Market Definition

The Europe Xanthates Market encompasses the production, formulation, distribution, and commercial application of xanthate compounds, a class of organosulfur chemicals synthesized through the reaction of an alcohol with carbon disulfide in the presence of an alkali metal hydroxide, yielding alkali metal xanthate salts of which potassium ethyl xanthate, sodium ethyl xanthate, sodium isobutyl xanthate, potassium amyl xanthate, and sodium isopropyl xanthate represent the principal commercially significant variants deployed across industrial applications in the region. Xanthates function as highly selective collector reagents in froth flotation mineral processing operations, where their chemisorptive interaction with sulfide mineral surfaces imparts hydrophobicity that enables the selective attachment of target mineral particles to air bubbles and their concentration into froth overflow products, making xanthates the dominant class of sulfide mineral collectors used in the flotation beneficiation of copper, lead, zinc, nickel, molybdenum, and precious metal-bearing sulfide ore concentrates processed at European mining and metallurgical operations. Beyond mineral processing, xanthates serve as accelerators and vulcanization agents in natural and synthetic rubber compounding, as intermediates in the synthesis of herbicides and pesticides within the agrochemical industry, and as chemical reagents in textile fiber processing applications including the viscose rayon production process in which cellulose xanthate intermediate formation constitutes the central chemical transformation step. Key market participants encompass integrated chemical manufacturers producing xanthates within broader organosulfur or mining chemicals product portfolios, specialty reagent formulators supplying customized collector blends to mineral processing customers, mining company procurement organizations sourcing flotation reagents for captive European mine operations, rubber compounding facilities integrating xanthate accelerators into elastomer processing formulations, and agrochemical manufacturers utilizing xanthate chemistry as synthetic building blocks in crop protection product development.

Market Insights

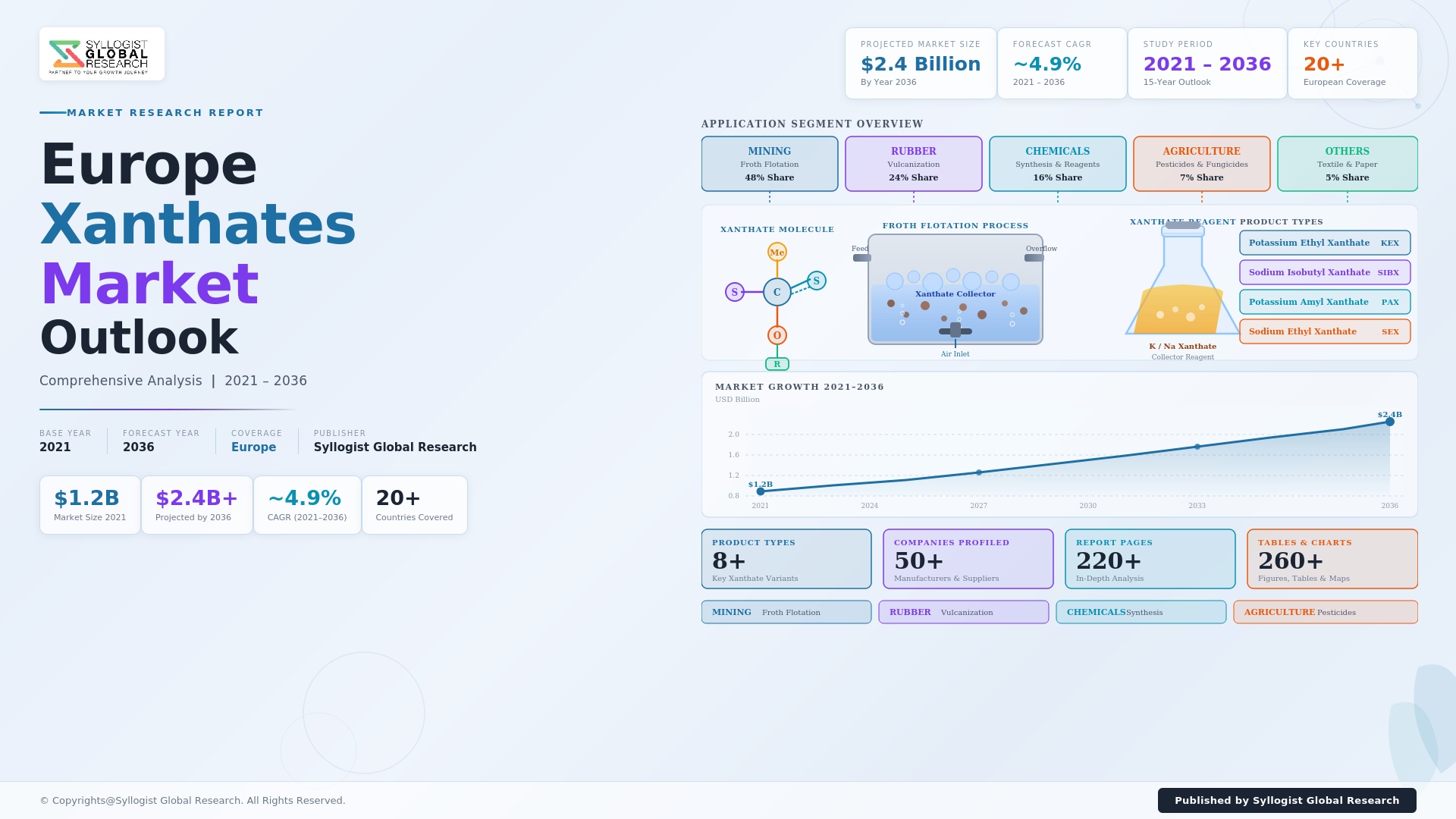

The European xanthates market is defined by its structural dependence on the mining and mineral processing industry, which accounts for approximately 68% of total regional xanthate consumption in 2025, a demand concentration that anchors the market’s growth trajectory to the operational status and expansion plans of European base metal mining operations in Scandinavia, the Iberian Peninsula, Poland, and the Balkans, while simultaneously exposing regional xanthate demand to the cyclical capital expenditure and production volume dynamics of the European metals industry. The Europe Xanthates Market was valued at approximately USD 312 million in 2025 and is projected to reach USD 467 million by 2034, advancing at a compound annual growth rate of 4.6% over the forecast period from 2027 to 2034, driven by sustained demand from froth flotation applications in copper, zinc, and nickel sulfide ore processing across active European mining regions, incremental demand growth from rubber processing and agrochemical synthesis applications, and the progressive expansion of European critical mineral development programs that are advancing new sulfide ore deposit feasibility studies and mine construction projects with multi-decade production horizons. Sweden, Finland, and Norway collectively constitute the largest national demand cluster within Europe for froth flotation xanthate reagents, anchored by the operating copper, zinc, nickel, and cobalt mining complexes of the Fennoscandian Shield, where ore body mineralogy and processing plant design are optimized around xanthate-based collector systems that are deeply embedded in plant metallurgical practice and operationally difficult to substitute without substantial process re-engineering investment and production risk acceptance. Poland and the Czech Republic represent significant secondary demand centers, with Polish copper and zinc mining operations consuming substantial annual volumes of sodium ethyl xanthate and potassium amyl xanthate in flotation circuits processing complex polymetallic sulfide ores whose selective mineral separation requirements favor xanthate collectors over alternative collector chemistries for their established selectivity profiles and predictable metallurgical performance at industrial scale.

The critical minerals policy agenda advancing across the European Union under the European Critical Raw Materials Act, adopted in 2024 with binding targets for domestic extraction of 10% of the European Union’s annual consumption of strategic raw materials by 2030, is generating a structurally meaningful medium-term growth catalyst for European xanthate demand by accelerating the permitting, development, and production ramp-up of new copper, nickel, cobalt, and lithium mineral projects across member states whose sulfide ore mineralogy will require froth flotation beneficiation deploying xanthate collector reagents at commercial scale. The European Critical Raw Materials Act designation of copper, nickel, cobalt, manganese, and lithium as strategic raw materials subject to accelerated permitting timelines and enhanced project financing access creates a regulatory environment uniquely favorable to the commissioning of new European mining and processing operations that will establish additional structural xanthate consumption demand increments not anticipated in pre-policy demand projections. Finland is advancing multiple nickel and cobalt sulfide project developments in its central and northern mining districts, Spain is progressing copper and zinc project development in its Iberian Pyrite Belt, Serbia and North Macedonia are advancing copper porphyry and polymetallic project pipelines with significant production potential, and Greenland, while outside the European Union, is developing large-scale mineral deposits accessible to European processing infrastructure, collectively creating a pipeline of new xanthate-consuming flotation operations scheduled for commissioning between 2027 and 2034 that will expand the structural consumption base of the European xanthates market beyond its current established mining customer foundation. The total incremental annual xanthate demand attributable to the new European critical mineral project pipeline reaching production before 2034 is estimated at approximately 8,400 metric tons, representing a meaningful addition to current European annual consumption of approximately 41,200 metric tons.

The supply architecture of the European xanthates market is characterized by a concentrated manufacturing base in which a small number of integrated chemical producers operating large-scale production facilities in Germany, the Netherlands, Belgium, and Russia supply the majority of European industrial demand, supplemented by imports from Chinese xanthate producers who have established a significant European market presence on the basis of competitive pricing, product range breadth, and logistical flexibility that has intensified competitive pressure on European incumbent manufacturers over the past decade. European xanthate manufacturers are responding to Chinese import competition by differentiating on the basis of technical service capability, product consistency assurance, regulatory compliance documentation depth, and co-development of application-specific collector formulations that create customer switching costs and value-in-use advantages beyond the unit reagent price comparison framework within which Chinese volume producers seek to compete. The REACH regulation framework governing industrial chemical registration, evaluation, and authorization in the European Union imposes compliance documentation obligations on xanthate importers that increase the cost of market access for non-European suppliers and create a structural barrier that partially insulates European producers from the full force of Chinese import price competition, though established Chinese suppliers with invested REACH compliance infrastructure have navigated these barriers effectively and continue to supply European customers at competitive price points. Environmental and occupational health regulatory requirements governing carbon disulfide emissions and hydrogen sulfide gas generation during xanthate manufacturing, storage, and application operations are more stringent in Europe than in most competing production geographies, imposing higher operating cost burdens on European manufacturers but simultaneously incentivizing investment in safer manufacturing process designs, enclosed reagent handling systems, and environmental monitoring infrastructure that are increasingly valued by European mining customers with ambitious corporate sustainability commitments and supply chain environmental due diligence obligations.

The rubber processing and agrochemical application segments represent structurally stable secondary demand pools for European xanthates, with the rubber vulcanization accelerator application consuming xanthate compounds including zinc ethyl xanthate and zinc isopropyl xanthate in the compounding of natural rubber, styrene-butadiene rubber, and nitrile rubber articles including automotive seals, industrial hoses, conveyor belts, and specialty elastomeric components manufactured at European rubber processing facilities in Germany, France, Italy, Poland, and the United Kingdom. Xanthate-derived accelerators occupy a defined performance niche in rubber compounding formulations where their ultra-fast vulcanization kinetics at low processing temperatures provide practical manufacturing advantages for specific article geometries and processing equipment configurations that alternative accelerator chemistries cannot fully replicate, creating a structurally resilient xanthate demand segment in rubber that is moderately but not acutely sensitive to rubber compounding industry cyclicality. The agrochemical synthesis application for European xanthates is driven by the use of xanthate chemistry as an intermediate in the synthesis of dithiocarbamate fungicides, metam-sodium soil fumigants, and certain herbicide active ingredients manufactured at European agrochemical production facilities, with demand stability underpinned by the essential crop protection function of dithiocarbamate fungicides in European viticulture, potato cultivation, and horticultural production systems where alternatives with equivalent spectrum and cost-effectiveness remain limited despite regulatory scrutiny. The viscose rayon fiber application, while declining in absolute European production volume as textile manufacturing has migrated progressively to Asia over the past three decades, retains a niche consumption presence among specialty textile producers in Austria, Germany, and the Nordic countries whose high-value technical fiber and nonwoven fabric operations continue to utilize xanthate-based cellulose processing chemistry in the production of specialty viscose products commanding premium market positions in medical, filtration, and performance textile segments.

Key Drivers

European Critical Raw Materials Act and Strategic Mineral Independence Policy Driving New Mine Development and Incremental Flotation Reagent Demand Across the Region The adoption of the European Critical Raw Materials Act in 2024 and the parallel deployment of national critical mineral strategies across European Union member states and associated countries has established a policy-backed development pipeline for new European sulfide ore mining projects whose froth flotation beneficiation requirements will generate sustained incremental demand for xanthate collector reagents across the forecast period to 2034. The strategic imperative of reducing European dependence on imported critical mineral supplies from geopolitically concentrated production geographies has translated into accelerated environmental permitting decisions, enhanced public financing availability through the European Investment Bank and national development banks, and streamlined planning procedures under the European Critical Raw Materials Act Strategic Projects designation framework that collectively reduce the regulatory timeline and financing cost barriers that have historically constrained new European mine development. The beneficiation of copper, nickel, cobalt, and zinc sulfide ores at new and expanding European mining operations requires xanthate collector dosing rates of approximately 40 to 180 grams per metric ton of ore processed depending on ore mineralogy, sulfide mineral grade, and target recovery specifications, creating durable multi-year reagent procurement commitments from new mine operators that expand the structural consumption base of the European xanthates market on a foundation of long-term operating contract relationships whose demand is substantially insensitive to short-term commodity price fluctuations once mining operations have achieved steady-state production.

Expanding European Copper and Zinc Smelting and Recycling Operations Sustaining Concentrate Processing Demand for Froth Flotation Reagents at Existing Facilities Europe’s established base metal smelting and refining infrastructure in Germany, Belgium, Finland, Poland, Spain, and Bulgaria creates a sustained and contractually anchored demand for sulfide mineral concentrates produced by flotation beneficiation operations deploying xanthate collectors, with the operational continuity of smelter feed procurement relationships providing xanthate demand stability that is partially decoupled from the near-term fluctuations in European new mine development activity. The expansion of secondary copper and zinc recovery from electronic waste, industrial scrap, and complex residue streams through hydrometallurgical and pyrometallurgical processing routes integrated with flotation pre-concentration steps is generating incremental xanthate consumption at European urban mining operations and industrial residue processing facilities whose reagent requirements were not captured in historical xanthate demand accounting frameworks. The European Green Deal industrial transformation objectives, which target significant increases in domestic critical mineral processing and refining capacity as part of the strategic autonomy agenda, are supporting capital investment approvals for smelter capacity expansion and modernization projects at existing European metallurgical facilities that will increase the total sulfide concentrate processing throughput available to consume xanthate-beneficiated ore products, sustaining the mine-to-smelter demand pull for froth flotation reagent consumption at the upstream mining operation level through the forecast period.

Regulatory Pressure and Sustainability Requirements Driving Adoption of High-Performance Specialty Xanthate Formulations with Improved Selectivity and Reduced Environmental Footprint The progressive tightening of European Union and member state environmental regulations governing reagent discharge in mine process water, tailings facility management standards, and water body protection requirements applicable to mining operations is incentivizing European mine operators to adopt high-selectivity xanthate formulations and optimized collector dosing technologies that minimize xanthate residual concentrations in flotation tailings streams and process water recycling circuits, creating a product upgrade demand dynamic that increases per-unit revenue and technical differentiation value for specialty xanthate formulators relative to commodity-grade reagent suppliers. Mine operators with formal environmental management systems certified to ISO 14001 standards and subject to environmental permit conditions regulating reagent usage and discharge are increasingly specifying low-dosage, high-efficiency xanthate collector systems with documented biodegradation profiles and reduced ecotoxicity characteristics over generic xanthate formulations, generating procurement preference for technically differentiated products that command price premiums of 15% to 35% above commodity xanthate pricing and support higher-margin commercial relationships for specialty reagent manufacturers. The corporate ESG disclosure requirements applicable to European publicly listed mining companies, including Taxonomy Regulation alignment reporting and forthcoming Corporate Sustainability Reporting Directive disclosures covering supply chain chemical management practices, are driving environmental due diligence into xanthate procurement decisions and incentivizing investment in safer, more environmentally optimized reagent programs whose performance characteristics and environmental profiles are comprehensively documented and independently verified.

Key Challenges

Carbon Disulfide Feedstock Supply Concentration, Occupational Health Hazard Profile, and Tightening Industrial Emission Standards Constraining European Xanthate Manufacturing Economics The synthesis of all commercial xanthate compounds requires carbon disulfide as the primary sulfur-source feedstock, and the geographic concentration of European carbon disulfide production capacity among a limited number of chemical facilities in Germany, France, and the Czech Republic creates a supply security vulnerability for European xanthate manufacturers whose production economics are materially sensitive to carbon disulfide price movements, availability constraints generated by maintenance outages at concentrated production facilities, and the progressive regulatory pressure under the European Union’s industrial emissions framework that is increasing operating cost and capital investment requirements for carbon disulfide production and handling installations subject to Best Available Techniques Reference Document compliance obligations. Carbon disulfide is classified as a highly flammable, toxic, and environmentally hazardous substance under European chemicals regulations, requiring extensive engineering controls, enclosed handling infrastructure, continuous atmospheric monitoring, and emergency response systems at manufacturing facilities whose capital and operating cost burden disadvantages European xanthate producers relative to manufacturers in less stringently regulated production geographies. The European Union Industrial Emissions Directive revision and associated Best Available Techniques Reference Document updates are imposing more stringent carbon disulfide emission limit values and monitoring requirements on chemical manufacturing installations that will require capital investment in abatement technology upgrades at xanthate production facilities, adding fixed cost to European manufacturing operations already competing against lower-cost imported xanthate products from Chinese producers operating under less demanding regulatory compliance frameworks.

Substitution Pressure from Alternative Flotation Collector Chemistries and Process Technology Innovations Targeting Reduced Reagent Dependency in Mineral Processing Operations The mineral processing industry’s sustained research investment in alternative collector chemistries including thionocarbamates, dithiophosphates, dithiophosphinates, and hydroxamic acids is generating a portfolio of selective collector reagents capable of matching or exceeding xanthate performance in specific ore mineralogy and flotation circuit configurations, creating substitution pressure in application segments where xanthate performance limitations, environmental persistence concerns, or reagent toxicity considerations provide motivation for mine operators to evaluate alternative collector systems. Thionocarbamate collectors have achieved commercial adoption at several European copper and nickel flotation operations where their superior selectivity against pyrite gangue minerals reduces locked-cycle xanthate consumption requirements and improves concentrate grade specifications relative to equivalent xanthate-only collector programs, demonstrating that technically motivated substitution of xanthate collectors is commercially feasible and is being actively pursued by mine metallurgists seeking incremental process performance improvements. Column flotation technology advances, sensor-based froth characterization systems, and machine learning-assisted reagent dosing optimization tools being adopted at modernized European flotation plants are improving mineral recovery efficiency and enabling more precise collector dosing control that reduces overall xanthate consumption per metric ton of ore processed, creating a structural consumption efficiency improvement trend that partially offsets the volume growth contribution from new mine production additions within the European xanthate demand projection.

European Mining Permitting Delays, Social License Constraints, and Investment Uncertainty Moderating the Pace of New Mine Development That Would Expand the Regional Xanthate Demand Base Despite the policy intent of the European Critical Raw Materials Act to accelerate mine development timelines, European mining projects continue to encounter protracted environmental impact assessment processes, multi-jurisdictional regulatory coordination requirements, and community opposition dynamics that extend pre-production development periods well beyond the target timelines established under the accelerated permitting framework, creating uncertainty in the timing and magnitude of incremental xanthate demand additions from new mine commissioning events across the forecast period. Environmental non-governmental organization opposition to new mining operations in ecologically sensitive European landscapes, social license challenges in mining-adjacent communities, and political sensitivity surrounding water use, tailings facility siting, and landscape disturbance associated with large-scale open-pit and underground mining development projects have contributed to the cancellation, suspension, or indefinite delay of several announced European critical mineral projects whose xanthate demand contributions were anticipated in regional market demand projections. The cyclical dynamics of base metal commodity prices, particularly copper and zinc, create investment confidence volatility for European mine developers whose project financing feasibility assessments are sensitive to long-run metal price assumptions, with periods of metal price weakness reducing the economic returns of marginal European deposits whose higher capital and operating cost structures relative to South American and African peer projects require sustained metal price levels to support financing and construction investment decisions.

Market Segmentation

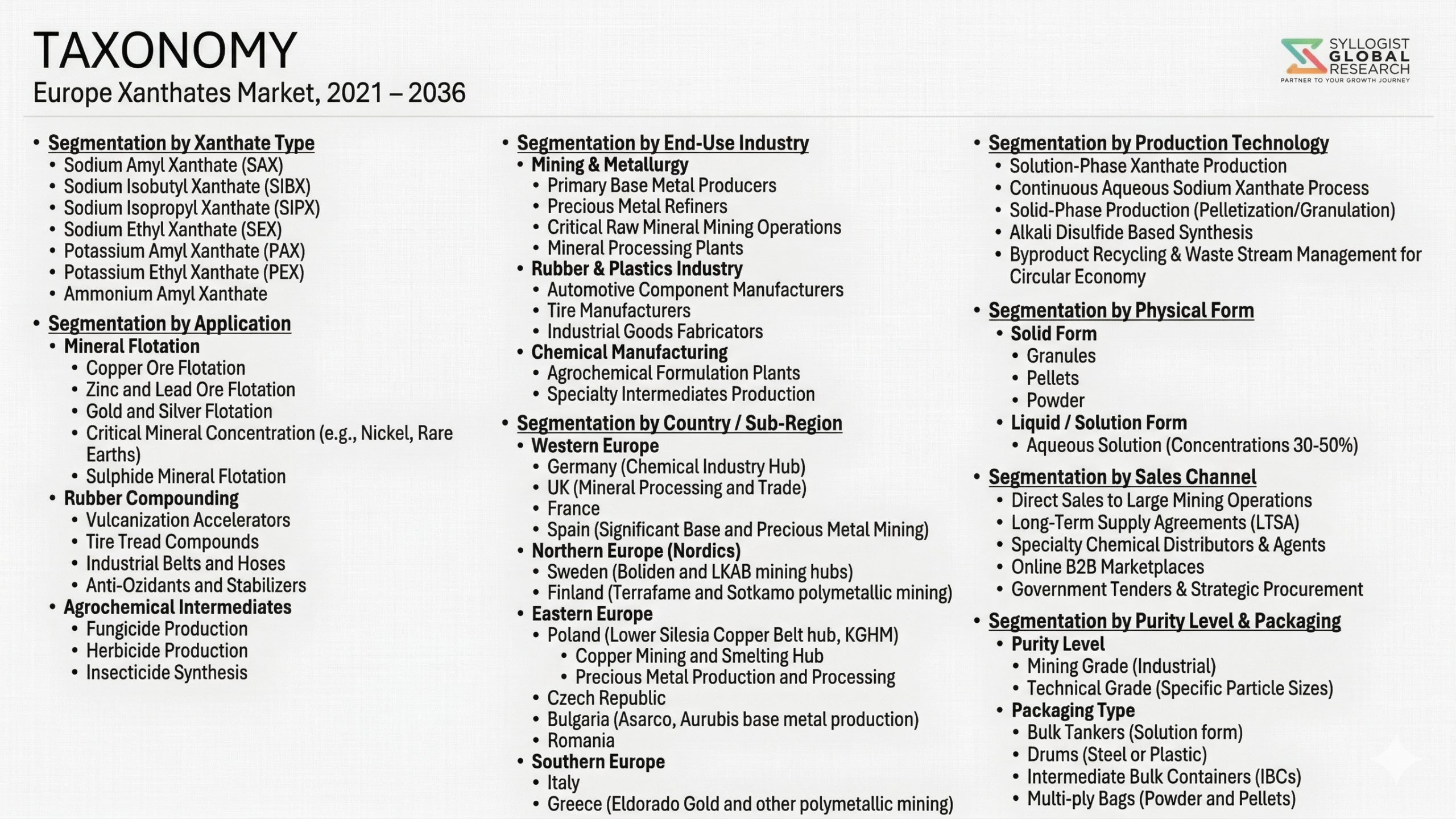

- Segmentation By Product Type

- Potassium Ethyl Xanthate (KEX)

- Sodium Ethyl Xanthate (SEX)

- Sodium Isobutyl Xanthate (SIBX)

- Potassium Amyl Xanthate (PAX)

- Sodium Isopropyl Xanthate (SIPX)

- Zinc Ethyl Xanthate and Zinc Isopropyl Xanthate (Rubber Grade)

- Others

- Segmentation By Physical Form

- Powder and Granule Xanthates

- Pellet Xanthates

- Aqueous Solution Xanthates

- Others

- Segmentation By Application

- Froth Flotation Mineral Processing (Sulfide Ore Collector)

- Rubber Vulcanization Accelerator

- Agrochemical Intermediate (Dithiocarbamate Synthesis)

- Viscose Rayon and Cellulose Fiber Processing

- Others

- Segmentation By Ore Type (Flotation Application)

- Copper Sulfide Ores

- Zinc and Lead Sulfide Ores

- Nickel and Cobalt Sulfide Ores

- Polymetallic and Complex Sulfide Ores

- Precious Metal-Bearing Sulfide Ores

- Others

- Segmentation By End User Industry

- Mining and Mineral Processing Companies

- Rubber and Elastomer Manufacturers

- Agrochemical and Crop Protection Manufacturers

- Textile and Specialty Fiber Producers

- Others

- Segmentation By Sales Channel

- Direct Supply to Mine Operators under Long-Term Reagent Agreements

- Specialty Mining Chemicals Distributor Channel

- Reagent Blending and Formulation Intermediary

- Spot Market and Short-Term Contract Supply

- Others

- Segmentation By Country

- Germany

- Sweden

- Finland

- Norway

- Poland

- Spain

- France

- Belgium

- Serbia and Balkans

- Rest of Europe

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total European market valuation of the Xanthates Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by product type, physical form, application, ore type served in flotation, end user industry, sales channel, and country, to enable xanthate producers, mining reagent distributors, mine operators, rubber compounders, and investors to identify which product segments and geographic markets will generate the highest absolute revenue and the most durable demand growth trajectory across the forecast period?

- How is the European Critical Raw Materials Act and associated national critical mineral development policy architecture expected to accelerate new sulfide ore mining project commissioning across Finland, Sweden, Spain, Serbia, and other European mining jurisdictions between 2027 and 2034, what is the estimated cumulative incremental annual xanthate collector demand attributable to these new mine production additions, and which specific project developments represent the largest individual demand contribution events in the context of regional xanthate market volume projections?

- What is the competitive positioning and market share structure of European xanthate manufacturers relative to Chinese import suppliers in the European market in 2025, how are European producers differentiating through technical service, product specification, REACH compliance infrastructure, and specialty formulation capability to defend market share against lower-cost imports, and what is the projected evolution of the European producer versus import supply balance across the forecast period as Chinese producers continue to invest in REACH compliance and European market access infrastructure?

- How are tightening European Union environmental regulations governing carbon disulfide emissions, process water discharge standards for mining operations, and industrial chemicals hazard management requirements affecting the operating cost structures, capital expenditure obligations, and competitive economics of European xanthate manufacturers relative to non-European producers, and what regulatory compliance cost differential between European and non-European production geographies is estimated for the 2025 to 2034 period under current and anticipated regulatory trajectories?

- What is the current and projected market penetration of alternative flotation collector chemistries including thionocarbamates, dithiophosphates, and dithiophosphinates as substitutes for xanthate collectors across specific European mine operator flotation circuits, at what ore mineralogy conditions and metallurgical performance thresholds does substitution become technically and economically justified, and what proportion of current European xanthate consumption volume is realistically addressable by alternative collector systems within the forecast period to 2034?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Sub-Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Carbon Disulphide (CS2) Feedstock Supply Concentration, Price Volatility & Logistical Risk

- Regulatory Tightening on Xanthate Handling, Effluent Discharge & Hazardous Substance Classification Risk

- Mining Activity Cyclicality, European Metal Production Decline & Flotation Reagent Demand Volatility Risk

- Substitution Risk from Alternative Flotation Collectors: Thionocarbamates, Dithiophosphates & Xanthogen Formates

- Import Competition, Dumping & Price Pressure from Low-Cost Asian Xanthate Producers

- Regulatory Framework & Standards

- REACH Regulation (EC 1907/2006): Xanthate Registration, Substance Evaluation, Authorisation & Restriction for Potassium and Sodium Xanthate Compounds Used in Mining & Industrial Applications

- CLP Regulation (EC 1272/2008): Xanthate Classification, Labelling & Packaging as Flammable Solid, Acute Toxicity & Aquatic Hazard and SDS Requirements under GHS Alignment

- Industrial Emissions Directive (IED 2010/75/EU) & Best Available Technique (BAT): Xanthate Manufacturing Plant Emission Limit, Effluent Treatment & CS2 Vapour Recovery Standards

- Water Framework Directive (2000/60/EC) & Mining Effluent Regulation: Xanthate Residue in Process Water Discharge, Aquatic Toxicity Limit & BREF for Non-Ferrous Metal Mining Flotation Reagent Management

- EU SVHC & Hazardous Chemicals Policy: Carbon Disulphide (CS2) SVHC Candidate Listing, Workplace Exposure Limit under Directive 2017/164/EU & National Transpositions Across EU Member States

- Europe Xanthates Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Metric Tonnes)

- Market Size & Forecast by Product Type

- Potassium Amyl Xanthate (PAX)

- Potassium Isobutyl Xanthate (PIBX)

- Potassium Ethyl Xanthate (PEX)

- Potassium Isopropyl Xanthate (PIPX)

- Sodium Isobutyl Xanthate (SIBX)

- Sodium Ethyl Xanthate (SEX)

- Sodium Isopropyl Xanthate (SIPX)

- Other Specialty & Custom Xanthate Compounds

- Market Size & Forecast by Physical Form

- Powder & Free-Flowing Granule

- Pellet & Briquette (Dust-Reduced, Safer-Handling Form)

- Aqueous Solution & Liquid Formulation

- Market Size & Forecast by Purity Grade

- High Purity Grade (Above 95%)

- Technical Grade (90% to 95%)

- Custom Blend & Proprietary Formulation Grade

- Market Size & Forecast by Application

- Mining & Mineral Processing: Froth Flotation Collector for Sulphide Ore

- Rubber & Polymer Industry: Vulcanisation Accelerator & Dithiocarbamate Intermediate

- Agriculture: Herbicide, Fungicide & Soil Treatment Active Ingredient

- Organic Synthesis & Pharmaceutical Chemical Intermediate

- Other Industrial & Specialty Chemical Application

- Market Size & Forecast by Mineral Type (Mining Application)

- Copper & Copper-Molybdenum Sulphide Ore Flotation

- Lead-Zinc & Galena-Sphalerite Ore Flotation

- Gold & Silver (Sulphide Carrier) Ore Flotation

- Nickel, Cobalt & PGM Sulphide Ore Flotation

- Pyrite, Iron Sulphide & Polymetallic Ore Flotation

- Market Size & Forecast by End-User

- Metal Mining & Ore Processing Company (European Mine Site & Concentrator)

- Rubber, Polymer & Specialty Chemical Manufacturer

- Agricultural Chemical & Crop Protection Company

- Chemical Distributor, Trading Company & Mine Reagent Supplier

- Contract Research Organisation & Specialty Chemical Laboratory

- Market Size & Forecast by Sales Channel

- Direct Long-Term Supply Agreement to Mine Site & Mineral Processing Plant

- Specialty Chemical Distributor & Mining Reagent Supplier Network

- Toll Manufacturing, Custom Synthesis & Private Label

- Online B2B Chemical Trading Platform & Spot Market

- Western Europe Xanthates Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Product Type

- By Physical Form

- By Purity Grade

- By Application

- By Mineral Type (Mining Application)

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Northern Europe Xanthates Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Product Type

- By Physical Form

- By Purity Grade

- By Application

- By Mineral Type (Mining Application)

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Eastern Europe Xanthates Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Product Type

- By Physical Form

- By Purity Grade

- By Application

- By Mineral Type (Mining Application)

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Southern Europe Xanthates Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Product Type

- By Physical Form

- By Purity Grade

- By Application

- By Mineral Type (Mining Application)

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- UK & Ireland Xanthates Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Product Type

- By Physical Form

- By Purity Grade

- By Application

- By Mineral Type (Mining Application)

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Europe Xanthates Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Product Type

- By Physical Form

- By Purity Grade

- By Application

- By Mineral Type (Mining Application)

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

*Countries Analyzed in the Syllogist Europe Research Portfolio: Germany, France, Netherlands, Belgium, Switzerland, Austria, Sweden, Norway, Finland, Denmark, Poland, Czech Republic, Slovakia, Romania, Bulgaria, Hungary, Spain, Portugal, Italy, Greece, United Kingdom, Ireland, Serbia

- Technology Landscape & Innovation Analysis

- Xanthate Synthesis Technology Deep-Dive: CS2 plus ROH plus KOH/NaOH Reaction Mechanism, Continuous vs. Batch Process Design, Reactor Configuration & Yield Optimisation

- Xanthate Pelletisation, Compaction & Dust-Reduced Solid Form Production Technology for Safer Mine Site Handling

- Xanthate Liquid Solution Formulation, Stabilisation & Direct Feed Technology for Automated Flotation Reagent Dosing

- Flotation Chemistry & Xanthate Collector Mechanism: Chemisorption on Sulphide Mineral Surface, Selectivity Control & pH-Dependent Performance

- Xanthate Effluent Decomposition, Wastewater Treatment & Cyanide-Xanthate Combined Effluent Management Technology

- Next-Generation Collector Technology: Thionocarbamates, Dithiophosphates, Xanthogen Formates & Mixed Collector Blends as Xanthate Supplement or Replacement

- Digital Reagent Dosing, Automated Flotation Control, AI-Based Reagent Optimisation & Online Xanthate Analyser Technology

- Patent & IP Landscape in Xanthate Production & Flotation Reagent Technologies Relevant to Europe

- Value Chain & Supply Chain Analysis

- Raw Material Supply Chain: Carbon Disulphide (CS2), Potassium Hydroxide (KOH), Sodium Hydroxide (NaOH) & Alcohol (Amyl, Isobutyl, Ethyl, Isopropyl) Sourcing in Europe

- Xanthate Manufacturer & Production Facility Landscape: European Domestic Producer vs. Import (China, Russia, South Africa) Channel

- Specialty Chemical Distributor, Mining Reagent Supplier & Pan-European Distribution Network

- Mine Site & Mineral Processing Plant Integration: Reagent Storage, Dosing Equipment & On-Site Technical Service

- Industrial & Agricultural Chemical End-User Supply & Application Channel

- Import & Re-Export: Rotterdam & Hamburg Hub Chemical Trading & Distribution

- Xanthate Waste & Effluent Management, Decomposition Treatment & Environmental Compliance Service

- Pricing Analysis

- Europe Xanthate Average Selling Price (ASP) Analysis by Product Type (PAX, PIBX, PEX, SIBX) & Physical Form (Powder, Pellet, Solution)

- European Domestic Production Cost vs. Import Price (China-Origin, FOB & CIF Hamburg) Comparison by Xanthate Type

- Xanthate Price Sensitivity to CS2 Feedstock Cost, KOH/NaOH Caustic Price & Energy Cost in European Manufacturing

- High Purity vs. Technical Grade Xanthate Price Premium Analysis by Application Segment

- Pellet & Liquid Solution Form Price Premium vs. Standard Powder: Handling, Safety & Convenience Value Analysis

- Xanthate Price Trend Forecast (2025-2034): Supply-Demand Balance, Import Competition & Regulatory Cost Impact on European Market Pricing

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Xanthate Production: Carbon Footprint, CS2 Emission, Energy Intensity & Water Use per Tonne of Xanthate Manufactured

- Xanthate Aquatic Toxicity, Biodegradability & Environmental Fate in Mining Process Water & Tailings Dam Effluent

- Xanthate Effluent Treatment Technology & Compliance with EU Water Framework Directive: Chemical Oxidation, UV Decomposition & Biological Degradation Performance

- Safer Handling Innovation: Pelletisation, Dust Suppression & Liquid Form Environmental & Worker Safety Benefit vs. Powder Xanthate

- Regulatory-Driven Sustainability: REACH SVHC Pressure on CS2, CLP Aquatic Hazard Classification, EU Green Deal Critical Raw Material Mining Reagent Policy & Responsible Mining Certification

- Competitive Landscape

- Market Structure & Concentration

- Europe Xanthates Market Consolidation Level (Fragmented vs. Concentrated by Product Type & Application)

- Top 10 Players Market Share by Volume & Revenue

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Product Type, Application & Sub-Region

- Player Classification

- European Domestic Xanthate Manufacturer & Producer

- Global Mining Chemicals Company with European Xanthate Portfolio (Nouryon, Solvay, Clariant)

- Asian Xanthate Importer & European Distributor (China & South Africa-Origin Supply)

- Specialty Chemical Distributor & Mining Reagent Supplier Active in Europe

- Flotation Reagent Technology Company with Xanthate & Alternative Collector Portfolio

- Integrated Mining Chemical Supplier Serving European Mine Sites

- Toll Manufacturer & Custom Synthesis Provider for Specialty Xanthate Grade

- Rubber & Agricultural Chemical Company Using Xanthate as Industrial Intermediate

- Competitive Analysis Frameworks

- Market Share Analysis by Product Type, Application & Sub-Region

- Company Profile

- Company Overview & Headquarters

- Xanthate Products & Portfolio (Grade, Form & Application Coverage)

- Key Customer Relationships & Reference Mine Site Supply Agreements

- Manufacturing Footprint & Annual Production Capacity (Metric Tonnes)

- Revenue (Xanthate & Mining Chemicals Segment) & Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Capacity Expansion, Product Launches, Regulatory Approvals)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Product Breadth vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Product Type, Physical Form, Application, Mineral Type & Sub-Region

- White Space Opportunity Analysis

- Strategic Output

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Sub-Regional Localisation Strategy

- Customer & Mine Site Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Regulatory Compliance Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)