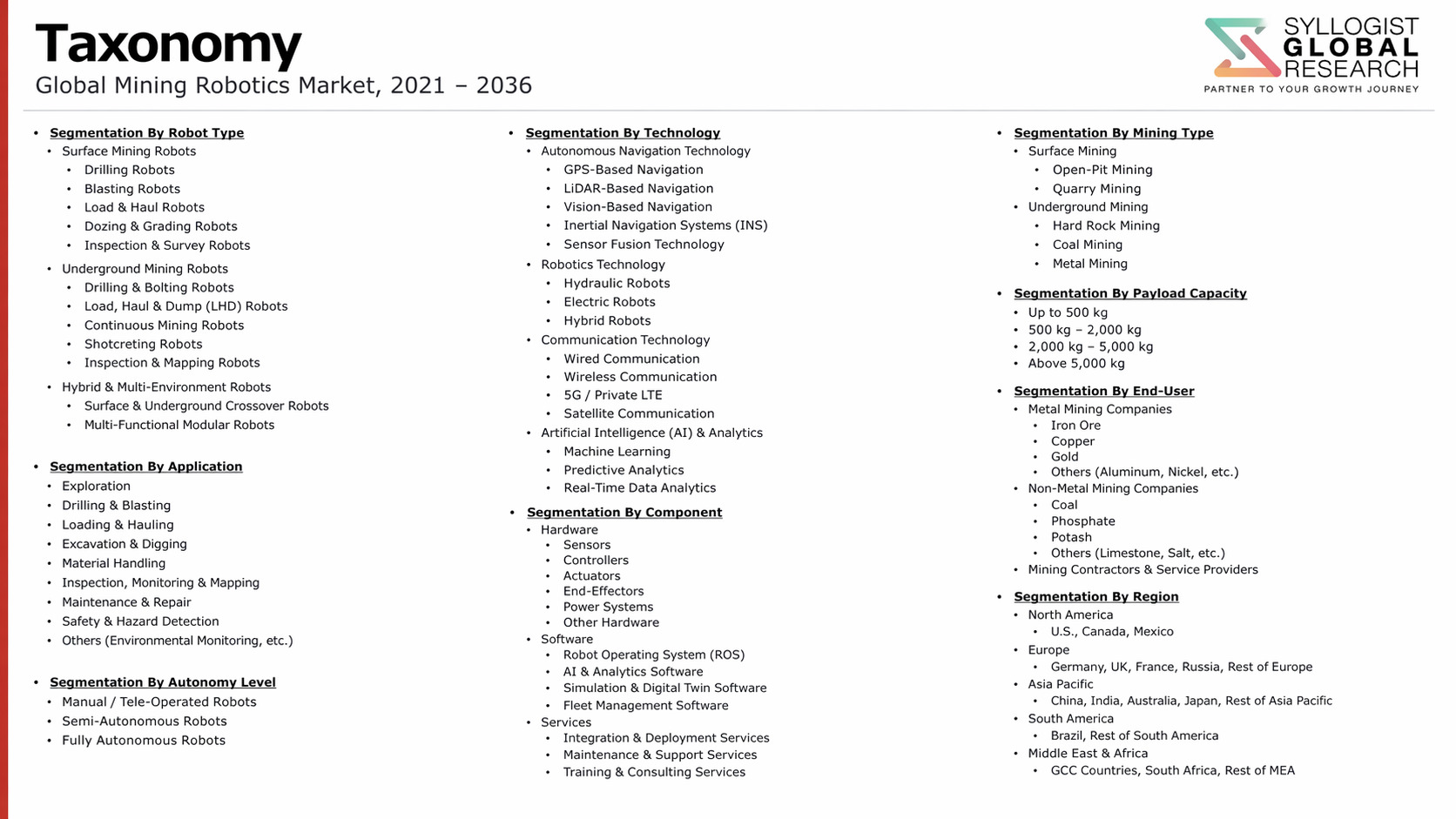

Market Segmentation

- Segmentation By Robot Type

- Autonomous Haulage Systems and Haul Trucks

- Robotic Drilling and Blasthole Drilling Systems

- Autonomous Load-Haul-Dump (LHD) Vehicles

- Robotic Bolting and Ground Support Systems

- Inspection and Monitoring Drones and UAVs

- AI-Powered Ore Sorting and Processing Robots

- Robotic Exploration Drilling Platforms

- Others

- Segmentation By Mining Method

- Open-Cut and Surface Mining Operations

- Underground Hard Rock Mining

- Underground Coal Mining

- Placer and Alluvial Mining

- Deep Sea and Subsea Mining

- In-Situ Leach and Solution Mining

- Segmentation By Technology

- LiDAR and Radar-Based Perception Systems

- AI and Machine Learning Navigation Software

- Real-Time Positioning and Localization Systems

- Fleet Management and Mine Automation Platforms

- Collision Avoidance and Proximity Detection Systems

- Remote Operation and Teleoperation Control Systems

- Predictive Maintenance and Digital Twin Platforms

- Others

- Segmentation By Application

- Ore Haulage and Material Transport

- Drilling, Blasting, and Rock Fragmentation

- Ground Support and Roof Bolting

- Geological Mapping and Exploration

- Ore Sorting and Grade Control

- Mine Inspection, Monitoring, and Surveying

- Mineral Processing and Plant Automation

- Others

- Segmentation By Autonomy Level

- Remote Controlled and Teleoperated Systems

- Semi-Autonomous Systems with Human Supervision

- Fully Autonomous Systems within Defined Mine Domains

- Integrated Mine-Wide Autonomous Operation Platforms

- Segmentation By End User

- Large-Scale Integrated Mining Companies

- Mid-Tier and Junior Mining Operators

- Contract Mining and Equipment Rental Companies

- Coal Mining Companies

- Precious Metal and Diamond Mining Operators

- Critical Mineral and Battery Metal Mining Companies

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Mining Robotics Market in 2025, projected through 2034, disaggregated by robot type, mining method, and application, enabling mining companies, robotics developers, equipment manufacturers, and investors to identify the highest-growth technology segments and most durable revenue opportunities across the global mine automation landscape?

- How are leading Tier 1 mining operators across iron ore, copper, coal, and critical mineral sectors structuring autonomous haulage, robotic drilling, and underground automation deployment programs, and which operational, safety, and productivity metrics are defining the commercial business cases driving mine automation investment decisions and influencing technology selection through 2034?

- What underground positioning, communications infrastructure, and sensor ruggedization technology advances are most critical to expanding autonomous system deployment from commercially proven surface operations into underground hard rock and coal mining environments, and which technology developers and mining equipment manufacturers are closest to achieving scalable underground autonomous operation at commercially viable performance and cost levels?

- Which mining robotics segments, including autonomous haulage, robotic bolting, AI-powered ore sorting, drone-based inspection, and exploration drilling automation, are generating the highest near-term adoption and revenue growth rates through 2034, and what safety compliance, productivity improvement, and total cost of ownership benchmarks are most critical to mining operator procurement decisions?

- How is the competitive landscape structured among mining equipment OEMs, specialist robotics and autonomy technology companies, mining software developers, and systems integrators, and what technology partnership, OEM collaboration, and aftermarket service strategies are enabling leading players to capture commercially sustainable positions across the mine automation value chain?

- What workforce transition challenges, union opposition dynamics, social license requirements, and community employment obligations are constraining autonomous mining system deployment timelines in major mining jurisdictions, and how are mining companies, governments, and technology providers designing transition programs that address workforce displacement concerns while advancing automation deployment objectives?

- Which regional mining robotics markets, specifically Asia-Pacific, North America, and Latin America, are expected to generate the most substantial autonomous system deployment activity through 2034, and what critical mineral development programs, mine safety regulatory frameworks, labor market conditions, and mining company automation investment strategies are driving technology procurement priorities in each region?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Technology Maturity, Interoperability & Fleet Integration Risk

- Capital Investment, Pilot-to-Commercial Scale-Up & Productivity Payback Risk

- Cybersecurity, Remote Operations & Network Reliability Risk

- Workforce Displacement, Labour Union & Social License Risk

- Regulatory, Mine Safety Approval & Autonomous System Certification Risk

- Regulatory Framework & Standards

- Mine Safety, Autonomous System Certification & Operator Licensing Frameworks

- Cybersecurity, Data Sovereignty & Remote Operations Centre Standards

- Autonomous Haulage, Collision Avoidance & Mine Traffic Management Regulations

- Airspace, UAV Drone Operation & Beyond Visual Line of Sight (BVLOS) Regulations

- Green Finance, ICMM, IRMA Certification & Sustainable Mining Procurement Standards

- Global Mining Robotics Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Robotic Units Deployed)

- Market Size & Forecast by Robot Type

- Autonomous Haul Trucks & Surface Haulage Systems

- Autonomous Load-Haul-Dump (LHD) & Underground Mobile Equipment

- Autonomous Drilling Rigs (Surface, Underground & Blast-Hole)

- Robotic Rock Bolting, Longwall Automation & Underground Support Systems

- Unmanned Aerial Vehicles (UAVs & Drones) for Surveying, Inspection & Mapping

- Remotely-Operated Vehicles (ROVs) for Flooded Mines & Underwater Operations

- Quadruped, Legged & Crawler Inspection Robots

- Robotic Ore Sorting, Sample Preparation & Automated Assay Systems

- Fleet Management, Remote Operations Centre & Orchestration Platforms

- Market Size & Forecast by Technology

- LiDAR, Radar, Camera & Multi-Sensor Perception Technology

- SLAM, GPS-Denied Navigation & Localisation Technology

- 5G, LTE, Mesh Networking & V2X Communication Technology

- Artificial Intelligence, Machine Learning & Computer Vision Technology

- Edge Computing, Onboard Processing & Real-Time Decision Technology

- Robotic Manipulation, End-Effector & Grasping Technology

- Battery, Hybrid-Electric & Autonomous Power System Technology

- Digital Twin, Simulation & Virtual Commissioning Technology

- Cybersecurity, Remote Authentication & Secure OTA Update Technology

- Market Size & Forecast by Autonomy Level

- Teleoperated & Remotely-Piloted Systems (Level 1)

- Supervised Autonomous Systems (Level 2)

- Conditionally Autonomous Systems with Human Oversight (Level 3)

- Highly Autonomous Systems (Level 4)

- Fully Autonomous Systems (Level 5)

- Market Size & Forecast by Project Scale

- Large-Scale Tier-1 Mine Fleet Deployment (Above 100 Robotic Units)

- Medium-Scale Mine Fleet Deployment (10 to 100 Robotic Units)

- Small-Scale & Pilot Deployment (Below 10 Robotic Units)

- Market Size & Forecast by Application

- Surface and Open-Pit Mining Operations

- Underground Hard-Rock Mining Operations

- Underground Coal Mining & Longwall Operations

- Quarrying & Construction Aggregates Operations

- Remote, Hazardous & Off-Grid Mining Operations

- Exploration, Geological Survey & Pre-Production Sites

- Mine Rehabilitation, Closure & Legacy Site Operations

- Market Size & Forecast by End-User

- Major Mining Company & Tier-1 Operator

- Mid-Tier & Junior Mining Company

- Mining Service Contractor, Drilling Contractor & Fleet Operator

- Mining EPC & System Integrator

- Government Mining Authority & State-Owned Enterprise

- Market Size & Forecast by Sales Channel

- Direct Equipment Supply & OEM Fleet Contract

- Technology Licensing, Joint Venture & Co-Development Partnership

- Robotics-as-a-Service (RaaS), Leasing & Subscription Model

- Operations & Maintenance (O&M), Remote Support & Performance Contract

- North America Mining Robotics Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Robotic Units Deployed)

- By Robot Type

- By Technology

- By Autonomy Level

- By Project Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Mining Robotics Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Robotic Units Deployed)

- By Robot Type

- By Technology

- By Autonomy Level

- By Project Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Mining Robotics Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Robotic Units Deployed)

- By Robot Type

- By Technology

- By Autonomy Level

- By Project Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Mining Robotics Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Robotic Units Deployed)

- By Robot Type

- By Technology

- By Autonomy Level

- By Project Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Mining Robotics Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Robotic Units Deployed)

- By Robot Type

- By Technology

- By Autonomy Level

- By Project Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Mining Robotics Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Robotic Units Deployed)

- By Robot Type

- By Technology

- By Autonomy Level

- By Project Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- *Countries Analysed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Italy, Norway, Sweden, China, Japan, India, Australia, South Korea, Singapore, Brazil, Chile, Saudi Arabia, UAE, Egypt, South Africa, Israel

- Technology Landscape & Innovation Analysis

- Autonomous Haulage System (AHS) & Surface Fleet Automation Technology Deep-Dive

- Autonomous LHD, Underground Equipment & Tele-Remote Operation Technology

- Autonomous Drilling, Rock Bolting & Longwall Automation Technology

- Drone, UAV & BVLOS Aerial Surveying Technology for Mining

- Quadruped, Legged Robot & Confined-Space Inspection Technology

- Robotic Sorting, Sample Preparation & Automated Assay Lab Technology

- AI, Machine Learning & Computer Vision Technology for Mining Operations

- Patent & IP Landscape in Mining Robotics Technologies

- Value Chain & Supply Chain Analysis

- Mining Equipment OEM & Autonomous Platform Manufacturing Supply Chain

- Sensor, LiDAR, Radar & Perception Component Supply Chain

- Communication, 5G, Networking & Telecom Infrastructure Supply Chain

- Software, AI Platform & Fleet Management System Supply Chain

- Mining EPC, System Integrator & Robotics Deployment Service Landscape

- Mining Operator, Contractor & Offtake Partner Channel

- Maintenance, Remote Support & Operator Training Service Ecosystem

- Pricing Analysis

- Autonomous Haul Truck Capital and Total Cost of Ownership (TCO) Analysis

- Autonomous LHD & Underground Equipment Capital and Operating Cost Analysis

- Autonomous Drilling, Rock Bolting & Longwall Automation TCO Analysis

- Drone, UAV & Inspection Robot Capital and Operating Cost Analysis

- Mining Robotics Long-Term Service Contract, RaaS & Subscription Pricing Analysis

- Total Autonomous Mine Project Economics: Cost per Tonne Mined & Productivity Payback Analysis

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Mining Robotics: Carbon Footprint, Energy Intensity & Material Footprint Across Robotic System Routes

- Carbon Neutrality & Net Zero Contribution: Pathway to Electric, Autonomous and Low-Emission Mining Fleet

- Responsible Sourcing, Critical Mineral Due Diligence in Robotic System Manufacturing

- Environmental Compliance, Worker Displacement Mitigation & Community Engagement Consideration

- Regulatory-Driven Sustainability, ICMM, SDG 8 (Decent Work) & SDG 9 (Industry Innovation) Alignment & Green Finance Eligibility

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Robot Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Robot Type, Technology & Geography

- Player Classification

- Global Mining Equipment OEM & Autonomous Platform Manufacturer

- Specialist Autonomous Haulage System & Fleet Management Provider

- Autonomous Drilling, Rock Bolting & Underground Equipment Specialist

- Drone, UAV & Aerial Robotic Inspection Provider

- Quadruped, Legged Robot & Confined-Space Inspection Innovator

- Robotic Sorting, Automated Sampling & Laboratory Automation Provider

- AI, Machine Learning & Mining Software Platform Vendor

- System Integrator, EPC & Robotics-as-a-Service (RaaS) Specialist

- Competitive Analysis Frameworks

- Market Share Analysis by Robot Type, Technology & Region

- Company Profile

- Company Overview & Headquarters

- Mining Robotics Products & Technology Portfolio

- Key Customer Relationships & Reference Mine Deployments

- Manufacturing Footprint & Production Capacity

- Revenue (Mining Robotics Segment) & Order Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Capacity Expansion, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Robot Type, Technology, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output