Market Definition

The Global Olefins Market encompasses the production, trading, and downstream conversion of unsaturated aliphatic hydrocarbon compounds containing one or more carbon-carbon double bonds, with the commercially dominant members being ethylene, propylene, butylene isomers including butene-1, butene-2, and isobutylene, and butadiene, produced primarily through the thermally intensive cracking of hydrocarbon feedstocks including ethane, propane, naphtha, liquefied petroleum gas, and gas oil, and secondarily as by-products of fluid catalytic cracking and propane dehydrogenation operations within petroleum refining and natural gas processing infrastructure globally. Olefins occupy the foundational position in the petrochemical value chain as the most widely produced organic chemical building blocks, with ethylene serving as the precursor for polyethylene, ethylene oxide, ethylene dichloride and polyvinyl chloride, ethylene glycol, ethylbenzene and styrene, acetaldehyde, and vinyl acetate, while propylene is converted to polypropylene, acrylonitrile, propylene oxide, cumene and phenol, acrylic acid, oxo-alcohols, and isopropyl alcohol, and butadiene serves as the essential monomer for synthetic rubber grades including styrene-butadiene rubber, polybutadiene rubber, and acrylonitrile-butadiene-styrene copolymer. The market encompasses the complete olefin value chain from feedstock supply and cracker operation through gas fractionation and product purification, pipeline and marine transport, storage and terminal infrastructure, and the integrated derivative units that convert olefins into the polymer, chemical, and specialty product intermediates consumed by the plastics, packaging, rubber, automotive, construction, textile, agricultural, and pharmaceutical end-use industries. Production technologies within the market span steam cracking as the dominant ethylene production route, fluid catalytic cracking as the primary refinery propylene source, propane dehydrogenation for on-purpose propylene production, methanol-to-olefins conversion from coal or natural gas methanol in Chinese operations, ethanol dehydration for bio-based ethylene production, and emerging power-to-chemicals electrification pathways for low-carbon olefin production. Key participants include integrated petrochemical companies, refinery operators, national oil and gas companies, independent chemical producers, trading houses, and the plastics and rubber converters whose consumption volumes define the demand structure of the global olefin market.

Market Insights

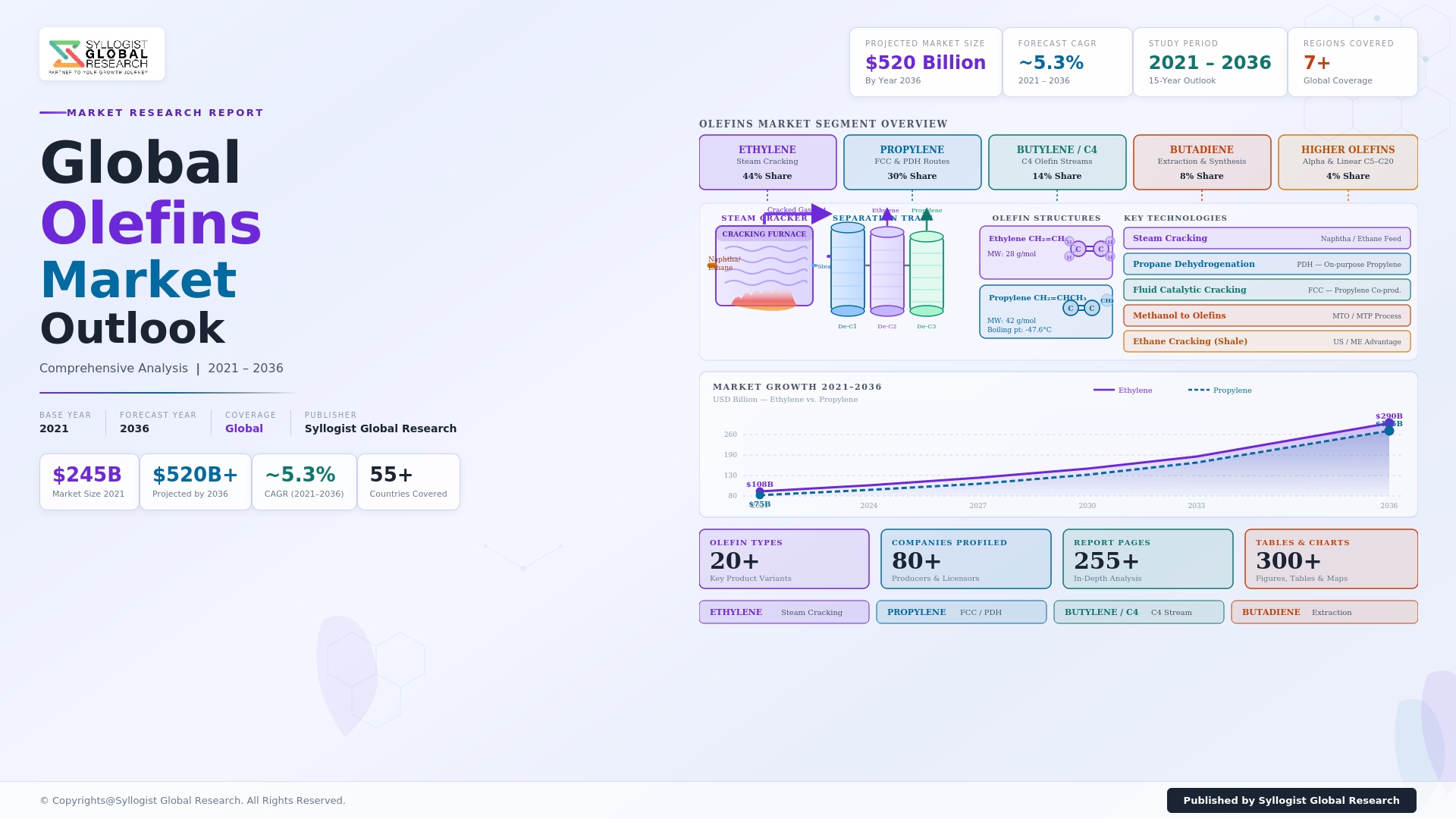

The global olefins market was valued at approximately USD 412.6 billion in 2025 and is projected to reach USD 624.8 billion by 2034, advancing at a compound annual growth rate of 4.7% over the forecast period from 2027 to 2034, driven by the sustained structural growth in polymer demand from packaging, construction, and consumer goods sectors in Asia-Pacific, the Middle East, and Africa whose rising middle-class consumption patterns are expanding polyethylene and polypropylene demand at rates consistently above global GDP growth, the continuing operational advantage of the United States Gulf Coast ethane steam cracking industry whose shale-derived ethane feedstock cost advantage relative to naphtha crackers in Asia and Europe has maintained North American ethylene production at competitive export economics, and the progressive scaling of methanol-to-olefins capacity in China whose coal-based methanol feedstock provides a domestic olefin supply alternative that is partially insulating Chinese polymer consumption from international steam cracking market cycles. Global ethylene production capacity reached approximately 227 million metric tons per year in 2025, with approximately 35 million metric tons of new capacity additions anticipated through 2028 concentrated in China, Iran, the United States, and the Middle East, creating a capacity overhang in light olefins that is suppressing cracker operating rates and margin spreads relative to the high-utilization rate environment of 2017 to 2019 when global ethylene capacity operating rates exceeded 92% and ethylene-ethane spreads in the United States reached approximately USD 580 per metric ton. Global propylene production reached approximately 138 million metric tons in 2025, with the propylene supply mix increasingly diversifying from its historical dependence on steam cracker and fluid catalytic cracker by-product streams toward dedicated on-purpose propylene production through propane dehydrogenation whose selectivity for propylene production eliminates co-product economics uncertainty and enables propylene supply independent of ethylene production decisions.

The ethylene segment dominates the global olefins market by both production volume and revenue value, with ethylene’s conversion into polyethylene representing approximately 62% of total global ethylene consumption in 2025 as polyethylene’s combination of processability, chemical resistance, low cost, and mechanical versatility sustains its position as the world’s most widely produced and consumed polymer. The United States Gulf Coast steam cracking industry, operating primarily on ethane feedstock sourced from the Permian Basin, Eagle Ford, Marcellus, and Utica shale formations at delivered cracker costs of approximately USD 130 to USD 190 per metric ton of ethylene produced, maintains a structural cost advantage of approximately USD 250 to USD 400 per metric ton over naphtha-based steam crackers in Northeast Asia and approximately USD 150 to USD 280 per metric ton over naphtha crackers in Western Europe at current naphtha and ethane price differentials, enabling United States ethylene and polyethylene producers to export material to Asian and Latin American markets at competitive delivered prices while sustaining acceptable margins on export-oriented production increments. The Middle East olefin complex, which benefits from highly subsidized ethane and propane feedstock pricing through government-administered natural gas pricing frameworks in Saudi Arabia, Iran, Qatar, and the United Arab Emirates, has maintained the lowest-cost global production position for ethylene and polyethylene with cracker cash production costs of approximately USD 80 to USD 130 per metric ton enabling competitive delivered pricing into Asian import markets that benchmark against Chinese domestic production economics from methanol-to-olefins and naphtha cracking at approximately USD 550 to USD 750 per metric ton of ethylene production cost. The competitive landscape of the global ethylene and polyethylene market is characterized by a pronounced oversupply condition anticipated through 2027 to 2028 as the large capacity addition wave of 2022 to 2026 in China, the United States, and the Middle East absorbs into demand growth, with industry operating rate projections suggesting ethylene plant utilization remaining below 85% globally through 2026 before demand growth and capacity attrition restore the market balance required for margin recovery.

The propylene and polypropylene segment presents a structurally differentiated demand growth and supply balance dynamic relative to the ethylene market, with propylene demand growing at approximately 4.2% annually in 2025 driven by the exceptional versatility and material performance profile of polypropylene whose lightweight, high stiffness-to-weight ratio, chemical resistance, and recyclability support penetration across automotive weight reduction programs, rigid and flexible packaging, medical devices, and construction materials at the expense of heavier alternative materials including steel, glass, and higher-density polymers. The propylene production mix is undergoing a fundamental shift away from steam cracker by-product and fluid catalytic cracker by-product dependence toward dedicated on-purpose propylene production through propane dehydrogenation, with global propane dehydrogenation capacity reaching approximately 32 million metric tons per year in 2025 and representing approximately 23% of global propylene supply, driven by the economics of propane-to-propylene conversion at favorable propane prices in the United States and Middle East and the growing Chinese investment in propane dehydrogenation as a propylene supply strategy that reduces dependence on naphtha cracker and methanol-to-olefins co-production. Asia-Pacific accounts for approximately 58% of global polypropylene consumption in 2025, with China representing approximately 34% of global demand at approximately 42 million metric tons annually, supporting a domestic polypropylene production capacity of approximately 39 million metric tons per year that still requires net import supply from South Korea, Japan, the Middle East, and Europe to meet demand during peak consumption periods, sustaining export market opportunities for globally competitive polypropylene producers despite China’s rapid domestic capacity expansion. The automotive polypropylene segment is experiencing structural demand growth driven by the lightweighting imperative across both internal combustion engine vehicles seeking fuel economy improvement and electric vehicles seeking range extension through vehicle mass reduction, with polypropylene content per vehicle increasing from approximately 45 kilograms in 2015 to approximately 68 kilograms in 2025 across major vehicle platforms.

The bio-based and circular economy dimension of the global olefins market is emerging as a commercially significant strategic development as major petrochemical producers respond to plastic waste regulation, corporate sustainability commitments, and the potential competitive advantage of supplying low-carbon olefins to consumer goods manufacturers and brands seeking to substantiate environmental claims for their polymer-intensive packaging and consumer product portfolios. Bio-based ethylene produced through the dehydration of bioethanol from sugarcane in Brazil and from corn in the United States is reaching commercial production at approximately 2.4 million metric tons per year globally in 2025, with Braskem’s Green PE from Brazilian sugarcane ethanol production representing the established commercial benchmark for bio-based polyethylene at a carbon footprint approximately 3.09 metric tons of carbon dioxide equivalent below conventional fossil-based polyethylene per metric ton produced, enabling consumer brands to substantiate bio-based and lower-carbon packaging claims that command premium pricing in sustainability-oriented retail channels. Chemical recycling of post-consumer plastic waste through pyrolysis and gasification to produce recycled feedstock for steam cracker operation is advancing from pilot to commercial scale, with LyondellBasell, Sabic, BASF, and Dow investing in pyrolysis oil sourcing and cracker co-feed programs that produce certified recycled content polyethylene and polypropylene under mass balance attribution frameworks whose chain of custody traceability and recycled content certification systems are enabling brands to claim circular economy polymer credentials for specific product lines, potentially disrupting the conventional virgin olefin demand trajectory as recycled content mandates in the European Union and extended producer responsibility schemes in multiple markets progressively require the incorporation of post-consumer recycled content in plastic packaging products through the forecast period.

Key Drivers

Sustained Polymer Demand Growth in Asia-Pacific and Emerging Markets Driven by Rising Middle-Class Consumption, Urbanization, and Packaging Industry Expansion

The structural and demographically anchored growth in polymer consumption across the developing economies of Asia-Pacific, South Asia, the Middle East, Africa, and Latin America, where rising per-capita income, urbanization-driven construction activity, expanding modern retail and food service infrastructure, and growing consumer goods penetration are driving plastic packaging, construction material, and consumer product polymer demand at rates of 5% to 8% annually in the highest-growth markets, provides the most durable and commercially predictable long-term demand driver for the global olefins industry that is sustaining capacity investment decisions despite near-term margin pressures from cyclical oversupply. India’s polymer consumption grew at approximately 8.6% annually in 2025 as organized retail expansion, packaged food adoption, agricultural film usage, and construction activity in residential housing programs sustained demand for polyethylene, polypropylene, and polyvinyl chloride at rates that significantly exceed GDP growth, with India’s per-capita plastic consumption of approximately 14 kilograms annually in 2025 representing less than 25% of the OECD average of approximately 60 kilograms, indicating a large structural gap between current and potential mature consumption levels that will be progressively closed over the forecast period as income and urbanization advance. The food packaging sector, driven by the global expansion of cold chain logistics, convenience food consumption, and e-commerce food delivery that requires protective polymer packaging to maintain product freshness and reduce food waste, is sustaining polyethylene film and polypropylene rigid container demand growth at approximately 5.2% annually globally, providing a defensive consumption base that is less susceptible to economic cycle downturns than industrial or construction polymer applications and sustaining ethylene and propylene demand stability through global economic fluctuations.

United States Ethane Cost Advantage from Shale Gas Development and Middle East Subsidized Feedstock Positioning Low-Cost Regions for Sustained Export Market Growth

The sustained development of North American shale gas production that has maintained Henry Hub natural gas prices at approximately USD 2.50 to USD 3.50 per million British thermal units and ethane prices at approximately USD 0.18 to USD 0.28 per gallon since 2015, combined with the extraordinary capital investment in United States Gulf Coast steam cracking and polyethylene capacity of approximately USD 62 billion between 2017 and 2025 by ExxonMobil, Dow, LyondellBasell, Chevron Phillips, and Formosa Plastics, has established the United States as the world’s largest polyethylene exporter at approximately 13 million metric tons per year, fundamentally reshaping global polymer trade flows and creating a persistent competitive cost challenge for naphtha-based producers in Asia and Europe whose feedstock economics are structurally at a disadvantage of USD 200 to USD 400 per metric ton of ethylene production cost relative to US ethane-based crackers at prevailing global energy prices. The Middle East’s combination of state-subsidized ethane and propane feedstock through Saudi Aramco, ADNOC, and National Petrochemical Company supply agreements, world-scale integrated cracker and polyethylene complex operations at Sadara, Kemya, Arrazi, and Borouge facilities, and strategic export positioning to Asian and African growth markets has maintained the Gulf Cooperation Council as the second-lowest-cost global polyethylene production region behind the United States, with Middle Eastern producers progressively moving up the petrochemical value chain toward specialty polymers and high-performance engineering thermoplastics that provide higher margin realization than commodity polyethylene grades facing increasing competition from Chinese capacity expansion. The competitive advantage of ethane-based crackers is expected to persist through the forecast period as United States shale gas production remains abundant and the capital recovery requirements of the 2017 to 2025 cracker investment wave incentivize continued high utilization of installed capacity regardless of shorter-term margin cycle fluctuations that create periodic financial pressure but do not alter the structural feedstock cost advantage underlying long-term competitive positioning.

Polypropylene Automotive Lightweighting, Medical Device, and Infrastructure Applications Driving Above-Market-Average Propylene and Polypropylene Demand Growth

Propylene and polypropylene are experiencing structural demand growth across automotive lightweighting, medical device, and durable infrastructure applications that is generating above-market-average demand expansion independent of the general polymer market cycle, as the technical performance advantages of polypropylene in impact resistance, chemical resistance, thermal stability, and processability support material substitution gains against heavier metallic and glass alternatives in applications where vehicle weight reduction, single-use medical device sterilizability, and construction material durability provide compelling functional justification for premium-positioned polypropylene grades. Electric vehicle manufacturing is creating a particularly favorable structural demand environment for polypropylene, as battery enclosure systems, thermal management components, high-voltage cable insulation, and lightweight structural components in electric vehicles require polypropylene grades with specific dielectric, flame retardant, and thermomechanical performance characteristics that are progressively replacing conventional materials in architecturally redesigned electric vehicle platforms, with polypropylene content per battery electric vehicle estimated at approximately 75 to 90 kilograms compared to approximately 60 to 68 kilograms in equivalent internal combustion engine vehicles. The global medical polypropylene market is growing at approximately 7.8% annually as the expansion of single-use medical device manufacturing driven by infection prevention protocol adoption, aging population healthcare demand, and the geographic expansion of formal healthcare systems in emerging economies creates sustained demand for medical-grade polypropylene whose clarity, sterilizability, and biocompatibility requirements command processing premiums that support higher propylene derivative value realization than commodity packaging grades, providing propylene producers and propane dehydrogenation operators with access to value-added product markets that partially insulate their revenue from commodity polypropylene price cycles driven by packaging demand fluctuations.

Key Challenges

Structural Capacity Oversupply, Compressed Cracker Margins, and Extended Market Rebalancing Timeline Creating Financial Pressure Across the Global Olefins Industry

The global olefins industry is navigating a prolonged period of capacity oversupply created by the convergence of major ethylene and polypropylene capacity addition waves in China, the United States, and the Middle East between 2020 and 2026 that collectively added approximately 55 million metric tons per year of new ethylene capacity in a compressed five-year period that demand growth of approximately 3.5% to 4.0% annually cannot absorb within the timeframe projected by the industry at investment decision, generating a structural margin compression environment in which ethylene cracker operating rates have declined below 85% globally and variable margin spreads of ethylene over naphtha and ethylene over ethane have fallen to levels that in some regional markets approach or temporarily fall below cash cost of production, creating financial distress at high-cost naphtha cracking assets and incentivizing temporary production rationalization that is insufficient to restore market balance given the scale of capacity overhang. Chinese methanol-to-olefins capacity expansion, adding approximately 8 to 12 million metric tons per year of ethylene and propylene production from coal-based methanol through 2026, represents a particularly persistent source of structural oversupply in the Asian market whose coal feedstock pricing independence from global crude oil and naphtha price cycles means methanol-to-olefins operators can continue production through naphtha cracker margin downturns that would force production cuts at conventional cracker facilities, making Chinese methanol-to-olefins capacity a market-of-last-resort volume supplier that effectively establishes the price floor in regional Asian olefin markets at coal-based methanol-to-olefins variable cost economics. Industry projections suggest that the global ethylene market will not return to an operating rate above 88% before 2027 to 2028, meaning that the margin compression environment will persist through the near-term forecast horizon and continue to suppress cracker profitability and new investment sanctioning across all but the lowest-cost production regions.

Plastic Waste Regulation, Extended Producer Responsibility Schemes, and Sustainability Mandates Creating Structural Demand Uncertainty for Virgin Olefin-Derived Polymers

The accelerating implementation of plastic waste reduction legislation, single-use plastic bans, and extended producer responsibility schemes across the European Union, United Kingdom, China, India, and multiple emerging market jurisdictions is creating structural demand uncertainty for virgin polyethylene and polypropylene derived from conventional fossil-based olefin production, as recycled content mandates, plastic tax instruments, and packaging take-back requirements progressively incentivize the substitution of virgin polymer with post-consumer recycled content material, bio-based polymer alternatives, and in some applications the elimination of plastic packaging formats entirely. The European Union’s Packaging and Packaging Waste Regulation, which mandates minimum recycled content levels of 10% to 55% in plastic packaging by 2030 depending on packaging type, combined with the EU Plastics Tax of EUR 0.80 per kilogram on non-recycled plastic packaging waste effective from 2021, creates a direct financial incentive to reduce virgin polyethylene and polypropylene consumption in European packaging applications that is simultaneously increasing the cost of unsorted plastic waste disposal for member state governments and brand owners while improving the economics of mechanical recycling and chemical recycling investments that compete with virgin polymer demand. India’s Plastic Waste Management Rules amendments and the Progressive Extended Producer Responsibility framework requiring plastic packaging producers and importers to achieve defined recycling targets are progressively increasing compliance cost for virgin polymer users and creating institutional investment in plastic waste collection and processing infrastructure that will support a growing domestic recycled polymer supply competing with virgin polyethylene and polypropylene demand, while China’s aggressive single-use plastic ban implementation covering approximately 15 product categories is reducing polyethylene demand in previously significant end-use applications at rates that are partially offsetting growth in other consumption categories.

Energy Transition, Carbon Pricing, and Decarbonization Pressure on Steam Cracker Operations Increasing Cost Structure and Creating Long-Term Asset Viability Uncertainty for Carbon-Intensive Production

Steam cracking of hydrocarbons is among the most energy-intensive industrial processes globally, with a world-scale naphtha steam cracker of 1 million metric tons per year ethylene capacity consuming approximately 15 to 20 gigajoules of fuel energy per metric ton of ethylene produced and emitting approximately 0.8 to 1.2 metric tons of carbon dioxide per metric ton of ethylene from process heating, representing a total annual carbon dioxide emission of approximately 800,000 to 1.2 million metric tons per cracker that is increasingly subject to carbon pricing mechanisms including the European Union Emissions Trading System, UK ETS, and emerging carbon cost frameworks in South Korea, Singapore, and China whose progressive phase-in of full-cost carbon pricing will add approximately USD 50 to USD 100 per metric ton of ethylene production cost to European cracker operations by 2030, materially altering the competitive cost structure of European olefin production relative to regions without equivalent carbon pricing. The electrification of steam cracker furnaces, which are currently fired by fossil natural gas or liquid hydrocarbons to supply the endothermic cracking reaction heat at tube temperatures of 800 to 850 degrees Celsius, using renewable electricity through resistive or plasma heating technologies is being developed by BASF, LyondellBasell, and Technip Energies in collaborative demonstration projects that could potentially reduce cracker carbon emissions by approximately 90% relative to fossil fuel firing, but whose commercial readiness timeline extends to 2030 to 2035 for initial commercial-scale deployment and whose economic viability at scale depends on the availability of renewable electricity at prices below approximately USD 0.04 to USD 0.06 per kilowatt-hour to remain competitive with fossil-fired cracking at current and projected carbon prices. The capital investment required to decarbonize existing steam cracker operations through fuel switching, electrification, carbon capture and storage, or hydrogen co-firing is estimated at USD 400 million to USD 1.2 billion per cracker complex depending on technology pathway and scale, creating a decarbonization capital burden that is competing with normal maintenance and debottlenecking investment and creating financial planning challenges for cracker owners whose return on decarbonization investment depends on carbon price trajectories and green hydrogen costs that cannot be reliably projected over twenty-year investment horizons.

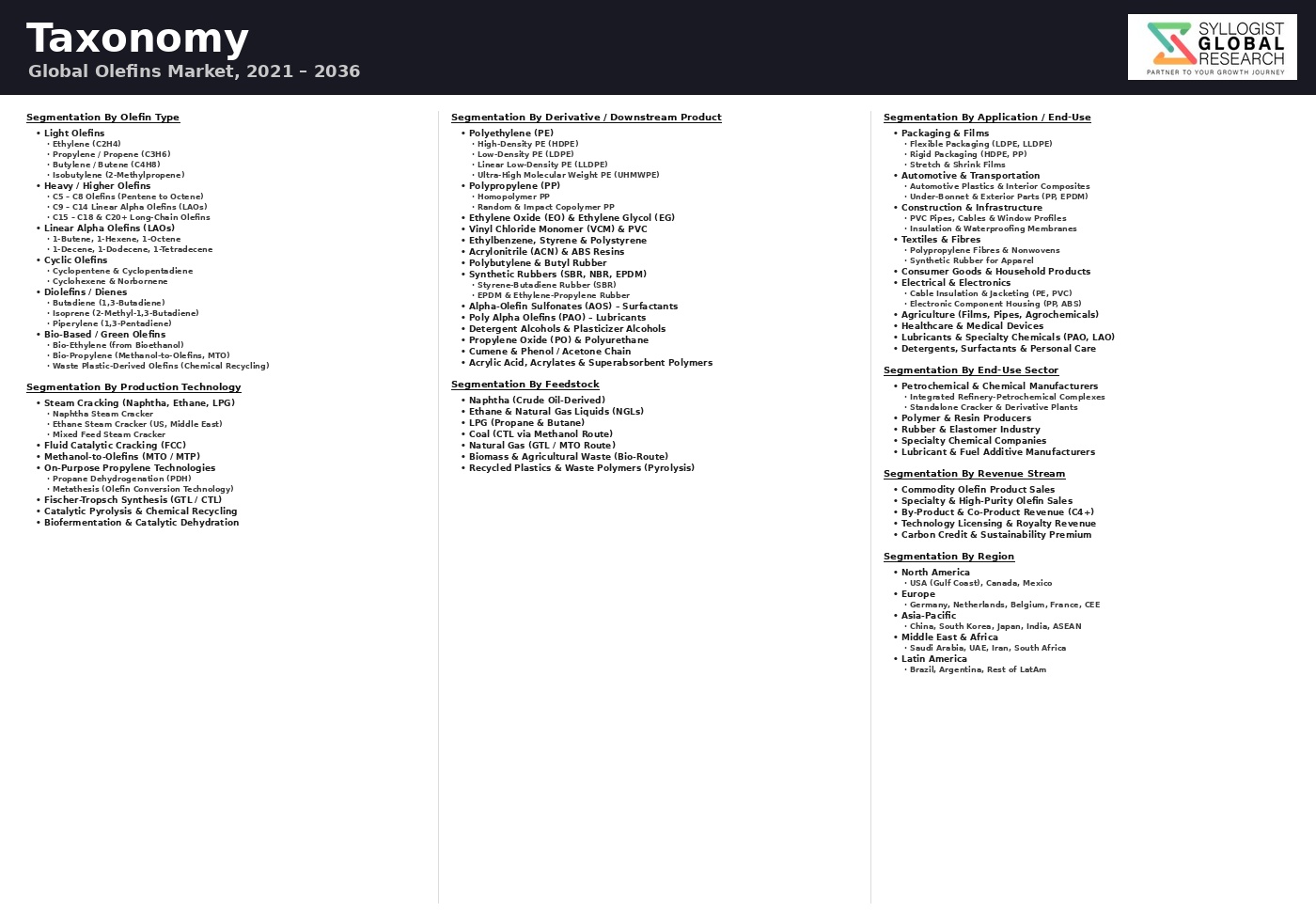

Market Segmentation

- Segmentation By Olefin Type

- Ethylene

- Propylene

- Butylene (Butene-1, Butene-2, and Isobutylene)

- Butadiene

- Alpha-Olefins (1-Hexene, 1-Octene, and Higher Alpha-Olefins)

- Others

- Segmentation By Production Technology

- Steam Cracking (Naphtha, Ethane, Propane, and Gas Oil Feedstock)

- Fluid Catalytic Cracking (Refinery Propylene and Butylene)

- Propane Dehydrogenation (PDH)

- Methanol-to-Olefins (MTO) and Methanol-to-Propylene (MTP)

- Coal-to-Olefins (CTO)

- Ethanol Dehydration (Bio-Based Ethylene)

- Fischer-Tropsch Olefin Production

- Others

- Segmentation By Feedstock

- Naphtha

- Ethane

- Propane and LPG

- Natural Gas (via Methanol)

- Coal (via Methanol)

- Bio-Based Feedstocks (Bioethanol and Vegetable Oils)

- Recycled Plastic Pyrolysis Oil

- Others

- Segmentation By Downstream Derivative

- Polyethylene (HDPE, LDPE, and LLDPE)

- Polypropylene (Homopolymer and Copolymer)

- Polyvinyl Chloride (PVC)

- Ethylene Oxide and Glycol

- Styrene and Acrylonitrile-Butadiene-Styrene (ABS)

- Synthetic Rubber (SBR, BR, and EPDM)

- Oxo-Alcohols and Acrylates

- Polypropylene Fibers and Non-Woven Fabrics

- Others

- Segmentation By End-Use Industry

- Packaging (Flexible and Rigid)

- Automotive and Transportation

- Construction and Infrastructure

- Agriculture (Films, Pipes, and Irrigation)

- Textiles and Non-Woven Fabrics

- Healthcare and Medical Devices

- Electrical and Electronics

- Consumer Goods and Household Products

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Olefins Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by olefin type including ethylene, propylene, butylene, butadiene, and alpha-olefins, by production technology including steam cracking on naphtha and ethane feedstock, fluid catalytic cracking, propane dehydrogenation, methanol-to-olefins, and bio-based ethylene routes, by downstream derivative including polyethylene, polypropylene, polyvinyl chloride, ethylene oxide and glycol, and synthetic rubber, and by end-use industry including packaging, automotive, construction, agriculture, textiles, and healthcare, to enable integrated petrochemical producers, polymer converters, specialty chemical companies, infrastructure investors, and energy transition strategists to identify the highest-growth derivative and application combinations across the global olefins value chain through 2034?

- How is the global ethylene capacity overhang of approximately 55 million metric tons per year added between 2020 and 2026 in China, the United States, and the Middle East expected to be absorbed through demand growth, capacity rationalization, and cracker utilization rate normalization on a region-by-region and feedstock-specific basis through the forecast period, and what are the projected ethylene and ethylene-naphtha spread trajectories for the United States Gulf Coast, Western Europe, Northeast Asia, and the Middle East under different crude oil, naphtha, and natural gas price scenarios, and at what operating rate level and timeline does the global ethylene market reach the 88% to 90% utilization threshold at which producer margins recover to levels that re-incentivize new grassroots cracker investment decisions?

- What are the production cost economics, carbon footprint per metric ton, capital cost, and technology readiness level of bio-based ethylene from sugarcane and corn bioethanol, chemical recycling-derived olefins from plastic pyrolysis oil steam cracker co-feeding, power-to-chemicals electrolysis-based pathways, and electrified steam cracker furnace technology, and how are regulatory drivers including the European Union Packaging and Packaging Waste Regulation recycled content mandates, national plastic taxes, and voluntary brand owner sustainability commitments creating commercially quantifiable demand premiums for certified bio-based, recycled-content, and low-carbon olefin-derived polymers that are justifying above-cost-parity investment in these emerging production pathways by major petrochemical producers including LyondellBasell, Dow, BASF, Sabic, and Braskem?

- How are the European Union Emissions Trading System carbon price trajectory toward USD 130 per metric ton by 2030, the progressive phase-out of free carbon allowance allocation for the chemical sector from 2026, the Carbon Border Adjustment Mechanism application to organic chemicals and polymers under potential scope expansion beyond current product coverage, and equivalent carbon pricing mechanisms in South Korea, Singapore, and China affecting the competitive cost position of European naphtha-based steam cracker operations relative to United States ethane-based and Middle Eastern subsidized feedstock crackers, and what decarbonization technology pathways including electrified cracking, hydrogen co-firing, and carbon capture and storage are European petrochemical companies evaluating to maintain operational competitiveness and social license within an increasingly carbon-priced production environment?

- What is the current production capacity, competitive cost structure, methanol feedstock supply chain, propylene and ethylene output quality, and growth investment program of China’s methanol-to-olefins and coal-to-olefins industry, and how is Chinese domestic olefin production from methanol-to-olefins, propane dehydrogenation, and new naphtha steam cracker investments affecting China’s net import position for polyethylene, polypropylene, and other olefin derivatives, and what are the implications of China’s trajectory toward olefin self-sufficiency and potential net export status for the global olefin trade flows, price dynamics, and competitive positioning of export-oriented producers in the United States, Middle East, South Korea, Japan, and Europe whose current and planned export volumes are directly dependent on continued Chinese net polymer import demand through the forecast period?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Crude Oil, Naphtha & NGL Feedstock Price Volatility & Supply Disruption Risk

- Capacity Oversupply, Margin Compression & Cracker Utilisation Rate Cycle Risk

- Regulatory, Plastic Restriction & Single-Use Plastic Ban Risk Impacting Downstream Derivative Demand

- Energy Transition & Carbon Pricing Risk: Scope 1 & 2 Emission Cost Exposure for Energy-Intensive Steam Cracking Operations

- Geopolitical, Trade Tariff & Petrochemical Complex Concentration Risk in Middle East & Asia

- Regulatory Framework & Standards

- Plastic Regulation & Single-Use Plastic Directive: EU SUP Directive (2019/904), US Plastic Pollution Prevention & Responsibility Act, China Plastic Restriction Order & National Plastic Waste Policy Impact on Polyethylene & Polypropylene Demand

- Carbon Pricing, EU ETS, Carbon Border Adjustment Mechanism (CBAM) & National Carbon Tax Impact on Ethylene & Propylene Production Cost Competitiveness

- REACH, Hazardous Chemical Control & VOC Emission Regulation for Olefin Derivative Production: EU REACH, US TSCA, China MEE Standards & Industrial Emission Directive Compliance

- Product Specification & Quality Standard for Olefins: ASTM, ISO & National Industry Standards for Polymer-Grade Ethylene, Polymer-Grade Propylene & Butadiene Purity

- Bio-Based Plastics & Circular Economy Policy: EU Packaging Regulation Recycled Content Mandate, Bioplastics Standard (EN 13432, ASTM D6400) & Extended Producer Responsibility (EPR) Driving Bio-Olefin Demand

- Global Olefins Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Million Tonnes)

- Market Size & Forecast by Olefin Type

- Ethylene

- Propylene

- Butadiene (1,3-Butadiene)

- Isobutylene & Butylenes (1-Butylene, cis-2-Butylene & trans-2-Butylene)

- Linear Alpha Olefins (LAO: C4, C6, C8, C10, C12 & Higher)

- Higher Olefins & Internal Olefins

- Bio-Based Olefins (Bio-Ethylene, Bio-Propylene & Bio-Butadiene)

- Market Size & Forecast by Production Process

- Steam Cracking (Naphtha, Ethane, LPG & Gas Oil Feedstock)

- Fluid Catalytic Cracking (FCC) for On-Purpose & Co-Product Propylene

- Propane Dehydrogenation (PDH) for On-Purpose Propylene

- Methanol-to-Olefins (MTO) & Methanol-to-Propylene (MTP)

- Coal-to-Olefins (CTO) via Gasification & MTO Route

- Oxidative Dehydrogenation (ODH) of Ethane & On-Purpose Butadiene

- Bio-Based Route: Ethanol Dehydration, Sugar-to-Olefin & Fermentation-Based

- Market Size & Forecast by Feedstock

- Naphtha (Petroleum-Derived, Primary Global Steam Cracker Feed)

- Ethane (Natural Gas Liquid: US, Middle East & Shale-Derived)

- LPG (Propane & Butane Mix)

- Gas Oil & Heavy Oil Feed

- Methanol (Coal-Based, Gas-Based & Bio-Based)

- Bioethanol & Sugarcane (Bio-Olefin Route)

- Market Size & Forecast by Grade

- Polymer Grade (Ethylene & Propylene, Purity Above 99.5%)

- Chemical Grade (Ethylene & Propylene, Purity 95 to 99%)

- Refinery & Fuel Grade

- Rubber & Synthetic Elastomer Grade (Butadiene)

- Market Size & Forecast by Derivative & Downstream Application

- Polyethylene (HDPE, LDPE, LLDPE, UHMWPE & mLLDPE)

- Polypropylene (PP Homopolymer, Random Copolymer & Impact Copolymer)

- Polyvinyl Chloride (PVC) via Ethylene Dichloride (EDC) & VCM

- Ethylene Oxide & Ethylene Glycol (MEG, DEG, TEG)

- Ethylbenzene & Styrene

- Acrylonitrile & Acrylic Acid (via Propylene Ammoxidation & Oxidation)

- Oxo Chemicals & Oxo Alcohols (via Propylene & Butylene)

- Synthetic Rubber (SBR, BR, NBR & IIR via Butadiene & Isobutylene)

- Polyalphaolefins (PAO) & Synthetic Lubricant Base Oil (via LAO)

- Detergent Alcohol, Linear Alkylbenzene (LAB) & Surfactant (via LAO)

- Market Size & Forecast by End-Use Industry

- Packaging (Flexible Plastic Film, Rigid Container & Industrial Packaging)

- Automotive & Transportation (Polypropylene Interior, Polyethylene Pipe & Synthetic Rubber Tyre)

- Construction & Infrastructure (PVC Pipe, PE Pipe, Insulation & Geomembrane)

- Textile & Fibre (Polypropylene Fibre, Polyester, Nylon & Nonwoven Fabric)

- Consumer Goods & Household Products (Appliance, Furniture & FMCG Packaging)

- Healthcare & Pharmaceutical (Medical Device, Drug Packaging & Sterile Film)

- Adhesives, Coatings, Sealants & Paints

- Agriculture (Agricultural Film, Irrigation Pipe & Agrochemical Feedstock)

- Market Size & Forecast by Sales Channel

- Long-Term Supply Agreement (Term Contract Direct to Petrochemical Derivative Producer)

- Spot Market, OTC Trading & Commodity Exchange (ICE, CME NYMEX)

- Integrated Pipeline & Cracker-to-Derivative Complex (Captive Internal Transfer)

- Merchant, Trader & Distributor Channel

- North America Olefins Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Tonnes)

- By Olefin Type

- By Production Process

- By Feedstock

- By Grade

- By Derivative & Downstream Application

- By End-Use Industry

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Olefins Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Tonnes)

- By Olefin Type

- By Production Process

- By Feedstock

- By Grade

- By Derivative & Downstream Application

- By End-Use Industry

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Olefins Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Tonnes)

- By Olefin Type

- By Production Process

- By Feedstock

- By Grade

- By Derivative & Downstream Application

- By End-Use Industry

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Olefins Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Tonnes)

- By Olefin Type

- By Production Process

- By Feedstock

- By Grade

- By Derivative & Downstream Application

- By End-Use Industry

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Olefins Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Tonnes)

- By Olefin Type

- By Production Process

- By Feedstock

- By Grade

- By Derivative & Downstream Application

- By End-Use Industry

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Olefins Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Tonnes)

- By Olefin Type

- By Production Process

- By Feedstock

- By Grade

- By Derivative & Downstream Application

- By End-Use Industry

- By Country

- By Sales Channel

- Market Size & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Germany, France, Belgium, Netherlands, United Kingdom, Italy, Spain, Saudi Arabia, UAE, Iran, Kuwait, Qatar, China, Japan, South Korea, India, Singapore, Taiwan, Thailand, Brazil, Mexico

- Technology Landscape & Innovation Analysis

- Steam Cracking Furnace Design, Advanced Tube Material, Coke Mitigation & Energy Efficiency Technology Deep-Dive

- Methanol-to-Olefins (MTO) & Methanol-to-Propylene (MTP) Catalyst Development, Reactor Design & Regeneration Technology

- Propane Dehydrogenation (PDH) Catalyst System, Reactor Configuration & Selectivity Optimisation Technology

- Fluid Catalytic Cracking (FCC) Catalyst & Hardware Modification for Maximum On-Purpose Propylene Technology

- Bio-Based Olefin Production Technology: Ethanol Catalytic Dehydration, Sugar-to-Olefin Fermentation & Biomass Gasification Route

- Steam Cracker Decarbonisation Technology: Electric Cracking Furnace, Green Hydrogen Co-Firing & Carbon Capture Integration

- Advanced Separation, Cryogenic Distillation, Heat Integration, Process Digitalisation & AI-Based Cracker Optimisation Technology

- Patent & IP Landscape in Olefin Production & Derivative Technologies

- Value Chain & Supply Chain Analysis

- Upstream Feedstock Supply Chain: Crude Oil, Naphtha, NGL, Ethane, LPG & Methanol Supply & Price Dynamics

- Steam Cracker & Olefin Production Plant Technology & Equipment Supplier Landscape

- Catalyst & Chemical Additive Supply Chain for MTO, PDH, FCC & Steam Cracking

- Olefin Producer, World-Scale Cracker & Integrated Petrochemical Complex Landscape

- Derivative Producer Integration: Polyethylene, Polypropylene, PVC, MEG & Rubber Plant

- Commodity Trader, Logistics, Pipeline, Tanker & Storage Terminal Supply Chain

- Convertor, End-Market Processor & Circular Economy Recycling Loop

- Pricing Analysis

- Ethylene Spot & Contract Price Analysis by Region (NWE, SEA, US Gulf Coast, NEA) & Feedstock Cost Correlation

- Propylene Price Analysis: Polymer Grade vs. Chemical Grade vs. Refinery Grade & PDH vs. FCC vs. Steam Cracker Co-Product Price Differential

- Butadiene & Butylene Price Analysis: C4 Stream Extraction Cost vs. Spot Price & Synthetic Rubber Demand Correlation

- Linear Alpha Olefin (LAO) Price Analysis by Carbon Chain Length (C4 to C12 Plus) & Derivative Application Premium

- Steam Cracking Cash Cost Analysis by Feedstock: Naphtha vs. Ethane vs. LPG vs. Gas Oil Cracker Cost Competitiveness by Region

- Olefin Derivative Spread Analysis: Ethylene to Polyethylene Spread, Propylene to Polypropylene Spread & MEG Spread vs. Historical Benchmark

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Olefin Production Routes: Carbon Footprint of Naphtha Cracking vs. Ethane Cracking vs. MTO vs. Bio-Based Route per Tonne Ethylene & Propylene

- Steam Cracker Net Zero Roadmap: Electric Furnace, Green Hydrogen Co-Firing, CCUS Retrofit & Renewable Energy Integration for Olefin Production Decarbonisation

- Circular Economy & Mechanical Recycling: Polyethylene & Polypropylene Post-Consumer Recycled (PCR) Content Target Impact on Virgin Olefin Demand Trajectory

- Chemical Recycling & Pyrolysis-to-Naphtha: Plastic Waste as Alternative Feedstock for Steam Cracker & Circular Olefin Production

- Regulatory-Driven Sustainability: EU Packaging Regulation Recycled Content Mandate, CBAM Impact on Olefin Trade Flows & Corporate Net Zero Supply Chain Target Effect on Bio-Olefin Demand

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Olefin Type & Geography)

- Top 10 Players Market Share by Production Capacity & Volume

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Olefin Type, Production Process & Geography

- Player Classification

- Global Integrated Refinery & Petrochemical Major with World-Scale Steam Cracker Portfolio

- State-Owned Petrochemical Enterprise & National Oil Company Olefin Complex

- Dedicated Olefin & Polymer Producer (Pure-Play Cracker Operator)

- MTO & Coal-to-Olefins (CTO) Producer (China-Centric)

- On-Purpose PDH & Propylene Specialist

- Bio-Based Olefin & Green Petrochemical Pioneer

- Linear Alpha Olefin (LAO) Specialist & Synthetic Lubricant Precursor Producer

- Technology Licensor & Catalyst Supplier for Olefin Production

- Competitive Analysis Frameworks

- Market Share Analysis by Olefin Type, Production Process & Region

- Company Profile

- Company Overview & Headquarters

- Olefin Products, Production Process & Derivative Portfolio

- Key Customer Relationships & Offtake Agreements

- Manufacturing Footprint, Cracker Location & Nameplate Capacity (ktpa)

- Revenue (Olefins Segment) & EBITDA

- Technology Differentiators, Catalyst Assets & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Capacity Expansion, Debottleneck, Feedstock Switch, Net Zero Milestone)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Cost Competitiveness vs. Derivative Integration Breadth)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Olefin Type, Production Process, Feedstock, Derivative & Geography

- White Space Opportunity Analysis

- Strategic Output

- Strategic Recommendations

- Product Portfolio & Cracker Technology Investment Strategy

- Manufacturing, Feedstock Optimisation & Operational Excellence Strategy

- Geographic Expansion & Market Development Strategy

- Customer & Derivative Producer Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability, Decarbonisation & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)