Market Definition

The Global Textile Chemicals Market encompasses the research, development, formulation, manufacture, and supply of specialty and commodity chemical products applied across every stage of the textile and apparel value chain, from raw fiber preparation and yarn spinning through fabric formation, pretreatment, dyeing, printing, finishing, and functional coating operations that collectively transform natural and synthetic fibers into end-use textile products meeting defined aesthetic, functional, durability, and regulatory performance requirements. Textile chemicals are applied to a broad range of substrates including cotton, wool, silk, and other natural cellulosic and protein fibers; polyester, nylon, acrylic, and polypropylene synthetic fibers; regenerated fibers including viscose, modal, lyocell, and cupro; and blended fiber constructions across woven, knitted, and nonwoven fabric architectures. The chemical categories encompassed by the market include pretreatment chemicals such as desizing agents, scouring agents, bleaching chemicals, and mercerizing auxiliaries; dyestuffs and pigments spanning reactive, disperse, acid, vat, direct, and sulphur dye classes; printing chemicals including binders, thickeners, and specialty effect formulations; finishing chemicals encompassing softeners, handle modifiers, easy-care and wrinkle-resistant treatments, flame retardants, antimicrobial agents, water and oil repellents, and ultraviolet protection finishes; coating and lamination chemicals; and specialty functional chemical systems enabling moisture management, anti-static, phase-change thermal regulation, and smart textile capabilities. The complete market value chain extends from petrochemical and oleochemical raw material suppliers and dye intermediate producers through formulated textile chemical manufacturers, application auxiliaries suppliers, dyehouse machinery providers, and ultimately the global textile and apparel manufacturing industry whose production volumes, geographic concentration, and evolving performance and sustainability requirements define the demand structure of the global textile chemicals market.

Market Insights

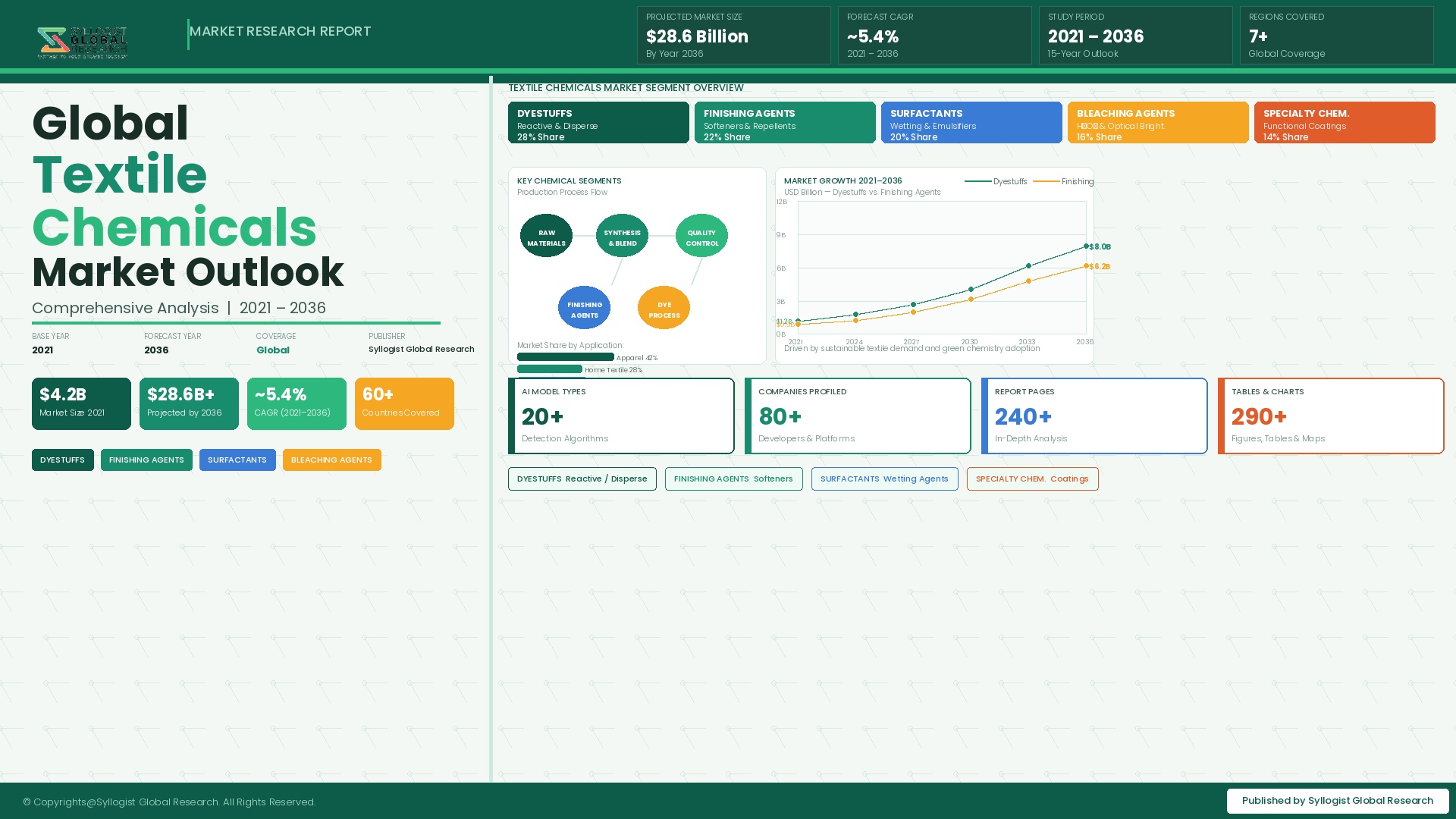

The global textile chemicals market was valued at approximately USD 26.8 billion in 2025 and is projected to reach USD 38.4 billion by 2034, advancing at a compound annual growth rate of 4.0% over the forecast period from 2027 to 2034. Market growth is underpinned by the continued expansion of global textile and apparel production volumes, the rising per-capita consumption of clothing and home textiles in emerging economies, and the growing application of functional and performance textile chemical treatments in technical textile, activewear, workwear, and home furnishing segments where value-added chemical finishing delivers measurable end-use performance differentiation. The industry is simultaneously undergoing a structural technology and sustainability transition as brands, retailers, and regulators intensify requirements for reduced chemical hazard profiles, lower water and energy consumption in wet processing operations, and verified supply chain compliance with chemical management standards, compelling textile chemical manufacturers to invest in next-generation formulation platforms that deliver equivalent or superior performance within tightened toxicological, environmental, and processing efficiency parameters.

The dyestuffs and pigments segment remains the largest single product category within textile chemicals by revenue, accounting for approximately 28% of global market value in 2025, with reactive dyes for cellulosic fiber dyeing and disperse dyes for polyester dyeing collectively representing the dominant dye consumption volumes across the global textile wet processing industry. However, the most commercially dynamic growth is occurring in functional and performance finishing chemicals, which are advancing at approximately 6.2% annually, driven by consumer demand for activewear and outdoor performance apparel with durable water repellency, moisture wicking, antimicrobial protection, and ultraviolet barrier properties; by occupational safety requirements driving flame retardant treatment of industrial workwear; and by home textile segment demand for easy-care, allergen barrier, and antimicrobial mattress, bedding, and upholstery fabric treatments. The transition away from perfluorooctanoic acid and perfluorooctane sulfonate-based durable water repellent chemistries toward fluorine-free alternatives is one of the most commercially significant technology transitions currently underway in textile finishing, with the global fluorine-free durable water repellent segment growing at approximately 11.4% annually as brands and manufacturers accelerate phase-out commitments ahead of regulatory deadlines and voluntary chemical restriction milestones.

Asia-Pacific dominates global textile chemical consumption, accounting for approximately 61% of total market volume in 2025, driven by the overwhelming concentration of global textile and apparel manufacturing capacity in China, India, Bangladesh, Vietnam, Indonesia, Pakistan, and Turkey, whose collective output encompasses the vast majority of the world’s fiber processing, fabric production, dyeing, and garment manufacturing activity. China alone accounts for approximately 38% of global textile chemical consumption, representing the world’s largest single national market served by both domestic textile chemical manufacturers and international specialty chemical suppliers operating local production and technical service infrastructure. India’s textile chemical market is the second-largest in Asia-Pacific and is growing at approximately 5.8% annually, driven by expanding domestic apparel manufacturing capacity, government-supported textile park development, and the migration of global apparel sourcing programs toward Indian suppliers in response to supply chain diversification strategies implemented by major international fashion brands and retailers. Europe and North America together account for approximately 24% of global textile chemical revenue, with consumption concentrated in high-value technical textile, performance apparel, home furnishing, and automotive textile applications where advanced functional finishing chemistry commands premium pricing.

Sustainability and circular economy imperatives are reshaping the technology investment priorities and competitive positioning requirements of textile chemical manufacturers more profoundly than any other market force in the current decade, as the global apparel and textile industry faces intensifying scrutiny of its environmental footprint from regulators, brand sustainability programs, investor environmental, social, and governance criteria, and end-consumer awareness of textile manufacturing’s water, chemical, and carbon impacts. The Zdhc Manufacturer Restricted Substances List and its associated wastewater guidelines have become de facto compliance requirements for chemical suppliers serving the major international apparel brand supply chains, compelling textile chemical manufacturers to invest in comprehensive product toxicological assessment, safer chemistry reformulation, and supply chain transparency infrastructure to maintain access to the premium brand tier of the global apparel market. Waterless and low-water textile dyeing and finishing technologies, including supercritical carbon dioxide dyeing, foam application finishing, digital textile printing, and plasma surface treatment, are advancing from pilot-scale demonstration toward commercial adoption, with digital textile printing growing at approximately 13.6% annually and progressively displacing conventional screen printing in fashion fabric and home decor printing applications where short run flexibility, design complexity, and reduced water consumption deliver compelling process and commercial advantages.

Key Drivers

Expanding Global Apparel and Technical Textile Production Volumes Sustaining Broad-Based Textile Chemical Demand Across Fiber, Fabric, and Finishing Segments

The structural expansion of global apparel consumption, driven by rising disposable incomes and growing middle-class populations across Asia-Pacific, the Middle East, Africa, and Latin America, is generating sustained volume growth in textile and garment production that directly translates into increasing demand for the full spectrum of textile process chemicals applied across fiber preparation, dyeing, printing, and finishing stages of the textile manufacturing value chain. Global fiber production reached approximately 124 million metric tons in 2025, of which polyester accounted for approximately 57%, cotton for approximately 22%, and other synthetic, cellulosic, and natural fibers for the remainder, with total fiber output projected to grow to approximately 152 million metric tons by 2034 as apparel consumption growth in emerging markets and the expanding technical textile sector collectively drive fiber demand beyond the historical growth trajectory of the apparel segment alone. Technical textiles represent the fastest-growing end-use category for advanced textile chemical applications, encompassing geotextiles, medical and hygiene nonwovens, automotive interior fabrics, filtration media, protective clothing, and construction textiles whose performance requirements demand sophisticated chemical treatment systems including durable flame retardants, high-performance binders and coating systems, and specialty functional finishes that command substantially higher average selling prices per unit weight of fabric treated than equivalent chemicals applied in conventional apparel fabric finishing operations.

Performance Apparel and Activewear Growth Driving Durable Functional Finishing Chemical Demand Across Water Repellency, Antimicrobial, and Moisture Management Applications

The sustained global growth of the activewear, athleisure, and outdoor performance apparel segments is generating structurally expanding demand for advanced textile finishing chemical systems delivering durable water repellency, moisture transport and quick-dry performance, antimicrobial odor control, ultraviolet protection, and mechanical stretch enhancement properties that differentiate premium performance garments in a competitive marketplace where functional performance claims are validated by standardized test method compliance and durability through repeated laundering cycles. The global activewear market, valued at approximately USD 386 billion in 2025, is growing at approximately 6.4% annually and requires a disproportionately high chemical treatment content per unit weight of fabric relative to conventional apparel, as the multi-functional performance specifications of technical activewear garments necessitate multiple sequential or combined chemical finishing treatments applied with precision to maintain performance durability through 50 or more home wash cycles. The regulatory-mandated transition away from long-chain perfluorocarbon durable water repellent chemistries is generating a qualification and adoption cycle for fluorine-free alternatives including dendrimer-based, polyurethane-based, wax dispersion, and bio-based repellent technologies, creating significant commercial opportunities for textile chemical manufacturers who have successfully developed and validated fluorine-free durable water repellent systems meeting the demanding wash durability and repellency performance requirements of leading performance apparel brands.

Nonwoven Fabric Industry Expansion in Hygiene, Medical, and Filtration Applications Generating Specialty Binder and Functional Chemical Demand

The global nonwoven fabrics industry is among the fastest-growing segments of the broader textile manufacturing sector, with production volumes expanding at approximately 6.1% annually driven by sustained demand growth in disposable hygiene products including diapers, adult incontinence articles, and feminine hygiene products; single-use and reusable medical and surgical nonwovens including gowns, drapes, and face masks whose demand base was permanently elevated following the global health emergency of 2020 to 2022; filtration media for air and liquid purification applications in industrial, HVAC, and automotive sectors; and geotextile applications in road construction, drainage, and erosion control infrastructure. Nonwoven fabric production requires specialty textile chemical inputs including acrylic, vinyl acetate, and styrene-butadiene latex binders for bonded nonwoven construction; hydrophilic and hydrophobic surface treatment agents governing fluid management behavior in hygiene and medical applications; flame retardant finishes for construction and automotive nonwovens; and specialty softeners and mechanical property modifiers that define the tactile and functional performance characteristics of the finished nonwoven product. The growing adoption of sustainable and compostable nonwoven materials based on polylactic acid, lyocell, and other bio-derived fiber platforms is generating incremental demand for compatible binder chemistries, bio-based finishing agents, and process auxiliaries specifically formulated for the distinctive chemical and thermal characteristics of next-generation sustainable nonwoven substrates.

Key Challenges

Stringent Chemical Restriction Frameworks and the Compliance Cost of Reformulating Restricted Substance List Non-Compliant Textile Chemical Products

The global textile chemical industry operates under an increasingly stringent and complex regulatory and brand-driven chemical restriction environment, with the Zdhc Manufacturer Restricted Substances List, REACH regulation, Oeko-Tex Standard 100, bluesign system requirements, and country-specific restricted substance regulations collectively governing the permissible chemistry scope for textile chemicals sold into major international apparel brand supply chains, imposing continuous reformulation requirements on chemical suppliers whose product portfolios contain substances flagged for hazard classification, environmental persistence, or bioaccumulation potential under evolving toxicological assessment frameworks. The pace of restricted substance list expansion has accelerated materially since 2018, with new substances added to the Zdhc Manufacturing Restricted Substances List and REACH candidate list at a rate that requires textile chemical manufacturers to maintain continuous product toxicological surveillance programs, invest in alternative chemistry development ahead of formal regulatory restriction timelines, and manage complex customer communication and product transition programs that consume significant technical service and regulatory affairs resources. Reformulation of restricted textile chemical products is technically complex and commercially costly, as the functional performance of established softener, dye, finishing agent, and auxiliary chemical formulations often depends on specific chemical structural features or active ingredient combinations whose direct substitution with lower-hazard alternatives requires extensive application testing, process parameter re-optimization, and customer qualification programs that can extend from 12 to 24 months per product reformulation program.

Water Scarcity, Effluent Treatment Compliance, and the Capital Investment Required for Sustainable Wet Processing Infrastructure Constraining Market Growth

Textile dyeing and finishing operations are among the most water-intensive manufacturing processes in global industry, with conventional continuous and batch dyeing processes consuming between 50 and 150 liters of water per kilogram of fabric processed depending on substrate type, dye class, and process configuration, generating large volumes of colored and chemically contaminated wastewater whose treatment and disposal impose substantial operating cost and regulatory compliance obligations on textile wet processing facilities in all major manufacturing regions. Tightening wastewater discharge standards across China, India, Bangladesh, Vietnam, and other major textile manufacturing jurisdictions are compelling wet processing facilities to invest in effluent treatment plant upgrades, water recycling systems, and process chemistry modifications that reduce both water consumption per kilogram of production and the chemical oxygen demand, color, heavy metal, and priority substance concentrations of treated effluent, generating investment requirements that are particularly burdensome for small and medium-sized dyeing and finishing operators who constitute the majority of the global textile wet processing industry by establishment count. Textile chemical manufacturers are responding by developing high-exhaustion dyeing systems, low-electrolyte reactive dye formulations, concentrated and reduced-dosage finishing chemical formats, and process auxiliary systems compatible with short-liquor-ratio dyeing machinery, but the pace of sustainable wet processing technology adoption across the fragmented global dyeing and finishing industry is constrained by capital availability limitations, technical knowledge barriers, and competitive price pressure that prioritizes short-term production cost minimization over longer-term sustainability investment.

Raw Material Cost Volatility and Supply Chain Disruption Risk Across Petrochemical, Oleochemical, and Dye Intermediate Supply Chains

Textile chemical manufacturers operate across multiple raw material supply chains whose price dynamics are governed by petrochemical feedstock costs, oleochemical commodity markets, and the highly concentrated global supply base of synthetic dye intermediates, creating persistent and often simultaneous raw material cost pressures that are difficult to manage within the price-competitive and contractually constrained pricing relationships characterizing textile chemical supply to large-scale dyeing and finishing operations in cost-focused manufacturing regions. The global synthetic dye intermediate supply chain is heavily concentrated in China, which accounts for the majority of global production capacity for key dye intermediates including H-acid, gamma acid, vinyl sulphone, and anthraquinone derivatives, creating systemic supply vulnerability to Chinese production curtailments triggered by environmental inspection programs, energy rationing events, or export policy changes, as demonstrated by the severe dye intermediate shortages and price spikes experienced across the global textile wet processing industry during multiple supply disruption events in recent years. Surfactant and emulsifier raw materials for textile auxiliary chemical formulation are subject to the price volatility of fatty alcohol, ethylene oxide, and propylene oxide feedstocks whose cost cycles are driven by palm kernel oil and coconut oil commodity markets and petrochemical feedstock pricing, creating correlated cost pressures across multiple textile auxiliary chemical product lines that compress formulator margins during feedstock price escalation events when limited customer price pass-through flexibility constrains revenue recovery within contracted supply relationships.

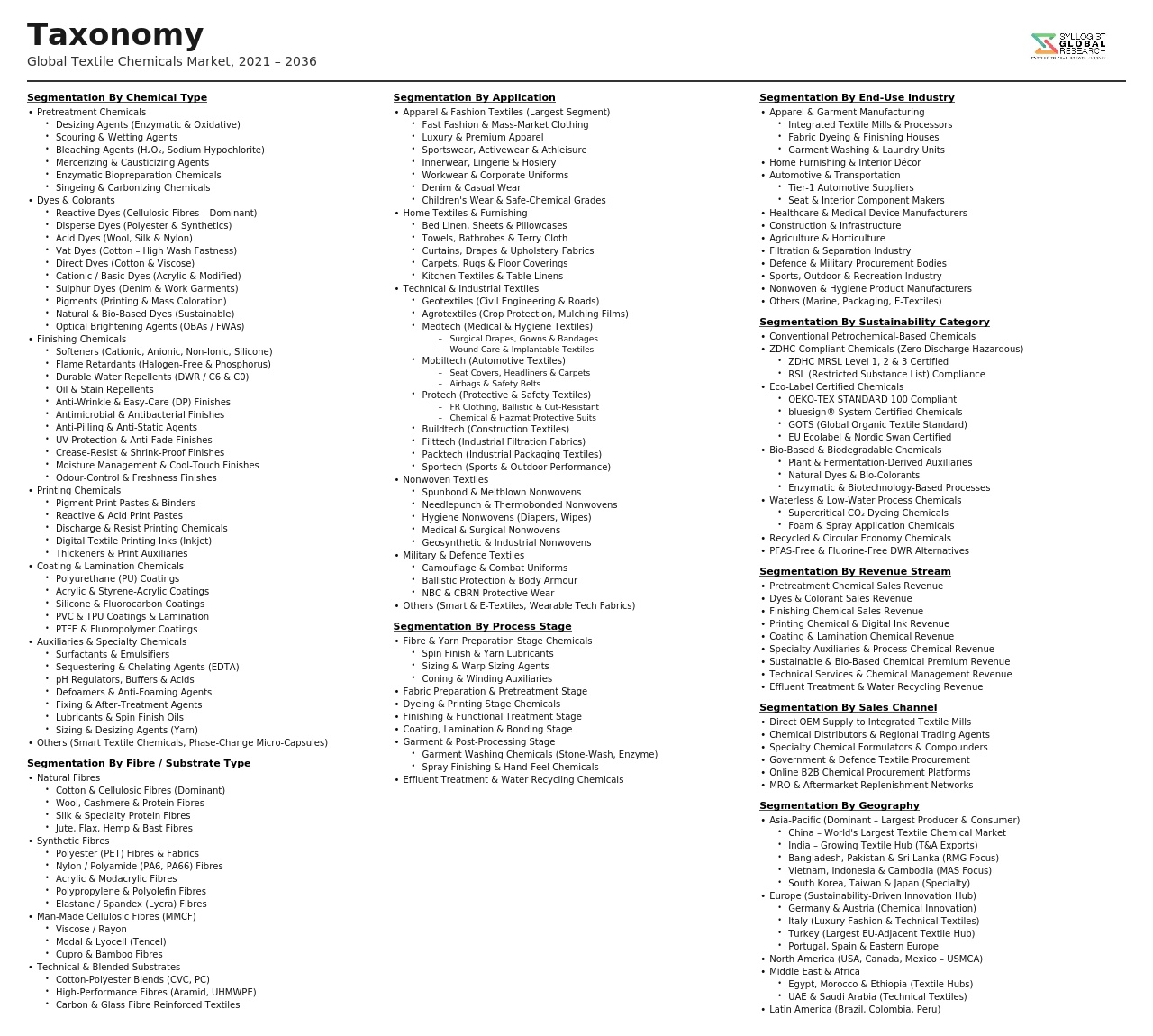

Market Segmentation

- Segmentation By Product Type

- Dyestuffs (Reactive, Disperse, Acid, Vat, Direct, and Sulphur Dyes)

- Pigments and Pigment Preparations

- Pretreatment Chemicals (Desizing, Scouring, Bleaching, and Mercerizing Agents)

- Finishing Chemicals (Softeners, Wrinkle Resist, Flame Retardants, and Repellents)

- Printing Chemicals (Binders, Thickeners, and Specialty Effect Formulations)

- Coating and Lamination Chemicals

- Sizing and Re-Sizing Agents

- Specialty Functional Chemicals (Antimicrobial, UV Protection, and Moisture Management)

- Others

- Segmentation By Application Process

- Fiber and Yarn Preparation

- Fabric Pretreatment and Preparation

- Dyeing (Exhaust, Continuous, and Semi-Continuous)

- Textile Printing (Screen, Rotary, and Digital)

- Chemical and Functional Finishing

- Coating and Lamination

- Nonwoven Bonding and Finishing

- Others

- Segmentation By Fiber Type

- Cotton and Natural Cellulosic Fibers

- Wool, Silk, and Protein Fibers

- Polyester

- Nylon (Polyamide)

- Acrylic and Other Synthetic Fibers

- Viscose, Modal, Lyocell, and Regenerated Cellulosic Fibers

- Blended Fiber Constructions

- Others

- Segmentation By End-Use Industry

- Apparel and Garments

- Home Textiles (Bedding, Upholstery, and Floor Coverings)

- Technical Textiles (Geotextiles, Automotive, and Protective Clothing)

- Medical and Hygiene Nonwovens

- Filtration Textiles

- Sports and Performance Apparel

- Industrial Textiles

- Others

- Segmentation By Functionality

- Aesthetic Finishing (Softness, Handle, and Appearance)

- Durable Water and Oil Repellency

- Flame Retardant Treatment

- Antimicrobial and Odor Control

- Easy Care and Wrinkle Resistance

- Ultraviolet Protection

- Moisture Management and Quick Dry

- Thermal Regulation and Phase Change

- Others

- Segmentation By Technology

- Conventional Aqueous Wet Processing Chemicals

- Low-Water and Waterless Process Chemicals

- Fluorine-Free Functional Finish Systems

- Bio-Based and Biodegradable Textile Chemicals

- Digital Printing Ink and Pretreatment Systems

- Others

- Segmentation By Sales Channel

- Direct Supply to Textile Mills and Dyehouses

- Specialty Chemical Distributors

- Textile Machinery and Process Integrators

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Textile Chemicals Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by product type, dyestuffs, finishing chemicals, pretreatment chemicals, printing chemicals, and coating chemicals, and by end-use application, apparel, home textiles, technical textiles, and nonwovens, to enable textile chemical manufacturers, apparel brands, fiber producers, and investors to identify which product categories and application segments will generate the highest absolute revenue and most durable growth trajectory across the forecast period in the context of expanding global fiber production, sustainability-driven technology transitions, and the rapid growth of technical textile applications?

- How is the global regulatory and brand-driven transition away from restricted substances, specifically long-chain perfluorocarbon durable water repellent chemistries, certain reactive and disperse dye classes, formaldehyde-releasing easy-care finishing agents, and halogenated flame retardants, expected to reshape the technology investment priorities, product portfolio composition, and competitive positioning of textile chemical manufacturers through 2034, and which alternative chemistry platforms are best positioned to capture the qualification and adoption opportunities generated by the phase-out of restricted substances across durable water repellency, flame retardancy, easy-care finishing, and antimicrobial treatment application segments?

- What is the projected market size, growth rate, and competitive structure of the fluorine-free durable water repellent textile finishing segment through 2034, encompassing dendrimer-based, polyurethane-based, wax dispersion, and bio-based repellent technologies, which performance parameters represent the most significant remaining technical barriers to full replacement of perfluorocarbon-based systems in demanding outdoor and performance apparel applications, and which textile chemical manufacturers have achieved the highest levels of brand qualification and commercial adoption across tier-one performance apparel supply chains?

- How are digital textile printing technology adoption, waterless and low-water dyeing and finishing process innovations including supercritical carbon dioxide dyeing and foam application systems, and bio-based and biodegradable textile chemical platform development expected to reshape the competitive dynamics, capital investment requirements, and revenue trajectory of the global textile chemicals market through 2034, and what are the implications for incumbent conventional textile chemical suppliers, new entrant sustainable chemistry developers, and the dyeing and finishing equipment manufacturers whose process platforms define the chemical application environment?

- Who are the leading textile chemical manufacturers, specialty dye producers, functional finishing chemical developers, and sustainable textile chemistry innovators currently defining the competitive landscape of the global textile chemicals market, and what are their respective product portfolio breadth across dye classes and finishing chemical categories, manufacturing footprint and regional technical service infrastructure, customer qualification status with major international apparel brands and technical textile manufacturers, research and development investment in sustainable and bio-based chemistry platforms, and strategic positioning responses to the regulatory, sustainability, and raw material supply chain challenges reshaping global textile chemical market competitive dynamics through 2034?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Raw Material Price Volatility, Petrochemical Feedstock Dependency & Supply Chain Disruption Risk

- Stringent Chemical Restriction Regulations (ZDHC, REACH, OEKO-TEX) & Hazardous Substance Compliance Risk

- Wastewater Effluent Standards, Environmental Liability & Effluent Treatment Cost Risk for Textile Wet Processing Units

- Textile End-Market Demand Volatility: Fast Fashion Cyclicality, Apparel Consumption Shifts & Nearshoring Risk

- Substitution Risk from Sustainable, Bio-Based & Waterless Processing Technologies Disrupting Conventional Chemical Use

- Regulatory Framework & Standards

- ZDHC (Zero Discharge of Hazardous Chemicals) Manufacturing Restricted Substances List (MRSL) & Wastewater Guidelines for Textile Chemical Suppliers

- REACH Regulation, SVHC Restrictions & Substance Authorisation Framework Applicable to Textile Auxiliaries and Dyes in the European Union

- OEKO-TEX STANDARD 100, BLUESIGN, GRS & Third-Party Certification Schemes for Textile Chemical Safety and Sustainability

- National Effluent Discharge Standards, Colour and COD Limits & Industrial Wastewater Regulations Across Key Textile Manufacturing Geographies

- Azo Dye Restrictions, Formaldehyde Limits, APEOs Ban & Consumer Product Chemical Safety Regulations in Apparel and Home Textiles

- Global Textile Chemicals Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Kilotons)

- Market Size & Forecast by Chemical Type

- Dyes and Pigments

- Finishing Chemicals

- Coating and Sizing Chemicals

- Desizing, Scouring and Bleaching Chemicals

- Surfactants and Wetting Agents

- Fixing Agents, Softeners and Handle Modifiers

- Flame Retardants for Textiles

- Antimicrobial and Odour-Control Agents

- Optical Brightening Agents (OBAs)

- Specialty and Functional Chemicals (Moisture Management, UV Protection and Soil Release)

- Other Textile Chemicals

- Market Size & Forecast by Dye Type

- Reactive Dyes

- Disperse Dyes

- Acid Dyes

- Direct Dyes

- Vat Dyes

- Sulphur Dyes

- Basic (Cationic) Dyes

- Pigment Dyes and Print Pastes

- Natural and Bio-Based Dyes

- Market Size & Forecast by Process Stage

- Fibre and Yarn Preparation (Sizing, Desizing, Scouring and Bleaching)

- Dyeing and Printing

- Finishing and Functional Treatment

- Coating and Lamination

- Washing, Rinsing and Effluent Treatment

- Market Size & Forecast by Fibre Type

- Cotton and Natural Cellulosic Fibres

- Polyester and Synthetic Fibres

- Nylon (Polyamide)

- Wool and Protein Fibres

- Viscose, Modal and Lyocell (Regenerated Cellulosic Fibres)

- Blended and Technical Fibres

- Market Size & Forecast by End-Use Industry

- Apparel and Fashion (Woven, Knitted and Denim)

- Home Textiles (Bed Linen, Curtains, Upholstery and Carpets)

- Technical and Industrial Textiles (Geotextiles, Filtration, Medical and Protective)

- Nonwovens (Hygiene, Medical and Construction Nonwovens)

- Automotive Textiles (Seat Fabrics, Carpets and Headliners)

- Sportswear and Performance Textiles

- Market Size & Forecast by Formulation Type

- Waterborne Formulations

- Solvent-Based Formulations

- Powder and Solid Formulations

- Bio-Based and Sustainable Formulations

- Market Size & Forecast by Sales Channel

- Direct Sales to Textile Mills and Wet Processing Units

- Specialty Chemical Distributors and Trading Houses

- OEM and Long-Term Supply Agreement Channels

- E-Commerce and Spot Market Channels

- North America Textile Chemicals Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotons)

- By Chemical Type

- By Dye Type

- By Process Stage

- By Fibre Type

- By End-Use Industry

- By Formulation Type

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Textile Chemicals Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotons)

- By Chemical Type

- By Dye Type

- By Process Stage

- By Fibre Type

- By End-Use Industry

- By Formulation Type

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Textile Chemicals Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotons)

- By Chemical Type

- By Dye Type

- By Process Stage

- By Fibre Type

- By End-Use Industry

- By Formulation Type

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Textile Chemicals Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotons)

- By Chemical Type

- By Dye Type

- By Process Stage

- By Fibre Type

- By End-Use Industry

- By Formulation Type

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Textile Chemicals Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotons)

- By Chemical Type

- By Dye Type

- By Process Stage

- By Fibre Type

- By End-Use Industry

- By Formulation Type

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Textile Chemicals Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotons)

- By Chemical Type

- By Dye Type

- By Process Stage

- By Fibre Type

- By End-Use Industry

- By Formulation Type

- By Country

- By Sales Channel

- Market Size & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Italy, Spain, Netherlands, Turkey, China, India, Bangladesh, Pakistan, Vietnam, Indonesia, South Korea, Japan, Brazil, Argentina, Saudi Arabia, UAE, Egypt, South Africa

- Technology Landscape & Innovation Analysis

- Low-Liquor-Ratio and Waterless Dyeing Technology Deep-Dive (Supercritical CO2 and Air Dyeing)

- Reactive Dye Chemistry Innovations for High Fixation, Low Salt and Low Water Dyeing of Cotton

- Digital Textile Printing Chemistry: Inkjet Inks, Pre-Treatment and Post-Treatment Chemical Systems

- Bio-Based and Enzymatic Processing: Biopreparation, Biopolishing and Enzyme-Assisted Dyeing

- Nanotechnology Applications in Textile Finishing: Nanosilver, Nano-TiO2 and Nanocoatings

- Durable Water Repellency (DWR) Chemistry: PFAS-Free Alternatives and Next-Generation Fluorocarbon Substitutes

- Smart and Functional Textile Chemical Technologies: Phase-Change Materials, Chromic Dyes and Electrically Conductive Coatings

- Patent & IP Landscape in Textile Chemical Technologies

- Value Chain & Supply Chain Analysis

- Raw Material and Intermediate Chemical Supply Chain (Aromatic Intermediates, Auxiliaries and Surfactant Feedstocks)

- Dye and Pigment Synthesis and Manufacturing Supply Chain

- Textile Auxiliary and Finishing Chemical Formulation and Compounding

- Quality Testing, ZDHC MRSL Conformance and Third-Party Certification

- Distribution and Logistics to Wet Processing Mills and Converters

- Effluent Treatment, Dye Recovery and Circular Economy in Textile Chemical Use

- Brand and Retailer Chemical Compliance Programmes and Supply Chain Transparency

- Pricing Analysis

- Raw Material and Intermediate Cost Passthrough: Aromatic Feedstock Price Linkage to Dye and Auxiliary Pricing

- Reactive and Disperse Dye Spot and Contract Price Trends

- Textile Auxiliary and Finishing Chemical Price Benchmarking by Application

- Bio-Based and Sustainable Textile Chemical Price Premium Analysis vs. Conventional Alternatives

- Regional Price Differentials and Import Parity Analysis Across Key Textile Manufacturing Hubs

- Pricing Dynamics, Contract Structures and Volume Discount Frameworks

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Textile Chemicals: Carbon Footprint, Water Consumption and Hazardous Waste Generation Across Chemical Categories and Process Stages

- Water Intensity, Effluent Colour, COD and Heavy Metal Discharge: Environmental Impact of Conventional Dyeing and Finishing

- Transition to PFAS-Free DWR, Low-Salt Reactive Dyeing and Formaldehyde-Free Finishing: Regulatory Drivers and Market Adoption

- Bio-Based and Biodegradable Textile Chemical Adoption: Feedstock Sourcing, Biodegradability Claims and Commercial Readiness

- Regulatory-Driven Sustainability, ZDHC, OEKO-TEX, SDG 6 (Clean Water) Alignment and ESG Disclosure in Textile Chemical Supply Chains

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Chemical Type and Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Chemical Type, Process Stage and Geography

- Player Classification

- Global Integrated Textile Dye and Chemical Manufacturers

- Specialty Textile Auxiliary and Finishing Chemical Companies

- Dedicated Reactive and Disperse Dye Producers

- Bio-Based and Sustainable Textile Chemical Specialists

- Digital Textile Printing Ink and Pre-Treatment Chemical Providers

- Regional and Emerging Market Textile Chemical Manufacturers

- Competitive Analysis Frameworks

- Market Share Analysis by Chemical Type, Process Stage and Region

- Company Profile

- Company Overview & Headquarters

- Textile Chemical Product Portfolio and Technology Platforms

- Key Customer Relationships & Reference Mill Accounts

- Manufacturing Footprint & Production Capacity

- Revenue (Textile Chemicals Segment) and R&D Spend

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Product Launches, ZDHC Approvals and Capacity Expansions)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Sustainability Leadership vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Strategic Outlook & Opportunity Analysis

- Strategic Output

- Market Opportunity Matrix: By Chemical Type, Dye Type, Process Stage, End-Use Industry and Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output