Market Definition

The India Ready-Mix Concrete Market encompasses the industrial production, batching, transportation, placement, and quality assurance of factory-manufactured concrete delivered in a freshly mixed and unhardened state to construction sites across residential, commercial, industrial, and infrastructure end-use segments throughout the country. Ready-mix concrete is produced at centralized automated batching plants where cement, coarse and fine aggregates, water, chemical admixtures, and supplementary cementitious materials including fly ash, ground granulated blast furnace slag, silica fume, and metakaolin are proportioned and mixed under controlled conditions to achieve specified fresh and hardened concrete properties, and transported to site in transit mixer trucks that maintain mix homogeneity during delivery within defined time and distance parameters. The market encompasses the complete value chain from raw material procurement of cement, aggregates, chemical admixtures, and supplementary cementitious materials through batching plant operations, logistics and transit mixing, site delivery and placement services, and quality control and technical support functions. Product offerings span standard-grade concretes in compressive strength classes from M10 to M100, self-compacting concrete, high-performance concrete, waterproof concrete, lightweight concrete, coloured and architectural concrete, fibre-reinforced concrete, shotcrete, and specialty concrete systems for marine, industrial flooring, precast, and infrastructure applications. Key participants include large national ready-mix concrete producers operating multi-city plant networks, cement manufacturer-affiliated concrete divisions, regional and city-level independent operators, real estate and infrastructure developers who captively consume significant volumes, admixture and supplementary cementitious material suppliers, transit mixer fleet operators, and the construction contractors and project management consultants whose specifications and procurement decisions govern concrete grade selection, quality requirements, and supplier qualification across India’s rapidly expanding built environment.

Market Insights

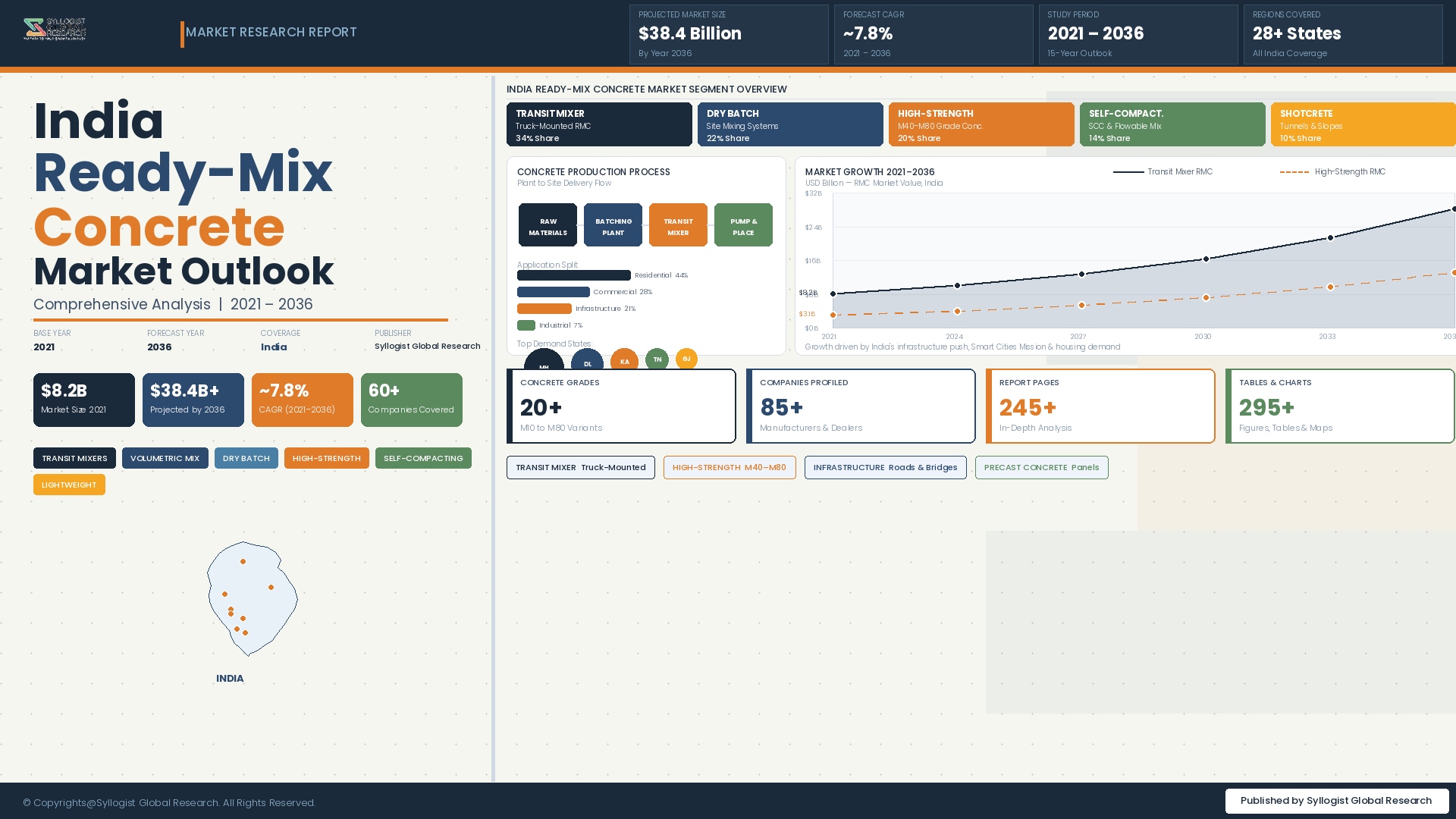

The India ready-mix concrete market was valued at approximately USD 9.6 billion in 2025 and is projected to reach USD 19.8 billion by 2034, advancing at a compound annual growth rate of 8.3% over the forecast period from 2027 to 2034, making it one of the fastest-growing national ready-mix concrete markets globally. This growth trajectory is anchored in India’s government-driven infrastructure investment supercycle, the structural expansion of organised residential construction, and the progressive shift in concrete procurement behaviour among mid-sized and large construction contractors away from site-mixed concrete toward ready-mix concrete as urbanisation, labour cost escalation, and project quality requirements collectively strengthen the economic and technical case for centralised batching plant supply. Total cement consumption in India reached approximately 420 million metric tons in 2025, of which ready-mix concrete accounted for an estimated 8.5% share by cement volume equivalent, compared to ready-mix concrete penetration rates of 70% to 80% in mature markets such as the United States and Western Europe, underscoring the very substantial headroom for further ready-mix concrete adoption across India’s construction industry over the forecast period.

Infrastructure construction represents the single most significant demand driver for ready-mix concrete in India, with government capital expenditure on roads, highways, expressways, metro rail systems, airports, ports, urban mass transit, bridges, and water infrastructure collectively generating demand for high-volume concrete supplies at construction sites where the scale, pace, and quality consistency requirements of modern infrastructure projects are most effectively served by ready-mix concrete procurement from professionally operated batching plant networks. The Pradhan Mantri Gati Shakti National Master Plan, the National Infrastructure Pipeline with its projected investment of approximately USD 1.4 trillion across the period to 2030, and the sustained expansion of metro rail networks in cities including Delhi, Mumbai, Bangalore, Chennai, Hyderabad, Pune, and Ahmedabad are generating concentrated demand for high-performance concrete in tunnelling, elevated viaduct, underground station, and bridge deck applications where self-compacting concrete, high early strength mixes, and mass concrete thermal management specifications require the technical capability and process control infrastructure of ready-mix concrete producers rather than site mixing operations. The rural and semi-urban infrastructure expansion programs including Pradhan Mantri Gram Sadak Yojana road connectivity and Jal Jeevan Mission water supply infrastructure are additionally extending ready-mix concrete demand into tier-three and tier-four cities and peri-urban areas where batching plant penetration has historically been limited.

The organised residential real estate segment is the second-largest and fastest-growing demand category for ready-mix concrete in India, driven by the structural expansion of mid-income and affordable housing construction in metropolitan and tier-one city markets where large-format residential tower projects routinely specify ready-mix concrete for structural frames, slabs, columns, and shear walls to achieve the construction pace, structural performance, and quality consistency required by homebuyer expectations and regulatory compliance obligations. The adoption of modern construction methods including aluminium formwork systems, slip forming, jump forming, and precast concrete elements is reinforcing the preference for ready-mix concrete among residential developers, as these construction technologies require concrete with tightly controlled workability, setting time, and strength development profiles that are most reliably achieved through ready-mix batching plant supply rather than site mixing. Commercial real estate construction encompassing Grade A office developments, data centres, logistics warehouses, retail malls, and hospitality properties is generating incremental high-specification concrete demand in major urban centres, with data centre construction in particular emerging as a high-growth, high-specification concrete application requiring demanding concrete mix designs for thick mat foundations, high-load floor slabs, and EMI-shielding concrete wall systems.

The ready-mix concrete industry in India is characterised by significant geographical concentration, with the top seven metropolitan areas comprising Mumbai, Delhi-NCR, Bangalore, Chennai, Hyderabad, Pune, and Ahmedabad accounting for approximately 62% of total national ready-mix concrete consumption in 2025, reflecting the concentration of large-scale organised construction activity, infrastructure investment, and commercial real estate development in these urban centres where plant economics, aggregate supply logistics, and transit mixer delivery radius constraints make centralised batching most commercially viable. The competitive landscape is evolving rapidly, with cement manufacturers increasingly integrating forward into ready-mix concrete production as a margin enhancement and cement demand pull-through strategy, while national ready-mix concrete operators are investing in automated plant upgrades, admixture innovation, and technical service capabilities to differentiate on quality and service consistency rather than price alone. Sustainability is emerging as a structurally important market dimension, with leading developers and infrastructure project owners beginning to specify concrete mix designs incorporating higher proportions of supplementary cementitious materials including fly ash and ground granulated blast furnace slag to reduce the embodied carbon content of structural concrete, creating commercial opportunities for technically capable ready-mix producers who can deliver lower-carbon concrete mix designs that meet structural performance specifications while satisfying developer environmental, social, and governance reporting requirements.

Key Drivers

Government Infrastructure Investment Supercycle and National Capital Expenditure Programs Generating Structural High-Volume Ready-Mix Concrete Demand

The Indian government’s commitment to infrastructure-led economic development, expressed through successive increases in the Union Budget capital expenditure allocation that reached approximately INR 11.1 trillion in the 2024-25 fiscal year and the comprehensive project pipeline of the National Infrastructure Pipeline, is generating a multi-year, broad-based demand stimulus for ready-mix concrete across road and highway construction, metro rail system development, airport modernisation, port capacity expansion, river linking and water supply infrastructure, and urban development projects that collectively constitute the largest infrastructure investment program in India’s post-independence history. National highway construction under the National Highways Authority of India program has been progressing at approximately 10,000 to 12,000 kilometres of new highway construction annually in recent years, with rigid pavement concrete roads, flyovers, tunnels, bridges, and culvert structures generating sustained high-volume cement-intensive concrete demand along highway corridors across all regions of the country. The metro rail expansion program, with systems under construction or planned in more than 27 Indian cities as of 2025, represents a particularly high-value ready-mix concrete demand segment due to the large volumes of high-specification underwater concrete, tunnel lining concrete, high early strength concrete for precast segments, and self-compacting concrete for complex reinforced structural elements that metro construction requires, with each new metro line generating estimated ready-mix concrete consumption of 1.5 million to 3 million cubic metres depending on route length and proportion of underground alignment.

Rapid Urbanisation and Organised Real Estate Sector Growth Accelerating Ready-Mix Concrete Adoption in Residential and Commercial Construction

India’s urbanisation trajectory, with the urban population projected to expand from approximately 520 million in 2025 to over 600 million by 2034, is generating structural and durable demand for residential, commercial, and civic construction that underpins the long-term growth foundation of the ready-mix concrete market independent of specific government program cycles. The formalisation of the Indian real estate sector following the implementation of the Real Estate Regulation and Development Act and the Goods and Services Tax has accelerated the shift in residential construction from fragmented self-construction toward organised developer-led projects, where project scale, construction pace requirements, financial accountability, and homebuyer quality expectations consistently favour ready-mix concrete procurement over traditional site-mixed concrete as the primary concrete supply method. Large residential township projects by listed and institutional developers in cities including Mumbai Metropolitan Region, Pune, Bangalore, and Delhi-NCR regularly specify ready-mix concrete across entire project phases, generating committed long-term volume offtake that supports the capital investment case for new batching plant capacity deployment in these markets. The growth of data centre construction, logistics park development, and cold chain infrastructure in peri-urban locations around major cities is additionally extending high-specification ready-mix concrete demand into locations previously served only by site-mixed concrete, pulling batching plant network expansion beyond the immediate urban core in the most developed metropolitan markets.

Quality Imperative, Labour Cost Escalation, and Construction Speed Requirements Strengthening the Economic Case for Ready-Mix Concrete Over Site-Mixed Alternatives

The structural shift in the economic and technical calculus governing concrete procurement decisions at Indian construction sites is accelerating the conversion of volume from site-mixed concrete toward ready-mix concrete, driven by the convergence of rising skilled construction labour costs, increasingly stringent structural concrete quality requirements in building codes and developer specifications, contractor liability for structural performance, and the adoption of construction methods whose pace and quality consistency requirements cannot be reliably met by site mixing operations. Construction labour costs in metropolitan India have increased by approximately 8% to 12% annually in the three years preceding 2025, compressing the historical site-mixing labour cost advantage over ready-mix concrete supply and shifting the all-in cost comparison in favour of ready-mix concrete in an expanding set of project types and locations. Bureau of Indian Standards IS 456 and IS 10262 concrete mix design requirements, combined with increasing enforcement of third-party quality audits on large residential and commercial projects, are raising the practical threshold of mixing process control and mix design documentation that site mixing operations must achieve to satisfy project quality management systems, further favouring ready-mix concrete procurement. The growing adoption of faster construction cycle technologies including aluminium formwork, climbing formwork, and mechanised placement equipment by large developers and infrastructure contractors simultaneously increases the pace at which concrete must be delivered and placed, creating logistical requirements that favour the transit mixer delivery model of ready-mix concrete over the batch-and-mix approach of site production.

Key Challenges

Aggregate Supply Chain Constraints, Sand Availability Disruption, and Raw Material Logistics Cost Escalation Compressing Ready-Mix Concrete Margins

The ready-mix concrete industry in India faces persistent and structurally challenging raw material supply constraints, particularly in river sand procurement, where the regulatory framework governing sand mining from riverbeds has become increasingly restrictive across multiple states in response to environmental concerns about riverbed ecology, groundwater recharge, and river morphology, creating acute sand shortages and price volatility in major construction markets including Maharashtra, Karnataka, Tamil Nadu, and the Delhi-NCR region whose ready-mix concrete industries collectively account for a substantial proportion of national consumption. Sand price escalation and supply disruption force ready-mix concrete producers to substitute river sand with manufactured sand produced from crushed rock quarries and alternative aggregates including recycled concrete aggregate and bottom ash, requiring admixture system reformulation, quality management system adaptation, and customer technical communication programs that impose operational and management costs beyond the direct material substitution expense. Coarse aggregate supply chain logistics represent a second significant raw material cost challenge, as the geographic concentration of suitable hard rock quarry resources at distances of 30 to 150 kilometres from major urban construction markets generates transportation cost burdens that are sensitive to diesel price movements and road freight tariff escalation, with aggregate freight costs constituting 25% to 35% of delivered aggregate cost in the most supply-constrained metropolitan markets and limiting the competitive economics of ready-mix concrete relative to on-site mixing in locations beyond the economic delivery radius of established quarry and plant supply networks.

Fragmented and Price-Driven Market Competition from Unorganised Site-Mixed Concrete and the Challenge of Demonstrating Total Value Proposition to Cost-Sensitive Customers

The ready-mix concrete market in India continues to face intense competitive pressure from the entrenched practice of site-mixed concrete production, which accounts for an estimated 91.5% of total concrete consumption by volume in 2025 and is sustained by the price sensitivity of a large proportion of construction activity, particularly in the residential self-construction, small-scale commercial, and rural infrastructure segments where the apparent direct material cost of site mixing compares favourably to ready-mix concrete pricing when buyers do not fully account for the indirect costs of site batching including labour supervision, equipment capital, waste, rework, quality failure, and construction schedule delay attributable to concrete quality inconsistency. Ready-mix concrete producers face a persistent market communication challenge in quantifying and conveying the total value proposition of ready-mix concrete procurement to construction clients whose procurement decisions are dominated by direct material price comparisons rather than lifecycle cost or structural performance risk assessments, particularly in tier-two and tier-three cities where technical awareness of ready-mix concrete quality and process advantages is lower than in the metropolitan markets where long-term customer relationships and repeat project procurement have established quality and service track records. The prevalence of small and informal concrete batching operations using portable mixers and manual batching in peri-urban and semi-urban markets creates a price floor that professional ready-mix concrete producers with higher fixed cost structures cannot match on direct price alone, requiring differentiated sales and marketing approaches that emphasise quality certification, structural warranty provision, and project management risk reduction to justify pricing premiums.

Transit Mixer Fleet Logistics, Urban Traffic Congestion, and Batching Plant Location Constraints Limiting Delivery Efficiency and Market Coverage

The operational model of ready-mix concrete production and delivery is fundamentally constrained by the time-sensitive nature of fresh concrete logistics, with maximum transport time between batching plant and site placement typically limited to 90 minutes under normal conditions and reduced further under high ambient temperature conditions prevalent across much of India for six to eight months annually, creating hard geographic coverage limitations for individual batching plant locations and requiring capital-intensive multi-plant network investment to achieve commercially viable coverage of large metropolitan construction markets. Urban traffic congestion in major Indian cities including Mumbai, Delhi, Bangalore, Chennai, and Hyderabad has become a severe operational constraint for transit mixer fleet efficiency, with average delivery cycle times in heavily congested urban zones extending to four to six hours per trip compared to an optimal two to three hour cycle, reducing the effective daily output capacity of transit mixer fleets, increasing fuel and driver costs per cubic metre delivered, and creating concrete setting time risk for deliveries that encounter unanticipated traffic delays beyond the hydration-controlled workability retention window of the fresh concrete mix. Batching plant location acquisition and permitting in urban areas has become progressively more difficult as urban land values escalate, industrial zoning becomes more restrictive, and community concerns about truck traffic, dust, and noise generated by batching plant operations intensify regulatory scrutiny of new plant establishment approvals, limiting the ability of ready-mix concrete operators to site batching plants within optimal delivery radius proximity to major construction demand centres and compelling operators to absorb longer average haul distances with attendant cost and logistics complexity implications.

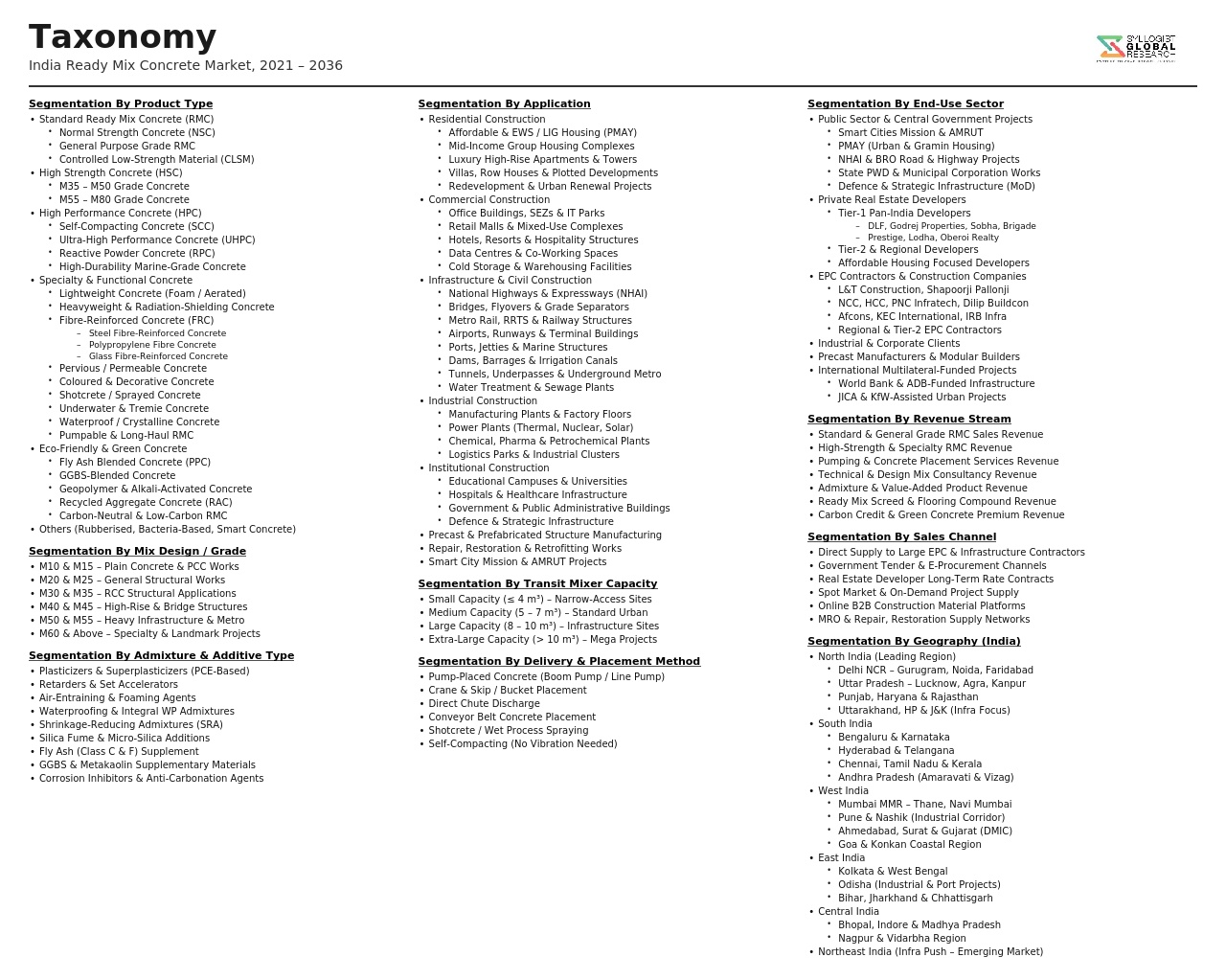

Market Segmentation

- Segmentation By Concrete Grade

- Standard Grade Concrete (M10 to M30)

- High-Strength Concrete (M35 to M55)

- Ultra High-Strength Concrete (M60 and Above)

- Self-Compacting Concrete (SCC)

- High-Performance Concrete (HPC)

- Waterproof and Crystalline Concrete

- Lightweight Concrete

- Fibre-Reinforced Concrete (Steel, Polypropylene, and Glass Fibre)

- Coloured and Architectural Concrete

- Others

- Segmentation By End-Use Sector

- Residential Construction (Affordable, Mid-Income, and Premium Housing)

- Commercial Real Estate (Offices, Retail, and Hospitality)

- Industrial Construction (Factories, Warehouses, and Data Centres)

- Road and Highway Infrastructure

- Metro Rail and Urban Mass Transit

- Bridges, Flyovers, and Elevated Structures

- Airport and Port Infrastructure

- Water Supply and Sewerage Infrastructure

- Others

- Segmentation By Application

- Structural Frames, Columns, and Slabs

- Foundations and Pile Caps

- Industrial Flooring and Ground Slabs

- Precast and Prefabricated Elements

- Tunnelling and Underground Structures

- Pavement and Rigid Road Construction

- Marine and Hydraulic Structures

- Others

- Segmentation By Supplementary Cementitious Material

- Ordinary Portland Cement-Based Concrete

- Fly Ash Blended Concrete

- Ground Granulated Blast Furnace Slag (GGBS) Concrete

- Silica Fume Concrete

- Metakaolin and Calcined Clay Blended Concrete

- Multi-Blend Low-Carbon Concrete

- Segmentation By Admixture Type

- Polycarboxylate Ether Superplasticiser-Based Concrete

- Retarder and Extended Workability Concrete

- Accelerator and High Early Strength Concrete

- Viscosity Modifying Agent Concrete

- Shrinkage-Reducing Admixture Concrete

- Others

- Segmentation By Batching Plant Type

- Stationary Central Mix Batching Plants

- Transit Mix (Truck Mix) Batching Plants

- Mobile and Semi-Mobile Batching Plants

- Volumetric Mobile Mixer Units

- Segmentation By Sales Channel

- Direct Supply to Infrastructure Project Contractors

- Real Estate Developer and EPC Contractor Procurement

- Retail and Small Contractor Supply

- Captive Plant Supply by Large Developers

- Others

- Segmentation By Region

- North India (Delhi-NCR, Uttar Pradesh, Rajasthan, and Punjab)

- West India (Maharashtra, Gujarat, and Goa)

- South India (Karnataka, Tamil Nadu, Telangana, and Kerala)

- East India (West Bengal, Odisha, and Bihar)

- Central India (Madhya Pradesh and Chhattisgarh)

- Northeast India

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total valuation of the India Ready-Mix Concrete Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by concrete grade, standard, high-performance, and specialty concrete, by end-use sector, residential, commercial, infrastructure, and industrial, and by region, to enable ready-mix concrete producers, cement manufacturers, admixture suppliers, construction developers, and investors to identify which product segments, application categories, and geographic markets will generate the highest absolute revenue and most durable volume growth trajectory across the forecast period?

- How is the Government of India’s National Infrastructure Pipeline investment program, including national highway construction, metro rail expansion, smart city development, and water infrastructure programs, expected to translate into ready-mix concrete volume demand by project type, geographic corridor, and concrete specification category through 2034, and which regional markets across Maharashtra, Karnataka, Tamil Nadu, Delhi-NCR, Gujarat, Telangana, and Uttar Pradesh are projected to generate the largest incremental ready-mix concrete demand from infrastructure construction activity relative to current installed batching plant capacity?

- What is the projected trajectory of ready-mix concrete market penetration as a proportion of total concrete consumption in India through 2034, which construction segment and city-tier combinations offer the highest near-term conversion opportunity from site-mixed to ready-mix concrete procurement, and what are the enabling factors including construction formalisation, labour cost escalation, quality regulation enforcement, and modern construction method adoption that are most likely to accelerate the penetration rate uplift in tier-two and tier-three city markets currently underserved by professional ready-mix concrete supply networks?

- How are aggregate supply chain constraints, manufactured sand adoption, supplementary cementitious material availability, and chemical admixture technology evolution expected to shape the raw material cost structure, concrete mix design capabilities, and sustainability performance of the Indian ready-mix concrete industry through 2034, and what are the implications for producer margins, customer concrete specification requirements, embodied carbon reduction commitments by real estate developers and infrastructure project owners, and competitive differentiation between technically advanced and commodity-positioned ready-mix concrete operators?

- Who are the leading ready-mix concrete producers, cement company-affiliated concrete divisions, and regional batching plant operators currently defining the competitive landscape of the India ready-mix concrete market, and what are their respective installed plant capacity and geographic coverage footprints, volume growth and greenfield expansion strategies across metropolitan and emerging tier-two markets, technical service and mix design differentiation capabilities, admixture and supplementary cementitious material partnership strategies, and competitive positioning responses to the market share, pricing, and sustainability challenges reshaping the India ready-mix concrete industry through 2034?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Raw Material Price Volatility: Cement, Aggregates, Admixture and Water Availability Risk

- Logistics, Transit Time and Slump Loss Risk in Large-City and High-Traffic Delivery Corridors

- Monsoon Seasonality, Construction Activity Disruption & Demand Cyclicality Risk

- Competition from Site-Mixed Concrete, Unorganised Sector & Self-Consumption Risk at Large Project Sites

- Regulatory Compliance, BIS Standards Enforcement & Quality Assurance Risk Across Tier-2 and Tier-3 Markets

- Regulatory Framework & Standards

- Bureau of Indian Standards (BIS) IS 4926: Code of Practice for Ready-Mixed Concrete and Mandatory BIS Certification Requirements

- IS 456: Plain and Reinforced Concrete Code of Practice and Its Implications for RMC Grade Specifications and Mix Design

- National Building Code (NBC) 2016 Requirements, CPWD and State PWD Specifications for RMC Use in Government Projects

- Environment Regulations: Consent to Establish and Operate (CTE/CTO) Under Environment Protection Act, Dust and Noise Norms for Batching Plants

- GST Framework for Ready-Mix Concrete, Input Tax Credit Structure & State-Level Construction Material Taxation

- India Ready-Mix Concrete Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Million Cubic Metres)

- Market Size & Forecast by Grade and Mix Type

- Standard Grade RMC (M10 to M25)

- High-Strength Grade RMC (M30 to M50)

- Very High-Strength and Ultra-High-Performance Concrete (Above M50)

- Self-Compacting Concrete (SCC)

- High-Performance Concrete (HPC)

- Lightweight Concrete

- Fibre-Reinforced Concrete (FRC)

- Shotcrete and Sprayed Concrete

- Pervious and Permeable Concrete

- Other Specialty Mix Types

- Market Size & Forecast by Application

- Residential Construction (Mass Housing, Affordable Housing and Premium Residential)

- Commercial Construction (Offices, Retail, Hospitality and Mixed-Use Developments)

- Infrastructure (Roads, Highways, Flyovers and Bridges)

- Metro Rail, Urban Transit and Railway Infrastructure

- Industrial Construction (Factories, Warehouses and Logistics Parks)

- Institutional Construction (Hospitals, Educational Institutions and Government Buildings)

- Energy Infrastructure (Power Plants, Dams and Renewable Energy Foundations)

- Ports, Airports and Marine Structures

- Market Size & Forecast by End-User

- Real Estate Developers (Private and Government)

- Infrastructure and EPC Contractors

- Government Agencies and Public Sector Undertakings (PSUs)

- Industrial and Institutional Project Owners

- Individual Home Builders (IHB) and Small Contractors

- Market Size & Forecast by Cement Type Used

- Ordinary Portland Cement (OPC)

- Portland Pozzolana Cement (PPC)

- Portland Slag Cement (PSC)

- Blended and Specialty Cements

- Market Size & Forecast by Admixture Type Used

- Plasticizers and Superplasticizers (PCE and Naphthalene-Based)

- Retarders and Set-Controlling Admixtures

- Accelerators and Early-Strength Admixtures

- Air-Entraining Admixtures

- Waterproofing and Permeability-Reducing Admixtures

- Specialty and Multi-Functional Admixtures

- Market Size & Forecast by Plant Type

- Stationary (Fixed) Batching Plants

- Mobile and Transit Batching Plants

- Volumetric and On-Site Mobile Mixers

- Market Size & Forecast by Sales Channel

- Direct Supply to Large Projects and EPC Contractors

- Supply through Dealer and Sub-Dealer Networks

- Government and Institutional Tender-Based Supply

- Captive RMC Plants of Large Real Estate and Infrastructure Groups

- North India Ready-Mix Concrete Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Cubic Metres)

- By Grade and Mix Type

- By Application

- By End-User

- By Cement Type Used

- By Admixture Type Used

- By Plant Type

- By State

- By Sales Channel

- Market Size & Forecast

- South India Ready-Mix Concrete Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Cubic Metres)

- By Grade and Mix Type

- By Application

- By End-User

- By Cement Type Used

- By Admixture Type Used

- By Plant Type

- By State

- By Sales Channel

- Market Size & Forecast

- West India Ready-Mix Concrete Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Cubic Metres)

- By Grade and Mix Type

- By Application

- By End-User

- By Cement Type Used

- By Admixture Type Used

- By Plant Type

- By State

- By Sales Channel

- Market Size & Forecast

- East India Ready-Mix Concrete Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Cubic Metres)

- By Grade and Mix Type

- By Application

- By End-User

- By Cement Type Used

- By Admixture Type Used

- By Plant Type

- By State

- By Sales Channel

- Market Size & Forecast

- Central India Ready-Mix Concrete Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Cubic Metres)

- By Grade and Mix Type

- By Application

- By End-User

- By Cement Type Used

- By Admixture Type Used

- By Plant Type

- By State

- By Sales Channel

- Market Size & Forecast

- State-Wise* Ready-Mix Concrete Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Cubic Metres)

- By Grade and Mix Type

- By Application

- By End-User

- By Cement Type Used

- By Admixture Type Used

- By Plant Type

- By State

- By Sales Channel

- Market Size & Forecast

- *States Analyzed in the Syllogist Global Research Portfolio: Maharashtra, Gujarat, Karnataka, Tamil Nadu, Telangana, Andhra Pradesh, Delhi NCR, Uttar Pradesh, Rajasthan, Haryana, Punjab, West Bengal, Odisha, Madhya Pradesh, Chhattisgarh, Kerala, Bihar, Jharkhand

- Technology Landscape & Innovation Analysis

- Advanced Batching Plant Automation, IoT-Enabled Weighing Systems and Real-Time Mix Control Technology Deep-Dive

- High-Performance and Self-Compacting Concrete Mix Design Technology for High-Rise and Infrastructure Applications

- Supplementary Cementitious Materials (SCMs): Fly Ash, GGBS and Silica Fume Integration in Indian RMC Formulations

- Polycarboxylate Ether (PCE) Superplasticizer Technology for Low Water-to-Cement Ratio and High-Durability Concrete

- Fibre-Reinforced Concrete Technology: Steel, Polypropylene and Macro-Synthetic Fibre Applications

- Telematics, GPS Tracking and Drum-Rotation Monitoring Technology for Transit Mixer Fleet Management

- Green Concrete Technology: Recycled Aggregate Concrete, Geopolymer Concrete and Low-Carbon Mix Design

- Patent & IP Landscape in Ready-Mix Concrete Technologies Relevant to the Indian Market

- Value Chain & Supply Chain Analysis

- Cement Procurement, Logistics and Storage Supply Chain for RMC Producers in India

- Coarse and Fine Aggregate (Crushed Stone, Sand and M-Sand) Sourcing and Supply Chain

- Chemical Admixture Procurement, Quality Control and Approved Supplier Management

- Supplementary Cementitious Material (Fly Ash, GGBS) Sourcing from Power Plants and Steel Mills

- Transit Mixer Fleet, Pump Deployment and Last-Mile Delivery Infrastructure

- Batching Plant Network Planning, Site Selection and Capacity Optimisation

- Washout Water Management, Return Concrete Reclaim and Sustainable Waste Handling

- Pricing Analysis

- Input Cost Structure: Cement, Aggregate, Admixture, Water and Energy Cost Per Cubic Metre

- RMC Grade-Wise Pricing Trends: M20 to M60 Retail and Bulk Contract Price Benchmarking Across Key Indian Cities

- Regional Price Differentials: Metro vs. Tier-2 and Tier-3 City Price Comparison

- Seasonal Pricing Dynamics: Pre-Monsoon, Post-Monsoon and Peak Construction Season Price Movements

- Margin Analysis: Gross and Net Margin Benchmarking for Organised and Unorganised RMC Producers

- Pricing Dynamics, Contract Structures and Volume Discount Frameworks for Large Project Supply

- Sustainability & Environmental Analysis

- Carbon Footprint of Ready-Mix Concrete in India: Embodied Carbon, Cement-Intensity Benchmarks and Pathway to Low-Carbon Concrete

- Fly Ash and GGBS Utilisation in Indian RMC: Environmental Benefits, Regulatory Mandates and Adoption Gaps

- Manufactured Sand (M-Sand) and Recycled Aggregate Adoption: Natural River Sand Conservation and Regulatory Push

- Water Consumption, Washout Water Recycling and Zero-Liquid-Discharge Practices at Indian RMC Batching Plants

- Green Building Rating Systems (GRIHA, IGBC and LEED India) and Their Influence on RMC Material Selection and Low-Carbon Mix Design

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Organised vs. Unorganised Sector and Regional Concentration)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Grade, Application and Geography

- Player Classification

- Pan-India Integrated RMC Companies (Cement Manufacturer-Backed)

- Independent and Private Equity-Backed RMC Producers

- Regional and City-Level RMC Operators

- Captive RMC Plants of Large Real Estate and Infrastructure Groups

- Emerging Technology-Driven and Green Concrete Specialists

- Competitive Analysis Frameworks

- Market Share Analysis by Grade, Application and Region

- Company Profile

- Company Overview & Headquarters

- RMC Product Portfolio, Grade Range and Specialty Mix Offerings

- Batching Plant Network: Number of Plants, Locations and Installed Capacity

- Transit Mixer and Pump Fleet Size

- Revenue (RMC Segment) and Volume Sold

- Key Project References and Customer Relationships

- Technology Differentiators, Quality Certifications & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Plant Expansions, New City Entries and Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Geographic Reach vs. Product Specialisation)

- Key Company Profiles

- Market Structure & Concentration

- Strategic Outlook & Opportunity Analysis

- Strategic Output

- Market Opportunity Matrix: By Grade, Application, End-User, Plant Type and Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Mix Design Innovation Strategy

- Plant Network Expansion & Operational Excellence Strategy

- Geographic Expansion into Tier-2 and Tier-3 Cities Strategy

- Customer & Project Developer Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability, Green Concrete & Low-Carbon Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output