Market Definition

The Global Plasticizers Market encompasses the development, production, distribution, and application of chemical additives incorporated into polymers and resins to increase their flexibility, workability, durability, and elongation properties by reducing the intermolecular forces and glass transition temperature of the base polymer matrix, enabling the processing and end-use performance of materials that would otherwise be rigid, brittle, or difficult to fabricate at ambient conditions. Plasticizers are primarily consumed in polyvinyl chloride formulations, where they are used extensively to produce flexible PVC products across flooring, wall coverings, cables and wires, medical tubing and bags, automotive interior components, synthetic leather, coated fabrics, films and sheets, roofing membranes, and consumer goods, and are also applied in polyvinyl butyral, cellulose esters, polyurethane, polylactic acid, and other polymer systems requiring flexibility modification. The market encompasses a broad range of chemical families including phthalate plasticizers such as diisononyl phthalate, diisodecyl phthalate, and di-2-ethylhexyl phthalate; non-phthalate alternatives including dioctyl terephthalate, diisononyl cyclohexane-1,2-dicarboxylate, trioctyl trimellitate, acetyl tributyl citrate, and epoxidized vegetable oil plasticizers; adipate and sebacate esters for low-temperature flexibility applications; polymeric plasticizers for permanence-critical applications; and bio-based plasticizer platforms derived from renewable feedstocks including citrates, succinates, and isosorbide derivatives. The complete value chain encompasses petrochemical and oleochemical raw material suppliers, plasticizer manufacturer and formulators, compounders, and end-use fabricators across construction, automotive, electrical, medical, packaging, and consumer product industries whose regulatory and performance specifications define the formulation requirements governing plasticizer selection and supply across major global manufacturing markets.

Market Insights

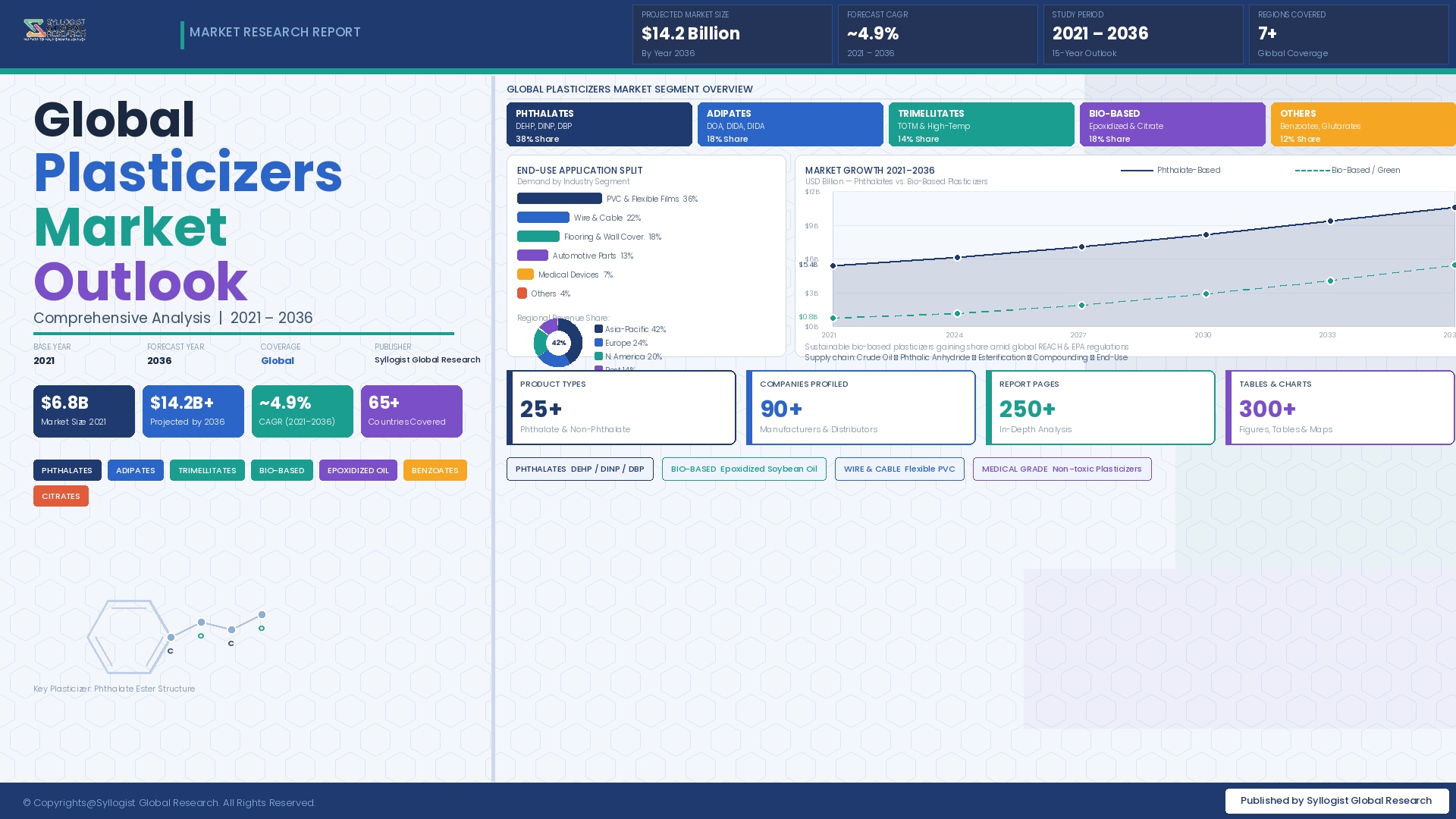

The global plasticizers market was valued at approximately USD 18.3 billion in 2025 and is projected to reach USD 26.7 billion by 2034, advancing at a compound annual growth rate of 4.1% over the forecast period from 2027 to 2034. The foundational demand driver is the continuing large-scale consumption of flexible polyvinyl chloride across construction, electrical, and automotive applications in both established and rapidly industrializing economies, where PVC’s cost-performance advantage over alternative flexible polymers sustains its dominant position in high-volume applications despite competitive pressure from thermoplastic elastomers and polyolefin alternatives. The market is simultaneously navigating a structural transition from legacy phthalate plasticizer systems toward non-phthalate and bio-based alternatives, driven by regulatory restriction, brand owner sustainability commitments, and end-consumer preference evolution, which is reshaping the revenue composition and supplier competitive dynamics of the market while sustaining overall volume growth across the forecast period.

The non-phthalate plasticizer segment is the most commercially dynamic sub-market within the global plasticizers industry, advancing at approximately 6.9% annually compared to the 1.8% annual growth trajectory of the legacy phthalate segment, as regulatory frameworks in the European Union, United States, Canada, Japan, and South Korea progressively restrict or eliminate the use of ortho-phthalate plasticizers in children’s products, food contact materials, medical devices, and increasingly in general flexible PVC applications. Dioctyl terephthalate has emerged as the dominant volume non-phthalate alternative in flexible PVC general applications, achieving commercial scale economics that are approaching parity with incumbent diisononyl phthalate in regions with established terephthalate production infrastructure. Diisononyl cyclohexane-1,2-dicarboxylate, a hydrogenated phthalate structure with demonstrated low toxicological profile, has achieved broad acceptance in sensitive end-use applications including medical-grade flexible PVC tubing and bags, food contact flexible films, and children’s product materials, and is growing at approximately 9.3% annually as medical device manufacturers and food packaging producers complete their phthalate phase-out programs.

Asia-Pacific dominates global plasticizer consumption, accounting for approximately 52% of total volume in 2025, driven by China’s position as both the world’s largest polyvinyl chloride producer and the world’s largest consumer of flexible PVC products across construction flooring, cable insulation, agricultural film, synthetic leather, and consumer goods applications, supported by the rapidly expanding flexible PVC consumption of India, Southeast Asia, and the broader Asian manufacturing corridor. China’s domestic plasticizer market is undergoing a quality and regulatory upgrade cycle, with stricter enforcement of restrictions on certain ortho-phthalates in food contact and children’s product applications accelerating the adoption of dioctyl terephthalate and other non-phthalate alternatives by Chinese flexible PVC compounders, generating incremental demand for domestically produced non-phthalate plasticizer grades. Europe represents the most advanced regional market in terms of non-phthalate adoption, with the REACH regulation’s restriction of di-2-ethylhexyl phthalate, dibutyl phthalate, benzyl butyl phthalate, and diisobutyl phthalate across a wide range of applications having effectively eliminated these substances from European flexible PVC supply chains, positioning European plasticizer demand as a leading indicator of the global regulatory and technology transition trajectory.

Bio-based and renewable plasticizers represent the fastest-growing technology segment within the global plasticizers market, advancing from a commercially nascent position to approximately 7.4% of global plasticizer volume in 2025, driven by brand owner sustainability commitments, bio-based content certification requirements in certain regulated applications, and the improving cost-competitiveness of citrate ester, epoxidized soybean oil, and isosorbide-based plasticizer platforms relative to fossil-derived alternatives. Epoxidized soybean oil and epoxidized linseed oil, which function as both plasticizers and heat stabilizer co-agents in flexible PVC formulations, represent the largest volume bio-based plasticizer category and are well-established in flexible PVC applications across food packaging films, agricultural mulch films, and coated fabric segments in regions with established soybean and linseed oil processing infrastructure. The development of second-generation bio-based plasticizer platforms with performance profiles matching petroleum-derived plasticizers in critical parameters including low-temperature flexibility, permanence, and electrical resistivity is progressing rapidly, creating commercial opportunities for specialty chemical companies capable of delivering both the renewable content credentials and the technical performance required by demanding flexible PVC application segments in medical, automotive, and premium consumer product markets.

Key Drivers

Construction Sector Expansion and Flexible PVC Demand Growth in Flooring, Roofing, and Electrical Cable Applications Sustaining Structural Plasticizer Volume

The global construction industry remains the single largest end-use sector for plasticizers, generating sustained high-volume demand across resilient vinyl flooring, luxury vinyl tile and plank, plastisol-coated wallcoverings, flexible roofing membranes, waterproofing geomembranes, and polyvinyl chloride-insulated electrical wire and cable systems whose installation volumes are directly linked to residential and commercial construction activity in both mature and rapidly developing economies. Construction spending across Asia-Pacific, the Middle East, and Africa is generating incremental new-build volume demand for plasticizer-containing PVC construction products that is supplemented by renovation and refurbishment activity in mature markets, where the replacement of aging flooring, wall covering, and roofing systems drives durable aftermarket plasticizer consumption that is substantially independent of new construction cycle fluctuations. The electrification of transportation infrastructure, including charging network installation, grid modernization programs, and the expansion of renewable energy transmission capacity, is generating sustained demand growth for flexible PVC cable insulation and jacketing compounds, each requiring plasticizer content of approximately 25% to 40% by weight, across applications where flexible PVC maintains a dominant market position relative to thermoplastic polyolefin and cross-linked polyethylene alternatives based on its combination of flame retardancy, flexibility, processability, and installed-cost economics at scale across both low-voltage and medium-voltage cable applications.

Regulatory-Driven Phthalate Phase-Out Programs Accelerating Non-Phthalate Adoption and Generating Premium Plasticizer Technology Upgrade Investment

Accelerating regulatory restriction of ortho-phthalate plasticizers across the European Union, United States, Canada, and a growing number of Asia-Pacific jurisdictions is compelling flexible PVC formulators, compounders, and end-use manufacturers to qualify and adopt non-phthalate plasticizer alternatives across their entire product portfolios, generating a multi-year technology upgrade investment cycle that creates substantial new product development, qualification, and supply positioning opportunities for specialty plasticizer manufacturers with established non-phthalate chemistry platforms. The European Union REACH authorisation list and restriction entries for di-2-ethylhexyl phthalate, benzyl butyl phthalate, dibutyl phthalate, and diisobutyl phthalate have created definitive regulatory sunset dates that force compounders in scope to complete non-phthalate transitions regardless of cost premium, establishing a non-negotiable demand driver for compliant alternative plasticizer supply. The United States Consumer Product Safety Improvement Act permanent prohibition on certain ortho-phthalates in children’s products and child care articles has been supplemented by the Environmental Protection Agency’s assessment activities under the Toxic Substances Control Act that may expand phthalate restriction into additional product categories, creating ongoing regulatory uncertainty that incentivizes proactive non-phthalate adoption by consumer product manufacturers seeking to future-proof their formulations against incremental regulatory expansion through the forecast period.

Automotive Lightweighting and Electric Vehicle Interior Component Growth Expanding High-Performance Plasticizer Demand in Transportation Applications

The automotive industry’s sustained transition toward lighter vehicle designs, advanced driver assistance system-integrated interiors, and the expanding proportion of electric vehicle platforms in global new vehicle production is generating incremental and technically differentiated demand for high-performance plasticizer systems capable of meeting the elevated heat resistance, low fogging, low volatile organic compound emission, and UV stability specifications that characterize premium automotive interior flexible PVC applications in instrument panels, door panels, seating surfaces, and center console coverings. Automotive OEM specifications for plasticizer systems in interior flexible PVC applications have become progressively more demanding, with fogging performance requirements below 1 milligram condensate per DIN 75201 method and heat aging retention targets at temperatures up to 120 degrees Celsius effectively restricting compliant plasticizer selection to trimellitate esters, polymeric plasticizers, and selected non-phthalate monomeric systems capable of delivering the permanence performance required by OEM-specified service life requirements. Electric vehicle platforms intensify automotive plasticizer value content through the increased use of flexible PVC in high-voltage battery cable insulation, charging connector flexible components, and battery management system wiring harnesses, where specialty plasticizer systems providing flexibility at temperatures down to minus 40 degrees Celsius and compatibility with high-temperature continuous service ratings are required, creating a technically demanding and growing demand stream for specialty plasticizer manufacturers with automotive qualification programs and application engineering capabilities.

Key Challenges

Regulatory Pressure on Phthalate Plasticizers and the Cost and Complexity of Reformulation Across Large Installed Flexible PVC Compound Portfolios

The progressive restriction of ortho-phthalate plasticizers across multiple regulatory jurisdictions imposes substantial reformulation, retesting, and re-qualification costs on flexible PVC compounders and end-product manufacturers whose compound libraries contain dozens or hundreds of formulations historically reliant on diisononyl phthalate, diisodecyl phthalate, and other phthalate grades that must be converted to non-phthalate alternatives within regulatory timelines that may not fully reflect the practical complexity of large-scale compound portfolio reformulation programs. Non-phthalate alternative plasticizers typically command price premiums ranging from 15% to 40% above equivalent phthalate grades on a cost-per-unit-flexibility-contribution basis, imposing a structural cost increase on flexible PVC formulations that compounds in parallel with the development and testing investment required to validate the performance equivalence of reformulated compounds across the full range of end-use specifications, regulatory compliance tests, and customer approval requirements applicable to each affected product line. The performance trade-offs associated with certain non-phthalate alternatives relative to incumbent phthalate grades in parameters including low-temperature flexibility, fusion characteristics, and electrical resistivity require additional formulation optimization investment and may necessitate recipe adjustments beyond simple plasticizer substitution, particularly in demanding technical applications where compound performance margins against specification limits are narrow and where qualification testing is costly and time-consuming.

Raw Material Feedstock Volatility and Supply Concentration in Oxo-Alcohol and Phthalic Anhydride Production Constraining Plasticizer Cost Stability

Plasticizer manufacturing costs are fundamentally governed by the price and availability of oxo-alcohol feedstocks, principally 2-ethylhexanol, isononanol, and isodecanol, whose production is concentrated in a relatively small number of globally operating propylene-based oxo synthesis facilities whose output and pricing are subject to propylene feedstock cost cycles, planned and unplanned maintenance shutdowns, and regional supply-demand imbalances that can generate rapid and severe plasticizer production cost escalation with limited short-term substitution options available to plasticizer manufacturers operating within fixed or semi-fixed customer supply agreements. The 2-ethylhexanol market, which supplies the dominant feedstock for di-2-ethylhexyl phthalate and dioctyl terephthalate production, is served by a globally concentrated producer base in which a small number of large integrated petrochemical manufacturers account for the majority of global capacity, creating systemic supply vulnerability to single-facility outages whose effects propagate rapidly through the plasticizer value chain to flexible PVC compounders and end-use manufacturers. Phthalic anhydride, the second key raw material for phthalate plasticizer synthesis, is itself subject to orthoxylene feedstock price volatility and capacity concentration dynamics that introduce a second independent source of cost volatility into the phthalate plasticizer manufacturing cost structure, while the terephthalic acid raw material for dioctyl terephthalate production is exposed to purified terephthalic acid market dynamics governed by paraxylene feedstock pricing and global PET production cycle demand fluctuations.

Bio-Based Plasticizer Performance Limitations and the High Cost of Achieving Technical Equivalence with Petroleum-Derived Plasticizer Systems

Despite the commercial momentum generated by sustainability mandates and regulatory incentives for bio-based plasticizer adoption, the majority of bio-derived plasticizer platforms available in commercial supply continue to exhibit performance limitations in one or more technically critical parameters that restrict their applicability in demanding flexible PVC segments and require formulation compromises that offset a portion of their sustainability and regulatory compliance benefits. Citrate ester plasticizers, the most commercially developed bio-based platform in sensitive applications, exhibit higher water extractability and lower permanence relative to non-phthalate petroleum-derived alternatives in applications involving sustained aqueous contact, elevated temperature service, or long-term outdoor exposure, limiting their use to less demanding flexible PVC applications or requiring higher loading levels that reduce compound economics relative to petroleum-based alternatives. Epoxidized vegetable oil plasticizers, while cost-competitive and widely used as secondary plasticizers and stabilizer co-agents, lack the primary plasticizer efficiency of dedicated monomeric plasticizer grades and generate compound properties including reduced low-temperature flexibility and altered rheology that require compensating formulation modifications. The development of bio-based primary plasticizer platforms with full technical equivalence to established non-phthalate petroleum-derived grades requires sustained research investment, process scale-up capital, and customer qualification programs whose cumulative cost and timeline present commercial barriers to new entrants and constrain the pace at which bio-based plasticizer systems can displace established petroleum-derived alternatives across technically demanding flexible PVC market segments.

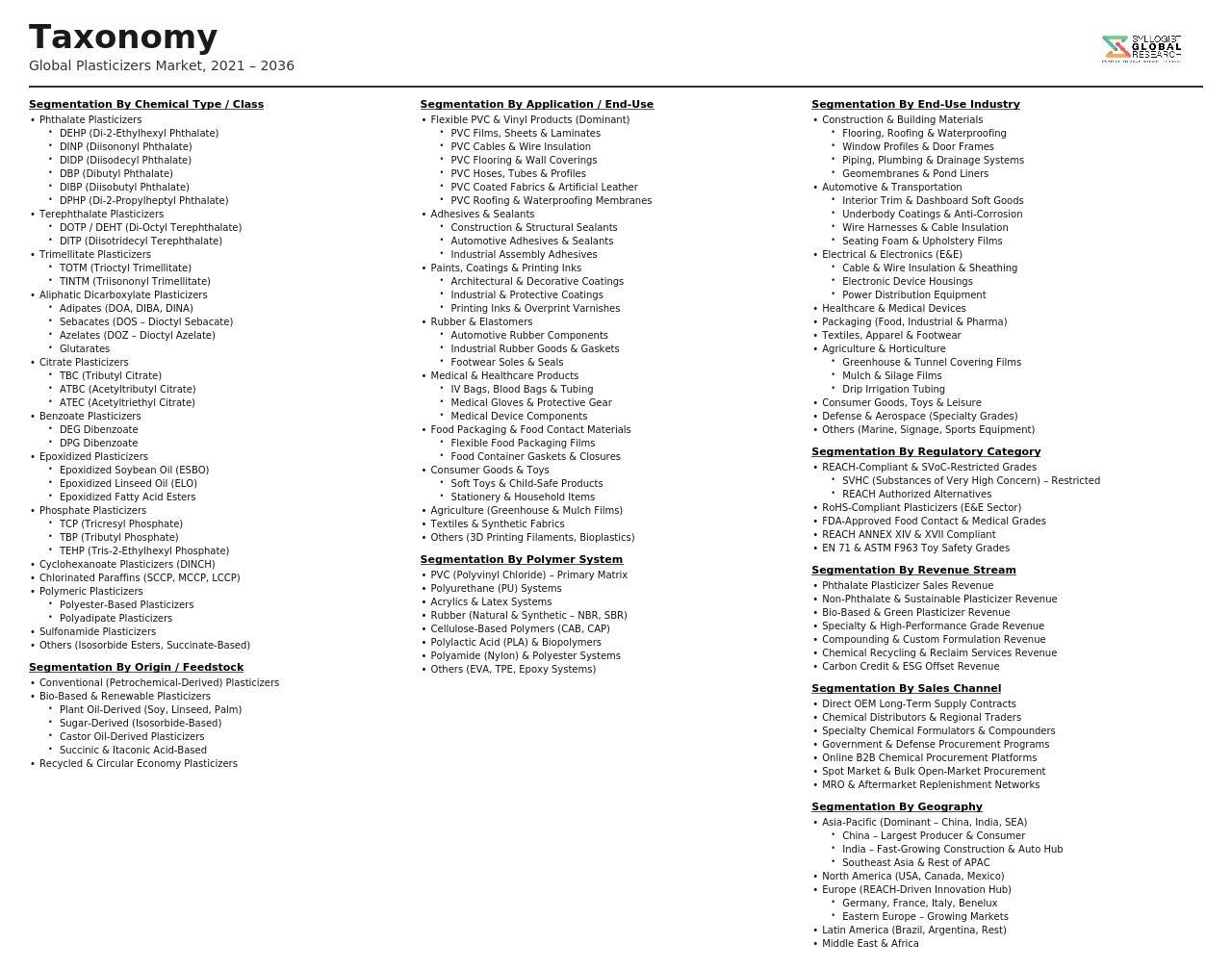

Market Segmentation

- Segmentation By Chemical Type

- Phthalate Plasticizers (DINP, DIDP, DPHP, and Others)

- Terephthalate Plasticizers (DOTP)

- Trimellitate Plasticizers (TOTM and TINTM)

- Adipate and Sebacate Ester Plasticizers

- Citrate Ester Plasticizers (ATBC and TBC)

- Epoxidized Vegetable Oil Plasticizers (ESBO and ELO)

- Cyclohexanoate Plasticizers (DINCH)

- Polymeric Plasticizers

- Phosphate Ester Plasticizers

- Isosorbide and Succinate-Based Bio-Based Plasticizers

- Others

- Segmentation By Plasticizer Origin

- Petroleum-Derived Plasticizers

- Bio-Based and Renewable Plasticizers

- Hybrid (Partially Bio-Based) Plasticizers

- Segmentation By Polymer Application

- Polyvinyl Chloride (PVC)

- Polyvinyl Butyral (PVB)

- Cellulose Esters

- Polyurethane

- Polylactic Acid (PLA) and Biopolymers

- Nitrile Rubber and Synthetic Elastomers

- Others

- Segmentation By End-Use Industry

- Construction and Infrastructure (Flooring, Roofing, and Wall Coverings)

- Electrical and Electronics (Cable and Wire Insulation)

- Automotive and Transportation

- Medical Devices and Healthcare (Tubing, Bags, and Devices)

- Packaging (Films, Sheets, and Coatings)

- Consumer Goods (Footwear, Toys, and Apparel)

- Agriculture (Mulch Films and Irrigation Systems)

- Coated Fabrics and Synthetic Leather

- Others

- Segmentation By Application Type

- Flexible PVC Compounds and Dry Blends

- Plastisols and Organosols

- PVC Films and Sheets

- Coatings and Surface Treatments

- Sealants and Adhesives

- Others

- Segmentation By Functionality

- Primary Plasticizers

- Secondary Plasticizers and Extenders

- Polymeric and Permanent Plasticizers

- Specialty and Functional Plasticizers

- Segmentation By Sales Channel

- Direct Supply to PVC Compounders and Processors

- Specialty Chemical Distributors

- Polymer and Additive Masterbatch Suppliers

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Plasticizers Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by chemical type, phthalate, non-phthalate, and bio-based, and by end-use industry, construction, automotive, electrical, medical, and packaging, to enable plasticizer manufacturers, flexible PVC compounders, polymer producers, and investors to identify which chemistry platforms and application segments will generate the highest absolute revenue and most durable growth trajectory across the forecast period in the context of the accelerating regulatory-driven transition away from ortho-phthalate systems and the concurrent expansion of non-phthalate and bio-based alternative supply?

- How are the regulatory frameworks governing ortho-phthalate restriction across the European Union REACH authorisation and restriction processes, the United States Consumer Product Safety Improvement Act and Toxic Substances Control Act review programs, and equivalent regulatory actions in Canada, Japan, South Korea, and China expected to evolve through 2034, and what are the projected compliance-driven reformulation timelines, non-phthalate adoption volume trajectories, and incremental cost impacts on flexible PVC compound portfolios across construction, medical, automotive, and consumer product end-use segments in each major regulatory jurisdiction?

- What is the projected market size, compound annual growth rate, and competitive structure of the bio-based plasticizers segment through 2034, encompassing citrate esters, epoxidized vegetable oils, succinates, and isosorbide-based platforms, which performance parameters represent the most commercially significant technical barriers to broader bio-based plasticizer adoption in demanding flexible PVC applications, and which feedstock platforms and chemistry development programs are most likely to achieve the technical equivalence and cost parity thresholds required to capture material share from petroleum-derived non-phthalate alternatives across premium flexible PVC market segments?

- How are construction sector investment cycles, residential and commercial building activity trends, electrical grid modernization and renewable energy infrastructure expansion programs, and automotive flexible interior and cable application growth expected to collectively shape regional plasticizer volume demand trajectories across Asia-Pacific, Europe, North America, the Middle East and Africa, and Latin America through 2034, and what are the regional production capacity adequacy, import-export trade flow, and local supplier competitive positioning implications of the projected demand distribution across these geographies?

- Who are the leading plasticizer manufacturers, non-phthalate specialty chemical developers, and bio-based plasticizer producers currently defining the competitive landscape of the global plasticizers market, and what are their respective product portfolios across phthalate, non-phthalate, and bio-based chemistries, manufacturing footprint and oxo-alcohol feedstock integration strategies, customer qualification status in automotive and medical end-use segments, technology development investment in next-generation sustainable plasticizer platforms, and strategic positioning responses to the regulatory, sustainability, and raw material volatility challenges reshaping global plasticizer market competitive dynamics through 2034?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Petrochemical Feedstock Price Volatility, Supply Disruption & Crude Oil Dependency Risk

- Phthalate Phase-Out, SVHC Listing & Hazardous Substance Regulatory Risk

- Substitution Risk from Bio-Based, Non-Phthalate & Alternative Plasticizer Chemistries

- PVC End-Market Demand Cyclicality: Construction, Automotive & Wire and Cable Sensitivity Risk

- Counterfeit and Off-Specification Product Risk in Emerging Market Supply Chains

- Regulatory Framework & Standards

- REACH SVHC Authorisation, Restriction & Phthalate Sunset Date Frameworks in the European Union

- US EPA TSCA Risk Evaluation, CPSC Phthalate Restrictions & State-Level Regulations (California Prop 65)

- Food Contact, Toy Safety & Medical Device Plasticizer Regulations (EU 10/2011, EN 71, ISO 10993)

- RoHS, ELV & WEEE Directive Implications for Plasticizers in Automotive and Electrical Applications

- China GB Standards, APAC National Regulations & Emerging Market Plasticizer Compliance Frameworks

- Global Plasticizers Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Kilotons)

- Market Size & Forecast by Product Type

- Phthalate Plasticizers

- Non-Phthalate Plasticizers

- Bio-Based Plasticizers

- Polymeric Plasticizers

- Other Specialty Plasticizers

- Market Size & Forecast by Chemical Type

- Diisononyl Phthalate (DINP)

- Diisodecyl Phthalate (DIDP)

- Di(2-ethylhexyl) Phthalate (DEHP)

- Dioctyl Terephthalate (DOTP / DEHT)

- Diisononyl Cyclohexane-1,2-Dicarboxylate (DINCH)

- Adipate Plasticizers (DOA, DIDA and DINA)

- Trimellitate Plasticizers (TOTM and TINTM)

- Citrate Plasticizers (TBC, ATBC and TEC)

- Epoxidised Soybean Oil (ESBO) and Epoxidised Linseed Oil (ELO)

- Benzoate Plasticizers

- Phosphate Plasticizers (TCP, TXP and Others)

- Other Chemical Types

- Market Size & Forecast by Polymer

- Polyvinyl Chloride (PVC) and Vinyl Polymers

- Polyurethane (PU)

- Cellulose-Based Polymers

- Rubber and Elastomers

- Bioplastics (PLA, PHA and Starch Blends)

- Other Polymers

- Market Size & Forecast by End-Use Industry

- Construction (Flooring, Roofing, Window Profiles, Wall Coverings and Geomembranes)

- Wire and Cable (Power Cables, Data Cables and Automotive Wiring Harnesses)

- Automotive and Transportation (Interior Trim, Underbody Coatings and Seals)

- Packaging (Films, Wraps, Containers and Medical Packaging)

- Medical and Healthcare (IV Bags, Blood Tubing, Gloves and Medical Devices)

- Consumer Goods (Toys, Footwear, Apparel and Household Products)

- Coatings, Inks and Adhesives

- Agriculture (Mulch Films, Greenhouse Covers and Irrigation Tubing)

- Electronics and Electrical Equipment

- Other End-Use Industries

- Market Size & Forecast by Application

- Flexible PVC Compounds and Compounds for Extrusion

- Plastisols and Organosols

- Calendered Films and Sheets

- Coated Fabrics and Artificial Leather

- Moulded and Extruded Parts

- Specialty Functional Applications (Flame Retardant, Low Temperature and High Performance)

- Market Size & Forecast by Sales Channel

- Direct Sales to Compounders and PVC Processors

- Specialty Chemical Distributors and Trading Houses

- OEM and Long-Term Supply Agreement Channels

- E-Commerce and Spot Market Channels

- North America Plasticizers Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotons)

- By Product Type

- By Chemical Type

- By Polymer

- By End-Use Industry

- By Application

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Plasticizers Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotons)

- By Product Type

- By Chemical Type

- By Polymer

- By End-Use Industry

- By Application

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Plasticizers Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotons)

- By Product Type

- By Chemical Type

- By Polymer

- By End-Use Industry

- By Application

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Plasticizers Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotons)

- By Product Type

- By Chemical Type

- By Polymer

- By End-Use Industry

- By Application

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Plasticizers Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotons)

- By Product Type

- By Chemical Type

- By Polymer

- By End-Use Industry

- By Application

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Plasticizers Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotons)

- By Product Type

- By Chemical Type

- By Polymer

- By End-Use Industry

- By Application

- By Country

- By Sales Channel

- Market Size & Forecast

- *Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Italy, Spain, Poland, China, Japan, India, South Korea, Taiwan, Indonesia, Thailand, Brazil, Argentina, Saudi Arabia, UAE, South Africa, Turkey, Egypt

- Technology Landscape & Innovation Analysis

- Non-Phthalate Plasticizer Chemistry: DOTP, DINCH and Next-Generation Alternatives Technology Deep-Dive

- Bio-Based Plasticizer Technology: Epoxidised Vegetable Oils, Citrates and Isosorbide Derivatives

- Polymeric and High Molecular Weight Plasticizer Technology for Low Migration Applications

- Reactive Plasticizer Technology for Permanent Bonding and Migration Resistance

- Flame-Retardant Plasticizer Technology (Phosphate and Halogenated Esters)

- Plasticizer Blending and Synergistic Formulation Technology for Performance Optimisation

- Digital Formulation Assistance and AI-Based Plasticizer Selection Platforms

- Patent & IP Landscape in Plasticizer Technologies

- Value Chain & Supply Chain Analysis

- Petrochemical Feedstock Supply Chain (Oxo-Alcohols, Phthalic Anhydride and 2-EH)

- Bio-Based and Renewable Feedstock Supply Chain (Vegetable Oils, Citric Acid and Isosorbide)

- Plasticizer Synthesis, Esterification and Purification Manufacturing

- Quality Control, Specification Testing and Regulatory Documentation

- Bulk Logistics, Storage and Handling Infrastructure for Liquid Plasticizers

- Distribution to PVC Compounders, Processors and End-Use Industries

- Waste Plasticizer Recovery, Recycling and Circular Economy Initiatives

- Pricing Analysis

- Feedstock Cost Passthrough: Oxo-Alcohol and Phthalic Anhydride Price Linkage to Plasticizer Pricing

- Phthalate Plasticizer (DINP, DIDP and DEHP) Spot and Contract Price Trends

- Non-Phthalate Plasticizer (DOTP and DINCH) Price Premium Analysis vs. Conventional Phthalates

- Bio-Based Plasticizer Pricing and Cost Competitiveness vs. Petrochemical Alternatives

- Regional Price Differentials and Import Parity Analysis

- Pricing Dynamics, Contract Structures and Volume Discount Frameworks

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Plasticizers: Carbon Footprint, Energy Intensity and End-of-Life Implications Across Chemical Types

- Endocrine Disruption, Human Health & Ecotoxicity Concerns: The Science Behind Phthalate Regulation and Phase-Out

- Bio-Based Plasticizer Adoption: Renewable Carbon Content, Carbon Sequestration Benefits and Commercial Readiness

- Migration, Leaching and Microplastic Contamination: Environmental Fate of Plasticizers in Soil, Water and Air

- Regulatory-Driven Sustainability, REACH SVHC, SDG Alignment and ESG Disclosure in Plasticizer Supply Chains

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Chemical Type and Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Chemical Type, End-Use Industry and Geography

- Player Classification

- Integrated Petrochemical and Specialty Chemical Plasticizer Producers

- Dedicated Non-Phthalate and DINCH/DOTP Plasticizer Manufacturers

- Bio-Based and Renewable Plasticizer Specialists

- Polymeric and High-Performance Plasticizer Producers

- Regional and Emerging Market Plasticizer Manufacturers

- Competitive Analysis Frameworks

- Market Share Analysis by Chemical Type, End-Use Industry and Region

- Company Profile

- Company Overview & Headquarters

- Plasticizer Product Portfolio and Chemical Technology Platforms

- Key Customer Relationships & Reference Accounts

- Manufacturing Footprint & Production Capacity

- Revenue (Plasticizers Segment) and R&D Spend

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Product Launches, Capacity Expansions and Regulatory Approvals)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Breadth vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Strategic Outlook & Opportunity Analysis

- Strategic Output

- Market Opportunity Matrix: By Chemical Type, Polymer, End-Use Industry, Application and Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output